|

시장보고서

상품코드

1850039

헬스케어 생체인식 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Healthcare Biometrics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

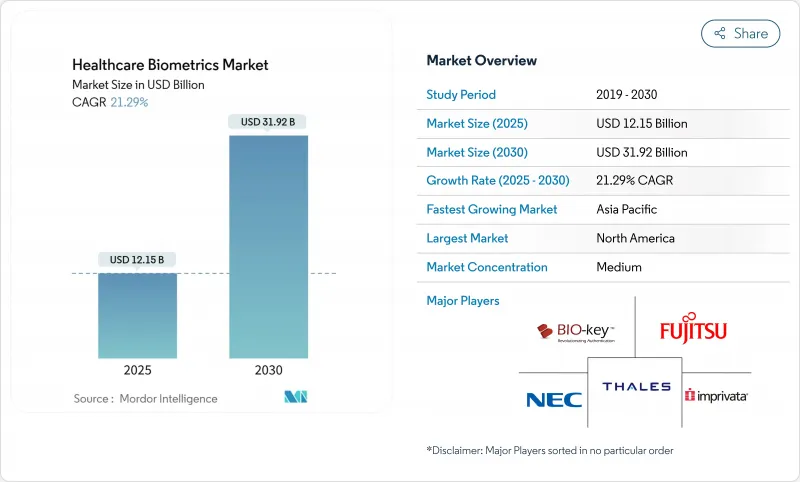

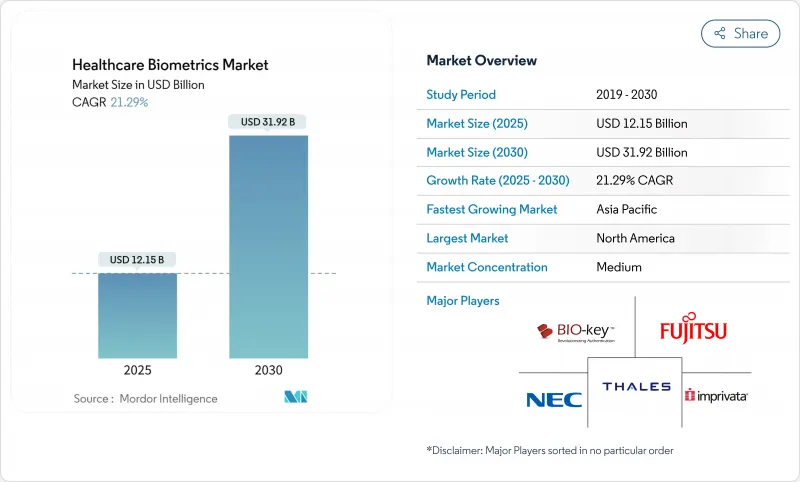

헬스케어 생체인식 시장 규모는 2025년에 121억 5,000만 달러로 추정되고, 예측 기간(2025-2030년)의 CAGR은 21.29%를 나타내, 2030년에는 319억 2,000만 달러에 달할 것으로 예상되고 있습니다.

이러한 급성장은 디지털 건강 의무화, 전자 의료 기록(EHR) 생태계 확대, 2024년에 1억 명 이상의 환자 파일이 유출된 기록적인 데이터 유출 파도에 의해 촉진되었습니다. 의료 ID 사기 증가, 정부 e-ID 프로그램, 비밀번호가 없는 임상 워크플로우의 필요성으로 인해 생체인식 인증은 선택적 부가 기능이 아닌 중요한 인프라로 자리매김하고 있습니다. 하드웨어가 여전히 지출의 대부분을 차지하고 있지만, 공급자가 통합 전문 지식을 선호하기 때문에 서비스가 가장 급성장을 기록하고 있습니다. 아시아태평양의 CAGR 25.13%는 대규모 공공 부문 프로젝트를 반영하며, 북미는 엄격한 개인정보보호법과 성숙한 병원 IT 시설을 통해 리더십을 유지하고 있습니다.

세계의 헬스케어 생체인식 시장 동향과 인사이트

정부에 의한 E-ID 및 EHR의 의무화

국가의 디지털 ID 프로그램은 헬스케어에서 생체 인식 인증을 의무화하고 있습니다. 일본의 '마이 넘버' 보험증은 2024년 12월까지 92.5%공급자에게 보급되어 8,100만명의 국민이 얼굴인식 단말기에 연결되었습니다. 인도의 아유슈만 바랏 디지털 미션에서는 6억 5,000만 명 이상의 생체인식 건강 계정이 등록되어 원격 등록 및 기록에 대한 액세스가 단순화되었습니다. 에스토니아는 전자 서비스 스택 전체에 AI 주도 ID 확인을 통합하여 이 모델을 확장하고 있습니다. 미국에서는 21세기 경화법(21st-Century Cures Act)에 준거함으로써 비밀번호에 의한 로그인을 보다 강력한 요소로 대체하도록 병원에 압력을 가하여 바이오메트릭스에 의한 싱글 사인온의 보급을 가속화하고 있습니다. 이러한 조치를 종합하면 경기 사이클 전반에 걸쳐 지속적인 수요가 확보됩니다.

의료 개인 정보 도난 및 데이터 유출 급증

Change Healthcare의 랜섬웨어 공격은 2024년에 1억 건 이상의 미국 기록을 유출시켜 과거 최악의 정보 유출이 되었습니다. 카이저 퍼머넌트 및 기타 네트워크에서 발생한 사건은 이 분야가 사이버 범죄와 악성 데이터 공유 모두에 취약하다는 것을 나타냅니다. 전국 의료부정방지협회(National Health Care Anti-Fraud Association)는 연간 부정행위를 680억 달러로 추정하고 있으며, 그 대부분은 오인에 뿌리를 두고 있습니다. 퓨 챠리타블 트러스트는 매치 미스만으로도 연간 60억 달러의 비용이 들고 있다고 계산합니다. 이러한 금전적 손실로 인해 생체 지표는 재량 지출에서 이사회 수준의 우선 순위로 전환하고 있습니다.

높은 장치와 통합 비용

스캐너, 서버, 현장 지원에 필요한 설비 투자액은 여전히 큽니다. 소규모 클리닉에서는 시스템을 신속하게 상각할 수 있는 거래량이 없기 때문에 투자 대 효과 모델이 개선되더라도 도입이 지연됩니다. 레거시 의료 정보 시스템과의 복잡한 인터페이스는 전문적인 통합자를 필요로 하며 도입 비용이 많이 듭니다. 클라우드 호스팅형 biometric-as-a-service(BaaS)는 하드웨어의 필요성을 어느 정도 완화해 주지만, 프리미엄 구독은 스케일 메리트가 나올 때까지 엄격한 예산을 압박할 가능성이 있습니다.

부문 분석

단일 요소 인증은 2024년에 37.31%의 최대 판매 점유율을 차지했는데, 이는 성숙하고 비용 효율적인 스캐너가 병원 입원에 침투하기 때문입니다. 그럼에도 불구하고 정밀도, 스푸핑 내성 및 장애 조치 기능이 헬스케어 생체인식 시장 전체의 전략적 구매 기준이 됨에 따라 멀티 모달 엔진이 CAGR 24.76%로 가장 빠르게 확대되고 있습니다. NEC의 개별화된 암 백신을 위한 얼굴 대조 시스템은 멀티모달 디자인이 정밀의료 워크플로우를 어떻게 지원하는지 보여줍니다. 키 스트로크의 케이던스와 포인터의 역학을 추적하는 행동 생체 인식은 백그라운드 안전 가드로 EHR에 도입되고 있습니다. 한편, 홍채 인증과 정맥 인증은 비접촉 조작이 필수적인 무균 환경에서 지지를 모으고 있습니다. 오인식률을 낮추는 기반 모델의 돌파구로 멀티모달 옵션은 10년 후까지 지문과 동등해질 가능성이 높습니다.

공급업체는 현재 단일 소프트웨어 개발 키트로 얼굴, 음성, 홍채 및 행동 신호를 오케스트레이션하는 프레임워크를 판매하고 있으며 통합 오버헤드를 줄이고 있습니다. 병원은 도입 후 액세스 카드의 분실 사고가 40% 감소하여 환자 중심의 디지털 프로젝트에 운영 예산을 나누게 되었다고 합니다. 그러나 지문 인증 시스템은 저렴한 센서와 임상의에 널리 친숙해지기 때문에 예산에 제약이 있는 시설에 여전히 매력적입니다.

시설이 엔트리 키오스크, POC(Point-of-Care) 기기, 모바일 리더를 업그레이드했기 때문에 하드웨어는 2024년 매출의 52.26%를 차지했습니다. 예측 기간 동안 전문 서비스 및 관리 서비스는 컨설팅, 워크플로 매핑 및 규제 보증을 고정 요금 패키지에 번들로 제공하여 CAGR 22.99%를 나타낼 전망입니다. 세일포인트를 통한 임프리바타의 정체성 지배구조 라인 인수는 헬스케어에 특화된 도메인 지식에 대한 프리미엄 증가를 보여줍니다.

통합의 복잡성은 여전히 중요한 판매 포인트입니다. 의료기관은 전체 바이오메트릭 예산의 40-60%를 인증을 임상 케어 패스에 정합시켜, HL7/FHIR과의 호환성을 확보해, 감사 추적을 유지하는 서비스에 할당하고 있습니다. 매니지드 서비스는 24시간 모니터링, 알고리즘 자동 업데이트, 분기별 바이어스 테스트를 제공하여 사이버 보안 인력 부족에 직면하는 병원 IT 팀을 완화합니다.

지역 분석

2024년 헬스케어 생체인식 시장은 북미가 36.81%의 수익 점유율로 선도했으며, HIPAA의 엄격한 시행, BIPA의 소송 리스크, EHR의 급속한 보급이 그 요인이 되고 있습니다. 병원에서는 정보 유출과 관련된 비용 회피 및 워크플로우 효율성을 고려하면 ROI는 22개월로 짧다고 보고합니다. 연방 정부 기관에서는 퇴역 군인 케어 등록을 위해 멀티 모달 키오스크를 시험적으로 도입하여 조달의 폭을 넓히고 있습니다.

유럽에서는 공공 부문의 강력한 인센티브가 이어지고 있습니다. 유럽 의료 데이터 공간은 국경을 넘어서는 데이터 인프라에 8억 1,000만 유로(9억 4,100만 달러)를 기록하고 있으며, 그중 상당수는 일반 데이터 보호 규칙의 프라이버시 바이 디자인 조항을 충족하기 위해 바이오메트릭스 관리가 필요합니다. 스칸디나비아의 의료 시스템은 이미 환자 포털에 얼굴 인증을 통합했으며 비밀번호가 필요 없는 로그인으로 88%의 사용자 만족도를 기록하고 있습니다.

아시아태평양이 가장 빠르게 진행되고 있습니다. 인도의 Ayushman Bharat은 현재 매일 약 100만 개의 생체인식 ID를 발행하고 있으며 이 지역이 카드 기반 시스템을 뛰어넘는 규모임을 보여줍니다. 일본에서는 마이 넘버 보험증의 전개에 의해 비접촉형의 얼굴 인증이 전국의 1차 케어 진료소에 도입되고 있습니다. 한편 중국에서는 약국 대기시간을 30% 단축하고 현금처리 비용을 절감하는 병원의 얼굴인증레인을 도입하고 있습니다. 이러한 진보는 아시아태평양의 CAGR 25.13%를 뒷받침하고 2030년까지 아시아태평양의 매출을 북미 수준에 가깝게할 것으로 보입니다.

라틴아메리카, 중동 및 아프리카는 형성 단계에 들어가고 있습니다. 브라질과 아랍에미리트(UAE)의 조종사 프로젝트는 생체 인식 ID를 예방 접종 기록과 연결하여 조기이지만 확고한 노력을 보여줍니다. 자금조달의 제약과 인프라의 격차가 단기적인 보급을 억제하고 있지만, 다국간의 의료 디지털화 보조금으로 10년 후반에 걸쳐 보급이 가속될 것으로 예측됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 정부의 E-ID 및 EHR 의무화

- 의료 개인 정보의 도난과 데이터 유출의 급증

- 급속한 EHR 도입으로 안전한 로그인 수요 촉진

- 텔레헬스 ID 온보딩의 급증

- 스마트 병원 IoT용 생체인식 웨어러블

- AI를 활용한 멀티 모달 정밀도의 비약적 진보

- 시장 성장 억제요인

- 높은 기기와 통합 비용

- 프라이버시와 규제 준수의 장애물

- 알고리즘 바이어스 소송 위험

- EHR과 생체인식 API의 상호 운용성의 갭

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측(달러)

- 기술별

- 단일 요소 인증

- 지문 인식

- 얼굴 인식

- 홍채 인식

- 정맥/손바닥 인식

- 행동 생체인식

- 다중 요소 인증

- 다중 모드 생체인식

- Biometric-as-a-Service(BaaS)

- 단일 요소 인증

- 구성 요소별

- 하드웨어

- 소프트웨어

- 서비스

- 용도별

- 환자 식별 및 추적

- 의료기록/데이터센터 보안

- 의료진 인증

- 원격 의료 및 원격 온보딩

- 약국 및 규제 약물 조제

- 가정/원격 환자 모니터링

- 최종 사용자별

- 병원 및 클리닉

- 진단 및 연구 실험실

- 보험사 및 지불 기관

- 재택 간병 및 노인 요양 시설

- 제약 및 생명과학 기업

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Thales Group

- NEC Corporation

- Fujitsu Ltd

- Bio-Key International

- Imprivata Inc

- Suprema Inc

- ZKTeco Inc

- IDEMIA

- HID Global

- Crossmatch

- 3M Cogent

- Integrated Biometrics

- Lumidigm

- FaceTec

- Aratek

- M2SYS

- Vision-Box

- Certis ID

- CLEAR

- Redrock Biometrics

- AnyVision

제7장 시장 기회와 향후 전망

KTH 25.11.04The Healthcare Biometrics Market size is estimated at USD 12.15 billion in 2025, and is expected to reach USD 31.92 billion by 2030, at a CAGR of 21.29% during the forecast period (2025-2030).

The sharp rise is fuelled by digital-health mandates, expanding electronic health record (EHR) ecosystems, and a record wave of data breaches that exposed more than 100 million patient files in 2024 TechCrunch. Mounting medical-identity fraud, government e-ID programs, and the need for password-free clinical workflows now position biometric authentication as critical infrastructure rather than an optional add-on. Hardware still accounts for the majority of spending, yet services register the fastest growth as providers prioritise integration expertise. Asia-Pacific's 25.13% CAGR reflects large-scale public-sector projects, while North America sustains leadership through stringent privacy laws and mature hospital IT estates.

Global Healthcare Biometrics Market Trends and Insights

Government E-ID & EHR Mandates

National digital-identity programs are making biometric verification obligatory in healthcare. Japan's "My Number" insurance cards reached 92.5% provider uptake by December 2024, linking 81 million citizens to facial-recognition terminals. India's Ayushman Bharat Digital Mission enrolled more than 650 million biometric health accounts, simplifying remote registration and record access. Estonia extends the model by embedding AI-driven identity checks across its e-services stack. In the United States, 21st-Century Cures Act compliance pressures hospitals to replace password log-ins with stronger factors, accelerating uptake of biometric single-sign-on. Collectively, these measures ensure enduring demand across economic cycles.

Escalating Medical Identity Theft & Data Breaches

The Change Healthcare ransomware attack compromised over 100 million American records in 2024, the worst breach on record. Subsequent incidents at Kaiser Permanente and other networks illustrate the sector's vulnerability to both cybercrime and unauthorised data-sharing. The National Health Care Anti-Fraud Association pegs annual fraud at USD 68 billion, much of it rooted in misidentification. Pew Charitable Trusts calculates that matching errors alone cost the system USD 6 billion annually. These financial exposures are moving biometrics from discretionary spend to board-level priority.

High Device & Integration Costs

Capital outlays for scanners, servers, and on-site support remain substantial. Smaller practices lack the transaction volume to amortise systems quickly, slowing roll-outs even as return-on-investment models improve. Complex interfacing with legacy health-information systems demands specialist integrators and hikes implementation spend. While cloud-hosted biometric-as-a-service (BaaS) eases some hardware needs, premium subscriptions can strain tight budgets until economies of scale arrive.

Other drivers and restraints analyzed in the detailed report include:

- Rapid EHR Adoption Driving Secure Log-In Demand

- Tele-Health Identity Onboarding Surge

- Privacy & Regulatory Compliance Hurdles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Single-factor authentication held the largest revenue share of 37.31% in 2024, courtesy of mature, cost-effective scanners entrenched in hospital admissions. Nevertheless, multimodal engines are scaling fastest on a 24.76% CAGR as accuracy, spoof resistance, and fail-over capability become strategic purchase criteria across the healthcare biometrics market. NEC's facial-matching system for personalised cancer vaccines exemplifies how multimodal design supports precision medicine workflows.Behavioural biometrics, tracking keystroke cadence and pointer dynamics, is entering EHRs as a background safeguard. Meanwhile, iris and vein recognition gain traction in sterile environments where contact-free operation is vital. Foundation-model breakthroughs lowering false-reject rates are likely to propel multimodal options toward parity with fingerprints by decade-end.

Vendors now sell frameworks that orchestrate face, voice, iris, and behavioural signals in a single software development kit, reducing integration overheads. Hospitals cite a 40% drop in access-card loss incidents post-deployment, freeing operational budgets for patient-centric digital projects. Yet fingerprint systems still appeal to budget-constrained facilities because of inexpensive sensors and wide clinician familiarity.

Hardware commanded 52.26% of 2024 revenue as facilities upgraded entry kiosks, point-of-care devices, and mobile readers. Over the forecast horizon, professional and managed services outpace equipment at 22.99% CAGR by bundling consulting, workflow mapping, and regulatory assurance into fixed-fee packages. SailPoint's purchase of Imprivata's identity-governance line signals the growing premium on healthcare-specific domain knowledge.

Integration complexity remains a critical selling point. Providers allocate 40-60% of total biometric budgets to services that align authentication with clinical-care pathways, ensure HL7/FHIR compatibility, and maintain audit trails. Managed offerings deliver round-the-clock monitoring, automatic algorithm updates, and quarterly bias testing, relieving hospital IT teams that face cybersecurity staffing gaps.

The Healthcare Biometrics Market Report is Segmented by Technology (Single-Factor Authentication, Behavioral Biometrics, and More), Component (Hardware, Software, and Services), Application (Patient Identification and Tracking, and More), End User (Hospital and Clinics, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led the healthcare biometrics market in 2024 with 36.81% revenue share, propelled by stringent HIPAA enforcement, BIPA litigation risk, and rapid EHR penetration. Hospitals report ROI windows as short as 22 months when factoring breach-related cost avoidance and workflow efficiencies. Federal agencies are piloting multimodal kiosks for veteran-care enrolment, broadening procurement pools.

Europe follows with robust public-sector incentives. The European Health Data Space earmarks EUR 810 (USD 941) million for cross-border data infrastructure, much of which requires biometric controls to meet the General Data Protection Regulation's privacy-by-design clause. Scandinavian health systems already embed facial verification in patient portals, clocking 88% user-satisfaction scores for password-less log-ins.

Asia-Pacific is the fastest mover. India's Ayushman Bharat now issues roughly 1 million biometric IDs daily, illustrating the scale at which the region is leapfrogging card-based systems. Japan's roll-out of My Number insurance cards brings contactless face authentication to primary-care clinics nationwide. China, meanwhile, deploys hospital facial-payment lanes that shorten pharmacy queues by 30% and lower cash-handling costs. These advances underpin a 25.13% CAGR that will lift Asia-Pacific close to North American revenue levels by 2030.

Latin America, the Middle East, and Africa are entering a formative phase. Pilot projects in Brazil and the United Arab Emirates tie biometric ID to vaccination records, indicating early but firm commitment. Funding constraints and infrastructure gaps temper near-term volumes, yet multilateral health-digitisation grants are expected to accelerate adoption through the second half of the decade

- Thales Group

- NEC

- Fujitsu Ltd

- Bio-Key International

- Imprivata

- Suprema

- ZKTeco Inc

- IDEMIA

- HID Global

- Crossmatch

- 3M Cogent

- Integrated Biometrics

- Lumidigm

- FaceTec

- Aratek

- M2SYS

- Vision-Box

- Certis ID

- CLEAR

- Redrock Biometrics

- AnyVision

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government E-ID & EHR Mandates

- 4.2.2 Escalating Medical Identity Theft & Data Breaches

- 4.2.3 Rapid EHR Adoption Driving Secure Log-In Demand

- 4.2.4 Tele-Health Identity Onboarding Surge

- 4.2.5 Biometric Wearables for Smart-Hospital IoT

- 4.2.6 AI-Powered Multimodal Accuracy Breakthroughs

- 4.3 Market Restraints

- 4.3.1 High Device & Integration Costs

- 4.3.2 Privacy & Regulatory Compliance Hurdles

- 4.3.3 Algorithmic Bias Litigation Risk

- 4.3.4 EHR-Biometric API Interoperability Gaps

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Technology

- 5.1.1 Single-factor Authentication

- 5.1.1.1 Fingerprint Recognition

- 5.1.1.2 Facial Recognition

- 5.1.1.3 Iris Recognition

- 5.1.1.4 Vein/Palm Recognition

- 5.1.2 Behavioral Biometrics

- 5.1.3 Multi-factor Authentication

- 5.1.4 Multimodal Biometrics

- 5.1.5 Biometric-as-a-Service (BaaS)

- 5.1.1 Single-factor Authentication

- 5.2 By Component

- 5.2.1 Hardware

- 5.2.2 Software

- 5.2.3 Services

- 5.3 By Application

- 5.3.1 Patient Identification & Tracking

- 5.3.2 Medical Record / Data-Centre Security

- 5.3.3 Care-provider Authentication

- 5.3.4 Tele-Health & Remote Onboarding

- 5.3.5 Pharmacy & Controlled-Substance Dispensing

- 5.3.6 Home / Remote Patient Monitoring

- 5.4 By End User

- 5.4.1 Hospitals & Clinics

- 5.4.2 Diagnostic & Research Laboratories

- 5.4.3 Insurance & Payers

- 5.4.4 Home Care & Aged Care Facilities

- 5.4.5 Pharma & Life Science Companies

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Thales Group

- 6.3.2 NEC Corporation

- 6.3.3 Fujitsu Ltd

- 6.3.4 Bio-Key International

- 6.3.5 Imprivata Inc

- 6.3.6 Suprema Inc

- 6.3.7 ZKTeco Inc

- 6.3.8 IDEMIA

- 6.3.9 HID Global

- 6.3.10 Crossmatch

- 6.3.11 3M Cogent

- 6.3.12 Integrated Biometrics

- 6.3.13 Lumidigm

- 6.3.14 FaceTec

- 6.3.15 Aratek

- 6.3.16 M2SYS

- 6.3.17 Vision-Box

- 6.3.18 Certis ID

- 6.3.19 CLEAR

- 6.3.20 Redrock Biometrics

- 6.3.21 AnyVision

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment