|

시장보고서

상품코드

1848319

암 지지요법 약물 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Cancer Supportive Care Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

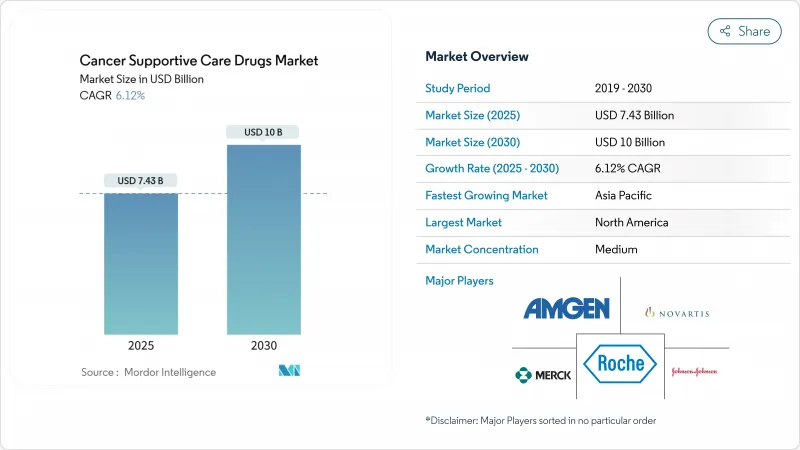

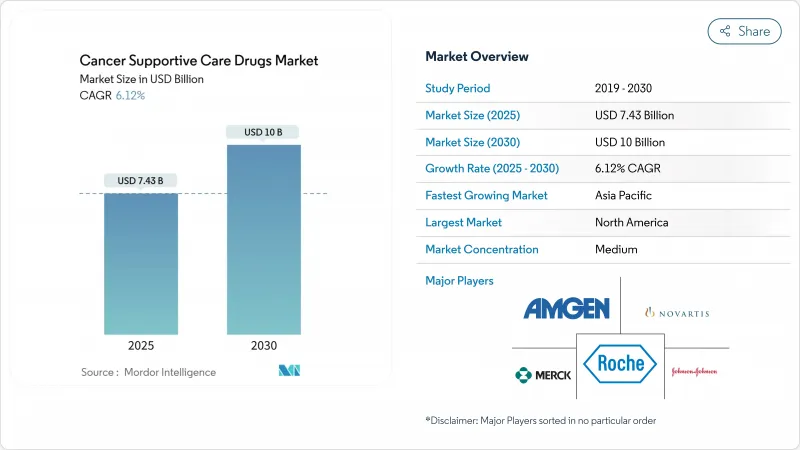

암 지지요법 약물 시장 규모는 2025년에 74억 3,000만 달러로 평가되었고, 2030년에 100억 달러로 확대될 것으로 예측되며, CAGR은 6.12%를 나타낼 전망입니다.

이러한 확장은 전 세계적으로 증가하는 암 발병률, 다제 병용 화학요법의 확대 적용, 그리고 저가 바이오시밀러에 대한 규제적 호재가 반영된 결과입니다. 가치 기반 보상 체계의 확산은 프로토콜에 기반한 조기 지지요법 사용을 촉진하는 한편, 자가 투여 제형에 대한 환자 수요는 경구 및 피하 투여 제품의 혁신을 이끌고 있습니다. 바이오시밀러 G-CSF 및 골보호제가 신속하게 채택되며 경쟁 압력이 고조되고 있으며, 이는 효능을 저하시키지 않으면서 획득 비용을 절감하고 있습니다. 동시에 보험사 및 의료 제공자들은 재입원률 감소에 주력하고 있으며, 이는 지지적 치료의 일관된 준수와 밀접하게 연관된 목표입니다. 이러한 복합적 요인들은 2030년까지 암 지지요법 약물 시장의 건전한 전망을 유지할 것입니다.

세계의 암 지지요법 약물 시장 동향 및 인사이트

세계 암 부담 증가

신규 발병 건수가 급증하고 있습니다. IARC는 2040년까지 연간 2,840만 건의 진단이 이루어질 것으로 전망하며, 이는 2020년 대비 55% 증가한 수치입니다. 50세 미만의 젊은 환자층에서 1990년부터 2019년 사이 암 발병률이 79% 급증하여 생존 기간이 연장되고 반복적인 치료 주기가 발생하고 있습니다. 이러한 인구학적 변화는 골수억제 요법 노출 기간을 연장시켜 암 지지요법 약물 시장 전반에 걸쳐 G-CSF, 항구토제, 빈혈 치료제 수요를 증가시킵니다. 경제적 부담 역시 상당합니다. 유럽만 해도 2018년 암 관련 지출이 1,990억 유로에 달했으며, 이 중 320억 유로가 항암제에 할당되었습니다. 아시아태평양 지역의 성장은 두드러지며, 2026년까지 중국의 항암제 지출이 127억 달러에 달할 것으로 예상되는 것이 그 예시로서, 지지 치료 도입을 위한 상당한 성장 여력을 강화하고 있습니다.

화학요법과 병용요법 채택 증가

복합 프로토콜은 현재 고형 종양 및 혈액 악성 종양의 1차 치료를 지배하고 있으며, 단일요법에 비해 3-4등급 혈액학적 독성을 40-60% 증가시킵니다. 그 결과 예방적 G-CSF, 적혈구 생성 자극제, 차세대 항구토제의 꾸준한 사용이 이어지고 있습니다. 트라스투주맙 데룩스테칸과 같은 신흥 항체-약물 접합체는 기존 부작용 프로필에 독특한 폐 및 위장관 독성을 추가하여 암 지지요법 약물 시장의 임상적 적용 범위를 확대하고 있습니다. 종양학자들이 표적 치료제를 백본 화학요법과 통합함에 따라, 지지 치료 프로토콜은 세포독성 및 면역 매개 부작용 예방을 모두 포괄하도록 확대됩니다.

독성이 낮은 표적요법과 면역 종양요법의 출현

면역 체크포인트 억제제와 정밀 소분자 억제제는 골수를 보호하는 경우가 많아, 기존 화학요법 대비 중성구 감소증 발생률이 60-70% 낮습니다. 결과적으로 이러한 치료법이 1차 표준이 되는 지역에서는 G-CSF 사용량이 감소할 수 있습니다. 그럼에도 지지적 치료의 필요성은 사라지지 않고 진화합니다. 면역 관련 이상반응은 코르티코스테로이드, 내분비 대체 요법, 피부과 치료제 등을 요구하며, 이들은 암 지지요법 약물 시장 내 인접 치료 영역을 차지합니다. 이러한 신흥 수요를 겨냥해 파이프라인을 전환하는 제약사는 기존 카테고리의 시장 침식을 상쇄할 수 있습니다.

부문 분석

G-CSF는 2024년 암 지지요법 약물 시장의 35.23%를 차지하며 중성구 감소증 예방에서의 핵심적 역할을 입증했습니다. 이 세그먼트의 회복력은 다양한 종양 유형에서 예측 가능한 화학요법 유발 골수 억제와 임상 지침에서의 강력한 권고에 기인합니다. 바이오시밀러의 급속한 보급은 단가를 압박하지만 치료 적용 범위를 확대하여 매출 증가 추세를 유지합니다. 생존 기간 연장으로 부각되는 독성 반응을 해결하는 스테로이드 구강 세정제 및 점막염 차단 젤 등 국소 제제는 2030년까지 연평균 8.43% 성장률을 기록할 전망입니다. ESA는 수혈에 반응하지 않는 빈혈 치료에 여전히 필수적이지만 안전성 라벨링으로 인한 중간 수준의 역풍에 직면해 있습니다. 항구토제는 지연성 구토를 표적으로 한 고정 용량 복합제 출시로 점진적 성장을 지속합니다. 비스포스포네이트 및 데노수맙 바이오시밀러는 고령 인구에서 증가하는 골격 관련 사건 위험과 함께 꾸준히 성장합니다. 한편, 오피오이드 수요는 변화하는 통증 관리 패러다임을 반영하여 감소합니다. 종합적으로 이러한 추세는 임상 실무의 진화와 보험 적용 변화가 암 지지요법 시장 내 약물군 지형을 지속적으로 재편하는 방식을 보여줍니다.

매출 측면에서 G-CSF 암 지지요법 약물 시장 규모는 가격 경쟁이 심화되더라도 예측 기간 동안 급속히 확대될 전망입니다. 반대로 오피오이드 매출은 환자 수는 안정적임에도 일일 평균 투여량 감소로 축소되며, 이는 지불 주체가 위험 완화 대안을 중시함을 입증합니다. 국소 및 피하 투여 형태의 지속적인 혁신은 제조사들이 상품화된 주사제 beyond를 넘어 다각화하는 데 기여하며, 신규 하위 분류에서 지속 가능한 두 자릿수 성장을 주도합니다.

지역 분석

북미는 2024년 글로벌 매출의 43.23%를 차지했으며, 이는 선진적인 종양학 인프라와 고비용 생물학적 제제를 보상하는 광범위한 보험 적용에 기반합니다. '종양학 모델 강화(Enhancing Oncology Model)'와 같은 가치 기반 시범 사업은 측정 가능한 비용 절감을 입증하여 상업적 지불자 간 확산을 촉진하고 지침에 부합하는 지원 치료 도입을 강화하고 있습니다.

유럽은 두 번째로 큰 지역 시장입니다. 일부 국가에서 공격적인 바이오시밀러 조달로 암 치료제 가격이 최대 97.8%까지 하락하여 접근성을 확대하고 예산 부담을 완화했습니다. 국가 보건 시스템은 항암제에 상당한 지출(2018년 기준 320억 유로)을 할당하며 지원 치료 보장 정책에 대한 강력한 정치적 의지를 입증하고 있습니다. 회원국 간 상환 변동성으로 인해 제조사들은 가격 전략을 맞춤화해야 하지만, 광범위한 HTA 프레임워크는 비용 효율성이 최우선 고려사항으로 남도록 보장합니다.

아시아태평양 지역은 인구 고령화, 중산층 확대, 보험 보급률 증가에 힘입어 7.45%의 연평균 성장률(CAGR)로 가장 빠르게 성장하는 지역입니다. 중국의 항암제 지출은 2026년까지 127억 달러에 달할 전망이며, 인도는 국내 생물학적 제제 생산 촉진을 위해 외국인 직접 투자 규제를 완화하고 있습니다. 정부 검진 프로그램과 진단 인식 제고로 조기 발견률이 높아지면서 치료 환자 집단이 확대되고 암 지지요법 약물 시장의 수요가 지속되고 있습니다.

라틴 아메리카와 중동 및 아프리카는 규모는 작지만 꾸준히 성장하는 시장입니다. 브라질과 멕시코의 조달 컨소시엄은 바이오시밀러 시장 진입 시기와 연계된 물량 기반 할인을 협상 중입니다. 한편 걸프협력회의(GCC) 회원국들은 3차 암 센터에 투자하며, 광범위한 의료 관광 목표의 일환으로 프로토콜 기반 지원 치료를 도입하고 있습니다. 이러한 지역들은 종합적으로 점진적인 물량 증가를 통해 글로벌 성장 모멘텀을 강화하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 세계에서 증대하는 암의 부담

- 화학요법과 병용요법의 채택 증가

- 비용 효율적인 바이오시밀러 도입

- 가치 기반 종양학 치료 모델로의 전환

- 재택 치료를 가능하게 하는 경구 및 피하 제형의 확대

- 시장 성장 억제요인

- 독성이 낮은 표적 치료와 면역종양 치료의 출현

- 오피오이드 오용 및 ESA 관련 혈전증 사건에 대한 안전성 우려

- 기준가격제 및 입찰 시스템으로 인한 가격 압박

- 약물 수요를 감소시키는 디지털 증상 관리의 증가하는 사용

- 규제 상황

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 약물 클래스별

- G-CSF

- ESA

- 제토제

- 비스포스포네이트

- 오피오이드

- NSAIDs

- 국소 약

- 기타 약품 클래스

- 적응증별

- 화학요법 유발성 호중구감소증

- 화학요법 유발성 빈혈

- 메스꺼움 및 구토

- 암에 의한 골다공증

- 암 통증

- 구강 및 피부 점막염

- 유통 채널별

- 병원 약국

- 소매 약국

- 온라인 약국

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Amgen Inc.

- Johnson & Johnson(Janssen)

- F. Hoffmann-La Roche AG

- Novartis AG(Sandoz & Hexal)

- Teva Pharmaceutical Industries Ltd.

- Pfizer Inc.

- Sanofi

- Helsinn Healthcare SA

- Heron Therapeutics Inc.

- Dr. Reddy's Laboratories

- Sun Pharmaceutical Industries Ltd.

- Ipsen Pharma

- Kyowa Kirin Co. Ltd.

- Otsuka Holdings Co. Ltd.

- Accord Healthcare

- Fresenius Kabi

- Lupin Ltd.

제7장 시장 기회와 장래의 전망

HBR 25.11.12The cancer supportive care drugs market size was valued at USD 7.43 billion in 2025 and is forecast to climb to USD 10.00 billion by 2030, translating into a 6.12% CAGR.

This expansion reflects rising global cancer incidence, wider use of multi-agent chemotherapy, and regulatory tailwinds for lower-priced biosimilars. Growing acceptance of value-based reimbursement encourages earlier, protocol-driven use of supportive therapies, while patient demand for self-administered formulations fuels innovation in oral and subcutaneous products. Competitive pressure intensifies as biosimilar G-CSFs and bone-protective agents win rapid uptake, trimming acquisition costs without sacrificing efficacy. At the same time, payers and providers focus on reducing hospital readmissions, a goal closely tied to more consistent supportive care adherence. These converging factors sustain a healthy outlook for the cancer supportive care drugs market through 2030.

Global Cancer Supportive Care Drugs Market Trends and Insights

Growing Burden of Cancer Worldwide

New cases are rising sharply: IARC projects 28.4 million annual diagnoses by 2040, a 55% jump from 2020. Younger patients-those under 50-saw a 79% surge in cancer incidence between 1990 and 2019, leading to longer survival horizons and repeated treatment cycles. These demographic shifts lengthen exposure to myelosuppressive regimens, elevating demand for G-CSFs, antiemetics, and anemia therapies across the cancer supportive care drugs market. Economic pressure is equally significant; Europe alone spent EUR 199 billion on cancer in 2018, with EUR 32 billion earmarked for oncology medicines. Asia-Pacific growth is pronounced, exemplified by China's projected USD 12.7 billion oncology spend by 2026, reinforcing a sizeable runway for supportive care uptake.

Rising Adoption of Chemotherapy and Combination Regimens

Combination protocols now dominate frontline therapy for solid tumors and hematologic malignancies, raising grade 3-4 hematologic toxicities by 40-60% versus monotherapy. The result is steady utilization of prophylactic G-CSFs, erythropoiesis-stimulating agents, and next-generation antiemetics. Emerging antibody-drug conjugates, such as trastuzumab deruxtecan, layer unique pulmonary and gastrointestinal toxicities onto conventional adverse-event profiles, widening the clinical remit of the cancer supportive care drugs market. As oncologists integrate targeted agents with backbone chemotherapy, supportive care protocols broaden to encompass both cytotoxic and immune-mediated side-effect prevention.

Emergence of Targeted and Immuno-Oncology Therapies with Lower Toxicity

Immune checkpoint inhibitors and precision small-molecule inhibitors frequently spare bone marrow, leading to 60-70% lower neutropenia rates compared with traditional chemotherapy. Consequently, G-CSF volumes may moderate in regions where these modalities become first-line standards. Nonetheless, the supportive care mandate evolves rather than disappears: immune-related adverse events demand corticosteroids, endocrine replacement, and dermatologic agents that occupy adjacent therapeutic niches within the cancer supportive care drugs market. Manufacturers that pivot pipelines toward these emerging needs can offset erosion in legacy categories.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Value-Based Oncology Care Models

- Expansion of Oral and Subcutaneous Formulations Enabling Home Care

- Safety Concerns Around Opioid Misuse and ESA-Linked Thrombotic Events

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

G-CSFs represented 35.23% of the cancer supportive care drugs market in 2024, underscoring their pivotal role in neutropenia prophylaxis. The segment's resilience stems from predictable chemotherapy-induced marrow suppression across tumor types and strong endorsement in clinical guidelines. Rapid biosimilar uptake compresses unit prices but expands treatment penetration, keeping revenue on an upward trajectory. Topical agents, including steroid mouthwashes and barrier gels for mucositis, post an 8.43% CAGR to 2030 by addressing toxicities that gain visibility as survival lengthens. ESAs remain essential for anemia unresponsive to transfusion yet face moderate headwinds from safety labeling. Antiemetics sustain incremental gains, supported by fixed-dose combination launches targeting delayed emesis. Bisphosphonates and denosumab biosimilars grow steadily alongside rising skeletal-related-event risk in aging populations. Meanwhile, opioid demand softens, mirroring changing pain-control paradigms. Collectively, these trends illustrate how clinical-practice evolution and reimbursement shifts continually reshape the drug-class landscape within the cancer supportive care drugs market.

In revenue terms, the cancer supportive care drugs market size for G-CSFs is projected to expand briskly through the forecast horizon, even as price competition intensifies. Conversely, opioid revenues diminish due to lower average daily doses despite stable patient counts, validating payer emphasis on risk-mitigating alternatives. Continuous innovation in topical and subcutaneous formats helps manufacturers diversify beyond commoditized injectables, anchoring sustainable double-digit growth in newer subclasses.

The Cancer Supportive Care Drugs Market Report is Segmented by Drug Class (G-CSFs, Esas, Antiemetics, and More), Indication (Chemotherapy-Induced Neutropenia, and More), Distribution Channel (Hospital Pharmacies, and More), Geography (North America, Europe, Asia-Pacific, The Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 43.23% of global revenue in 2024, underpinned by advanced oncology infrastructure and widespread insurance coverage that reimburses high-cost biologics. Value-based pilots such as the Enhancing Oncology Model demonstrate measurable savings, encouraging replication across commercial payers and fortifying guideline-aligned supportive care uptake.

Europe stands as the second-largest regional market. Aggressive biosimilar procurement cut cancer-medicine prices by up to 97.8% in select countries, broadening access and curbing budget impact. National health systems devote substantial outlays-EUR 32 billion in 2018-for oncology drugs, evidencing strong political commitment to supportive therapy coverage. Reimbursement variability across member states prompts manufacturers to tailor pricing strategies, but widespread HTA frameworks ensure cost-effectiveness remains front-of-mind.

Asia-Pacific is the fastest-growing region with a 7.45% CAGR, energized by demographic aging, expanding middle classes, and broader insurance penetration. China's oncology expenditure is on course to reach USD 12.7 billion by 2026, while India liberalizes foreign-direct-investment norms to spur domestic biologics manufacture. Government screening programs and rising diagnostic literacy heighten early detection rates, translating into larger treated cohorts and sustained demand in the cancer supportive care drugs market.

Latin America and the Middle East & Africa constitute smaller but steadily advancing markets. Procurement consortia in Brazil and Mexico negotiate volume-based discounts that align with biosimilar entry timelines. Meanwhile, Gulf Cooperation Council members invest in tertiary cancer centers, importing protocol-driven supportive care as part of broader medical-tourism aspirations. Collectively, these geographies add incremental volume that bolsters global growth momentum.

- Amgen

- Johnson & Johnson

- Roche

- Novartis AG (Sandoz & Hexal)

- Teva Pharmaceutical Industries

- Pfizer

- Sanofi

- Helsinn Healthcare

- Heron Therapeutics Inc.

- Dr. Reddy's Laboratories

- Sun Pharmaceuticals Industries

- Ipsen

- Kyowa Kirin Co. Ltd.

- Otsuka

- Accord Healthcare

- Fresenius

- Lupin

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Burden Of Cancer Worldwide

- 4.2.2 Rising Adoption Of Chemotherapy And Combination Regimens

- 4.2.3 Introduction Of Cost-Effective Biosimilars

- 4.2.4 Shift Toward Value-Based Oncology Care Models

- 4.2.5 Expansion Of Oral And Subcutaneous Formulations Enabling Home Care

- 4.3 Market Restraints

- 4.3.1 Emergence Of Targeted And Immuno-Oncology Therapies With Lower Toxicity

- 4.3.2 Safety Concerns Around Opioid Misuse And ESA-Linked Thrombotic Events

- 4.3.3 Pricing Pressures From Reference-Pricing And Tender Systems

- 4.3.4 Growing Use Of Digital Symptom Management Reducing Pharmacologic Demand

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Drug Class

- 5.1.1 G-CSFs

- 5.1.2 ESAs

- 5.1.3 Antiemetics

- 5.1.4 Bisphosphonates

- 5.1.5 Opioids

- 5.1.6 NSAIDs

- 5.1.7 Topical Agents

- 5.1.8 Other Drug Classes

- 5.2 By Indication

- 5.2.1 Chemotherapy-induced Neutropenia

- 5.2.2 Chemotherapy-induced Anemia

- 5.2.3 Nausea & Vomiting

- 5.2.4 Cancer-related Bone Loss

- 5.2.5 Cancer Pain

- 5.2.6 Oral & Dermal Mucositis

- 5.3 By Distribution Channel

- 5.3.1 Hospital Pharmacies

- 5.3.2 Retail Pharmacies

- 5.3.3 Online Pharmacies

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Amgen Inc.

- 6.3.2 Johnson & Johnson (Janssen)

- 6.3.3 F. Hoffmann-La Roche AG

- 6.3.4 Novartis AG (Sandoz & Hexal)

- 6.3.5 Teva Pharmaceutical Industries Ltd.

- 6.3.6 Pfizer Inc.

- 6.3.7 Sanofi

- 6.3.8 Helsinn Healthcare SA

- 6.3.9 Heron Therapeutics Inc.

- 6.3.10 Dr. Reddy's Laboratories

- 6.3.11 Sun Pharmaceutical Industries Ltd.

- 6.3.12 Ipsen Pharma

- 6.3.13 Kyowa Kirin Co. Ltd.

- 6.3.14 Otsuka Holdings Co. Ltd.

- 6.3.15 Accord Healthcare

- 6.3.16 Fresenius Kabi

- 6.3.17 Lupin Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment