|

시장보고서

상품코드

1846347

의료용 커넥터 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Medical Connectors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

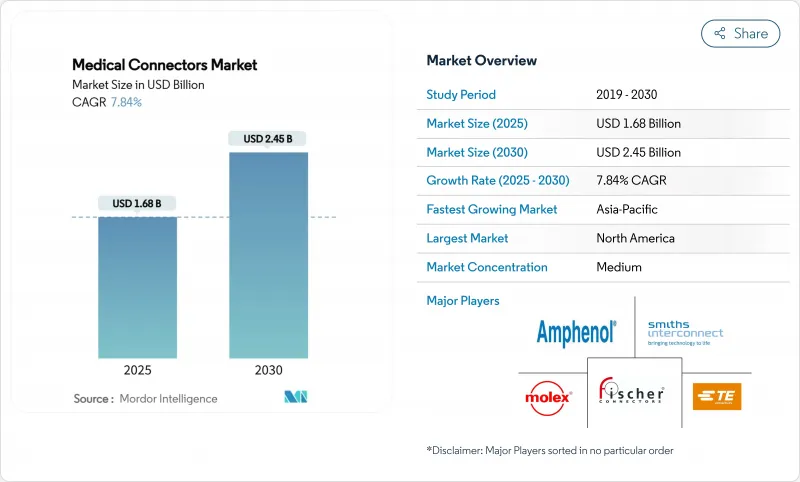

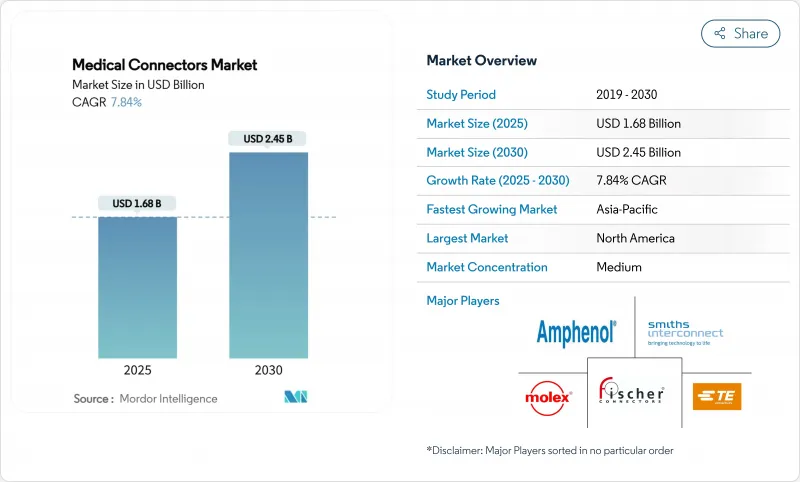

의료용 커넥터 시장 규모는 2025년에 16억 8,000만 달러로 추정되고, 2030년에는 24억 5,000만 달러에 이를 것으로 예측되며, 이 기간 동안 CAGR 7.84%로 성장할 전망입니다.

수요의 확대는 디지털 네트워크 의료로의 꾸준한 이동, 웨어러블 모니터의 보급, 컴팩트하고 멸균 가능한 인터페이스에 의존하는 단일 사용 장치 플랫폼의 채택 확대로 인한 것입니다. 제조업체 각 회사는 기계적 마모를 없애고 집중 치료실에서 장치의 턴어라운드 시간을 단축하는 자기 퀵 커넥트 디자인에 투자하고 있습니다. 병원 정보 시스템의 상호 운용성 이니셔티브는 표준화된 핀 구성의 필요성을 강화하는 반면, 재택 치료에 대한 채택은 직관적이고 환자에게 안전한 연결 방법을 유사하게 중시합니다. 지역적 기회의 분산은 현저합니다. : 북미는 여전히 기술 중심이지만, 아시아태평양은 모듈형 다목적 커넥터 제품군을 선호하는 공립 병원 네트워크의 용량 강화로 이익을 얻고 있습니다. 특히 실리콘 쉴드나 구리 합금의 방청 처리 등 재료과학의 돌파구는 수명과 성능을 더욱 향상시킵니다.

세계의 의료용 커넥터 시장 동향 및 인사이트

만성 질환 증가

심혈관계와 당뇨병의 이환율이 상승하고 견고하고 얇은 전기 인터페이스에 의존하는 실시간 모니터링의 요구가 강해지고 있습니다. 이식형 루프 레코더와 인슐린 주입 펌프는 장시간 장착해도 중단 없는 원격 측정을 지원하는 내습성 콘택트 도금의 지정이 증가하고 있습니다. 예측 분석을 추구하는 의료 시스템은 전자기 간섭 없이 높은 샘플링 주파수를 유지하는 커넥터를 요구합니다. 병원 워크로드가 사전 활동적인 질병 관리로 전환함에 따라 자기 퀵 커넥트 솔루션은 아크 방전을 피하고 커넥터 피로를 줄이기 위해 지지를 받고 있습니다. 지속적인 데이터 획득은 사이버 보안 모니터링을 강화하기 때문에 OEM은 물리적 키잉과 암호화 가능 배선 아키텍처를 통합한 차폐 커넥터 하우징을 지정합니다.

의료기기 설치 기반 확대

아시아태평양의 병원 확장 및 로봇 투자는 누적 장비를 증가시키고 예비 부품 물류를 간소화하는 상호 운용 가능한 커넥터의 풋프린트가 선호됩니다. 캡슐 내시경 및 마이크로펌프로 대표되는 장비의 소형화로 인해 사용 가능한 기판 공간이 줄어들기 때문에 제조업체는 솔더 리플로우 가능한 실리콘 오버몰드를 사용하는 서브밀리 피치 헤더를 개발해야 합니다. 레거시 주입 펌프를 대상으로 하는 레트로핏 프로그램은 전기적 및 생체적합성 표준의 개정에 따라 업데이트된 커넥터 블록을 인증할 수 있는 벤더에게 레트로핏의 수익원을 열게 됩니다. 외과용 로봇을 채용하는 기업은 도금 박리 없이 3,000회의 오토클레이브 패스를 견딜 수 있는 하이사이클 커넥터를 요구하고 있습니다. 엔드 투 엔드 인증 데이터를 제공하는 공급업체는 OEM 설계 사이클을 단축하고 의료용 커넥터 시장에서 우위를 차지할 수 있습니다.

엄격한 세계 및 지역 규정 준수

ISO13485 : 2016에 따른 FDA의 품질 관리 시스템 규제로의 전환은 제조업체가 문서화 아키텍처 및 감사 절차를 오버홀하게 합니다. 유럽의 MDR 시스템은 고유한 장치 식별자의 의무를 부과하고 모든 커넥터 배치에 추적성 비용을 추가합니다. 라틴아메리카 시장에서는 인증된 생체적합성 보고서에 대한 요구가 증가하고 있으며, 폴리머 개정의 승인 주기가 장기화되고 있습니다. 소규모 공급업체는 여러 법역에 걸친 동시 신청을 위한 자금 조달에 어려움을 겪고 있으며 의료용 커넥터 시장에서의 통합이 가속화되고 있습니다. 사이버 보안 조항은 환자 식별자를 전송하는 커넥터에도 적용되며 제품 검증 타임라인을 늘리는 암호화 테스트 단계가 도입됩니다.

부문 분석

플랫 실리콘 수술용 케이블은 2024년 의료용 커넥터 시장 점유율에서 38.89%를 차지했으며, 전기 수술용 핸드피스와 복강경용 에너지 플랫폼에서 계속 우위를 유지하고 있는 것으로 나타났습니다. 이 부문은 실리콘의 유연성, 유전 안정성, 오토 클레이브 사이클과의 호환성, 유지 보수 간격의 단축 및 전기적 무결성을 유지하는 특성으로부터 이익을 얻었습니다. 레이어 압출 성형의 발전으로 현재 2톤 절연이 통합되어 손상을 즉시 시각적으로 감지할 수 있어 병원의 리스크 관리 프로토콜이 강화되었습니다. 자기 의료용 커넥터는 현재 설치 베이스는 작지만, 대전류 이동 중 아크 형성을 최소화하는 비접촉식 커플링으로 인해 CAGR은 8.65%를 보일 것으로 예측됩니다. 일회용 플라스틱 커넥터는 세척의 번거로움을 줄임으로써 감염 제어의 의무에 따라 단일 사용 관개용 지팡이로의 수용을 확대합니다. 푸시 풀 방식은 일반 병동의 모니터링에 계속 대응하고 간호 직원이 신뢰하는 친숙한 촉각 신호를 제공합니다. 하이브리드 서큘러 시스템은 로봇 엔드 이펙터 내에서 전력, 섬유 및 공압의 복합 라우팅을 가능하게 하여 수술 자동화 전문가의 설계 자유도를 향상시킵니다. 이와 같이 다양한 형태가 있기 때문에 의료용 커넥터 시장은 건전한 제품 믹스의 역동성을 유지하고 있습니다.

자기 선택은 초기 자본 비용보다 마모가 없는 긴 수명을 선호함으로써 구매 기준을 재구성합니다. 금-코발트 펠렛과 같은 새로운 합금은 자기 포화 한계를 높여 유지력을 손상시키지 않고 소형화를 가능하게 합니다. 물리치료기기에서 리드를 빼낼 때 장비포트에 스트레스가 걸리지 않기 때문에 신속한 제거가 전복예방 프로그램을 지원합니다. 온보드 EEPROM 칩을 커넥터 쉘에 통합하는 공급업체는 플러그 앤 플레이의 추적성을 제공하고 기술자가 예지 보전을 계획할 수 있도록 도와줍니다. 전기 수술 케이블 공급업체는 과열을 시각적으로 보여주는 열 변색 재킷을 연구하고 절연 불량을 사전에 방지합니다. 다접점 밀도를 추구하는 움직임은 서브어셈블리의 모듈화에 박차를 가하고 OEM은 ISO 14644-1 클린룸 인증을 보유한 커넥터 전문 제조업체에 오버몰드 공정을 위탁하고 있습니다. 이러한 노력은 의료용 커넥터 시장에서 제품 혁신의 기세를 지원합니다.

지역 분석

북미는 성숙한 자본 설비 사이클과 하이스펙 커넥터의 조기 채용이 보상되는 확립된 컴플라이언스 체제를 반영하여 2024년에 41.03%의 매출 최고를 유지했습니다. 가치관을 기반으로 한 의료 지표는 병원이 커넥터 하우징에 예지 보전 센서를 통합하는 것을 뒷받침하여 계획되지 않은 가동 중지 시간을 줄입니다. 이 지역은 다른 지역에 앞서 ISO 80369-7의 도입을 추진하여 교환 수요를 가속화하고 있습니다. Minneapolis와 Boston의 신흥 생태계는 차세대 신경 자극기를 육성하고 지역 커넥터 설계 활동을 더욱 활성화합니다. 국내 반도체 패키징에 대한 정책적 우대 조치는 소형화된 전극 어레이를 통합하는 공급업체에게 이익을 제공하고 의료용 커넥터 시장의 기술적 이점을 유지합니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR) 8.89%에서 최고 속도를 기록할 전망입니다. 중국과 인도의 공공 의료 보험자들이 만성 질환 관리 기술에 대한 접근을 확대하기 위해 노력하고 있기 때문입니다. 현지 OEM은 주입 펌프의 생산량을 확대하여 기준선의 커넥터 소비를 확대합니다. 싱가포르와 한국의 규제기관이 미국 FDA와 문서를 정합시켜 세계 공급업체의 중복을 줄이고 제품 출시를 앞당깁니다. 국산 의료용 전자기기 제조에 대한 정부의 보조금에 의해 수입 의존도가 저하되고, 다국적 기업이 말레이시아와 베트남에 커넥터 조립 공장을 설립하게 됩니다. 도시화로 2차 도시에서의 환자 모니터링 시스템 수요가 높아져 Tier1 헬스케어의 중심지 이외에도 수요가 확대되어 의료용 커넥터 시장의 기회가 다양화합니다.

유럽은 재활용 가능한 커넥터 재료를 선호하는 엄격한 환경 정책에 힘입어 꾸준한 확대를 유지하고 있습니다. 국가의 의료 서비스는 노후된 장비를 업데이트하고 할로겐이 없는 절연 화합물을 선호하는 RoHS 및 REACH 규정 준수를 강화합니다. 북유럽 전역의 공동 구매 플랫폼은 단위 마진을 압축하지만 다년간 수량 확약을 보장합니다. 독일의 정밀 공학 거점은 EU가 자금 제공하는 연구에 의해 재료 과학의 개선을 추진하고 수술 로봇용 하이브리드 원형 커넥터의 개척을 계속하고 있습니다. 동유럽은 비용 경쟁력 있는 제조 거점으로 부상하고 아시아태평양의 운임 변동을 우려하는 서양 공급업체에게 니어 쇼어 옵션을 제공합니다. 그 결과, 이 지역은 성능면에서의 리더십과 지속가능성에 대한 개입을 양립시켜 의료용 커넥터 시장에서의 전략적 관련성을 유지하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 도입

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 만성 질환 증가

- 의료기기 설치 대수의 확대

- 재택치료 및 원격 감시 솔루션으로의 이동

- 소형화 및 고밀도 멀티 콘택트 설계

- 호스피탈 등급의 자기 퀵 커넥터의 채용

- 일회용 유체 경로 커넥터를 단일 사용 OEM 키트에 통합

- 시장 성장 억제요인

- 엄격한 세계적 및 지역적 규제 준수

- 멸균에 의한 재료 열화 위험

- 커넥터의 오감합 및 상호 접속의 위험성

- 의료 등급 수지 및 구리 합금 공급망 부족

- 규제 상황

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측

- 제품별

- 플랫 실리콘 수술용 케이블

- 내장형 일렉트로닉스 커넥터

- 고주파 커넥터

- 일회용 플라스틱 커넥터

- 하이브리드 원형 커넥터 및 리셉터클 시스템

- 유지 시스템 부착 전원 코드

- 조명이 있는 호스피탈 등급 코드

- 자기 의료용 커넥터

- 푸시풀 커넥터

- 용도별

- 환자 모니터링 장비

- 전기외과 수술용 기기

- 화상 진단 장치

- 심장병학기기

- 분석 및 처리 장치

- 호흡기용 기기

- 치과용 기기

- 내시경 검사 장비

- 신경 기기

- 경장용 기기

- 기타 용도

- 최종 사용자별

- 병원

- 외래수술센터(ASC)

- 기타 최종 사용자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- TE Connectivity

- Amphenol Corporation

- Smiths Interconnect

- Fischer Connectors SA

- Molex LLC

- ITT Interconnect Solutions

- Souriau(Souriau-Sunbank)

- Omnetics Connector Corp

- KEL Corporation

- Qosina Corp

- Shenzhen Xime Connector Technology

- Salter Labs

- Lemo SA

- Samtec Inc.

- Aptiv PLC

- Rosenberger Hochfrequenztechnik

- ODU GmbH

- Neutrik AG

- Phoenix Contact

- Plastics One

제7장 시장 기회 및 전망

AJY 25.11.10The medical connectors market size stands at USD 1.68 billion in 2025 and is forecast to reach USD 2.45 billion by 2030, reflecting a 7.84% CAGR through the period.

Demand expansion arises from the steady shift toward digitally networked care, the proliferation of wearable monitors, and the growing adoption of single-use device platforms that rely on compact, sterilizable interfaces. Manufacturers are investing in magnetic quick-connect designs that eliminate mechanical wear and accelerate device turnaround times in intensive care units. Interoperability initiatives within hospital information systems reinforce the need for standardized pin configurations, while home-care adoption places equal emphasis on intuitive, patient-safe connection methods. Regional opportunity dispersion is pronounced: North America remains technology-centric, whereas Asia-Pacific benefits from capacity build-out in public hospital networks that prefer modular, multi-purpose connector families. Material science breakthroughs, particularly in silicone shielding and copper-alloy anti-corrosion treatments, further enhance lifespan and performance.

Global Medical Connectors Market Trends and Insights

Rising Incidence of Chronic Diseases

Elevated cardiovascular and diabetes prevalence has intensified real-time monitoring requirements that depend on robust, low-profile electrical interfaces. Implantable loop recorders and insulin infusion pumps increasingly specify moisture-resistant contact plating that supports uninterrupted telemetry during extended wear periods. Health systems pursuing predictive analytics mandate connectors that sustain high sampling frequencies without electromagnetic interference. As hospital workloads migrate toward proactive disease management, magnetic quick-connect solutions gain traction because they avoid arcing and reduce connector fatigue. Continuous data capture also amplifies cybersecurity scrutiny, prompting OEMs to specify shielded connector housings that integrate physical keying with encryption-ready wiring architectures.

Expansion of the Medical Device Installed Base

Asia-Pacific hospital expansions and robotics investments enlarge the cumulative equipment fleet, driving preference for interoperable connector footprints that streamline spare-parts logistics. Device miniaturization, illustrated by capsule endoscopes and micro-pumps, compresses available board space, compelling manufacturers to develop sub-millimeter pitch headers with solder-reflowable silicone over-molds. Retrofit programs targeting legacy infusion pumps open retrofit revenue streams for vendors able to certify updated connector blocks under revised electrical and biocompatibility norms. Surgical robotics adopters request high-cycle connectors capable of surviving 3,000 autoclave passes without plating delamination. Suppliers that offer end-to-end qualification data shorten OEM design cycles and gain an edge in the medical connectors market.

Stringent Global and Regional Regulatory Compliance

The FDA's transition to the Quality Management System Regulation that aligns with ISO 13485:2016 compels manufacturers to overhaul documentation architectures and audit procedures. Europe's MDR regime imposes unique device identifier obligations, adding traceability costs to every connector batch. Markets in Latin America increasingly demand certified biocompatibility reports, elongating approval cycles for polymer revisions. Smaller suppliers struggle to finance concurrent submissions across multiple jurisdictions, accelerating consolidation within the medical connectors market. Cybersecurity clauses now extend to connectors that transmit patient identifiers, introducing encryption-testing steps that lengthen product validation timelines.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Home-Care and Remote Monitoring Solutions

- Miniaturization and High-Density Multi-Contact Designs

- Sterilization-Induced Material Degradation Risk

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Flat silicone surgical cables retained a 38.89% stake in the medical connectors market share during 2024, underlining their continued primacy in electrosurgical handpieces and laparoscopic energy platforms. The segment benefits from silicone's flexibility, dielectric stability, and compatibility with autoclave cycles, characteristics that shorten maintenance intervals and uphold electrical integrity. Advancements in layered extrusion now integrate two-tone insulation that provides instant visual damage detection, reinforcing hospital risk-management protocols. Magnetic medical connectors, though presently smaller in installed base, are forecast to log an 8.65% CAGR due to their contactless coupling that minimizes arc formation during high-current transfers. Disposable plastic connectors expand reception in single-use irrigation wands, where eliminating cleaning overhead aligns with infection-control mandates. Push-pull formats continue to address general ward monitoring, delivering a familiar tactile cue that nursing staff trust. Hybrid circular systems enable combined power, fiber, and pneumatic routing within robotic end-effectors, enhancing design freedom for surgical automation specialists. This plurality of formats ensures that the medical connectors market retains healthy product-mix dynamism.

Magnetic alternatives are reshaping purchasing criteria by prioritizing zero-wear longevity over upfront capital cost. Novel alloys such as gold-cobalt pellets enhance magnetic saturation limits, allowing downsizing without compromising retention force. Rapid detachment supports fall-prevention programs, as yanking leads from physiotherapy equipment no longer stresses device ports. Vendors integrating on-board EEPROM chips into connector shells create plug-and-play traceability, which helps technicians schedule predictive maintenance. Electrosurgical cable suppliers are exploring thermochromic jackets that visually indicate overheating, pre-empting insulation failure. The drive toward multi-contact density has spurred sub-assembly modularization, with OEMs outsourcing over-molding processes to connector specialists that hold ISO 14644-1 cleanroom certifications. These initiatives collectively sustain momentum for product innovation within the medical connectors market .

The Medical Connectors Market Report is Segmented by Product (Flat Silicone Surgical Cables, Embedded Electronics Connectors, and More), Application (Patient Monitoring Devices, Electrosurgical Devices, and More), End User (Hospitals, Ambulatory Surgical Centers, Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 41.03% revenue leadership in 2024, reflecting mature capital equipment cycles and well-established compliance frameworks that reward early adoption of high-specification connectors. Value-based care metrics push hospitals to embed predictive maintenance sensors within connector housings, thereby reducing unplanned downtime. The region champions ISO 80369-7 implementation ahead of other geographies, accelerating replacement demand. Start-up ecosystems in Minneapolis and Boston foster next-generation neurostimulation devices, further lifting local connector design activity. Policy incentives for domestic semiconductor packaging benefit suppliers integrating miniaturized electrode arrays, maintaining technological headship for the medical connectors market.

Asia-Pacific will post the fastest regional trajectory at an 8.89% CAGR through 2030 as public health insurers in China and India commit to broadening access to chronic disease management technologies. Local OEMs are scaling infusion pump output, thereby enlarging baseline connector consumption. Regulatory agencies in Singapore and South Korea harmonize documentation with the US FDA, lowering duplication for global suppliers and hastening product launches. Government subsidies for indigenous medical electronics manufacturing reduce import dependency, prompting multinationals to establish connector assembly plants in Malaysia and Vietnam. Urbanization intensifies demand for patient monitoring systems in secondary cities, spreading volume beyond Tier 1 healthcare hubs and diversifying opportunity within the medical connectors market.

Europe maintains steady expansion driven by stringent environmental policies that prioritize recyclable connector materials. National health services renew aging device fleets, enforcing RoHS and REACH compliance that favors halogen-free insulation compounds. Collaborative purchasing platforms across the Nordics compress unit margins but guarantee multi-year volume commitments. Germany's precision-engineering base continues to pioneer hybrid circular connectors for surgical robotics, with EU-funded research propelling material science improvements. Eastern Europe emerges as a cost-competitive manufacturing locus, providing a near-shore alternative for Western suppliers concerned about Asia-Pacific freight volatility. Consequently, the region balances performance leadership with sustainability interventions, sustaining its strategic relevance in the medical connectors market.

- TE Connectivity

- Amphenol

- Smiths Group

- Fischer Connectors

- Molex

- ITT Interconnect Solutions

- Souriau (Souriau-Sunbank)

- Omnetics Connector

- KEL

- Qosina Corp

- Shenzhen Xime Connector Technology

- Salter Labs

- Lemo SA

- Samtec Inc.

- Aptiv PLC

- Rosenberger Hochfrequenztechnik

- ODU GmbH

- Neutrik AG

- Phoenix Contact

- Plastics One

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising incidence of chronic diseases

- 4.2.2 Expansion of the medical device installed-base

- 4.2.3 Shift toward home-care & remote monitoring solutions

- 4.2.4 Miniaturisation & high-density multi-contact designs

- 4.2.5 Hospital-grade magnetic quick-connect adoption

- 4.2.6 Integration of disposable fluid-path connectors in single-use OEM kits

- 4.3 Market Restraints

- 4.3.1 Stringent global & regional regulatory compliance

- 4.3.2 Sterilisation-induced material degradation risk

- 4.3.3 Connector mis-mating & cross-connection hazards

- 4.3.4 Supply-chain shortages of medical-grade resins & copper alloys

- 4.4 Regulatory Landscape

- 4.5 Porters Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Flat Silicone Surgical Cables

- 5.1.2 Embedded Electronics Connectors

- 5.1.3 Radio-Frequency Connectors

- 5.1.4 Disposable Plastic Connectors

- 5.1.5 Hybrid Circular Connector & Receptacle Systems

- 5.1.6 Power Cords with Retention Systems

- 5.1.7 Lighted Hospital-Grade Cords

- 5.1.8 Magnetic Medical Connectors

- 5.1.9 Push-Pull Connectors

- 5.2 By Application

- 5.2.1 Patient Monitoring Devices

- 5.2.2 Electrosurgical Devices

- 5.2.3 Diagnostic Imaging Devices

- 5.2.4 Cardiology Devices

- 5.2.5 Analysers & Processing Equipment

- 5.2.6 Respiratory Devices

- 5.2.7 Dental Instruments

- 5.2.8 Endoscopy Devices

- 5.2.9 Neurology Devices

- 5.2.10 Enteral Devices

- 5.2.11 Other Applications

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgical Centers

- 5.3.3 Other End Users

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, Recent Developments)

- 6.3.1 TE Connectivity

- 6.3.2 Amphenol Corporation

- 6.3.3 Smiths Interconnect

- 6.3.4 Fischer Connectors SA

- 6.3.5 Molex LLC

- 6.3.6 ITT Interconnect Solutions

- 6.3.7 Souriau (Souriau-Sunbank)

- 6.3.8 Omnetics Connector Corp

- 6.3.9 KEL Corporation

- 6.3.10 Qosina Corp

- 6.3.11 Shenzhen Xime Connector Technology

- 6.3.12 Salter Labs

- 6.3.13 Lemo SA

- 6.3.14 Samtec Inc.

- 6.3.15 Aptiv PLC

- 6.3.16 Rosenberger Hochfrequenztechnik

- 6.3.17 ODU GmbH

- 6.3.18 Neutrik AG

- 6.3.19 Phoenix Contact

- 6.3.20 Plastics One

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment