|

시장보고서

상품코드

1846339

면역조직화학 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Immunohistochemistry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

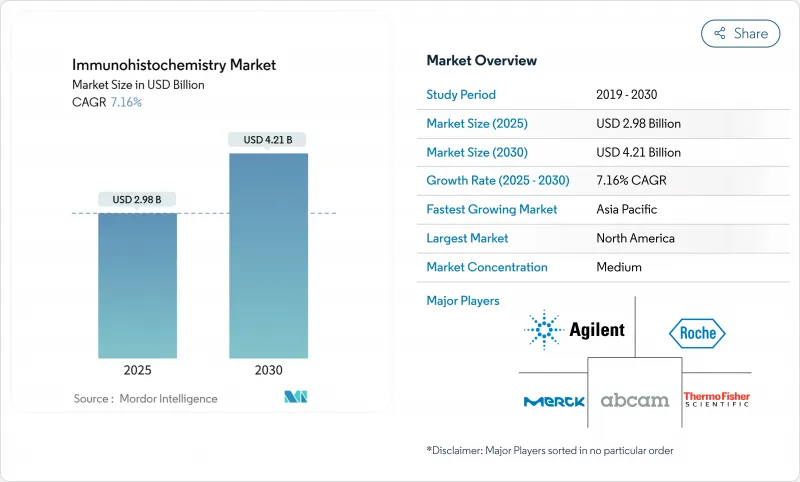

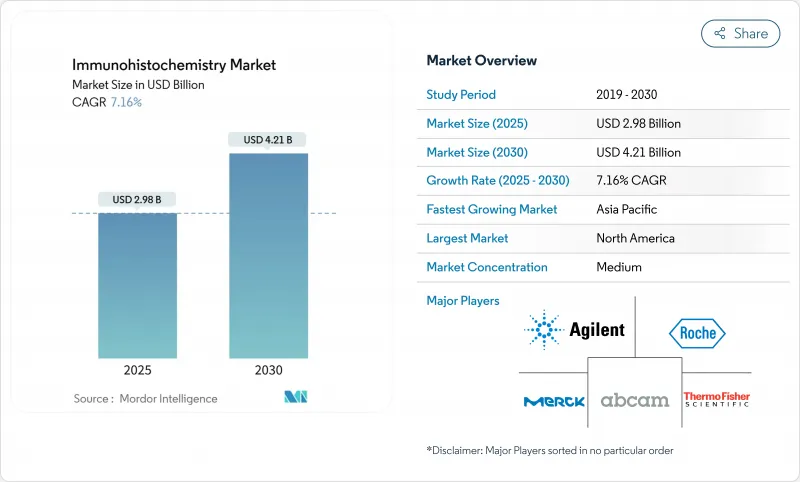

세계의 면역조직화학 시장은 2025년에 29억 8,000만 달러로 추정되고, 2030년에는 42억 1,000만 달러에 이를 것으로 예측되며, CAGR 7.16%로 성장할 전망입니다.

성장을 지지하고 있는 것은 암 이환율의 상승, 동반진단의 보급, 진단 정밀도를 향상시키면서 소요 시간을 단축하는 AI 대응 멀티플렉스 염색 워크플로우의 급속한 채용입니다. 디지털 병리학적 통합 증가, 중소득층 검사실에서의 자동 슬라이드 염색기의 보급, 창약 아웃소싱에 대한 투자 증가가 더욱 기세를 늘리고 있습니다. 동시에 FDA가 면역조직화학 검정을 의료기기로 재분류함에 따라 컴플라이언스 비용이 상승했지만 이미 세계 인증된 품질 시스템을 운영하고 있는 선두 업체들이 유리합니다. 지역적인 수요는 서서히 아시아태평양으로 이동하고 암 영역의 인프라 및 제조 능력의 확대가 미충족의 진단 요구를 보완합니다. 2024년 Danaher와 Abcam의 파트너십으로 대표되는 공급업체 간의 통합은 엔드 투 엔드 시약, 장비 및 소프트웨어 포트폴리오에 경쟁이 중점을 두고 있음을 시사합니다.

세계의 면역조직화학 시장 동향 및 인사이트

암의 유병률 상승

암 이환율의 급증은 단일 세포 해상도에서 종양 생물학을 밝히는 면역조직화학 검사에 대한 높은 수요를 지지하고 있습니다. 멀티플렉스 염색은 면역과 종양의 상호 작용을 밝히고 체크포인트 억제제 치료의 선택을 유도합니다. FDA는 HER2-ultralow 검사를 승인하고 Zanidatamab의 담도 적응은 견고한 HER2 염색에 의존합니다. 직접 면역형광 보충법에 의한 천포창 진단과 같은 희소암의 이용 사례는 면역조직화학 시장을 더욱 확대합니다.

고령화 인구 및 만성 질환 부담

평균 수명의 연장은 만성 질환의 병존을 증가시키고 기존의 병리 조직 검사 능력을 증가시키는 사례 수를 증가시킵니다. 인구 100만 명당 병리의의 수는 전 세계적으로 14명 이하이며, 일량 증가(많은 지역에서 연간 4,000 증례 이상)에 의해 자동화에 대한 의존이 높아지고 있습니다. 병원 검사실에서의 면역조직화학 검사 의뢰는 10년 전과 비교해 20% 증가하고 있지만, 자본적 제약으로부터 디지털 병리 검사를 도입하고 있는 임상 시설은 3분의 1에 불과합니다. 이 갭은 염색 강도와 스코어링을 표준화하고 질을 낮추지 않고 처리량을 향상시키는 AI 대응 슬라이드 스캐너의 채용을 가속화하고 있습니다.

프리미엄 항체 및 검출 키트의 고비용

시판되고 있는 항체의 3분의 2가 기본적인 특이성 테스트로 불합격이 되어, 실험실은 비용이 많이 드는 인하우스 밸리데이션을 실시할 수밖에 없게 되어, 1테스트 당의 지출이 부풀어오고 있습니다. 1,000개의 항체를 대상으로 한 YCharOS의 리뷰에 따르면, 재현성이 없는 항체의 손실은 미국에서만 연간 18억 달러에 달할 전망입니다. 모노클로날 치료제의 정가의 중앙값은 여전히 15,624-14만 3,833달러이며, 이는 공정 개선에도 불구하고 제조 규모의 한계를 반영합니다. 메디케어의 로컬 커버리지 의사결정(2024년 7월 이후 시행)에서는 면역조직화학 염색에 엄격한 의료 필요성의 문서화가 요구되고 확장 패널의 상환이 제한되고 있습니다.

부문 분석

항체는 2024년에도 면역조직화학 시장의 42.23%를 차지하며, 모든 분석에서 중요한 역할을 담당하고 있습니다. 그러나 소프트웨어는 여러 시설에서 알고리즘 전개를 가능하게 하는 클라우드 호스팅 이미지 분석으로의 전환과 함께 CAGR 8.02%로 발전하고 있습니다. navify Digital Pathology와 통합된 Roche의 VENTANA DP 200 슬라이드 스캐너는 염색에서 AI 스코어링까지의 원활한 경로를 보여줍니다. 항체 카테고리 자체도 진화하고 있습니다. 1차 모노클로날 클론은 밸리데이션의 투명성을 향상시키고, 멀티플렉스-대응 2차 항체는 낮은 존재량의 표적을 증폭시킵니다. 장치의 업그레이드는 이러한 시프트와 병행하여 이루어지며, 자동 염색기는 수작업으로 인한 실수를 줄이고 숙련된 노동력을 해석 작업으로 향하게 합니다. QuPath와 HistoQC와 같은 오픈소스 툴이 이미지 표준화를 개선함에 따라 중소득국의 실험실은 디지털 플랫폼을 더욱 빠르게 채택하여 면역조직화학 시장 전반에 걸친 소프트웨어의 전략적 중요성을 강화하고 있습니다.

키트 및 시약에서 동반진단 약물의 승인은 구매 의사 결정에 영향을 미칩니다. 슬라이드 스캐너와 조직 마이크로어레이는 고처리량의 변환 연구를 지원하기 위해 융합되어 있습니다. 제조업체는 FDA의 디바이스 재분류 규칙에 따른 컴플라이언스를 용이하게 하기 위해 품질 보증 시약 번들로 대응합니다. 이러한 상호작용을 통해 소프트웨어는 보조 도구에서 핵심 수익 기여자로 승격하고 면역조직화학 시장은 2030년까지 두 자릿수 성장을 이루게 됩니다.

2024년 면역조직화학 시장 규모의 61.44%는 진단이 차지하며, 이는 병원에서의 일상적인 종양 워크플로우를 반영하고 있습니다. 그러나 창약과 검사는 제약 스폰서가 조직 분석을 위탁 연구 기관에 위탁하기 때문에 CAGR 8.14%에서 가장 급상승합니다. ICON plc는 CAP 라이선스 실험실에서 Ventana Benchmark ULTRA 플랫폼을 통한 맞춤형 면역조직화학 분석 개발을 제공합니다. 아웃소싱은 면역조직화학 시장 규모 혜택으로부터 혜택을 누립니다. 중앙 관리 시설에서는 매일 수천 개의 슬라이드를 처리하고 AI를 도입하여 비정상적인 값을 신고하여 바이오마커 인증의 사이클 시간을 단축합니다.

종양학뿐만 아니라 조직 기반 분석은 감염 및 자가 면역 연구에 도움이 됩니다. Spatial omics는 면역조직화학과 하이플렉스 RNA 매핑을 결합하여 표적 탐색을 가속화하는 멀티오믹스 컨텍스트를 제공합니다. 실험실 자동화 및 알고리즘 중심의 스코어링은 재현성을 향상시키고 데이터 무결성을 스폰서에게 보장합니다. 규제 당국이 의약품 승인 패키지에서 조직 증거를 중시하는 동안, 계약 실험실은 능력을 확대하고 예측 기간 동안이 부문의 기세를 강화하고 있습니다.

지역 분석

북미는 2024년 매출의 41.45%를 차지했으며, 확립된 상환, 조기 AI 도입, 빈번한 동반진단약 승인에 지지되고 있습니다. 그러나 FDA의 2024년 임상검사실 개발 검사규칙 하에서 검사실은 5억 6,600만-35억 6,000만 달러의 컴플라이언스 지출을 흡수해야 하며, 대형 IVD 제조업체와의 전략적 제휴를 촉구하고 있습니다. 현재 임상시설의 33%에 도입된 디지털 병리 검사는 원격지 전문의가 읽을 수 있는 이미지 관리 플랫폼으로 자본 예산이 전환됨에 따라 가속될 것으로 예측됩니다.

아시아태평양은 CAGR 8.21%로 가장 높은 성장을 보이고 있으며, 암 이환율 상승, 바이오 제조 능력 확대, 공립 병원 업그레이드가 그 요인이 되고 있습니다. 중국과 인도는 자동 슬라이드 염색기를 갖춘 암 센터에 자극책 자금을 투입하고 있지만 노동력 부족은 여전히 심각합니다. 파키스탄 병리학의 밀도는 인구 450,000명 당 1명으로 고도의 면역조직화학 시장의 도입 속도를 억제하고 있습니다. AI를 활용한 스코어링 툴에 대한 투자는 경험이 적은 직원이 단순한 사례의 트리아지를 할 수 있게 함으로써 부분적인 완화를 가져옵니다.

유럽은 CE-IVDR의 무결성과 정밀의료 개발의 확대를 배경으로 꾸준히 성장하고 있습니다. 독일과 프랑스는 디지털 플랫폼의 전개에서 주도하고 있지만, 남부와 동부의 국가는 상환 격차로 인해 뒤쳐져 있습니다. NordiQC와 같은 지역 품질 프로그램을 통해 바이오마커의 합격률은 2017년 71%에서 2021년 79%로 상승하여 분석 표준화를 위한 대륙적 뒷받침을 강조하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 암의 유병률 상승

- 인구의 고령화 및 만성 질환의 부담

- 멀티플렉스 및 AI 지원 IHC 워크플로우의 진보

- 암 치료제의 동반자 진단 승인 확대

- 제약 아웃소싱에서 조직 기반 바이오 마커 탐색의 성장

- 신흥 실험실에서의 저가격 자동 슬라이드 스테너의 이용 가능성

- 시장 성장 억제요인

- 프리미엄 항체 및 검출 키트의 고비용

- 저소득지역에서 숙련된 병리조직의 부족

- 첨단 IHC 패널의 상환 갭

- 중요 시약 공급망 취약성

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측

- 제품별

- 항체

- 1차 항체

- 2차 항체

- 장치

- 자동 슬라이드 염색기

- 조직 마이크로어레이

- 슬라이드 스캐너

- 기타

- 키트 및 시약

- 소프트웨어

- 항체

- 용도별

- 진단약

- 암

- 감염증

- 자가면역질환

- 기타

- 창약 및 검사

- 진단약

- 최종 사용자별

- 병원 및 진단센터

- 학술기관 및 연구기관

- 수탁연구기관

- 기타

- 검출 방법별

- 직접법

- 간접법

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- F. Hoffmann-La Roche AG

- Agilent Technologies Inc.

- Thermo Fisher Scientific Inc.

- Danaher Corp.(Leica Biosystems)

- Merck KGaA

- Abcam plc

- Bio-Rad Laboratories Inc.

- PerkinElmer Inc.

- Cell Signaling Technology Inc.

- Bio SB Inc.

- Sakura Finetek Japan Co.

- Biocare Medical LLC

- Enzo Life Sciences Inc.

- Lunaphore Technologies SA

- Vector Laboratories Inc.

- 3DHISTECH Ltd.

- Fluidigm(Standard BioTools)

- Qritive Pte Ltd.

- Miltenyi Biotec

- Genemed Biotechnologies Inc.

제7장 시장 기회 및 전망

AJY 25.11.10The global immunohistochemistry market is valued at USD 2.98 billion in 2025 and is forecast to reach USD 4.21 billion in 2030, advancing at a 7.16% CAGR.

Growth is supported by rising cancer prevalence, broader use of companion diagnostics, and rapid adoption of AI-enabled multiplex staining workflows that shorten turnaround times while improving diagnostic precision . Increasing digital pathology integration, deeper penetration of automated slide stainers in middle-income laboratories, and mounting investments in drug discovery outsourcing add further momentum. At the same time, the FDA's re-classification of immunohistochemistry assays as medical devices raises compliance costs yet favors large manufacturers that already operate globally certified quality systems. Geographic demand gradually shifts to Asia-Pacific, where expanding oncology infrastructure and manufacturing capacity complement unmet diagnostic needs. Consolidation among suppliers-illustrated by the 2024 Danaher-Abcam deal-signals a competitive emphasis on end-to-end reagent, instrument, and software portfolios.

Global Immunohistochemistry Market Trends and Insights

Rising Prevalence of Cancer

Surging cancer incidence sustains high demand for immunohistochemistry market tests that clarify tumor biology with single-cell resolution . Multiplex staining reveals immune-tumor interactions, guiding checkpoint inhibitor therapy selection. Companion diagnostics broaden treatment eligibility: the FDA cleared HER2-ultralow testing, and zanidatamab's biliary tract indication relies on robust HER2 staining. Rare cancer use cases, such as pemphigus diagnosis via direct immunofluorescence replacement, further expand the immunohistochemistry market .

Ageing Population & Chronic Disease Burden

Longer life expectancy multiplies chronic comorbidities, driving case volumes that stretch existing histopathology capacity. Fewer than 14 pathologists per million population globally and escalating workloads (over 4,000 cases annually in many regions) increase reliance on automation. Hospital laboratories request 20% more immunohistochemistry tests than a decade earlier, while only one-third of clinical sites have implemented digital pathology due to capital constraints. This gap accelerates adoption of AI-enabled slide scanners that standardize staining intensity and scoring, improving throughput without lowering quality.

High Cost of Premium Antibodies & Detection Kits

Two-thirds of commercially available antibodies fail basic specificity tests, forcing labs to run costly in-house validations that inflate per-test expenditure. The YCharOS review of 1,000 antibodies pegged unreproducibility losses at up to USD 1.8 billion annually in the United States alone. Median list prices for monoclonal therapeutics remain between USD 15,624 and USD 143,833, reflecting manufacturing scale limitations despite process improvements. Medicare's Local Coverage Determinations (in force since July 2024) now require rigorous medical-necessity documentation for immunohistochemistry stains, crimping reimbursement for extended panels.

Other drivers and restraints analyzed in the detailed report include:

- Advancements in Multiplex & AI-Assisted Workflows

- Expansion of Companion-Diagnostic Approvals

- Scarcity of Skilled Histopathologists in Low-Income Regions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The antibodies subsegment still anchors 42.23% of immunohistochemistry market share in 2024, confirming its foundational role in every assay run. Software, however, is advancing at an 8.02% CAGR as laboratories migrate to cloud-hosted image analytics that enable multi-institutional algorithm deployment. Roche's VENTANA DP 200 slide scanner integrated with navify Digital Pathology illustrates a seamless pathway from staining through AI scoring. The antibodies category itself evolves: primary monoclonal clones gain validation transparency, while multiplex-ready secondary antibodies amplify low-abundance targets. Equipment upgrades parallel these shifts; automated stainers reduce manual errors and free skilled labor for interpretation tasks. As open-source tools such as QuPath and HistoQC improve image standardization, laboratories in mid-income countries adopt digital platforms more swiftly, reinforcing software's strategic importance across the immunohistochemistry market.

In kits and reagents, companion diagnostic approvals influence purchasing decisions because oncologists require strict lot-to-lot reproducibility. Slide scanners and tissue microarrayers converge to support high-throughput translational research. Manufacturers respond with quality-assured reagent bundles to ease compliance under the FDA's device re-classification rule. This interplay secures software's elevation from ancillary tool to core revenue contributor, setting the stage for double-digit growth through 2030 in the immunohistochemistry market.

Diagnostics retained 61.44% of immunohistochemistry market size in 2024, mirroring routine oncology workflows across hospitals. Yet drug discovery and testing climbs fastest at an 8.14% CAGR as pharmaceutical sponsors externalize tissue analysis to contract research organizations. ICON plc exemplifies this pivot, offering custom immunohistochemistry assay development on Ventana Benchmark ULTRA platforms within CAP-licensed labs. Outsourcing benefits from immunohistochemistry market economies of scale: centralized sites process thousands of slides daily and deploy AI to flag outliers, reducing cycle time for biomarker qualification.

Beyond oncology, tissue-based assays inform infectious disease and autoimmune research. Spatial omics couples immunohistochemistry with high-plex RNA mapping, affording multi-omic context that accelerates target discovery. Laboratory automation and algorithm-driven scoring boost reproducibility, assuring sponsors of data integrity. As regulatory agencies emphasize tissue evidence in drug approval packages, contract labs expand capacity, reinforcing the segment's momentum throughout the forecast period.

The Immunohistochemistry Market Report is Segmented by Product (Antibodies [Primary Antibodies, Secondary Antibodies], Equipment, and More), Application (Diagnostics, Drug Discovery and Testing), End-User (Hospitals and Diagnostic Centres, and More), Detection Method (Direct, Indirect), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commands 41.45% of 2024 revenue, buoyed by established reimbursement, early AI deployment, and frequent companion diagnostic approvals. However, laboratories must absorb compliance spending of USD 566 million-3.56 billion under the FDA's 2024 laboratory-developed test rule, prompting strategic partnerships with larger IVD manufacturers. Digital pathology adoption, currently 33% of clinical sites, is expected to accelerate as capital budgets migrate toward image management platforms that unlock remote sub-specialist reads.

Asia-Pacific exhibits the highest growth at 8.21% CAGR, driven by rising oncology incidence, expanding biomanufacturing capacity, and public hospital upgrades. China and India channel stimulus funds into cancer centers outfitted with automated slide stainers, though workforce shortages remain acute. Pathologist density in Pakistan stands at one per 450,000 people, restraining the speed of advanced immunohistochemistry market adoption. Investment in AI-enabled scoring tools offers partial mitigation, allowing less-experienced staff to triage simple cases.

Europe grows steadily on the back of CE-IVDR alignment and expanding precision medicine rollouts. Germany and France lead in digital platform deployments, while Southern and Eastern states lag due to reimbursement gaps: Bulgaria restricts coverage to limited breast malignancy markers, shifting costs to patients. Regional quality programs such as NordiQC boosted biomarker pass rates from 71% in 2017 to 79% in 2021, underscoring a continental push toward assay standardization.

- Roche

- Agilent Technologies

- Thermo Fisher Scientific

- Danaher Corp. (Leica Biosystems)

- Merck

- Abcam

- Bio-Rad Laboratories

- PerkinElmer

- Cell Signaling Technology

- Bio SB

- Sakura Finetek Japan Co.

- Biocare Medical

- Enzo Biochem

- Lunaphore Technologies SA

- Vector Laboratories

- 3DHistech

- Fluidigm (Standard BioTools)

- Qritive Pte Ltd.

- Miltenyi Biotec

- Genemed Biotechnologies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Cancer

- 4.2.2 Ageing Population & Chronic Disease Burden

- 4.2.3 Advancements In Multiplex & AI-Assisted IHC Workflows

- 4.2.4 Expansion Of Companion-Diagnostic Approvals for Targeted Oncology Drugs

- 4.2.5 Growth Of Tissue-Based Biomarker Discovery in Pharma Outsourcing

- 4.2.6 Accessibility Of Low-Cost Automated Slide Stainers in Emerging Labs

- 4.3 Market Restraints

- 4.3.1 High Cost of Premium Antibodies & Detection Kits

- 4.3.2 Scarcity Of Skilled Histopathologists in Low-Income Regions

- 4.3.3 Reimbursement Gaps for Advanced IHC Panels

- 4.3.4 Supply-Chain Fragility for Critical Reagents

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porters Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Antibodies

- 5.1.1.1 Primary Antibodies

- 5.1.1.2 Secondary Antibodies

- 5.1.2 Equipment

- 5.1.2.1 Automated Slide Stainers

- 5.1.2.2 Tissue Microarrayers

- 5.1.2.3 Slide Scanners

- 5.1.2.4 Others

- 5.1.3 Kits and Reagents

- 5.1.4 Software

- 5.1.1 Antibodies

- 5.2 By Application

- 5.2.1 Diagnostics

- 5.2.1.1 Cancer

- 5.2.1.2 Infectious Diseases

- 5.2.1.3 Auto-immune Diseases

- 5.2.1.4 Others

- 5.2.2 Drug Discovery and Testing

- 5.2.1 Diagnostics

- 5.3 By End-User

- 5.3.1 Hospitals and Diagnostic Centres

- 5.3.2 Academic and Research Institutes

- 5.3.3 Contract Research Organizations

- 5.3.4 Others

- 5.4 By Detection Method

- 5.4.1 Direct

- 5.4.2 Indirect

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 F. Hoffmann-La Roche AG

- 6.3.2 Agilent Technologies Inc.

- 6.3.3 Thermo Fisher Scientific Inc.

- 6.3.4 Danaher Corp. (Leica Biosystems)

- 6.3.5 Merck KGaA

- 6.3.6 Abcam plc

- 6.3.7 Bio-Rad Laboratories Inc.

- 6.3.8 PerkinElmer Inc.

- 6.3.9 Cell Signaling Technology Inc.

- 6.3.10 Bio SB Inc.

- 6.3.11 Sakura Finetek Japan Co.

- 6.3.12 Biocare Medical LLC

- 6.3.13 Enzo Life Sciences Inc.

- 6.3.14 Lunaphore Technologies SA

- 6.3.15 Vector Laboratories Inc.

- 6.3.16 3DHISTECH Ltd.

- 6.3.17 Fluidigm (Standard BioTools)

- 6.3.18 Qritive Pte Ltd.

- 6.3.19 Miltenyi Biotec

- 6.3.20 Genemed Biotechnologies Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment