|

시장보고서

상품코드

1846314

재분산성 폴리머 분말 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Redispersible Polymer Powder - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

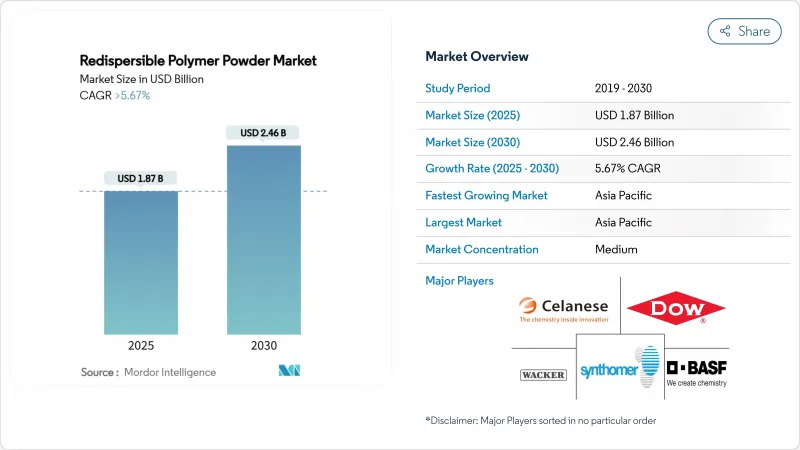

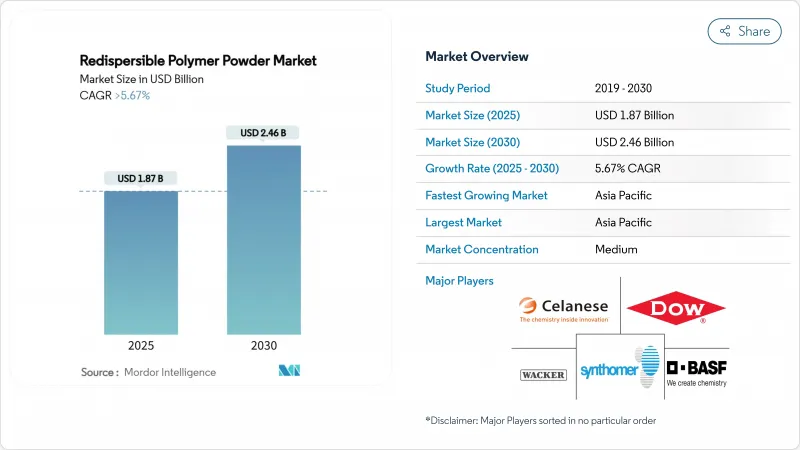

재분산성 폴리머 분말 시장 규모는 2025년에 18억 7,000만 달러로 추정되고, 예측 기간(2025-2030년) CAGR 5.67%로 성장할 전망이며, 2030년에는 24억 6,000만 달러에 이를 것으로 예측됩니다.

정책 입안자가 내구성이 높고 에너지 절약 건물을 추진하는 가운데 고성능의 드라이 모르타르 첨가제에 대한 수요가 높아지고 있습니다. 신흥국의 인프라 지출 확대가 강력한 수량 기준이 되는 반면, 유럽과 북미의 리노베이션 계획은 낮은 VOC 및 바이오 등급으로 제품 혁신을 지향합니다. 2024년 이후 휘발성 비닐 아세테이트 단량체 가격은 마진을 압박하지만, 주요 업체에 의한 수직 통합이 공급을 안정시킵니다. 분무 건조 기술 향상과 3D 프린팅 콘크리트용으로 조정된 폴리머 파우더가 재분산성 폴리머 분말 시장의 실용 범위를 확대하고 있습니다.

세계의 재분산성 폴리머 분말 시장 동향 및 인사이트

신흥국의 건설 붐

중국의 탄소 중립 계획 및 인도의 주택 건설 촉진이 아시아태평양의 소비량의 60% 이상을 차지하고 있으며, 아시아태평양의 인프라 확대가 장기적인 성장을 지원하고 있습니다. 바스프는 담강 바밴드 공장에 100억 달러를 할당하여 신재생 에너지로 건설용 폴리머 생산을 확보했습니다. 인도의 건설용 화학제품 매출은 2025년 20,000캐롤 루피에 이르렀으며, Master Builders Solutions는 2028년까지 500캐롤 루피의 매출 목표를 설정했습니다. 사우디아라비아의 NEOM 프로젝트에서는 로봇 건축에 13억 SAR의 예산이 계상되어 자동 조립에 대응할 수 있는 특수 바인더가 선호되고 있는 것이 부각되었습니다. 이러한 다년간의 공공 프로그램은 재분산성 폴리머 분말 시장이 일상적인 주거 주기를 넘어서는 가시성을 보장합니다.

레디믹스 드라이 모르타르 시스템으로의 급속한 전환

공장에서 생산되는 모르타르는 현장 노동력을 줄이고 혼합 변동을 최소화하기 위해 전통적인 배치 처리에서 표준화된 배합으로의 전환이 세계 가속화되고 있습니다. 독일과 프랑스의 조기 채용은 세계 공통의 품질 기준에 대한 경로를 입증했으며 미국의 대도시 지역에서도 비슷한 정책적 움직임이 나오고 있습니다. 와커는 자동 사일로 및 펌프용으로 설계된 바이오밸런스형 VAE 분말을 공급하는 VINNAPAS eco 시리즈를 발표했습니다. 레디믹스의 성장은 투여 정밀도를 향상시키고 계약자는 더 엄격한 타일 접착제의 전단 강도 요구 사항을 충족시킬 수 있습니다. 숙련 노동자 부족이 심각해짐에 따라, 자동 투여는 비용 회피 전략이 되어 재분산성 폴리머 분말 시장을 더욱 확대할 것입니다.

비닐 아세테이트 단량체 및 에틸렌 가격의 난고하

2024년 이후의 원료 상승으로 BASF와 Celanese는 여러 아세테이트 유도체의 가격 인상을 강요했습니다. 세라니즈는 텍사스 주 130만 톤의 아세트산 장치 및 난징의 70kt VAE 디보틀넥으로 대응해 스케일 메리트를 획득했습니다. 후방 통합된 대규모 그룹은 위험을 헤지하고 있지만 장기 계약이 없는 소규모 기업은 마진 압축에 직면하고 있으며 재분산성 폴리머 분말 산업 내 통합이 가속화되고 있습니다.

부문 분석

VAE는 비용 경쟁력이 있어 타일 접착제, 렌더, 셀프 라벨링 컴파운드 등 폭넓은 용도로 사용할 수 있기 때문에 2024년 재분산성 폴리머 분말 시장 점유율의 47.18%를 차지했습니다. 수요 집중은 현재 가격 주도권을 지원하는 규모의 경제를 가능하게 합니다. 그러나 고급 건축 공사 증가로 CAGR 6.21%로 성장하는 VAE-VeoVa 등급의 채용이 가속화되고 있습니다. VAE-VeoVa는 내 알칼리성과 유연성이 기후 스트레스 하에서 중요한 외부 단열 시스템에 선호됩니다. 아크릴 파우더는 자외선에 노출된 외관에서 틈새를 유지하며 에틸렌-염화비닐 블렌드는 화학적 내구성이 필요한 산업용 페인트에 사용됩니다.

성장 전망은 스프레이 건조의 안정성을 유지하는 생산자의 능력에 달려 있습니다. 와커의 신재생 자원 기반 제품군은 전단 강도를 낮추지 않고 탄소 발자국을 줄이는 것을 목표로 하고 있습니다. 세라니즈사는 지속가능성의 증명가능한 주장을 요구하는 건설업자에 대응하기 위해 바이오함량을 증명한 비닐아세테이트 ECO-B를 데뷔시켰습니다. 이와 같이 재분산성 폴리머 분말 시장은 VAE의 수량 확보와 특수 아형의 마진 성장이라는 두 가지 기세를 보이고 있습니다.

지역 분석

아시아태평양은 재분산성 폴리머 분말 시장을 독점하고, 2024년에는 세계 판매량의 45.28%를 차지하였으며, CAGR은 가장 빠른 5.97%로 성장할 전망입니다. 철도, 고속도로, 저렴한 주택 프로젝트에 대한 정부의 경기 자극책이 기준선 사용량을 증가시키고 중국의 탄소 중립 목표가 환경 인증 폴리머 등급을 뒷받침하고 있습니다. Seaka가 중국과 인도네시아에 쌍둥이 공장을 건설했듯이 생산 능력을 현지화하는 제조업체는 공급의 신뢰성을 보장하면서 통관과 운임면에서의 이점을 확보할 수 있습니다. 그 결과 세계 수요가 이 지역에 구조적으로 기울어지게 됩니다.

북미와 유럽은 엄격한 에너지 성능 규제 및 대규모 리노베이션 주식으로 점유율을 유지하고 있습니다. 미국 DOE의 2억 4,000만 달러의 보조금 풀은 각 국가의 첨단 법규 규정 채택을 촉진하고 건축업자를 열교의 발생을 억제하는 폴리머 솔루션으로 유도합니다. 구체화 탄소 보고서에 관한 EU 지침은 바이오 VAE-VeoVa 파우더의 채택을 가속화합니다. 양 지역의 성숙한 유통망은 커스터마이즈된 그레이드의 저스트 인 타임 납품을 가능하게 하고 있어 절대적인 성장률은 아시아태평양을 벗어나는 것, 견조한 마진의 요인이 되고 있습니다.

남미와 중동 및 아프리카는 거대 도시가 수송 회랑을 정비하고 해안 인프라를 기후 변화에 견딜 수 있게 함으로써 성장의 한 축을 담당하게 됩니다. 사우디아라비아의 13억 SAR 로봇 공학을 기반으로 한 NEOM 계획은 고내구성 바인더에 유리한 조달 프로토콜을 설정합니다. 브라질은 인프라 자극책을 하수도와 도로 개수에 돌려 보수 모르타르에 대한 폴리머 수요에 박차를 가하고 있습니다. 현지 공급 부족은 국산 원료를 활용하면서 기술을 이전하는 세계 기업과의 합작투자를 유치하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 신흥국 건설 붐

- 레디믹스 및 드라이 모르타르 시스템으로의 급속한 이행

- 고성능 타일용 접착제에 대한 리폼 수요

- 정부의 에너지 절약 건축 기준

- 재분산성 폴리머 바인더를 채용한 3D 프린팅 콘크리트 제제

- 시장 성장 억제요인

- 비닐 아세테이트 단량체 및 에틸렌의 가격 변동

- 일관된 스프레이 건조 품질을 달성하기 위한 기술적 복잡성

- 보호 콜로이드의 VOC 규제 강화

- 밸류체인 분석

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁도

제5장 시장 규모 및 성장 예측

- 유형별

- 아세트산비닐-에틸렌(VAE)

- 아세트산비닐 및 버사틱산비닐에스테르(VAE-VeoVa)

- 아크릴 분말

- 기타 유형(에틸렌-염화비닐, 스티렌-부타디엔 등)

- 용도별

- 석고 및 렌더

- 타일용 접착제

- 그라우트

- 모르타르 첨가제

- 기타 용도(외단열 복합 시스템(ETICS) 등)

- 최종 사용자 산업별

- 주택

- 상업

- 산업 및 시설

- 인프라

- 지역별

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- ASEAN 국가

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장의 집중도

- 전략적인 동향

- 시장 점유율(%) 및 분석

- 기업 프로파일

- Acquos

- ADA FINE CHEMICALS CO.,LTD

- Anhui Elite Industrial Co.,ltd

- Ashland

- BASF SE

- Bosson Union Tech(Beijing) Co.,Ltd

- Celanese Corporation

- Celotech Chemical Co., Ltd.

- DCC(Dairen Chemical Corporation)

- Dezhou Tengda Construction New Materials Co., Ltd.

- Dow Inc.

- Hebei Derek Chemical Limited

- Hexion Inc.

- JSC Pigment

- Organik Kimya.

- Oscrete Construction Products

- Sakshi Chem Sciences Pvt. Ltd.

- SIDLEY CHEMICAL CO.,LTD.

- Synthomer plc

- Vinavil SpA

- Wacker Chemie AG

제7장 시장 기회 및 전망

AJY 25.11.10The Redispersible Polymer Powder Market size is estimated at USD 1.87 billion in 2025, and is expected to reach USD 2.46 billion by 2030, at a CAGR of greater than 5.67% during the forecast period (2025-2030).

A steady preference for high-performance dry-mortar additives is raising demand as policymakers push for durable and energy-efficient buildings. Expanding infrastructure spending across emerging economies adds a strong volume base, while renovation programs in Europe and North America redirect product innovation toward low-VOC and bio-based grades. Volatile vinyl acetate monomer prices after 2024 compressed margins, yet vertical integration by leading producers helped to stabilize supply. Technology upgrades in spray-drying, along with polymer powders tailored for 3D-printed concrete, are widening the practical scope of the redispersible polymer powder market.

Global Redispersible Polymer Powder Market Trends and Insights

Construction Boom in Emerging Economies

Infrastructure expansion in Asia-Pacific underpins long-term growth as China's carbon-neutrality roadmap and India's housing drive collectively deliver more than 60% of regional consumption. BASF allocated USD 10 billion to its Zhanjiang Verbund site, ensuring renewable-powered production of construction polymers. India's construction chemicals revenue touched INR 20,000 crore in 2025, and Master Builders Solutions set a turnover target of INR 500 crore by 2028. Saudi Arabia's NEOM project earmarked SAR 1.3 billion for robotics-enabled building, which highlights a preference for specialty binders capable of supporting automated assembly. Such multi-year public programs guarantee visibility for the redispersible polymer powder market far beyond routine housing cycles.

Rapid Shift to Ready-Mix Dry-Mortar Systems

Factory-produced mortars cut job-site labor and minimize mixing inconsistencies, accelerating the worldwide transition from traditional batching to standardized formulations. Early adoption in Germany and France has proven the pathway for universal quality standards, and similar policy moves emerge in large U.S. metropolitan areas. Wacker introduced its VINNAPAS eco range to deliver bio-balanced VAE powders designed for automated silos and pumps. Ready-mix growth improves dosing accuracy, allowing contractors to meet stricter tile adhesive shear strength requirements. As skilled labor shortages worsen, automated dosing becomes a cost-avoidance strategy that further enlarges the redispersible polymer powder market.

Volatility in Vinyl-Acetate Monomer and Ethylene Prices

Feedstock spikes since 2024 forced BASF and Celanese to raise prices for several acetate derivatives. Celanese responded with a 1.3 million-ton acetic-acid unit in Texas and a 70 kt VAE debottleneck in Nanjing to capture scale economies. Larger groups with backward integration hedge risks, yet small firms lacking long-term contracts face margin compression, amplifying consolidation inside the redispersible polymer powder industry.

Other drivers and restraints analyzed in the detailed report include:

- Renovation-Led Demand for High-Performance Tile Adhesives

- Government Energy-Efficient Building Codes

- Stricter VOC Limits on Protective Colloids

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

VAE controlled 47.18% of redispersible polymer powder market share in 2024 owing to its competitive cost and broad utility across tile adhesives, renders, and self-leveling compounds . Demand concentration allows economies of scale that underpin current price leadership. An uptick in premium construction jobs, however, is accelerating the adoption of VAE-VeoVa grades that grow at a 6.21% CAGR. Formulators prefer VAE-VeoVa for exterior insulation systems where alkaline resistance and flexibility are critical under climate stress. Acrylic powders sustain a niche in UV-exposed facades, whereas ethylene-vinyl-chloride blends serve industrial coatings that need chemical endurance.

Growth prospects hinge on producers' capacity to maintain steady spray-drying consistency. Wacker's renewable resource-based range targets carbon-footprint reductions without dampening shear strength. Celanese debuted Vinyl Acetate ECO-B with certified bio-content, catering to builders seeking verifiable sustainability claims. The redispersible polymer powder market thus shows dual momentum: volume security in VAE and margin growth in specialty subtypes.

The Redispersible Polymer Powder Market Report is Segmented by Type (Vinyl Acetate-Ethylene, Vinyl Acetate/Vinyl Ester of Versatic Acid, and More), Application (Plasters and Renders, Tile Adhesives, and More), End-User Industry (Residential, Commercial, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific dominates the redispersible polymer powder market, recording 45.28% of global volume in 2024 and sustaining the fastest 5.97% CAGR. Government stimulus for rail, highway, and affordable housing projects amplifies baseline usage, while Chinese carbon-neutral targets encourage eco-certified polymer grades. Producers that localize capacity, as Sika did with twin plants in China and Indonesia, secure customs and freight benefits while ensuring supply reliability. The result is a structural tilt in global demand toward the region.

North America and Europe preserve share through stringent energy-performance regulations and large renovation stock. The U.S. DOE grant pool of USD 240 million elevates state adoption of advanced codes and steers builders toward polymer solutions that cut thermal bridging. EU directives on embodied-carbon reporting accelerate adoption of bio-based VAE-VeoVa powders. Mature distribution networks in both regions enable just-in-time delivery of customized grades, which explains robust margins even though absolute growth trails Asia-Pacific.

South America and Middle-East and Africa add a growth flank as megacities overhaul transport corridors and climate-proof coastal infrastructure. Saudi Arabia's SAR 1.3 billion robotics-based NEOM agenda sets procurement protocols that favor high-durability binders. Brazil channels infrastructure stimulus toward sewer and road rehabilitation, spurring polymer demand in repair mortars. Local supply gaps invite joint ventures with global players that transfer technology while leveraging indigenous raw materials.

- Acquos

- ADA FINE CHEMICALS CO.,LTD

- Anhui Elite Industrial Co.,ltd

- Ashland

- BASF SE

- Bosson Union Tech(Beijing) Co.,Ltd

- Celanese Corporation

- Celotech Chemical Co., Ltd.

- DCC (Dairen Chemical Corporation)

- Dezhou Tengda Construction New Materials Co. , Ltd.

- Dow Inc.

- Hebei Derek Chemical Limited

- Hexion Inc.

- JSC Pigment

- Organik Kimya.

- Oscrete Construction Products

- Sakshi Chem Sciences Pvt. Ltd.

- SIDLEY CHEMICAL CO.,LTD.

- Synthomer plc

- Vinavil S.p.A.

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Construction Boom in Emerging Economies

- 4.2.2 Rapid Shift to Ready-Mix Dry-Mortar Systems

- 4.2.3 Renovation-Led Demand for High-Performance Tile Adhesives

- 4.2.4 Government Energy-Efficient Building Codes

- 4.2.5 3D-Printed Concrete Formulations Adopting Redispersible Polymer Binders

- 4.3 Market Restraints

- 4.3.1 Volatility Iin Vinyl-Acetate Monomer and Ethylene Prices

- 4.3.2 Technical Complexity in Achieving Consistent Spray-Dry Quality

- 4.3.3 Stricter VOC Limits on Protective Colloids

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Vinyl Acetate-Ethylene (VAE)

- 5.1.2 Vinyl Aceteate/Vinayl Ester of Versatic Acid (VAE-VeoVa)

- 5.1.3 Acrylic Powders

- 5.1.4 Other Types (Ethylene-Vinyl Chloride, Styrene-Butadiene, etc.)

- 5.2 By Application

- 5.2.1 Plasters and Renders

- 5.2.2 Tile Adhesives

- 5.2.3 Grouts

- 5.2.4 Mortar Additives

- 5.2.5 Other Applications (External Thermal Insulation Composite Systems (ETICS), etc.)

- 5.3 By End-user Industry

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial / Institutional

- 5.3.4 Infrastructure

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Analysis Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Acquos

- 6.4.2 ADA FINE CHEMICALS CO.,LTD

- 6.4.3 Anhui Elite Industrial Co.,ltd

- 6.4.4 Ashland

- 6.4.5 BASF SE

- 6.4.6 Bosson Union Tech(Beijing) Co.,Ltd

- 6.4.7 Celanese Corporation

- 6.4.8 Celotech Chemical Co., Ltd.

- 6.4.9 DCC (Dairen Chemical Corporation)

- 6.4.10 Dezhou Tengda Construction New Materials Co. , Ltd.

- 6.4.11 Dow Inc.

- 6.4.12 Hebei Derek Chemical Limited

- 6.4.13 Hexion Inc.

- 6.4.14 JSC Pigment

- 6.4.15 Organik Kimya.

- 6.4.16 Oscrete Construction Products

- 6.4.17 Sakshi Chem Sciences Pvt. Ltd.

- 6.4.18 SIDLEY CHEMICAL CO.,LTD.

- 6.4.19 Synthomer plc

- 6.4.20 Vinavil S.p.A.

- 6.4.21 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment