|

시장보고서

상품코드

1848308

농업용 분무기 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Agricultural Sprayers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

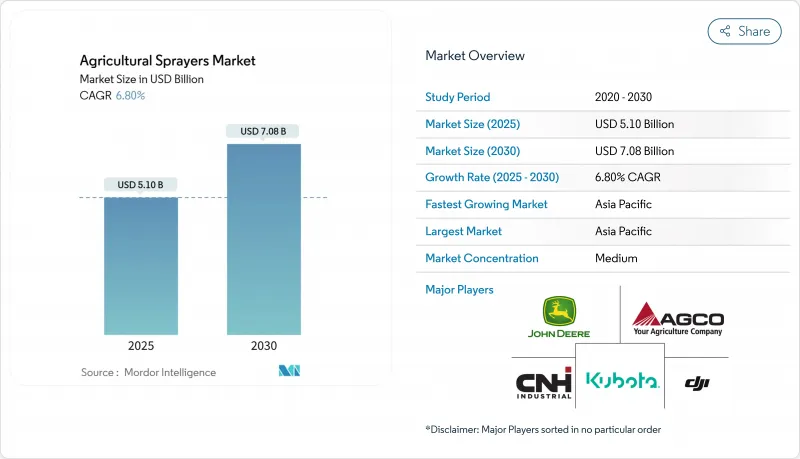

농업용 분무기 시장 규모는 2025년에 51억 달러로 평가되었고, 2030년에 70억 8,000만 달러에 이를 것으로 예측되며, CAGR은 6.80%를 나타낼 전망입니다.

센서, 머신러닝 알고리즘, 가변 속도 기술의 통합으로 기계식 분무기가 정밀한 데이터 기반 플랫폼으로 변모하며 화학 폐기물을 줄이고 증가하는 인건비 문제를 해결하고 있습니다. 아시아태평양 지역은 2024년 최고 매출 점유율로 농업용 분무기 시장을 주도하고 있으며, 이는 스마트 기계 도입을 장려하는 중국과 인도 정부의 보조금 프로그램에 힘입은 바 크다. 농민들이 운영 비용 절감과 탄소 배출권 획득을 우선시함에 따라 배터리 구동형 장비가 가장 빠른 성장세를 보이고 있습니다. 규제 체계가 발전함에 따라 드론 및 자율주행 분무기는 시범 단계에서 상업적 적용으로 전환되고 있으며, 인공지능 기반 시스템은 농약 사용량을 크게 줄이는 것으로 입증되고 있습니다. 글로벌 OEM 업체들이 장비에 비전 시스템과 분석 기능을 통합하고, 중소 기업들이 기존 장비 군을 업그레이드하기 위한 개조 키트를 출시함에 따라 시장 경쟁이 심화되고 있습니다.

세계의 농업용 분무기 시장 동향 및 인사이트

농약 사용량 증가

2022년 농약 수요는 전년 대비 4% 증가한 370만 톤을 기록했으며, 이는 1990년 대비 거의 두 배에 달하는 수준으로, 농가들은 정밀 살포가 가능한 대용량 장비를 확보해야 하는 상황입니다. 전 세계 농약 판매량은 특히 특수 노즐이 필요한 제초제 분야에서 지속적으로 증가하고 있습니다. 중국에서는 2025년까지 식물 보호용 드론 수요가 6만 대를 넘어설 것으로 예상되며, 서비스 제공업체들의 장비 확대로 농업용 스프레이어 시장이 확대되고 있습니다. 생물학적 제품 및 정밀 제형으로의 전환은 기존 화학 제품에 비해 더 구체적인 살포 매개변수가 필요한 만큼, 향상된 제어 시스템을 갖춘 스프레이어를 요구합니다. 브라질의 생물학적 투입재 부문은 지난 시즌 처리 면적을 35% 이상 증가시켜 살아있는 미생물 적용을 위한 초저용량 분무기 투자 증가를 주도했습니다.

노즐, 센서, AI 기반 제어의 기술 발전

존 디어의 ‘시 앤 스프레이(See and Spray)’ 시스템은 대규모 시험에서 제초제 사용량을 77% 줄이면서도 잡초 방제 효과를 유지하여 내장형 비전 및 딥러닝 모델의 효능을 입증했습니다. 2026년 가디언(Guardian) 분무기에 적용 예정인 뉴홀랜드(New Holland)의 인텔리센스(IntelliSense) 자동화 시스템은 캔자스 현장 시험에서 시속 25마일(약 40km) 작업 속도에서 질소 사용량을 10% 절감했으며, 이는 생산성 향상과 투입 비용 감소 간의 상관관계를 입증하여 농업용 분무기 시장 전반에 걸친 채택을 촉진하고 있습니다. 2025년 월드 애그 엑스포에서 주목받은 에코로보틱스의 카메라 장착 ARA 플랫폼은 센티미터 단위 정밀도를 달성하며 자동화 살포 기술의 진화를 보여줍니다.

고액의 초기 설비 투자 및 자금 조달 장애물

200마력 트랙터 가격은 1990년 이후 287% 상승하여 농가 물가 상승률을 크게 웃돌았으며, 금리는 2017년 이후 213% 급등하여 많은 농가가 현재 거래의 11%를 차지하는 리스 계약으로 몰리게 되었습니다. 순 현금 농가 소득은 2024년 약 20% 하락할 것으로 예상되어 신규 분무기 구입을 위한 유동성이 축소될 전망입니다. 중고 장비 목록은 과잉 공급 상태이며, 딜러들이 재고를 줄이면서 경매 낙찰률은 상승 중입니다. 화학약품, 비료, 기계류 등 투입 비용은 2011년 이후 37.5% 증가하여 농가 수익성과 장비 구매 결정에 복합적인 압박을 가하고 있습니다. 캐나다 농기계 판매 역시 유사한 도전에 직면해 있으며, 상품 가격 하락, 높은 운영 비용, 수익 감소로 인해 수요가 약화되어 2025년 판매가 제한될 전망입니다. 특히 트랙터와 콤바인 같은 대형 장비 부문에 큰 영향을 미칠 것으로 예상됩니다.

부문 분석

연료 구동식 분무기는 광범위한 급유 인프라와 장시간 현장 작업에서의 안정적인 성능을 바탕으로 2024년 매출 점유율 47.0%로 농업용 분무기 시장을 주도했습니다. 현재 시장 점유율이 낮은 배터리 구동식 장비는 운영 비용 절감, 탄소 배출권 인센티브, 디젤 가격 상승에 힘입어 2030년까지 연평균 17.9%의 성장률을 보일 것으로 전망됩니다. 연구에 따르면 자율 주행 전기 트랙터는 디젤 대체품 대비 온실가스 배출량이 72% 낮습니다. EU 규정 2023/1542 시행으로 배터리 재활용 함량 및 탄소 발자국 표시가 의무화되어 규정 준수 비용이 증가할 수 있으나, 지역 배터리 재활용 산업 발전을 촉진할 전망입니다.

농업용 분무기에는 특히 전기 충전 인프라가 제한된 외딴 농업 지역에서 내연기관이 여전히 널리 사용됩니다. 제조사들은 하이브리드 시스템과 배터리 전환 키트 도입으로 시장 변화에 대응하고 있습니다. 존 디어(John Deere)와 GUSS 오토메이션(GUSS Automation)은 2024년 말 전기 분무기 모델을 출시했으며, 쿠보타(Kubota)는 특수 작물용 전기 트랙터 개발을 위해 애그토노미(Agtonomy)와 협력했습니다. 아시아-태평양 지역에서는 태양광 충전 시설을 지원하는 정부 정책이 전기식 분무기 기술로의 점진적 시장 전환을 시사합니다.

트랙터 장착형 분무기는 부착 호환성과 자체 추진형 대비 비용 이점으로 2024년 판매량의 36.5%를 차지했습니다. 농업용 드론은 간소화된 면허 요건과 가파른 지형 또는 침수된 지역에서의 운용 능력으로 인해 연평균 20.2%의 성장률을 보입니다. 미주리 연구에 따르면 연간 처리 면적이 980에이커를 초과할 때 드론 소유가 경제적으로 타당해지며, 소유자의 운영 비용은 에이커당 12.27달러인 반면 위탁 서비스 비용은 7.39달러입니다.

자주식 기계는 대규모 북미 농업 운영에 여전히 필수적입니다. 2025년 6월 출시된 John Deere 500R은 향상된 운전자 시야와 PowrSpray 배관 기술을 적용해 98%의 살포 정밀도를 제공합니다. 소규모 농업에서는 자본 투자 감소와 우수한 유출 관리 능력으로 인해 배낭형 장비가 특수 작물 살포에 여전히 적합합니다. 농업용 분무기 기술의 이러한 시장 세분화는 자율 시스템이 기존 장비 범주를 계속 변화시키는 가운데 지속될 전망입니다.

지역 분석

아시아태평양 지역은 2024년 35.7% 점유율로 농업용 분무기 시장을 주도하며 연간 8.0% 성장률을 기록할 전망입니다. 중국은 크롤러 트랙터 및 스마트 농기구를 우선 지원하는 방식으로 보조금 구조를 개편했으며, 인도의 농업 기계화 하위 사업(SMAM)은 소규모 농가의 분무기 구매 비용의 최대 80%를 지원합니다. 기계화 추세는 환경 목표와 부합하는데, 연구에 따르면 초기 트랙터 도입은 배출량을 증가시켰으나 이후 정밀 시스템 도입으로 환경 영향이 감소하는 U자형 배출 패턴이 나타났습니다.

북미는 기술적으로 선진적인 시장 위치를 유지하고 있습니다. 2024년 ‘시 앤 스프레이(See and Spray)’ 기술은 100만 에이커 이상을 커버하며 제초제 사용량을 800만 갤런(약 3,028만 리터) 절감했습니다. 그러나 2024년 농가 현금 소득 20% 감소 전망과 금리 인상으로 장비 투자 회수 기간이 연장되며 시장이 도전에 직면했습니다. 정밀농업 장비 비용 환급을 포함한 기후 스마트 시범 프로그램에 대한 미국 농무부(USDA)의 30억 달러 배정은 시장 둔화 영향을 완화하는 데 기여합니다.

유럽의 농업용 분무기 시장 성장은 규제 정책에서 비롯됩니다. EU 배터리 규정은 재활용 소재 사용 의무를 시행하여 2028년 이후 전기식 분무기 사양에 영향을 미칠 것입니다. 이 지역 주요 살포 장비 제조사인 엑셀 인더스트리즈(EXEL Industries)는 2023-2024 회계연도에 농업 부문 매출 5억 7,810만 달러(5억 300만 유로)를 기록했으며, 이는 총 매출의 46%를 차지했습니다. 다만 농민들의 장비 교체 연기 현상으로 주문량이 감소한 점을 언급했습니다. 환경 규제와 그린딜 요건은 정밀 장비 도입을 지속적으로 촉진하여 어려운 경제 상황 속에서도 시장 안정성을 뒷받침하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 농약 사용량 증가

- 노즐, 센서, AI 기반의 제어에 있어서의 기술의 진보

- 인건비 상승과 심각한 작업자 부족

- 정부의 기계화와 스마트 농업에의 보조금

- 가변적 적용률에 대한 보상형 탄소 크레딧 프로그램

- 자율 분무기의 상업화

- 시장 성장 억제요인

- 고액의 초기 자본 지출과 자금 조달의 장애물

- 제한된 농업 전문가 또는 작업자 기술 역량

- 사이버 보안 및 데이터 무결성의 위험

- 배터리의 수명 종료시의 폐기 제약

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측(가치와 양)

- 동력원별

- 수동식

- 전지식/전동식

- 태양광 발전

- 연료 구동식

- 제품 유형별

- 핸드헬드/배낭형

- 트랙터 장착형

- 주도식

- 자주식

- UAV/드론 분무기

- 용도별

- 밭작물

- 과수원과 포도원

- 온실작물

- 잔디와 원예

- 분무기 용량별

- 초저용량

- 저용량

- 고용량

- 기술 수준별

- 기존

- 정밀/GPS 가이드

- AI 지원 및 자율

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 기타 북미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Deere & Company

- AGCO Corporation

- CNH Industrial NV

- Mahindra & Mahindra Ltd.

- Kubota Corporation

- DJI

- Exel Industries

- KUHN SAS

- ASPEE Agro Equipment Pvt. Ltd.

- Hockley International Ltd

- Jacto SA

- GUSS Automation LLC

- Yamaha Motor Co., Ltd.

- Hylio, Inc.

- Goldacres Pty Ltd

- Chafer Machinery Ltd.

제7장 시장 기회와 장래의 전망

HBR 25.11.12The agricultural sprayers market size is valued at USD 5.10 billion in 2025 and is projected to reach USD 7.08 billion by 2030, growing at a CAGR of 6.80%.

The integration of sensors, machine-learning algorithms, and variable-rate technologies is transforming mechanical sprayers into precise, data-driven platforms that reduce chemical waste and address increasing labor costs. The Asia-Pacific region dominates the agricultural sprayers market with the highest revenue share in 2024, supported by Chinese and Indian government subsidy programs that promote smart machinery adoption. Battery-powered units show the fastest growth as farmers prioritize reduced operating costs and carbon credits. Drone and autonomous sprayers are transitioning from pilot scale to commercial applications as regulatory frameworks develop, while AI-enabled systems demonstrate significant reductions in agrochemical usage. Market competition is intensifying as global OEMs integrate vision systems and analytics with equipment, and smaller companies introduce retrofit kits to upgrade existing fleets.

Global Agricultural Sprayers Market Trends and Insights

Growth in Agrochemical Usage

Pesticide demand reached 3.70 million metric tons in 2022, up 4% year on year and nearly double 1990 levels, compelling growers to acquire equipment capable of handling larger volumes with precise application. Global agrochemical sales continue to increase, particularly in herbicides that require specialized nozzles. In China, plant-protection drone demand is projected to exceed 60,000 units by 2025, expanding the agricultural sprayers market as service providers increase their fleets. The transition toward biological products and precision formulations necessitates sprayers with enhanced control systems, as these products require more specific application parameters compared to conventional chemicals. Brazil's bio-input segment increased treated acreage by more than 35% in the last season, driving investment in ultra-low-volume sprayers designed for live microbe applications.

Technological Advancements in Nozzle, Sensor and AI-Based Control

John Deere's See and Spray system demonstrated a 77% reduction in herbicide usage during broad-acre trials while maintaining weed control effectiveness, validating the efficacy of embedded vision and deep-learning models. New Holland's IntelliSense automation system, scheduled for implementation in 2026 Guardian sprayers, demonstrated 10% nitrogen reduction at 25 mph field speeds during Kansas field trials, establishing the correlation between enhanced productivity and decreased input costs, boosting adoption across the agricultural sprayer market. Ecorobotix's camera-equipped ARA platform, which received recognition at World Ag Expo 2025, achieves centimeter-level precision, indicating the evolution of automated spray applications.

High Upfront Capital Expenditure and Financing Hurdles

Prices for 200-horsepower tractors have climbed 287% since 1990, far outpacing farm-gate inflation, and interest rates have soared 213% since 2017, pushing many growers toward leases that now cover 11% of deals. Net cash farm income is forecast to fall nearly 20% in 2024, shrinking liquidity for new sprayers. Used equipment lists are bloated, and auction clearance rates are rising as dealers trim inventory. Input costs for chemicals, fertilizers, and machinery have increased 37.5% since 2011, creating compound pressure on farm profitability and equipment purchasing decisions. Canadian farm equipment sales face similar challenges, with weak demand limiting 2025 sales due to falling commodity prices, high operating costs, and reduced profits, particularly affecting large equipment categories like tractors and combines.

Other drivers and restraints analyzed in the detailed report include:

- Rising Labor-Cost and Acute Operator Shortages

- Government Mechanization and Smart-Farming Subsidies

- Limited Agronomist or Operator Skill Sets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fuel-powered sprayers dominated the agricultural sprayers market with a 47.0% revenue share in 2024, supported by widespread refueling infrastructure and reliable performance in extended field operations. Battery-powered units, currently representing a smaller market segment, are projected to grow at a 17.9% CAGR through 2030, driven by reduced operational costs, carbon credit incentives, and increasing diesel prices. Research indicates that autonomous electric tractors generate 72% lower greenhouse gas emissions compared to diesel alternatives. The EU Regulation 2023/1542 implementation requires recycled content and carbon-footprint labeling for batteries, potentially increasing compliance expenses while encouraging regional battery recycling development.

Combustion engines remain prevalent in agricultural sprayers, particularly in remote farming areas with limited electric charging infrastructure. Manufacturers are adapting to market changes by introducing hybrid systems and battery conversion kits. John Deere and GUSS Automation introduced an electric sprayer variant in late 2024, while Kubota partnered with Agtonomy to develop electric tractors for specialty crop applications. In the Asia-Pacific region, government initiatives supporting solar-powered charging facilities indicate a gradual market transition toward electric sprayer technologies.

Tractor-mounted sprayers constituted 36.5% of 2024 sales due to their attachment compatibility and cost advantages compared to self-propelled units. Agricultural drones demonstrate a 20.2% CAGR, attributed to streamlined licensing requirements and their capability to operate in steep or waterlogged terrain. Missouri research indicates that drone ownership becomes economically viable when annual treated areas exceed 980 acres, with operational costs of USD 12.27 per acre for owners compared to USD 7.39 for custom hiring services.

Self-propelled machines remain essential for large-scale North American agricultural operations. The John Deere 500R, released in June 2025, incorporates enhanced operator visibility and PowrSpray plumbing technology, delivering 98% application precision. In small-scale farming operations, knapsack units maintain their relevance for specialized crop applications due to reduced capital requirements and superior drift management. This market segmentation in agricultural sprayer technology persists while autonomous systems continue to transform traditional equipment categories.

The Agricultural Sprayers Market Report is Segmented by Source of Power (Manual, and More), by Product Type (Handheld/Knapsack, Tractor-Mounted, and More), by Application/Usage (Field Crops, and More), by Spray Volume Capacity (Ultra-Low Volume, and More), Technology Level (Conventional, and More), and by Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Asia-Pacific dominates the agricultural sprayers market with a 35.7% share in 2024 and projects an 8.0% annual growth rate. China has modified its subsidy structure to prioritize crawler tractors and smart implements, while India's Sub-Mission on Agricultural Mechanization (SMAM) provides up to 80% cost coverage for smallholder sprayer purchases. The mechanization trend aligns with environmental objectives, as research indicates a U-shaped emissions pattern where initial tractor adoption increased emissions, but subsequent precision system implementation reduced environmental impact.

North America maintains a technologically advanced market position. In 2024, See and Spray technology covered more than 1 million acres, reducing herbicide usage by 8 million gallons. However, the market faces challenges from a projected 20% decrease in 2024 cash farm income and increased interest rates, extending equipment investment recovery periods. The USDA's USD 3 billion allocation for climate-smart pilot programs, which includes precision agriculture equipment reimbursement, helps mitigate market slowdown impacts.

Europe's agricultural sprayers market growth stems from regulatory initiatives. The EU Battery Regulation implements recycled-content requirements that will influence electric sprayer specifications post-2028. EXEL Industries, the region's primary spray equipment manufacturer, reported agriculture revenue of USD 578.1 million (Euro 503 million) in fiscal 2023-2024, comprising 46% of total revenue, despite noting reduced orders due to farmers postponing equipment updates. Environmental regulations and green-deal requirements continue to drive precision equipment adoption, supporting market stability despite challenging economic conditions.

- Deere & Company

- AGCO Corporation

- CNH Industrial N.V.

- Mahindra & Mahindra Ltd.

- Kubota Corporation

- DJI

- Exel Industries

- KUHN SAS

- ASPEE Agro Equipment Pvt. Ltd.

- Hockley International Ltd

- Jacto S.A.

- GUSS Automation LLC

- Yamaha Motor Co., Ltd.

- Hylio, Inc.

- Goldacres Pty Ltd

- Chafer Machinery Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth in Agrochemical Usage

- 4.2.2 Technological Advancements in Nozzle, Sensor and AI-Based Control

- 4.2.3 Rising Labor-Cost and Acute Operator Shortages

- 4.2.4 Government Mechanization and Smart-Farming Subsidies

- 4.2.5 Carbon-Credit Programs Rewarding Variable-Rate Applications

- 4.2.6 Commercialization of Autonomous Sprayers

- 4.3 Market Restraints

- 4.3.1 High Upfront Capital Expenditure and Financing Hurdles

- 4.3.2 Limited Agronomist or Operator Skill Sets

- 4.3.3 Cyber-Security and Data-Integrity Risks

- 4.3.4 Battery End-of-Life Disposal Constraints

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Source of Power

- 5.1.1 Manual

- 5.1.2 Battery-Operated/Electric

- 5.1.3 Solar-Powered

- 5.1.4 Fuel-Operated

- 5.2 By Product Type

- 5.2.1 Handheld/Knapsack

- 5.2.2 Tractor-Mounted

- 5.2.3 Trailed/Pull-Type

- 5.2.4 Self-Propelled

- 5.2.5 UAV/Drone Sprayers

- 5.3 By Application/Usage

- 5.3.1 Field Crops

- 5.3.2 Orchards and Vineyards

- 5.3.3 Greenhouse Crops

- 5.3.4 Turf and Gardening

- 5.4 By Spray Volume Capacity

- 5.4.1 Ultra-Low Volume

- 5.4.2 Low Volume

- 5.4.3 High Volume

- 5.5 By Technology Level

- 5.5.1 Conventional

- 5.5.2 Precision/GPS-Guided

- 5.5.3 AI-Enabled and Autonomous

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.1.4 Rest of North America

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 UAE

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Rest of Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Deere & Company

- 6.4.2 AGCO Corporation

- 6.4.3 CNH Industrial N.V.

- 6.4.4 Mahindra & Mahindra Ltd.

- 6.4.5 Kubota Corporation

- 6.4.6 DJI

- 6.4.7 Exel Industries

- 6.4.8 KUHN SAS

- 6.4.9 ASPEE Agro Equipment Pvt. Ltd.

- 6.4.10 Hockley International Ltd

- 6.4.11 Jacto S.A.

- 6.4.12 GUSS Automation LLC

- 6.4.13 Yamaha Motor Co., Ltd.

- 6.4.14 Hylio, Inc.

- 6.4.15 Goldacres Pty Ltd

- 6.4.16 Chafer Machinery Ltd.