|

시장보고서

상품코드

1849913

플렉서블 디스플레이 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Flexible Display - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

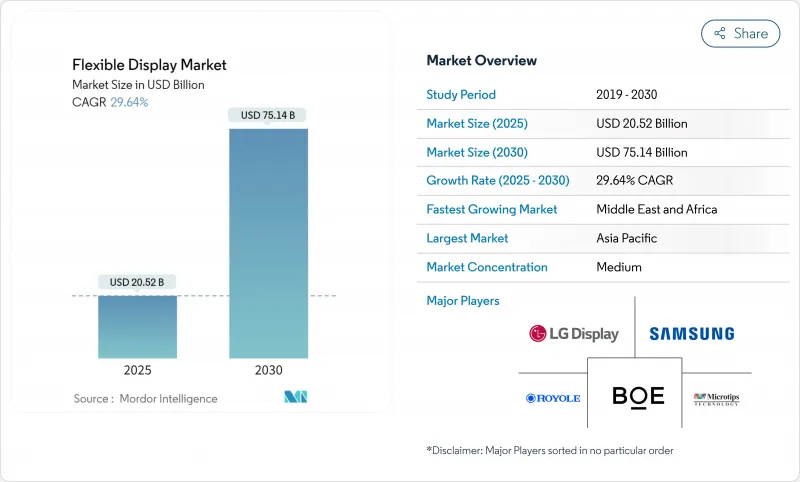

플렉서블 디스플레이 시장 규모는 2025년에 205억 2,000만 달러로 평가되었고, 2030년에 751억 4,000만 달러에 이를 것으로 예측되며, 이 기간 동안 CAGR은 29.64%를 나타낼 전망입니다.

가치 평가의 도약은 규모의 경제, 소재 혁신, 제품 설계 자유도가 수렴하여 유연 패널을 틈새 개념에서 소비자 가전, 모빌리티, 산업 환경 전반의 주류 인터페이스로 전환하는 전환점을 시사합니다. 8.6세대 OLED 공장 생산 투자, 롤러블 기술의 급속한 혁신, 웨어러블 기기로의 마이크로 LED 전환은 시장 규모를 확대하고 있으며, 유리 없는 모듈에 대한 규제 추진은 유럽에서 새로운 응용 분야를 촉진하고 있습니다. 중국 제조업체들이 한국 기존 업체들보다 빠르게 생산 능력을 확장하면서 경쟁 강도가 높아지고 있으며, 이는 기존 비용 구조에 도전장을 내밀고 가격 하락을 가속화하고 있습니다. 동시에 폴리이미드, 캡슐화 및 힌지 노하우를 확보한 통합 기업들은 공급 충격과 소송 위험으로부터 스스로를 보호하고 있습니다.

세계의 플렉서블 디스플레이 시장 동향 및 인사이트

중국과 한국에서 롤러블 및 폴더블 스마트폰 발매가 활발

플렉서블 OLED 스마트폰 패널 출하량은 2024년 26% 증가한 7억 8,400만 대를 기록하며 새로운 형태가 교체 수요를 자극하는 모습을 보여주었습니다. 2025년 말 출시 예정인 새로운 트라이폴드 디자인은 360도 회전과 주름 가시성을 낮추는 초박형 유리를 적용해 브랜드 차별화를 강화할 전망입니다. 중국 신규 진입업체들은 힌지 내구성 목표 달성 및 설계-출시 주기 단축으로 빠르게 규모를 확장하며 기존 업체들에 가격 및 혁신 속도 측면에서 압박을 가하고 있습니다. 힌지, 내열성 폴리이미드, 투명 커버 필름을 중심으로 한 부품 생태계가 직접적인 혜택을 볼 전망입니다. 이러한 상승세는 액세서리 및 수리 시장으로도 확산되어 추가적인 서비스 수익원을 창출할 것입니다.

유럽 전역 프리미엄 전기차의 곡면 OLED 콕핏 채택

럭셔리 전기차는 EQS SUV 하이퍼스린과 같은 확장형 곡면 대시보드로 실내 경험을 향상시킵니다. 이는 연속적인 유리 커버 아래 여러 디스플레이를 통합합니다. 자동차 OEM 업체들은 얇은 두께, 균일한 휘도, 디자인 자유도를 위해 플렉서블 OLED를 선호하며, 이는 차량당 디스플레이 면적 급증으로 이어집니다. 1차 공급업체들은 패널 제조사와의 협력을 강화해 공동으로 콕핏 플랫폼을 개발하고 있으며, 소프트웨어 정의 차량 전략은 지속적인 무선 업데이트를 지원하는 디스플레이를 요구합니다. 자율 주행 기능이 성숙해짐에 따라 다중 모드 상호작용과 신축성 있는 기둥 간 스크린이 차량당 디스플레이 면적 소비를 증가시킬 전망입니다.

8세대 이상 폴리이미드 수율 손실로 인한 스크랩 비용 증가

더 큰 모어글래스로의 확장은 유연한 PI 기판의 열적 스트레스를 가중시켜, 결함으로 인한 수율 하락을 유발하고 단위당 비용을 증가시킵니다. 에어로겔 강화 PI 섬유 연구는 열적 안정성 향상에 유망하지만 산업적 채택은 아직 초기 단계로, 양산 단계에서 공장들은 고가의 스크랩 위험에 노출됩니다. 현재 수율 회복 프로그램은 실시간 인라인 계측 및 AI 기반 예측 유지보수에 집중하여 대량 생산 시작 전 결함 밀도를 줄이는 데 주력하고 있습니다.

부문 분석

OLED는 2024년 플렉서블 디스플레이 시장에서 85% 점유율을 차지했으며, 백라이트 없이도 더 얇고 곡면 적용이 용이한 발광 픽셀을 활용했습니다. 중국 공장들의 원가 하락과 증발기 처리량 증가는 OLED를 스마트폰, 시계, 곡면 인포테인먼트 클러스터용 패널로 유지시켰습니다. 동시에 마이크로 LED 출하량은 시범 생산에서 초기 양산 단계로 확대되며, 양자점 컬러 컨버터, 대량 이송 정확도 및 수리 수율 개선에 힘입어 36%의 연평균 성장률(CAGR)을 기록할 전망입니다. 마이크로 LED는 밝기를 10,000니트까지 끌어올리고 높은 열 부하에서도 긴 수명을 제공하므로(천마의 8인치 프로토타입으로 입증됨), 자동차 헤드업 디스플레이와 내구성 높은 웨어러블 기기가 가장 먼저 혜택을 볼 것입니다. 전자종이는 저전력 간판 및 물류 태그 분야에서 틈새 시장을 유지하는 반면, 양자점 LCD 하이브리드 기술은 중급 기기에서 가격 및 색역 격차를 지속적으로 해소하고 있습니다.

OLED의 지배력은 세 가지 압박 요인에 직면해 있습니다. 첫째, 무기물 마이크로 LED 소재의 장수명은 OLED의 번인(burn-in) 위험 논리를 희석시킵니다. 둘째, Gen-8.6 공정 비용 우위로 경질 OLED와 유연 OLED의 평균판매가격(ASP) 격차가 좁혀지며 저가 시장이 유연 형태로 이동 중입니다. 셋째, 퀀텀닷 온칩(on-chip) 기술이 롤투롤(roll-to-roll) 플라스틱 기판과 호환되며 초대형 투명 창문 시장에서 미래 경쟁을 예고합니다. 그럼에도 생태계 성숙도, 장비 감가상각, 풍부한 공급량으로 중기적으로는 OLED의 우위가 지속될 전망입니다.

2024년 폴더블 기기는 플렉서블 디스플레이 시장의 71%를 점유했으며, 스마트폰 제조사들이 바이폴드, 트라이폴드, 랩어라운드 형식을 경쟁적으로 출시함에 따라 여전히 판매량 주도차 역할을 하고 있습니다. 힌지 기하학 구조와 UTG(초박형 유리) 라미네이션에 대한 특허 장벽은 선점 기업의 우위를 공고히 하지만, 라이선스를 취득하거나 대체 운동학적 스택을 혁신하는 경쟁사들의 진입을 완전히 차단하지는 못합니다. 연신형 스크린은 39%의 연평균 성장률(CAGR)로 확대될 전망이며, 컴팩트한 하우징으로 수축되어 공간 효율성을 극대화함으로써 주머니에 넣기 편하면서도 넓은 디스플레이를 원하는 소비자 수요에 부응합니다. 초기 노트북 및 태블릿 연신형 제품은 모터식 스풀과 신축 제한 적층 기술을 통해 3만 회 이상의 작동 반복성을 달성할 수 있음을 입증했습니다.

굽힘 및 변형 가능 디스플레이는 단순한 기계적 부하 덕분에 곡면 엣지 스마트폰, 피트니스 밴드, 자동차 레이더의 핵심 요소로 자리매김했습니다. 신축성 기판 메쉬와 뱀 모양 회로 패턴으로 구현되는 신생 ‘형태 자유’ 클래스는 피부 부착형 건강 패치 및 소프트 로봇을 위해 활발히 연구 중입니다. 신축성 디스플레이 관련 학술 논문은 2014년 17편에서 2023년 197편으로 급증하며 연구개발 투자의 증가를 반영했습니다. 상용화는 더딘 편이지만, 이러한 진전은 향후 10년 내 보편화된 주변 디스플레이 표면의 토대를 마련하고 있습니다.

지역 분석

아시아태평양 지역은 2024년 매출의 57%를 차지하며 주도적 위치를 유지했습니다. 이는 PI 수지 합성부터 모듈 조립까지 아우르는 한국, 중국, 대만의 밀집된 제조 생태계에 힘입은 결과입니다. 중국은 2028년까지 연간 8%의 플렉서블 OLED 생산 능력을 추가하는 반면, 한국은 2%의 증가율을 보이며 글로벌 패널 생산 점유율이 68%에서 74%로 상승할 전망입니다. 지역 정책 인센티브는 현지 선도 기업에 유리한 토지, 세금 및 전력 조건을 제공하며, 국내 스마트폰 OEM 업체들은 안정적인 수요를 창출합니다. 이러한 선순환 구조는 공급망 자급자족을 공고히 하고 신규 라인의 양산 시기를 단축시킵니다.

북미는 AR/VR, 고성능 컴퓨팅, 프리미엄 노트북 부문에서 주도권으로 기술 수요를 주도합니다. 미국 브랜드들은 2026년형 OLED 맥북급 패널을 조달하며, 공급사들에게 정적 UI 부하에서 수명을 연장하는 산화물 TFT 및 탠덤 스택 구조의 인증을 요구하고 있습니다. 힌지 특허로 인한 법적 위험은 여전히 주의사항이지만, 업체들은 출시 시기를 보호하기 위해 종종 합의나 상호 라이선싱을 선택합니다. 마이크로전자 산업의 리쇼어링을 위한 정부 보조금은 생태계의 일부를 미국으로 재편할 수 있으며, 특히 백플레인 및 유리 없는 캡슐화 공구 분야에서 두드러질 전망입니다.

유럽은 에코디자인 규정과 향후 도입될 디지털 제품 여권을 통해 규제적 영향력을 행사하며, 재활용 가능한 구조와 완전한 소재 공개를 산업계에 촉구하고 있습니다. 독일, 스웨덴, 영국의 자동차 클러스터는 곡면 OLED 클러스터를 빠르게 도입하며 현지 통합, 본딩 및 테스트 파트너사를 활성화하고 있습니다. 유럽의 2030년까지 순환 소재 사용률 24% 목표는 용제 감소형 폴리인산(PI), 생분해성 접착제, 쉬운 분리를 가능케 하는 기계적 패스너 개발을 촉진합니다.

중동 및 아프리카는 규모는 상대적으로 작지만 교통 허브, 스포츠 경기장, 레저 시설의 디지털 사이니지 확대로 연평균 32% 성장률을 기록하며 가장 빠른 성장세를 보입니다. 유리 외관에 밀착되는 플렉서블 LED 필름 스크린은 건축 분야에서 새로운 형태에 대한 수요를 보여줍니다. 정부 지원 스마트시티 프로젝트와 높은 주변광 조건은 고휘도 마이크로 LED를 매력적인 옵션으로 만듭니다. 남미는 스마트폰 보급률 증가와 수출 모델용 플렉서블 클러스터를 지정하기 시작한 자동차 조립 공장으로 뒤를 잇습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 중국과 한국의 롤러블 및 폴더블 스마트폰 출시 모멘텀

- 유럽 전역의 프리미엄 전기차(EV)용 커브드 OLED 계기판 채택

- 북미 지역의 경량 AR/VR 마이크로 OLED 패널 수요 급증

- 중국의 8.6세대 플렉서블 OLED 공장 비용 절감

- 유리 없는 모듈에 대한 EU 순환 경제 추진

- 일본 및 한국의 유연한 의료용 웨어러블 성장

- 시장 성장 억제요인

- 8세대 폴리이미드 수율 손실로 인한 스크랩 비용 증가

- 캡슐화 재료 공급 부족

- 폴더블 힌지에 대한 미국 중심 특허 소송

- 플라스틱 LCD 간판의 저온 기후 신뢰성 문제

- 업계 생태계 분석

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 디스플레이 유형별

- OLED

- LCD

- 전자 종이 디스플레이(EPD)

- 마이크로 LED

- 양자점과 기타 신흥 유형

- 형태별

- 폴더블

- 롤러블

- 벤더블

- 컨포머블(곡/랩 어라운드)

- 기판 재료별

- 유리

- 플라스틱-폴리이미드(PI)

- 플라스틱-PET/PEN

- 금속박

- 기타(폴리카보네이트, 초박판유리)

- 용도별

- 스마트폰 및 태블릿

- 스마트 웨어러블(시계, 패치)

- TV와 디지털 사이니지

- PC와 노트북

- 자동차 콕핏 및 인포테인먼트

- AR/VR 헤드 마운트 디스플레이

- 산업 및 대중교통기관 디스플레이

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 동남아시아

- 기타 아시아태평양

- 남미

- 브라질

- 기타 남미

- 중동 및 아프리카

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 기타 중동

- 아프리카

- 남아프리카

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Samsung Display Co., Ltd.

- LG Display Co., Ltd.

- BOE Technology Group Co., Ltd.

- ROYOLE Corporation

- E Ink Holdings Inc.

- AU Optronics Corp.

- Sharp Corporation

- Innolux Corporation

- TCL CSOT

- Visionox Co., Ltd.

- Tianma Micro-electronics Co., Ltd.

- Truly International Holdings

- Japan Display Inc.

- Microtips Technology

- FlexEnable Technology Ltd.

- Plastic Logic Germany

- Chunghwa Picture Tubes Ltd.

- Shenzhen China Star Optoelectronics Technology

- Huawei Technologies Co., Ltd.(Panel R&D)

- Guangzhou OED Technologies Co., Ltd.

- Universal Display Corporation

제7장 시장 기회와 장래의 전망

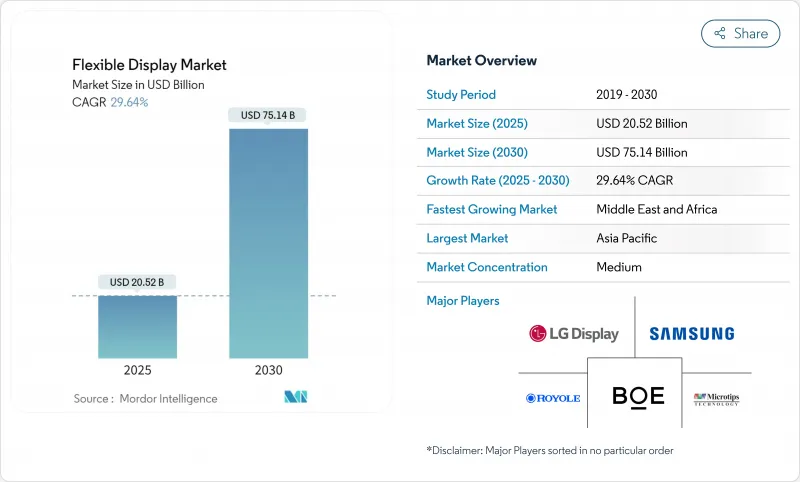

HBR 25.11.14The flexible display market size stands at USD 20.52 billion in 2025 and is forecast to reach USD 75.14 billion by 2030, translating into a powerful 29.64% CAGR over the period.

The valuation leap signals a turning point in which scale economies, material breakthroughs and product design freedom converge to shift flexible panels from niche concepts into mainstream interfaces across consumer electronics, mobility and industrial environments. Production investments in Gen-8.6 OLED fabs, rapid rollable innovation and the migration of micro-LED into wearables are widening the addressable base, while regulatory pushes for glass-free modules spur fresh applications in Europe. Competitive intensity is rising as Chinese manufacturers expand capacity faster than Korean incumbents, challenging established cost structures and accelerating price declines. Simultaneously, integrated players that secure polyimide, encapsulation and hinge know-how are insulating themselves from supply shocks and litigation risk.

Global Flexible Display Market Trends and Insights

Rollable and foldable smartphone launch momentum in China and Korea

Shipments of flexible OLED smartphone panels climbed 26% in 2024 to 784 million units, underscoring how fresh form factors stimulate replacement demand.New tri-fold designs slated for late 2025 bring 360-degree rotation and ultra-thin glass that lowers crease visibility, intensifying brand differentiation. Chinese entrants scale quickly by matching hinge durability targets and shortening design-to-launch cycles, pressuring incumbents on price and innovation tempo. Component ecosystems around hinges, temperature-resistant polyimide and transparent cover films benefit directly. The upturn also spills into accessory and repair markets, creating incremental service revenue streams.

Premium-EV curved OLED cockpit adoption across Europe

Luxury electric vehicles elevate interior experience through expansive curved dashboards such as the EQS SUV Hyper-screen, which merges multiple displays under a continuous glass cover.Automotive OEMs prefer flexible OLED for its thin profile, uniform luminance and design latitude, leading to a surge in display-area per vehicle. Tier-1 suppliers deepen partnerships with panel makers to co-develop cockpit platforms, while software-defined vehicle strategies demand displays that support continuous over-the-air upgrades. As autonomous functionality matures, multi-modal interaction and stretchable pillar-to-pillar screens are set to multiply display square-meter consumption per car.

Gen-8+ polyimide yield losses elevating scrap costs

Scaling to larger mother-glass intensifies thermal stress on flexible PI substrates, driving defect-induced yield drops that inflate per-unit cost. Research on aerogel-reinforced PI fibers shows promise in lifting thermal stability yet industrial adoption remains nascent, leaving fabs exposed to expensive scrap during ramp-up.Yield recovery programmes now focus on real-time in-line metrology and AI-based predictive maintenance to shave defect density before mass output begins.

Other drivers and restraints analyzed in the detailed report include:

- Lightweight AR/VR micro-OLED demand in North America

- Cost reduction from Gen-8.6 flexible OLED fabs in China

- Encapsulation material supply crunch

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

OLED held an 85% share of the flexible display market in 2024, leveraging emissive pixels that enable thinner, curve-friendly modules without backlights. Cost erosion from Chinese fabs and evaporator throughput gains have kept OLED the panel of choice for smartphones, watches and curved infotainment clusters. At the same time, micro-LED shipments are scaling from pilot to early mass production, posting a 36% forecast CAGR as quantum-dot colour converters, mass-transfer accuracy and repair yields improve. Automotive head-up displays and rugged wearables benefit first because micro-LED pushes brightness to 10,000 nits and delivers long lifetimes even under high thermal load, as evidenced by Tianma's 8-inch prototype. E-paper holds a niche in low-power signage and logistics tags, while quantum-dot LCD hybrids continue bridging price and colour-gamut gaps for mid-range devices.

OLED dominance faces three pressure points. First, inorganic micro-LED material longevity dilutes OLED's burn-in risk narrative. Second, Gen-8.6 cost advantages narrow the ASP gap between rigid and flexible OLED, nudging budget segments toward flexible form factors. Third, quantum-dot on-chip approaches are now compatible with roll-to-roll plastic substrates, seeding future competition in ultra-large transparent windows. Even so, ecosystem maturity, equipment depreciation and abundant supply keep OLED firmly in charge through the mid-term.

Foldable devices captured 71% of the flexible display market in 2024 and remain the volume engine as smartphone vendors race to iterate bi-fold, tri-fold and wrap-around formats. Patent barricades on hinge geometry and UTG lamination reinforce the lead of first movers yet do not preclude rivals that licence or innovate alternative kinematic stacks. Rollable screens, forecast to expand at a 39% CAGR, unlock spatial efficiency by retracting into compact housings, aligning with consumer demand for pocket-friendly yet expansive displays. Early notebook and tablet rollables demonstrate that motorised spools and stretch-limiting lamination can achieve repeatability over 30,000 actuations.

Bendable and conformable displays remain staples in curved edge phones, fitness bands and automotive radars thanks to their simpler mechanical loads. A nascent "form-factor free" class, enabled by stretchable substrate meshes and serpentine circuit patterns, is under active exploration for skin-adhesive health patches and soft robots. Academic output on stretchable displays jumped from 17 papers in 2014 to 197 in 2023, mirroring heightened R&D investment. While commercialisation lags, the progress sets the stage for ubiquitous ambient display surfaces later in the decade.

The Flexible Display Market Report is Segmented by Display Type (OLED, -Paper Display, and More), Form Factor (Foldable, Rollable, Bendable, Micro-LED, and More), Substrate Material (Glass, Plastic - Polyimide (PI), Plastic - PET/PEN, Metal Foil, and More), Application (Smartphones and Tablets, Smart Wearables, Televisions and Digital Signage, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific dominated with 57% revenue in 2024, propelled by dense manufacturing ecosystems in Korea, China and Taiwan that span PI resin synthesis to module assembly. China alone is adding 8% annual flexible OLED capacity through 2028 against Korea's 2% run-rate, lifting its share of global panel output from 68% to 74%. Regional policy incentives grant favourable land, tax and power terms to local champions, while domestic smartphone OEMs provide ready demand. This virtuous cycle cements supply-chain self-sufficiency and accelerates time-to-yield for new lines.

North America commands technology pull on account of its leadership in AR/VR, high-performance computing and premium notebook segments. US brands source OLED MacBook-class panels for 2026, compelling suppliers to qualify oxide TFT and tandem stack architectures that lengthen lifetime under static UI loads. Legal exposure arising from hinge patents remains a watch-item; however, players often settle or cross-licence to safeguard launch windows. Government grants for microelectronic reshoring may redirect portions of the ecosystem stateside, particularly in backplane and glass-free encapsulation tooling.

Europe exerts regulatory influence through the Ecodesign Regulation and the upcoming Digital Product Passport, pushing the industry toward recyclable structures and full material disclosure. Automotive clusters in Germany, Sweden and the United Kingdom adopt curved OLED clusters at a brisk pace, stimulating local integration, bonding and test partners. The continent's circular material use target of 24% by 2030 drives R&D into solvent-reduced PI, biodegradable adhesives and mechanical fasteners that enable easy separation.

The Middle East and Africa, while comparatively small, records the fastest growth at a 32% CAGR off expanding digital signage in transport hubs, sports arenas and leisure venues. Flexible LED film screens that conform to glass facades exemplify the architectural appetite for novel form factors. Government-backed smart-city projects and high ambient-light conditions make high-brightness micro-LED an attractive option. South America follows with rising smartphone penetration and automotive assembly plants beginning to specify flexible clusters for export models.

- Samsung Display Co., Ltd.

- LG Display Co., Ltd.

- BOE Technology Group Co., Ltd.

- ROYOLE Corporation

- E Ink Holdings Inc.

- AU Optronics Corp.

- Sharp Corporation

- Innolux Corporation

- TCL CSOT

- Visionox Co., Ltd.

- Tianma Micro-electronics Co., Ltd.

- Truly International Holdings

- Japan Display Inc.

- Microtips Technology

- FlexEnable Technology Ltd.

- Plastic Logic Germany

- Chunghwa Picture Tubes Ltd.

- Shenzhen China Star Optoelectronics Technology

- Huawei Technologies Co., Ltd. (Panel R&D)

- Guangzhou OED Technologies Co., Ltd.

- Universal Display Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rollable and Foldable Smartphone Launch Momentum in China and Korea

- 4.2.2 Premium-EV Curved OLED Cockpit Adoption Across Europe

- 4.2.3 Demand Spike for Lightweight AR/VR Micro-OLED Panels in North America

- 4.2.4 Cost Reduction from Gen-8.6 Flexible OLED Fabs in China

- 4.2.5 EU Circular-Economy Push for Glass-Free Modules

- 4.2.6 Growth in Flexible Medical Wearables in Japan and South Korea

- 4.3 Market Restraints

- 4.3.1 Gen-8+ Polyimide Yield Losses Elevating Scrap Costs

- 4.3.2 Encapsulation Material Supply Crunch

- 4.3.3 US-Centric Patent Litigation on Foldable Hinges

- 4.3.4 Cold-Climate Reliability Issues of Plastic-LCD Signage

- 4.4 Industry Ecosystem Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Display Type

- 5.1.1 OLED

- 5.1.2 LCD

- 5.1.3 E-Paper Display (EPD)

- 5.1.4 Micro-LED

- 5.1.5 Quantum-Dot and Other Emerging Types

- 5.2 By Form Factor

- 5.2.1 Foldable

- 5.2.2 Rollable

- 5.2.3 Bendable

- 5.2.4 Conformable (Curved/Wrap-around)

- 5.3 By Substrate Material

- 5.3.1 Glass

- 5.3.2 Plastic - Polyimide (PI)

- 5.3.3 Plastic - PET/PEN

- 5.3.4 Metal Foil

- 5.3.5 Others (Polycarbonate, Ultra-thin Glass)

- 5.4 By Application

- 5.4.1 Smartphones and Tablets

- 5.4.2 Smart Wearables (Watches, Patches)

- 5.4.3 Televisions and Digital Signage

- 5.4.4 Personal Computers and Laptops

- 5.4.5 Automotive Cockpit and Infotainment

- 5.4.6 AR/VR Head-Mounted Displays

- 5.4.7 Industrial and Public Transport Displays

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 South Korea

- 5.5.3.4 India

- 5.5.3.5 South East Asia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Samsung Display Co., Ltd.

- 6.4.2 LG Display Co., Ltd.

- 6.4.3 BOE Technology Group Co., Ltd.

- 6.4.4 ROYOLE Corporation

- 6.4.5 E Ink Holdings Inc.

- 6.4.6 AU Optronics Corp.

- 6.4.7 Sharp Corporation

- 6.4.8 Innolux Corporation

- 6.4.9 TCL CSOT

- 6.4.10 Visionox Co., Ltd.

- 6.4.11 Tianma Micro-electronics Co., Ltd.

- 6.4.12 Truly International Holdings

- 6.4.13 Japan Display Inc.

- 6.4.14 Microtips Technology

- 6.4.15 FlexEnable Technology Ltd.

- 6.4.16 Plastic Logic Germany

- 6.4.17 Chunghwa Picture Tubes Ltd.

- 6.4.18 Shenzhen China Star Optoelectronics Technology

- 6.4.19 Huawei Technologies Co., Ltd. (Panel R&D)

- 6.4.20 Guangzhou OED Technologies Co., Ltd.

- 6.4.21 Universal Display Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment