|

시장보고서

상품코드

1848287

항레트로바이러스약 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Anti-retroviral Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

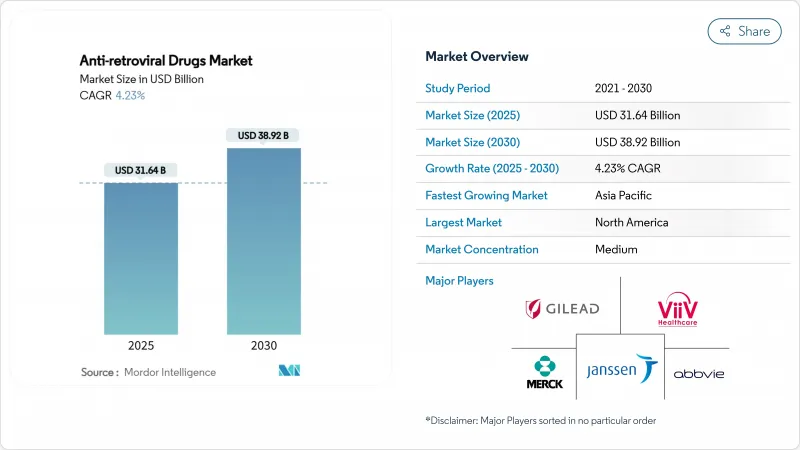

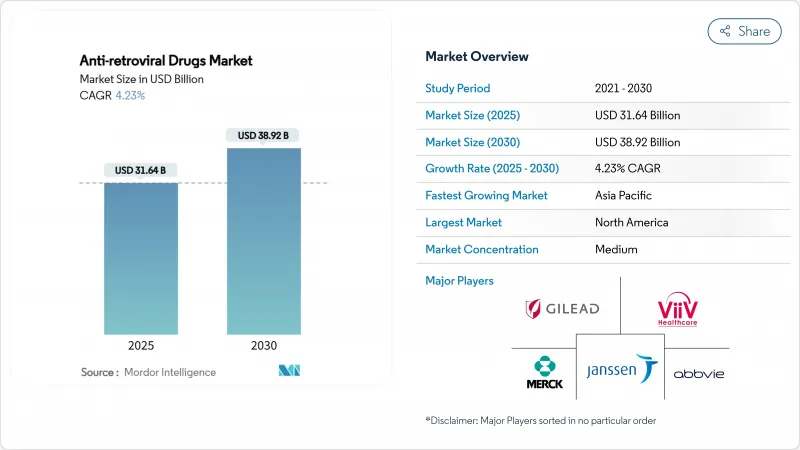

항레트로바이러스약 시장 규모는 2025년에 316억 4,000만 달러로 추정되고, 2030년에는 389억 2,000만 달러에 이를 것으로 예측됩니다.

이 속도는 지금까지의 급속한 확장에서 기술 혁신, 차별화된 접근 전략, 공급망의 강인성이 성장을 이끌어내는 성숙기로의 전환을 보여줍니다. 장시간 작용형 주사제, 주 1회 경구 투여 요법, 초내구성 예방약이 어드히어런스를 강화하고 새로운 예방 분야를 개척하는 한편, 1차 케어에의 통합적인 약제 공급과 디지털 어드히어런스 툴이 치료 범위를 확대합니다. 블록버스터의 특허 만료이 가까워짐에 따라 경쟁의 치열성이 증가하고 브랜드 제품의 라이프사이클 연장과 제네릭 의약품의 적극적인 포지셔닝이 모두 촉진되고 있습니다. 동시에 기부자로부터의 자금 제공, 가격 연계의 틀, 현지 제조에 대한 투자가 신규 감염의 대부분을 차지하는 중저소득 국가에서 수요를 계속 지원하고 있습니다.

세계의 항레트로바이러스약 시장 동향 및 인사이트

세계의 HIV 유병률 증가 및 치료 범위 확대

HIV 프로그램은 현재 치료되지 않은 채 바이러스와 공존하는 33%의 사람들을 대상으로 하고 있으며, 이 집단은 신흥 유럽, 중앙 아시아, 라틴아메리카의 일부에 집중하고 있습니다. 증가하는 중소득 국가의 예산은 단계적 가격 설정과 함께 항레트로바이러스약 시장을 1인당 잠재 지출이 과거 사하라 이남의 평균보다 높은 지역으로 밀어 올리고 있습니다. HIV에 걸린 채 고령화하는 성인이 증가함에 따라 신장과 뼈의 위험이 적은 병용 내성 요법이 지지를 모으고 이환율이 저하된 지역에서도 약가가 유지되고 있습니다. WHO가 제창하는 유니버설 테스트 앤 트리트 정책이 퍼스트라인 수요를 엄격히 유지하는 한편, 대규모화된 바이러스량 모니터링은 실패를 조기에 발견하고, 세컨드라인의 섭취를 높이고 있습니다. 이러한 원동력은 전체적으로 모든 치료 라인에 걸친 광범위한 수요의 반복적인 기반을 강화합니다.

보편적 ART 접근을 위한 공적 자금 및 공여자 자금 강화

세계 기금의 2024-2026년 92억 달러의 배분은 70개국에서 다년간의 조달 및 공급망 강화의 자금원이 되어 공급자에 대한 예측 가능한 수요를 지원합니다. PEPFAR의 국가 협업 대출에 대한 축족은 국가 예산 프레임을 박차하고 현금 흐름주기를 단축하는 제조업체 및 정부의 직접 계약을 유치합니다. 120개국을 다루는 길리아드의 레나카파빌 계약과 같은 사전구입 약정 및 자원봉사 라이선스는 일반 의약품의 조기 출시를 촉구하는 동시에 충성도 구조를 통해 발명자의 마진을 보호합니다. 전반적으로, 블렌드 파이낸싱 메커니즘은 중기적으로 기증자의 피폐로부터 항레트로바이러스약 시장을 보호하지만, 고소득 기증자 국가에서 미래의 거시 경제적 스트레스는 여전히 모니터링 목록의 위험입니다.

지속적인 약물 내성 및 바이러스 변이

WHO의 감시에 따르면, 돌테그라빌의 내성은 치료력이 있는 환자에서 3.9-8.6%, 과거에 내성이 확인된 환자에서 19.6%이며, 지불자는 보다 고비용의 세르베지 레지멘을 선택할 수밖에 없습니다. 저자원 환경에서의 내성 검사의 격차는 새로운 다중 클래스 실패를 덮고 가이드라인 업데이트를 복잡하게 합니다. 검사비용과 2차 치료제의 추가비용은 공여자 예산과 국민보험제도에 부담을 주고, 특허로 보호된 구제요법은 더욱 지출을 증가시킵니다. 공급업체에게는 내성균 증가에 따라 포트폴리오의 우선순위가 유전적 장벽이 높은 약제나 멀티모달적인 작용기전을 가지는 약으로 바뀌어 연구개발 예산이나 시험의 복잡성이 늘어나게 됩니다.

부문 분석

다제 병용 요법은 복약의 간편화 및 높은 내성 장벽에 의해 2024년에 38.45%의 매출을 확보해, 제1선택약의 내구성을 지원합니다. 인테그라제 억제제 중심의 처방은 CAGR 6.53%를 기록했으며, 이 클래스에서 가장 호조를 보였습니다. 이것은 전 치료가 많은 코호트에서 85% 이상의 억제율을 유지하는 1일 1회 투여의 빅테그라빌 또는 돌테그라빌 기반의 백본에 밀어붙인 것입니다. 뉴클레오시드계 역전사효소 억제제는 뼈와 신장에 대한 신호가 과거에 보고되었음에도 불구하고 여전히 주력제입니다. 개질된 테노포비르 아라페나미드는 이러한 위험을 줄이고 프랜차이즈 라이프를 연장하고 있습니다. 프로테아제 억제제는 살베지 요법의 부스트에 계속 사용되지만, 신진 대사 우려에서 임상의의 선호도가 변화하고 감소하고 있습니다. 중국이 신청 중인 알부버티드(albuvirtide)를 포함한 신규 진입 억제제와 광역 중화 항체는 파이프라인에 다양성을 가져오지만, 가이드라인에서 주목받기 위해서는 비용 효과를 실증할 필요가 있습니다.

인테그라제에 의한 내구성과 1일 1회 투여의 간편함은 1점 돌연변이에 대한 취약성에 의해 약제의 사용이 제한되어 있는 NNRTI로부터, 이 유형의 약제의 점유율을 확대하는 데 도움이 됩니다. 인테그라제 병용 요법 시장 규모는 임상 신뢰의 지속성과 적응증의 확대를 반영하여 2030년까지 180억 달러 이상에 달할 것으로 예측됩니다. 그러나 주요 특허가 해지되는 2031년 이후 제네릭 의약품에 대한 침식에 대비해야 하며, 제조업체는 가치를 지키기 위해 차세대 부스터나 초장시간 작용형의 디포 제제의 도입을 강요받고 있습니다.

2024년의 매출은 정제의 단제 요법이 압도적으로 많았지만, 매일의 복약 준수의 장벽을 없애는 디포 주사와의 경쟁이 격화하고 있습니다. 단일 정제 요법 시장 점유율은 광범위한 지불자들에게 친숙해지고 유통이 간소화됨에 따라 지원되지만, 복약 준수에 문제가 있는 코호트가 주사제로 이동함에 따라, 성장은 한 자릿수 전반에 둔화됩니다. 장시간 작용형 CAB-RPV는 고소득층에서 초기 도입이 진행되고 있으며, 레나카파비르의 6개월 투여 간격은 새로운 편리성의 지표가 되므로, 지불자 믹스를 전문 약국 채널로 시프트시킬 가능성이 있습니다.

임플란트 기술은 아직 조사 중이지만, 특히 높은 부담의 젊은 층에서의 예방을 위해 파괴적인 가능성을 가지고 있습니다. 주사제의 제조 스케일업은 콜드체인의 단절 및 장치 부족과 같은 공급망의 취약성을 초래합니다. 장기간 작용하는 양식에 특화된 항레트로바이러스약 시장 규모는 2030년까지 연평균 복합 성장률(CAGR) 6.99%로 54억 달러를 기록할 것으로 예상되며, 초기의 상업적 성공은 의료 제공업체의 트레이닝 인센티브 및 관리 서비스의 상환 코드에 달려 있습니다.

지역 분석

북미는 2024년 항레트로바이러스약 시장 매출액의 42.43%를 차지했으며, 획기적 신약에 대한 조기 접근과 환자 1인당 연간 25,000-3만 달러가 일상적으로 환불되는 보험 적용의 혜택을 받고 있습니다. 레나카파빌의 FDA 승인은 이 지역의 혁신적인 견인력을 강조하고 있지만, 빅테그라빌(2036년)과 돌테그라빌(2031년)의 특허 절벽이 다가오면서 가격 하락과 제네릭 의약품의 과제를 초래하고 있습니다. 지불 측과의 협상에서는 결과 기반 할인이 중요하며, 지속적인 억제와 어드히어런스 개선에 대한 실제 임상 증거를 제출해야 합니다.

유럽은 성장이 둔화되는 반면, 견조하게 추이하고 있습니다. 조화로운 HTA의 틀이 여러 국가에서 동시 출시를 촉진하는 반면, 엘리 릴리의 25억 달러를 투자한 독일 주사제 콤플렉스 등의 제조 투자는 세계적인 공급 확보에 있어서 유럽 대륙의 역할을 부각하고 있습니다. 특히 중동유럽에서는 2028년부터 레나카파빌이 저비용 제네릭 의약품과 경쟁할 수 있습니다. EU의 팬데믹 시대 공동 조달 경험은 판매자의 가격 결정력을 재구성 할 수 있는 지역 공동 구매에 활용됩니다.

아시아태평양의 CAGR은 7.12%로 가장 빠르며 중국과 인도가 견인하고 있습니다. 양국의 HIV 감염자 수는 360만 명입니다. 중국의 역학은 현재 이성 간 감염과 노인층에 편향되어 합병증에 대응하는 요법에 대한 수요가 높아지고 있습니다. 국내 제약기업은 항체의약과 장시간 작용형 주사제를 확대하고, 일대일로(Belt and Road)의 '건강의 실크로드'는 아프리카 전역으로의 수출을 촉진하고 있습니다. 인도에서는 제네릭 의약품이 압도적인 점유율을 자랑하고 있으며, 롤러스 랩 등의 기업이 HIV 원약의 생산 능력을 23년도에 CAGR로 27% 확대해, 국내에서의 치료 확대나 국제적인 기증자의 입찰을 지지하고 있습니다.

사하라 이남의 아프리카는 여전히 수량 중심으로 세계의 치료 과정의 절반 이상을 흡수하고 있지만, 기증자의 의존에 따라 금액의 성장은 평평해지고 있습니다. 프라이머리 케어와의 통합이 진행되어 6개월간 여러차례 조제가 이루어지게 되었기 때문에 환자 1인당의 매출은 둔화하고 있지만, 커버리지의 확대에 의해 절대적인 시장 규모는 확대하고 있습니다. 남미와 동유럽은 틈새 성장을 가져오면서도 다양한 상환과 지재 환경에 직면하고 있으며, 이는 콜롬비아의 돌테그라빌 강제 라이선스가 조달 비용을 90% 삭감한 것으로 입증되었습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 세계의 HIV 감염률 상승 및 치료 범위 확대

- 보편적인 ART 접근을 위한 공적 자금 및 기부금 강화

- 신규 장기 작용형 치료제의 지속적인 연구 개발

- ART와 1차 헬스케어 제공 플랫폼의 통합 확대

- 디지털 준수 기술 및 원격 모니터링 확대

- 소아 ART 제제의 신속 규제 패스웨이

- 시장 성장 억제요인

- 지속적인 약제 내성 및 바이러스의 변이

- 장기적인 안전성 우려 및 부작용

- 원료의약품 조달에서 공급망의 취약성

- 제네릭 의약품과의 경쟁에 의한 가격 저하 및 참고 가격 설정

- 규제 상황

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 약제 클래스별

- 프로테아제 억제제

- 인테그라제 억제제

- 멀티 클래스 조합 제품

- 뉴클레오시드 역전사효소 억제제(NRTI)

- 비뉴클레오시드계 역전사효소 억제제(NNRTI)

- 침입 및 융합 억제제

- 기타 약물 클래스

- 레지멘 유형별

- 단정 요법(STR)

- 복수정의 경구요법

- 장시간 작용형 주사제

- 임플란트 및 디포 제제

- 치료 분야별

- 퍼스트 라인

- 세컨드 라인

- 설비 및 서드라인

- 환자의 연령층별

- 성인(15세 이상)

- 청소년(10-14세)

- 소아과(10세 미만)

- 유통 채널별

- 병원 약국

- 소매 약국

- 온라인 약국

- NGO 및 도너 공급망

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Gilead Sciences, Inc.

- ViiV Healthcare(GlaxoSmithKline plc, Pfizer, Shionogi)

- Janssen Pharmaceuticals(Johnson & Johnson)

- Merck & Co., Inc.

- AbbVie Inc.

- Bristol-Myers Squibb Company

- F. Hoffmann-La Roche Ltd

- Boehringer Ingelheim Intl. GmbH

- Cipla Ltd

- Viatris Inc.

- Teva Pharmaceutical Industries Ltd

- Aurobindo Pharma Ltd

- Sun Pharmaceutical Industries Ltd

- Hetero Drugs Ltd

- Lupin Ltd

- Natco Pharma Ltd

- Mylan Laboratories Ltd(Generics)

- Shanghai Desano Pharmaceuticals

- Vistin Pharma ASA

- ViiV Healthcare-s Cabotegravir Partnership Network

제7장 시장 기회 및 향후 전망

AJY 25.11.03The anti-retroviral drugs market size reached USD 31.64 billion in 2025 and is forecast to rise to USD 38.92 billion by 2030, reflecting a 4.23% CAGR over the period.

This measured pace marks a transition from earlier rapid scale-up to a mature phase where innovation, differentiated access strategies and supply-chain resilience steer growth. Long-acting injectables, once-weekly oral regimens and ultra-durable prophylaxis strengthen adherence and open new prevention segments, while integrated primary care delivery and digital adherence tools broaden therapeutic reach. Competitive intensity is rising as blockbuster patents approach expiry, prompting both branded lifecycle extensions and aggressive generic positioning. At the same time, donor financing, tiered-pricing frameworks and local manufacturing investments continue to anchor demand in low- and middle-income countries, which account for almost all new infections.

Global Anti-retroviral Drugs Market Trends and Insights

Rising Global HIV Prevalence and Treatment Coverage Expansion

HIV programmes now target the 33% of people living with the virus who remain untreated, a cohort concentrated in emerging Europe, Central Asia and parts of Latin America. Growing middle-income country budgets, combined with tiered-pricing structures, push the anti-retroviral drugs market into regions where per-capita spending potential is higher than historical Sub-Saharan averages. As more adults age with HIV, comorbidity-tolerant regimens with fewer renal and bone risks gain traction, sustaining volume even where incidence is falling. Universal test-and-treat policies, championed by WHO, keep first-line demand resilient, while scaled viral-load monitoring identifies failure earlier and lifts second-line uptake. These dynamics collectively reinforce a broad base of recurring demand across all lines of therapy.

Enhanced Public and Donor Funding for Universal ART Access

The Global Fund's USD 9.2 billion 2024-2026 allocation underwrites multi-year procurement and strengthens supply chains in 70 countries, anchoring predictable demand for suppliers. PEPFAR's pivot toward country co-financing spurs national budget lines and invites direct manufacturer-government contracts that shorten cash-flow cycles. Advance purchase commitments and voluntary licences, such as Gilead's lenacapavir agreement covering 120 countries, encourage earlier generic ramp-up while protecting inventor margins through royalty structures. Collectively, blended finance mechanisms shield the anti-retroviral drugs market from donor fatigue in the medium term, although future macroeconomic stress in high-income donor nations remains a watch-list risk.

Persistent Drug Resistance and Viral Mutations

WHO surveillance shows dolutegravir resistance of 3.9-8.6% in treatment-naive patients and 19.6% in those previously exposed, pushing payers toward higher-cost salvage regimens. Resistance testing gaps in low-resource settings mask emerging multi-class failures and complicate guideline updates. The additional laboratory and second-line drug costs strain donor budgets and national insurance schemes, while patent-protected rescue therapies further elevate spend. For suppliers, rising resistance reshapes portfolio priorities toward agents with higher genetic barriers and multimodal modes of action, thereby raising R&D budgets and trial complexity.

Other drivers and restraints analyzed in the detailed report include:

- Ongoing Research and Development of Novel Long-Acting Therapies

- Growing Integration of ART With Primary Healthcare Delivery Platforms

- Long-Term Safety Concerns and Adverse Effects

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Multi-class combination pills preserved 38.45% revenue in 2024 through simplified dosing and high resistance barriers that support first-line durability. Integrase inhibitor-anchored regimens posted a 6.53% CAGR, the strongest within this class, propelled by once-daily bictegravir- or dolutegravir-based backbones that maintain >=85% suppression in heavily pre-treated cohorts. Nucleoside reverse transcriptase inhibitors remain a mainstay despite historic bone and renal signals; reformulated tenofovir alafenamide mitigates these risks and extends franchise life. Protease inhibitors continue niche use for boosted salvage regimens but decline as metabolic concerns prompt clinician preference shifts. Novel entry inhibitors and broadly neutralising antibodies, including China's pending albuvirtide, add pipeline diversity but must demonstrate cost-effectiveness to gain guideline prominence.

Integrase-driven durability and once-daily simplicity help this class capture incremental share from NNRTIs, whose vulnerability to single-point mutations curtails uptake. The anti-retroviral drugs market size for integrase-based combinations is projected to surpass USD 18 billion by 2030, reflecting sustained clinical confidence and expanding label indications. Yet, manufacturers must prepare for generic erosion after 2031 as key patents lapse, pressuring them to introduce next-generation boosters or ultra-long-acting depot versions to protect value.

Single-tablet regimens dominated 2024 sales but face heightened competition from depot injections that eliminate daily adherence barriers. The anti-retroviral drugs market share of single-tablet regimens is supported by broad payer familiarity and streamlined distribution, yet their growth moderates to low-single digits as adherence-challenged cohorts pivot to injectables. Long-acting CAB-RPV posted initial uptake in high-income settings, and lenacapavir's six-month dosing interval sets a new convenience benchmark that could shift payer mix toward specialty pharmacy channels.

Implant technologies remain investigational but present disruptive potential, especially for prevention in high-burden youth populations. Manufacturing scale-up for injectables introduces supply-chain fragilities-cold-chain breaks, device shortages-that suppliers must mitigate through dual-site production and buffer inventory. The anti-retroviral drugs market size dedicated to long-acting modalities is expected to register USD 5.4 billion by 2030 at a 6.99% CAGR, with early commercial success hinging on provider training incentives and reimbursement codes for administration services.

The Anti-Retroviral Drugs Market Report is Segmented by Drug Class (Protease Inhibitors, and More), Regimen Type (STRs, Multi-Pill Oral, Long-Acting Injectables, Implants & Depot), Patient Age Group (Adults (>=15 Yrs), and More), Line of Therapy (First-Line, and More), Distribution Channel (Hospital, Retail, and More), and Geography (North America, and More). Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 42.43% of anti-retroviral drugs market revenue in 2024, benefiting from early access to breakthrough designations and insurance coverage that routinely reimburses USD 25,000-30,000 per patient-year. Lenacapavir's FDA approval underscores the region's innovative pull, yet looming patent cliffs for bictegravir (2036) and dolutegravir (2031) invite price erosion and generic challenges. Payer negotiations emphasise outcomes-based discounts, pushing innovators to supply real-world evidence of sustained suppression and improved adherence.

Europe follows with a robust albeit slower growth trajectory. Harmonised HTA frameworks foster simultaneous multi-country launches, while manufacturing investments such as Eli Lilly's USD 2.5 billion German injectable complex highlight the continent's role in global supply security. Cost-effectiveness thresholds drive aggressive tendering, particularly in Central and Eastern Europe, where lenacapavir may compete against lower-cost generics post-2028. EU pandemic-era joint procurement experience informs regional pooled purchasing that could reshape seller pricing power.

Asia-Pacific delivers the fastest regional CAGR at 7.12%, led by China and India, which together house 3.6 million people living with HIV. China's epidemiology now skews toward heterosexual transmission and older age groups, boosting demand for comorbidity-compatible regimens. Domestic champions scale up antibody and long-acting injectables, while the Belt and Road "health silk road" fosters exports across Africa. India leverages its dominant generic base; companies such as Laurus Labs expanded HIV API capacity 27% CAGR in FY23, supporting both local therapy scale-up and international donor tenders.

Sub-Saharan Africa remains volume-centric, absorbing more than half of global treatment courses, yet donor reliance flattens value growth. Enhanced primary-care integration and six-month multi-dispensing blunt per-patient revenue, but expanding coverage lifts absolute market size. South America and Eastern Europe experience resurgent incidence, offering niche growth but confronting diverse reimbursement and IP landscapes, as demonstrated by Colombia's compulsory dolutegravir licence that sliced procurement costs by 90%.

- Gilead Sciences

- ViiV Healthcare (GlaxoSmithKline plc, Pfizer, Shionogi)

- Janssen Pharmaceuticals (Johnson & Johnson)

- Merck

- Abbvie

- Bristol-Myers Squibb

- Roche

- Boehringer Ingelheim Intl. GmbH

- Cipla

- Viatris

- Teva Pharmaceutical Industries

- Aurobindo Pharma

- Sun Pharmaceuticals Industries

- Hetero Drugs Ltd

- Lupin

- Natco Pharma Ltd

- Mylan Laboratories Ltd (Generics)

- Shanghai Desano Pharmaceuticals

- Vistin Pharma ASA

- ViiV Healthcare-s Cabotegravir Partnership Network

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Global HIV Prevalence and Treatment Coverage Expansion

- 4.2.2 Enhanced Public and Donor Funding for Universal ART Access

- 4.2.3 Ongoing Research and Development of Novel Long-Acting Therapies

- 4.2.4 Growing Integration of ART With Primary Healthcare Delivery Platforms

- 4.2.5 Expansion of Digital Adherence Technologies and Remote Monitoring

- 4.2.6 Accelerated Regulatory Pathways for Pediatric ART Formulations

- 4.3 Market Restraints

- 4.3.1 Persistent Drug Resistance and Viral Mutations

- 4.3.2 Long-Term Safety Concerns and Adverse Effects

- 4.3.3 Supply Chain Vulnerabilities in Active Pharmaceutical Ingredient Sourcing

- 4.3.4 Price Erosion from Generic Competition and Reference Pricing

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Drug Class

- 5.1.1 Protease Inhibitors

- 5.1.2 Integrase Inhibitors

- 5.1.3 Multi-class Combination Products

- 5.1.4 Nucleoside Reverse Transcriptase Inhibitors (NRTIs)

- 5.1.5 Non-Nucleoside Reverse Transcriptase Inhibitors (NNRTIs)

- 5.1.6 Entry & Fusion Inhibitors

- 5.1.7 Other Drug Class

- 5.2 By Regimen Type

- 5.2.1 Single-Tablet Regimens (STRs)

- 5.2.2 Multi-pill Oral Regimens

- 5.2.3 Long-Acting Injectables

- 5.2.4 Implants & Depot Formulations

- 5.3 By Line of Therapy

- 5.3.1 First-Line

- 5.3.2 Second-Line

- 5.3.3 Salvage / Third-Line

- 5.4 By Patient Age Group

- 5.4.1 Adults (>=15 yrs)

- 5.4.2 Adolescents (10-14 yrs)

- 5.4.3 Pediatrics (<10 yrs)

- 5.5 By Distribution Channel

- 5.5.1 Hospital Pharmacies

- 5.5.2 Retail Pharmacies

- 5.5.3 Online Pharmacies

- 5.5.4 NGO / Donor Supply Chains

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East & Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East & Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Gilead Sciences, Inc.

- 6.3.2 ViiV Healthcare (GlaxoSmithKline plc, Pfizer, Shionogi)

- 6.3.3 Janssen Pharmaceuticals (Johnson & Johnson)

- 6.3.4 Merck & Co., Inc.

- 6.3.5 AbbVie Inc.

- 6.3.6 Bristol-Myers Squibb Company

- 6.3.7 F. Hoffmann-La Roche Ltd

- 6.3.8 Boehringer Ingelheim Intl. GmbH

- 6.3.9 Cipla Ltd

- 6.3.10 Viatris Inc.

- 6.3.11 Teva Pharmaceutical Industries Ltd

- 6.3.12 Aurobindo Pharma Ltd

- 6.3.13 Sun Pharmaceutical Industries Ltd

- 6.3.14 Hetero Drugs Ltd

- 6.3.15 Lupin Ltd

- 6.3.16 Natco Pharma Ltd

- 6.3.17 Mylan Laboratories Ltd (Generics)

- 6.3.18 Shanghai Desano Pharmaceuticals

- 6.3.19 Vistin Pharma ASA

- 6.3.20 ViiV Healthcare-s Cabotegravir Partnership Network

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment