|

시장보고서

상품코드

1848314

세포 채취 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Cell Harvesting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

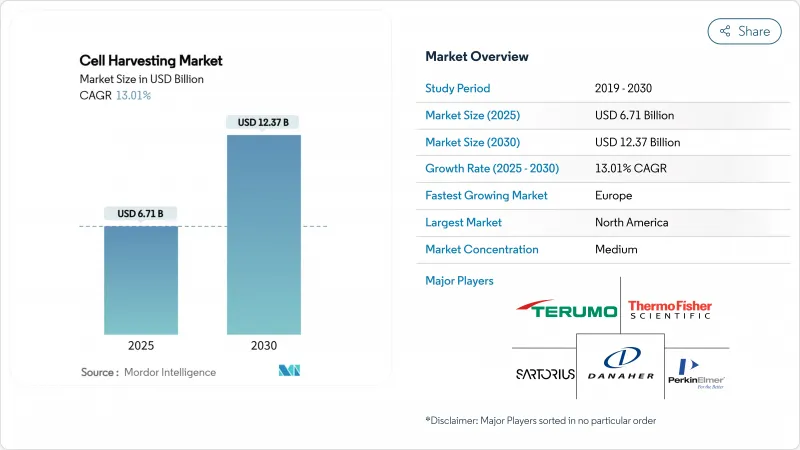

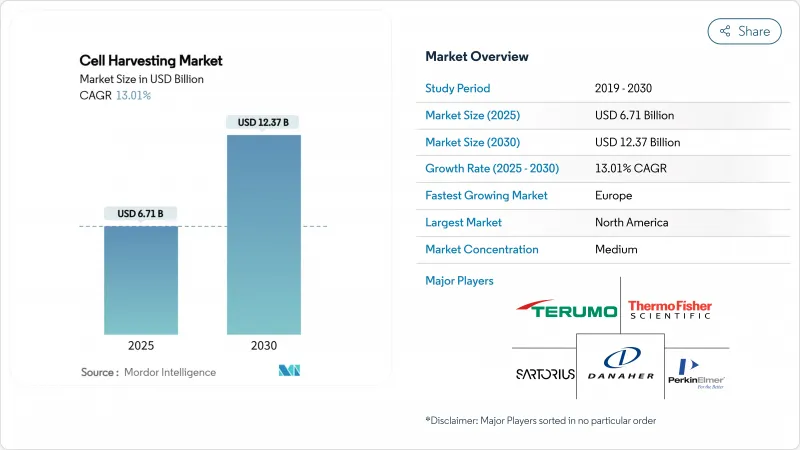

세포 채취 시장 규모는 2025년 67억 1,000만 달러로 추정되고, 2030년 123억 7,000만 달러로 성장할 것으로 예측되며, CAGR 13.01%로 성장할 전망입니다.

노동 요건을 최대 75%까지 줄이고 배치 일관성을 향상시키는 고급 밀폐형 자동 채취기의 보급이 성장의 주요 촉매입니다. 지난 10년간 23억 달러에 이르는 관민의 자금 조달, 연간 10-20개의 세포 및 유전자 치료를 승인하는 규제 당국의 헌신, 포인트 오브 케어(PoC) 제조 허브에 대한 공급망 투자가 이 확대를 뒷받침하고 있습니다. 북미의 조기 어댑터 수요, 아시아태평양의 생산 능력 증대, AI 애널리틱스와 일회용 하드웨어를 결합한 지속적인 플랫폼 혁신이 더욱 기세를 창출하고 있습니다.

세계의 세포 채취 시장 동향 및 인사이트

세포 및 유전자 치료에 대한 투자 확대

지난 10년간 23억 달러 이상의 자본이 세포 및 유전자 치료 벤처에 투입되어 세계 1,500건이 넘는 활발한 임상 연구가 진행되고 있습니다. FDA는 2024년 최초의 중간엽 간질 세포 제품인 Ryoncil을 포함한 8가지 새로운 첨단 요법을 허가하여 복잡한 생물학적 제제에 대한 규제 당국의 신뢰를 보였습니다. 제약 대기업은 급속히 규모를 확대하고 있습니다. 브리스톨 마이어스 스퀴브는 3개의 CAR-T 전용 공장을 개설하고, 아스트라제네카는 4억 2,500만 달러를 투입해 에소바이오텍사를 인수해, in vivo 프로그램을 가속시켰습니다. 자본 유입은 개발 일정을 단축하고 신뢰할 수 있는 높은 처리량 채취기를 필요로 하는 자가 및 동종 배치 양을 증가시킵니다. 투자자들은 현재 다제품 파이프라인을 지원할 수 있는 플랫폼을 선호하고 있으며 모듈식 애드온을 갖춘 통합 채취기의 매력을 높이고 있습니다.

바이오 의약품 제조 인프라 확대

후지 필름 디오신스의 덴마크-텍사스 사이의 16억 달러 확장은 8개의 20,000리터 바이오 리액터와 특수 다운 스트림 스위트를 추가하고, 롯데 바이오로직은 2027년까지 120,000리터의 용량을 달성하기 위해 마츠시마 바이오 캠퍼스에 10억 달러를 약속하고 있습니다. 이러한 메가 프로젝트는 일회용 및 스테인레스 스틸 트레인 모두에 해당하는 채취기를 필요로 하는 지역 클러스터를 생성합니다. 많은 CDMO가 여전히 50% 이하의 가동률로 운영되고 있기 때문에 오늘은 임상 규모의 자기 제형을 비용 효율적으로 처리하고 내일은 대규모 동종 제제를 처리할 수 있는 유연한 시스템이 요구되고 있습니다. 교환 가능한 원심분리 또는 여과 요소를 갖춘 모듈식 스키드 구조를 제공하는 아키텍처는 이 가동률 갭을 해결하고 생산 우선순위 변경에 따라 신속하게 재배치할 수 있습니다.

줄기세포 조달을 둘러싼 윤리적 및 규제적 우려

재주입된 세포는 FDA의 생물제제 규제의 대상이 되는 것이 미국의 항소법원에서 확인된 후 배아 줄기세포 연구와 미확인 지방유래처리는 감시의 강화에 직면하고 있습니다. EU, 미국, 아시아에서 서로 다른 기증자의 스크리닝 규칙은 다자간 연구를 복잡하게 하고 문서화 비용을 증가시키고 있습니다. 시행이 완만한 지역에서 기적적인 치료법을 홍보하는 무인가 클리닉이 사회적 신용을 저해하고, 규제 당국이 경고서를 발표하거나 클리닉의 폐쇄를 의무화합니다. 윤리적 조달과 GMP 출처를 문서화하는 컴플라이언스 준수 공급업체는 차별화를 도모할 수 있지만 국가마다 다른 동의 요건과 조직 은행 감사의 진화를 극복해야 합니다.

부문 분석

자동화 시스템은 근무 시간과 오염 위험을 줄이는 폐쇄적이고 프로그래밍 가능한 워크플로우로 2024년 세포 채취 시장 점유율의 63.45%를 차지했습니다. 2030년까지 연평균 복합 성장률(CAGR) 15.45%로 성장이 예측됩니다. 수작업으로 채취기는 탐험 작업과 변동이 심한 초기 단계의 프로토콜에 적합합니다. 그러나 아카데믹한 실험실조차도 기존의 인큐베이터에 볼트로 장착하는 반자동 모듈을 채택하여 촉각 모니터링과 디지털 모니터링을 융합시키고 있습니다. 연속 처리 및 일회용 어셈블리로의 업계 전반적인 전환은 10년 후까지 자동화 시스템을 세포 채취 시장 규모의 70% 이상으로 밀어올릴 것으로 보입니다.

자동화의 기세는 공장 디지털화의 목표와 일치합니다. 벤더는 라인의 클리어런스와 밸리데이션을 간소화하기 위해 원심분리, 여과, 세척을 하나의 섀시에 통합하고 있습니다. 원격 진단 및 소프트웨어 업데이트는 다운타임을 단축하고 성능을 사양 내에 유지합니다. 여러 관할 구역에서 시스템을 인증하고 24시간 부품 지원을 제공할 수 있는 공급업체는 세계 시험이 확대됨에 따라 경쟁력을 확보하고 있습니다.

지역 분석

북미는 성숙한 CGT 규제 프레임워크, 광범위한 CDMO 네트워크, 전문적인 물류 사업자의 지원을 받아 2024년 세계 매출의 39.42%를 차지했습니다. 그러나 2024년에 미국 적격 환자의 20% 미만만 이용 가능한 치료법에 액세스할 수 없었고, 자동 채취기가 경감할 수 있는 프로세스의 비효율성이 부각되고 있습니다. 지역의 성장은 숙련 노동자 공급에도 의존하기 때문에 기술자 육성을 위한 장비 벤더와 커뮤니티 칼리지의 제휴 프로그램이 촉구되고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR) 14.56%로 확대될 것으로 예측됩니다. 중국은 2024년에 세계 CGT 임상시험의 37%를 실시했으며, 일본의 패스트트랙과 한국의 재생의료법은 승인 스케줄을 단축했습니다. WuXi AppTec 및 SK Bioscience와 같은 국내 기업은 CGT 허브에 많은 투자를 하고 있으며 현지 GMP 가이드라인에 맞는 수확 모듈의 대량 주문을 추진하고 있습니다. 운영 비용 감소, 정부 우대 조치, 만성 질환 이환율 증가가 수요를 확대하고 있지만 공급업체는 진화하는 수입 규제 및 다국어 품질 문서에 적응해야 합니다.

유럽은 일관된 EMA 지침과 덴마크, 아일랜드, 독일의 견고한 CDMO 인프라를 통해 상당한 점유율을 유지하고 있습니다. 후지필름 지오신스의 덴마크 공장 확장은 지역의 자급률 향상을 목표로 한 지속적인 자본 유입의 예입니다. 에너지 비용은 시설에 짧은 사이클 시간에 에너지 효율적인 수확기를 채택하도록 촉구하고 있습니다. 중동 및 아프리카와 남미는 헬스케어 시스템이 제3차 의료에 투자하고 양자 간 기술 이전 협정을 수립하고 있기 때문에 새로운 기회 영역이 되었습니다. 전력 변동을 견디는 컴팩트하고 견고한 채취기는 이러한 지역에서 인기가 높아지고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 세포 및 유전자 치료에 대한 투자 증가

- 바이오 의약품 제조 인프라 확대

- 세포 치료가 필요한 만성질환의 유병률 상승

- 자동 세포 처리에서 기술적 진보

- 선진 치료를 지원하는 규제 틀

- 개인화된 포인트 오브 케어 세포 치료 플랫폼의 출현

- 시장 성장 억제요인

- 줄기세포 조달에 관한 윤리적 및 규제 상의 우려

- 자동 채취 시스템의 고비용

- 도너 유래 세포에서의 변동성 및 품질 관리의 과제

- 살아있는 세포의 콜드체인 및 물류의 복잡성

- 규제 상황

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력 및 소비자

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 세포 채취 유형별

- 수동 세포 채취기

- 자동 세포 채취기

- 용도별

- 바이오의약품에 대한 용도

- 줄기세포 연구

- 기타 용도

- 최종 사용자별

- 바이오테크놀러지 및 바이오의약품 기업

- 연구기관

- 기타 최종 사용자

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Thermo Fisher Scientific

- Danaher(Cytiva, Beckman Coulter)

- Sartorius AG

- Miltenyi Biotec

- Becton Dickinson & Co.

- Lonza Group

- STEMCELL Technologies

- Corning Inc.

- PerkinElmer Inc.

- Eppendorf SE

- Greiner Bio-One

- Eurofins Scientific

- Terumo Corporation

- Nipro Corporation

- Tomtec Inc.

- Alcami Corporation

- Esco Lifesciences

- PromoCell GmbH

- CellGenix GmbH

- Regen Lab SA

- PluriStem Therapeutics

제7장 시장 기회 및 향후 전망

AJY 25.11.03The cell harvesting market size is USD 6.71 billion in 2025 and will rise to USD 12.37 billion by 2030, reflecting a 13.01% CAGR.

Widespread adoption of advanced, closed, and automated harvesters that cut labor requirements by up to 75% and improve batch consistency is the prime growth catalyst. Public- and private-sector financing worth USD 2.3 billion over the past decade, regulatory commitments to approve 10-20 cell and gene therapies per year, and supply-chain investments in point-of-care (PoC) manufacturing hubs reinforce this expansion. North American early-adopter demand, Asia-Pacific capacity build-outs, and continuous platform innovation that combines AI analytics with single-use hardware create additional momentum.

Global Cell Harvesting Market Trends and Insights

Growing Investment in Cell and Gene Therapies

More than USD 2.3 billion in equity has entered cell and gene therapy ventures during the last decade, underpinning over 1,500 active clinical studies worldwide. The FDA cleared eight novel advanced therapies in 2024, including the first mesenchymal stromal cell product, Ryoncil, demonstrating regulatory confidence in complex biologics. Pharmaceutical majors are scaling quickly: Bristol Myers Squibb opened three dedicated CAR-T plants, and AstraZeneca spent USD 425 million for EsoBiotec to accelerate in vivo programs. Capital inflows shorten development timelines and increase the volume of autologous and allogeneic batches that require reliable, high-throughput harvesters. Investors now prioritize platforms that can support multiproduct pipelines, lifting the appeal of integrated harvest devices with modular add-ons.

Expansion of Biopharmaceutical Manufacturing Infrastructure

Fujifilm Diosynth's USD 1.6 billion Denmark-Texas expansion adds eight 20,000 L bioreactors and specialized downstream suites, while Lotte Biologics is committing USD 1 billion for its Songdo Bio Campus to reach 120,000 L capacity by 2027. Such mega-projects create regional clusters that need harvesters compatible with both single-use and stainless-steel trains. Many CDMOs still operate at less than 50% utilization, prompting demand for flexible systems that can cost-effectively handle clinical-scale autologous lots today and pivot to large allogeneic runs tomorrow. Suppliers offering modular skid architecture with interchangeable centrifugation or filtration elements address this utilization gap and can be rapidly redeployed as production priorities change.

Ethical and Regulatory Concerns Around Stem Cell Sourcing

Embryonic stem cell research and unproven adipose-derived procedures face increased oversight after U.S. appellate courts confirmed that reinjected cells fall under FDA biologics regulation. Divergent donor screening rules in the EU, United States, and Asia complicate multinational studies and raise documentation costs. Unlicensed clinics advertising miracle cures in regions with light enforcement undermine public confidence, prompting regulators to publish warning letters and mandate clinic closures. Compliant suppliers that document ethical sourcing and GMP provenance can differentiate, but they must navigate evolving consent requirements and tissue-bank audits that vary by country.

Other drivers and restraints analyzed in the detailed report include:

- Rising Prevalence of Chronic Diseases Requiring Cell Therapies

- Technological Advancements in Automated Cell Processing

- High Cost of Automated Harvesting Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Automated systems held 63.45% of the cell harvesting market share in 2024 thanks to closed, programmable workflows that cut labor hours and contamination risk. They are projected to record a 15.45% CAGR through 2030. Manual harvesters remain relevant for exploratory work or highly variable early-phase protocols that benefit from hands-on manipulation. However, even academic labs are adopting semi-automated modules that bolt onto legacy incubators, blending tactile oversight with digital monitoring. Industry-wide migration toward continuous processing and single-use assemblies will likely elevate automated systems to more than 70% of the cell harvesting market size by decade's end.

Automation's momentum aligns with factory digitization goals. Vendors are bundling integrated centrifugation, filtration, and washing in one chassis to streamline line clearance and validation. Remote diagnostics and software updates provide shorter downtimes and keep performance within specification. Suppliers able to certify systems in multiple jurisdictions and offer 24-hour parts support gain a competitive edge as global trials expand.

The Cell Harvesting Market Report is Segmented by Type of Cell Harvesting (Manual Cell Harvesters and Automated Cell Harvesters), Application (Biopharmaceutical Application, Stem-Cell Research, and Other Applications), End User (Biotechnology & Biopharmaceutical Companies, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 39.42% of global revenue in 2024, supported by a mature CGT regulatory framework, extensive CDMO network, and specialized logistics operators. Yet fewer than 20% of eligible U.S. patients accessed available therapies in 2024, underscoring process inefficiencies that automated harvesters can mitigate. Regional growth also depends on skilled labor supply, prompting partnership programs between equipment vendors and community colleges to cultivate technicians.

Asia-Pacific is projected to expand at 14.56% CAGR to 2030. China hosted 37% of global CGT trials in 2024, and Japan's Fast Track and South Korea's Regenerative Medicine Law cut approval timelines. Domestic players like WuXi AppTec and SK Bioscience have invested heavily in CGT hubs, driving bulk orders for harvest modules compatible with local GMP guidelines. Lower operating costs, government incentives, and rising chronic-disease prevalence amplify demand, but suppliers must adapt to evolving import regulations and multilingual quality documentation.

Europe maintains a sizable share anchored by harmonized EMA guidelines and robust CDMO infrastructure in Denmark, Ireland, and Germany. Fujifilm Diosynth's Danish plant expansion exemplifies continued capital inflow aimed at increasing regional self-sufficiency. Energy costs push facilities to adopt energy-efficient harvesters with shorter cycle times. The Middle East & Africa and South America are emerging opportunity zones as healthcare systems invest in tertiary care and establish bilateral technology-transfer agreements. Compact, rugged harvesters that tolerate power fluctuations find growing reception in these regions.

- Thermo Fisher Scientific

- Danaher (Cytiva, Beckman Coulter)

- Sartorius

- Miltenyi Biotec

- Becton Dickinson & Co.

- Lonza Group

- Stem Cell Technologies

- Corning

- PerkinElmer

- Eppendorf

- Greiner Bio-One

- Eurofins

- Terumo

- Nipro

- Tomtec Inc.

- Alcami

- Esco Lifesciences

- PromoCell

- CellGenix

- Regen Lab SA

- PluriStem Therapeutics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Investment in Cell and Gene Therapies

- 4.2.2 Expansion of Biopharmaceutical Manufacturing Infrastructure

- 4.2.3 Rising Prevalence of Chronic Diseases Requiring Cell Therapies

- 4.2.4 Technological Advancements in Automated Cell Processing

- 4.2.5 Supportive Regulatory Frameworks for Advanced Therapies

- 4.2.6 Emergence of Personalized and Point-of-Care Cell Therapy Platforms

- 4.3 Market Restraints

- 4.3.1 Ethical and Regulatory Concerns Around Stem Cell Sourcing

- 4.3.2 High Cost of Automated Harvesting Systems

- 4.3.3 Variability and Quality Control Challenges in Donor-Derived Cells

- 4.3.4 Cold-Chain and Logistics Complexities for Live Cells

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers / Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Type of Cell Harvesting

- 5.1.1 Manual Cell Harvesters

- 5.1.2 Automated Cell Harvesters

- 5.2 By Application

- 5.2.1 Biopharmaceutical Application

- 5.2.2 Stem-Cell Research

- 5.2.3 Other Applications

- 5.3 By End User

- 5.3.1 Biotechnology & Biopharmaceutical Companies

- 5.3.2 Research Institutes

- 5.3.3 Other End Users

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Thermo Fisher Scientific

- 6.3.2 Danaher (Cytiva, Beckman Coulter)

- 6.3.3 Sartorius AG

- 6.3.4 Miltenyi Biotec

- 6.3.5 Becton Dickinson & Co.

- 6.3.6 Lonza Group

- 6.3.7 STEMCELL Technologies

- 6.3.8 Corning Inc.

- 6.3.9 PerkinElmer Inc.

- 6.3.10 Eppendorf SE

- 6.3.11 Greiner Bio-One

- 6.3.12 Eurofins Scientific

- 6.3.13 Terumo Corporation

- 6.3.14 Nipro Corporation

- 6.3.15 Tomtec Inc.

- 6.3.16 Alcami Corporation

- 6.3.17 Esco Lifesciences

- 6.3.18 PromoCell GmbH

- 6.3.19 CellGenix GmbH

- 6.3.20 Regen Lab SA

- 6.3.21 PluriStem Therapeutics

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment