|

시장보고서

상품코드

1850048

헬스케어 자산 관리 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Healthcare Asset Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

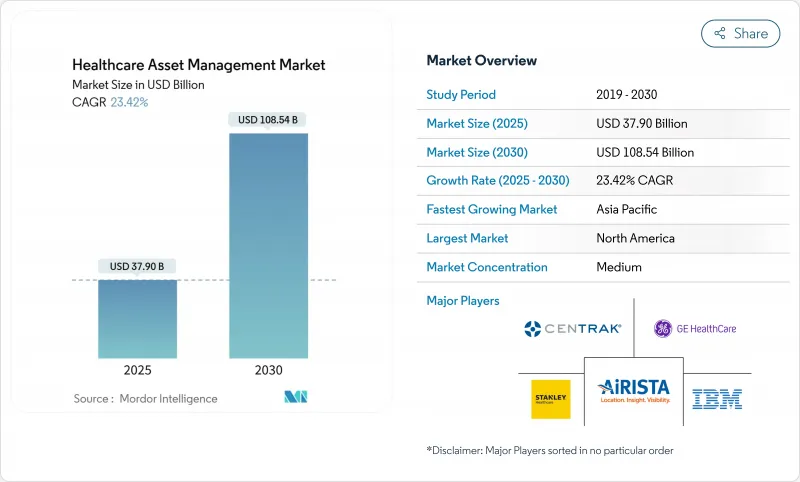

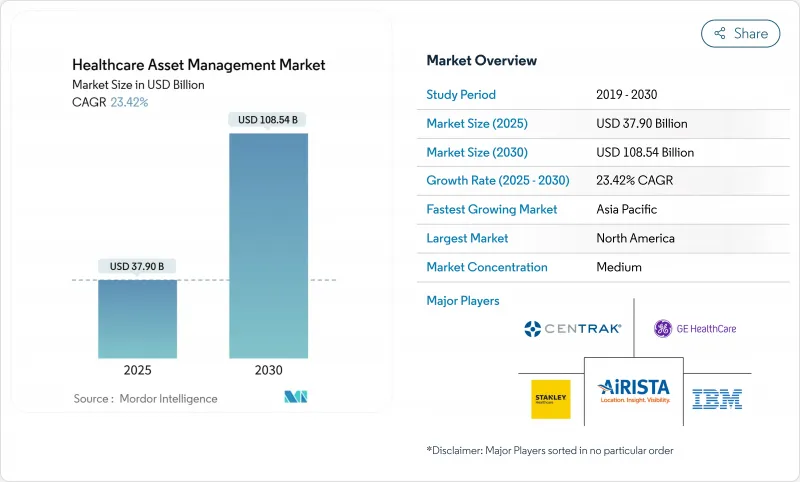

헬스케어 자산 관리 시장 규모는 2025년 379억 달러로 추정되고, 예측 기간(2025-2030년)의 CAGR은 23.42%를 나타낼 전망이며, 2030년에는 1,085억 4,000만 달러에 달할 것으로 예상됩니다.

이 성장 궤도는 규제의 의무화, 노동력 부족, 사이버 보안에 대한 기대가 자산 추적을 비용 억제 도구에서 디지털 의료 업무의 전략적 기둥으로 재배치하기 위해 어떻게 수렴하는지를 반영합니다. 병원은 바코드를 통한 재고 관리뿐만 아니라 FDA가 2024년에 개발한 기기 보안 지침 준수를 간소화하는 커넥티드 플랫폼에도 주목하고 있습니다. 수요는 또한 간호 직원의 제약과 직접 연결되어 있습니다. 임상 능력의 감소는 간병인이 장비의 위치를 확인하는 것에서 해방되고 대신 환자의 결과에 집중할 수 있도록 하는 시스템의 가치를 확대하고 있습니다. 이와 병행하여, 태그에 통합된 예측 분석은 유지보수가 사후 대응에서 예측 대응으로 이동하여 다운타임을 줄이고 자산 수명을 연장시킵니다. 이러한 힘을 결합하면 병원, 제약 공장 및 연구소가 통합 가시성, 사이버 보안 및 분석을 선택적 부가 기능이 아닌 양보할 수 없는 기능으로 간주하는 헬스케어 자산 관리 시장 환경을 실현할 수 있습니다.

세계의 헬스케어 자산 관리 시장 동향 및 인사이트

의약품 위조 방지를 위한 RFID 수요 증가

의약품 위조는 세계 경제에서 매년 2,000억 달러의 추정치를 유출시키고 있으며, 규제 당국은 엔드 투 엔드 시각화를 필수로 하는 직렬화 및 혈통 증명 요건을 부과하도록 촉구하고 있습니다. 미국 의약품 공급망 보안법(Drug Supply Chain Security Act)에서는 의약품 제조업체, 도매업체 및 제약 약국이 제품을 배달할 때마다 제품의 출처를 증명해야 합니다. 암호화 인증 RFID는 품목 수준의 식별과 온도에 민감한 생물학적 제제에 필요한 실시간 환경 모니터링을 결합하여 현재 이러한 배치의 대부분을 지원합니다. 2024년 이후 반도체 부족으로 인해 태그 가격은 최대 20% 상승했지만 컴플라이언스 위반 벌금과 리콜 비용이 하드웨어 지출을 훨씬 웃돌아 기업은 여전히 투자를 하고 있습니다. 사토와 같은 공급업체는 인증과 워크플로우 효율성을 모두 하나의 공정 단계에서 실현하는 멸균 방지 태그를 발표했습니다. 이러한 요인은 2025년부터 2030년까지 제약 및 생명공학 제조 고객이 예측하는 CAGR 26.8%를 나타낼 전망입니다.

간호 직원 부족으로 인한 효율화 압력

도시의 주요 병원에서는 간호사의 결원률이 15%를 넘어서 케어 팀이 늘어나고 관리자는 지원 기술로부터 가능한 한 효율화를 도모할 필요가 있습니다. 설문조사에 따르면 간호사는 각 이동의 5분의 1 이상을 잃어버린 기구를 검색하는 데 소비하고 있습니다. 수색 시간을 90% 이상 단축하는 RTLS의 구현은 인원을 늘리지 않고 침대에 인원을 계속 배치하는 직접적인 노동력을 제공합니다. 영국 시설에서는 장비 1대당 시간이 60분에서 10분으로 단축되어 환자 안전 점수 향상과 직원 정착률 개선으로 이어졌습니다는 것이 입증되었습니다. 첨단 배포는 BLE 배지, 공황 버튼, 예측 분석을 결합하여 임상의가 요구하기 전에 장치에 장비를 설치하여 워크플로 부담을 줄이고 만족도를 높입니다.

데이터 프라이버시 및 사이버 보안에 대한 우려

헬스케어의 정보 유출의 평균 비용은 2024년에 1건당 977만 달러에 이르렀으며 보안 위험이 신속한 배포의 중요한 억제력이 되었습니다. FDA의 2024년 판 지침 초안은 시판 전 보안 테스트를 강화하도록 요구하고 있으며, 구매자는 프로덕션 전에 암호화, 네트워크 세그먼테이션 및 지속적인 모니터링에 자금을 제공하도록 강제되었습니다. 따라서 많은 병원은 On-Premise(On-premise) 배포 및 클라우드로의 데이터 흐름을 제한하는 에어 갭 네트워크로 시작하여 위험을 줄이기 위해 분석 기능의 일부를 거래하고 있습니다. 안전한 펌웨어가 없는 레거시 장치는 통합을 더욱 복잡하게 하고 프로젝트 일정을 늘리고 예산을 부풀립니다.

부문 분석

RFID는 2024년 매출의 56.2%를 차지하며 수십년에 걸친 프로토콜의 성숙과 견고한 공급망을 통해 의약품 재고 및 수술 키트 추적의 기본 기술이 된 것을 뒷받침했습니다. RFID의 헬스케어 자산 관리 시장 규모는 2024년에 213억 달러에 달해 이 모달리티가 POC(Point-of-Care) 캐비닛과 중앙 무균 처리에 얼마나 깊이 침투하고 있는지를 보여주었습니다. 그러나 소프트웨어에 정의된 워크플로우는 ID 뿐만 아니라 위치 정보를 점점 더 필요로 합니다. 따라서 BLE, Wi-Fi, 울트라 와이드 밴드를 활용한 실시간 위치추적 시스템은 2030년까지 연평균 복합 성장률(CAGR) 28.1%를 나타내 정적 RFID 성장을 막을 것으로 예상되고 있습니다.

벤더가 RFID와 RTLS를 수동 ID와 실시간 원격 측정 사이를 오가는 멀티 모드 태그에 통합하면 두 번째 성장 단계가 나타납니다. 패시브 RFID는 비싼 약제의 수축을 제한하고 RTLS는 주입 펌프가 환자의 상태가 가장 급변하는 곳에서 순환하도록 보장합니다. 태그, 게이트웨이, 엑사이터가 전체 캠퍼스를 덮고 있기 때문에 하드웨어가 여전히 지출의 대부분을 차지하고 있지만 이익 풀은 장치 식별, 위치 및 사용을 단일 대시보드로 통합하는 플랫폼 라이선스로 이동합니다. 이러한 수렴이 진행됨에 따라 헬스케어 자산 관리 시장은 단일 모드 제품을 틈새 시장으로 간주할 것으로 보입니다.

2024년 매출의 62.4%를 하드웨어가 차지한 것은 수백만개의 태그, 리더, 천장 내장형 비콘의 지속적인 구매 때문입니다. 그럼에도 불구하고 병원이 자본 지출에서 관리되는 성과로 축발을 옮기면서 서비스는 CAGR 25.6%로 선행합니다. 구독 계약에서 공급업체는 업타임, 펌웨어 최신성 및 규제 대응 감사 로그를 보장하므로 IT 팀은 환자 대응에 전념할 수 있습니다. 서비스와 관련된 헬스케어 자산 관리 시장 규모는 2030년까지 326억 달러에 이를 것으로 예상되고 있으며, 인프라가 유비쿼터스가 되고 차별화가 컨설팅 최적화로 전환되는 성숙 주기를 제시합니다.

또한 전문 서비스 및 관리 서비스는 변경 관리, 시스템 통합 및 사이버 보안 인증과 같은 가장 어려운 오류를 해결합니다. 서비스 계약은 일반적으로 원격 장비 상태 확인, 알고리즘 업데이트, 컴플라이언스 문서 작성을 번들로 제공하며 비용은 여러 해 동안 균등하게 분산되며 상환주기와 일치합니다. 병원은 간호사의 과도한 근무 회피, 침대 회전 속도 향상, 장비 대여 감소로월사용료가 상쇄됨을 보여 계약을 정당화하는 경우가 늘고 있습니다.

헬스케어 자산 관리 시장은 기술(RFID, 실시간 위치추적 시스템 등), 구성요소(하드웨어, 소프트웨어, 서비스), 용도(기기, 장치 추적, 재고/공급 체인 관리 등), 최종 사용자(병원, 클리닉, 연구소, 진단센터 등), 지역별로 구분됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

지역 분석

북미는 2024년 매출의 37.8%를 차지하며 미국의 종합적인 직렬화법, 성숙한 EHR 백본, 통합된 안전한 플랫폼을 지지하는 의료기기 사이버 위협의 사건 증가에 의해 지원되었습니다. 캐나다의 각 주에서도 비슷한 정책이 채택되고 있으며, 멕시코의 민간 병원은 의료 관광객 확보와 미국 보험 회사의 감사를 충족하기 위해 자산 추적에 투자하고 있습니다. 안전 부족에 벌금을 부과하는 정부의 상환 모델은 이력회를 이사회 수준의 지표로 삼고, 이 지역의 헬스케어 자산 관리 시장의 채택을 더욱 강화하고 있습니다.

아시아태평양은 가장 빠르게 성장하는 지역으로, 2030년까지 연평균 복합 성장률(CAGR)은 22.5%를 나타낼 전망입니다. 중국, 인도, 동남아시아 공립병원 건설계획에서는 기존 바코드 절차를 생략하고 RFID-RTLS 컨버전스를 첫날부터 구현하는 그린필드 전개가 가능합니다. 이러한 시설 중 상당수는 자산 관리를 국가의 디지털 헬스 클라우드와 통합하여 지역 공급망 전체에서 실시간 의약품 인증을 가능하게 합니다. 설비 투자가 국민 모두 보험 목표에 부합하기 때문에 벤더는 수백 개의 새로운 병원을 다루는 다년간의 기본 계약을 보고했습니다.

유럽에서는 EU-MDR의 의무화, EUDAMED 데이터베이스의 전개, 라이프사이클의 최적화를 지지하는 국가의 지속가능성 목표에 견인되어 꾸준히 도입이 진행되고 있습니다. 독일과 영국이 조기 도입을 견인하고 있지만 동유럽에서는 구조기금이 디지털 전환을 중시하고 있기 때문에 자금조달 메커니즘이 따라잡고 있습니다. GDPR(EU 개인정보보호규정)을 기반으로 사이버 보안에 대한 기대는 On-Premise 및 하이브리드 클라우드에 대한 수요를 높이고 현지 데이터 레지던시를 실현함으로써 플랫폼 공급업체는 구성 옵션을 넓힐 수 있습니다. Brexit은 국경을 넘어서는 의료 무역에 세관의 복잡성을 더해주는 반면 영국 공급자는 항구 지연과 제품 낭비를 피하기 위해 추적성을 강조합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 시장 성장 촉진요인

- 의약품 위조 방지를 위한 RFID 수요 증가

- 간호 스탭 부족에 의한 효율화의 압력

- 환자 안전 규제(예 : UDI, EU-MDR)

- 태그에 내장된 AI 기반 예측 유지보수

- 자산 추적 가능성에 연결된 성과 보상

- 시장 성장 억제요인

- 데이터 프라이버시와 사이버 보안에 대한 우려

- 고액의 RTLS/RFID 인프라 초기 비용

- 중요한 무선 의료기기에의 무선 간섭

- 단편화된 레거시 CMMS가 통합을 지연

- 업계 밸류체인 분석

- 규제 상황

- 기술의 전망

- 업계의 매력 - Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 거시 경제 요인이 시장에 미치는 영향

제5장 시장 규모와 성장 예측(금액관)

- 기술별

- RFID

- 실시간 위치 추적 시스템(RTLS)

- 블루투스 저에너지(BLE) 및 Wi-Fi

- 적외선 및 초음파

- 구성 요소별

- 하드웨어(태그, 리더, 게이트웨이)

- 소프트웨어(분석, 미들웨어)

- 서비스(배포, 관리형, 교육)

- 용도별

- 장비 및 기기 추적

- 재고/공급망 관리

- 환자 및 직원 추적

- 병상 및 수용 능력 관리

- 환경 및 상태 모니터링

- 최종 사용자별

- 병원 및 진료소

- 연구소 및 진단센터

- 의약품 및 생명공학 제조

- 장기 요양 및 간병 시설

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 칠레

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 말레이시아

- 싱가포르

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 이집트

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Stanley Healthcare(Stanley Black & Decker)

- CenTrak Inc.

- AiRISTA Flow Inc.

- GE HealthCare Technologies Inc.

- IBM Corporation

- Infor Inc.

- Motorola Solutions Inc.

- Siemens Healthineers AG

- Accenture plc

- Sonitor Technologies AS

- Zebra Technologies Corporation

- Johnson Controls(Tyco International)

- Honeywell International Inc.

- Impinj Inc.

- Alien Technology LLC

- HID Global Corporation

- Ascom Holding AG

- Midmark Corporation(Versus RTLS)

- Trimble Inc.(Atrius)

- Cerner Corporation(Oracle Health)

- TagMaster AB

- Radianse LLC

- Kontakt.io Inc.

- Litum IoT Technologies

- Elpas Ltd.(Securitas)

제7장 시장 기회와 미래 동향

- 백스페이스 및 미충족 수요(Unmet Needs) 평가

The Healthcare Asset Management Market size is estimated at USD 37.90 billion in 2025, and is expected to reach USD 108.54 billion by 2030, at a CAGR of 23.42% during the forecast period (2025-2030).

The growth trajectory reflects how regulatory mandates, workforce shortages, and cybersecurity expectations converge to reposition asset tracking from a cost-containment tool to a strategic pillar of digital health operations. Hospitals are looking beyond bar-code inventory toward connected platforms that streamline compliance with the FDA's 2024 device-security guidance, an obligation that can consume 5% or more of a manufacturer's annual revenue. Demand also ties directly to nursing-staff constraints; shrinking clinical capacity magnifies the value of systems that free caregivers from locating equipment and instead let them focus on patient outcomes. In parallel, predictive analytics embedded in tags move maintenance from reactive to anticipatory, trimming downtime and extending asset life. Taken together, these forces enable a healthcare asset management market environment in which hospitals, pharma plants, and laboratories regard integrated visibility, cybersecurity, and analytics as non-negotiable features rather than optional add-ons.

Global Healthcare Asset Management Market Trends and Insights

Rising demand for RFID to curb drug counterfeiting

Pharmaceutical counterfeiting drains an estimated USD 200 billion from the global economy each year, prompting regulators to impose serialisation and pedigree requirements that make end-to-end visibility indispensable. Under the U.S. Drug Supply Chain Security Act, drug makers, wholesalers, and dispensers must prove product provenance at every hand-off. RFID with cryptographic authentication now underpins most of these deployments because it combines item-level identification with real-time environmental monitoring, a necessity for temperature-sensitive biologics. Semiconductor shortages since 2024 lifted tag prices by up to 20%, yet organisations still invest because non-compliance fines and recall costs far exceed hardware spending. Vendors such as SATO have introduced sterilisation-resistant tags that deliver both authentication and workflow efficiency in one process step. These factors underpin the 26.8% CAGR projected for pharmaceutical and biotech manufacturing customers between 2025 and 2030.

Efficiency pressures from nursing-staff shortages

Nursing vacancy rates above 15% in major urban hospitals leave care teams stretched and force administrators to squeeze every efficiency gain possible from support technology. Studies reveal that nurses spend over one-fifth of each shift searching for missing equipment; RTLS implementations that cut search time by more than 90% therefore provide a direct labour dividend that keeps beds staffed without adding headcount. British facilities have demonstrated time reductions from 60 minutes to 10 minutes per device, translating into heightened patient-safety scores and improved staff retention. Advanced deployments now combine BLE badges, panic buttons, and predictive analytics that stage equipment on units before clinicians request it, easing workflow strain and boosting satisfaction.

Data-privacy and cybersecurity concerns

Average breach costs in healthcare reached USD 9.77 million per incident in 2024, making security risk a material deterrent to rapid roll-outs. The FDA's 2024 draft guidance urges stronger pre-market security testing, compelling buyers to fund encryption, network segmentation, and continuous monitoring before go-live. Many hospitals, therefore, begin with on-premises deployments or air-gapped networks that limit data flow to the cloud, trading some analytics capability for risk reduction. Legacy devices without secure firmware further complicate integrations, extending project timelines and inflating budgets.

Other drivers and restraints analyzed in the detailed report include:

- Patient-safety regulations (UDI, EU-MDR)

- AI-based predictive maintenance embedded in tags

- High upfront RTLS/RFID infrastructure cost

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

RFID accounted for 56.2% of 2024 revenue, underlining decades of protocol maturity and robust supply chains that made the technology the default for drug inventory and surgical kit tracking. The healthcare asset management market size for RFID was USD 21.3 billion in 2024, showing how deeply the modality is entrenched at point-of-care cabinets and central sterile processing. Yet software-defined workflows increasingly require location, not just identity. Real-Time Location Systems leveraging BLE, Wi-Fi, and ultra-wideband are therefore forecast to compound at 28.1% CAGR to 2030, eating into static RFID growth.

A second growth phase emerges as vendors collapse RFID and RTLS into multi-mode tags that pivot between passive ID and real-time telemetry, a design that preserves prior capital investment while enabling richer analytics. Deployments at paediatric-care centres demonstrate this twin-mode value: passive RFID limits shrinkage of high-value drugs, while RTLS ensures infusion pumps circulate where patient acuity is highest. Hardware still dominates spending because tags, gateways, and exciters blanket entire campuses; however, the profit pool is shifting toward platform licences that unite device identity, location, and utilisation into one dashboard. As this convergence proceeds, the healthcare asset management market will likely regard single-mode offerings as a niche.

Hardware captured 62.4% of 2024 sales thanks to ongoing purchases of millions of tags, readers, and ceiling-mounted beacons. Even so, services are pacing ahead with a 25.6% CAGR as hospitals pivot from capital expense toward managed outcomes. Under subscription agreements, vendors guarantee uptime, firmware currency, and regulatory-ready audit logs, freeing IT teams to focus on patient-facing initiatives. The healthcare asset management market size tied to services is forecast to reach USD 32.6 billion by 2030, pointing to a maturation cycle where infrastructure becomes ubiquitous and differentiation shifts to consultative optimisation.

Professional and managed services also address the hardest obstacles-change management, systems integration, and cybersecurity accreditation-that no amount of shelf hardware alone can solve. Service contracts typically bundle remote device health checks, algorithm updates, and compliance documentation generation, costs that spread evenly across multi-year terms and match reimbursement cycles. Hospitals increasingly justify deals by showing that avoided nursing overtime, faster bed turnover, and reduced device rentals offset monthly subscription fees.

Healthcare Asset Management Market is Segmented by Technology (RFID, Real-Time Location Systems, and More), Component (Hardware, Software, and Services), Application (Equipment and Device Tracking, Inventory/Supply-Chain Management, and More), End-User (Hospitals and Clinics, Laboratories and Diagnostic Centers, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 37.8% of 2024 revenue, sustained by the United States' comprehensive serialisation law, a mature EHR backbone, and rising incidents of medical device cyber threats that favour integrated, secure platforms. Canadian provinces are adopting similar policies, while Mexican private-sector hospitals invest in asset tracking to retain medical tourists and satisfy U.S. insurer audits. Government reimbursement models that penalise safety lapses make traceability a board-level metric, further supporting healthcare asset management market adoption across the region.

Asia-Pacific is the fastest-growing area with a 22.5% CAGR expected through 2030. Public-hospital construction programmes in China, India, and Southeast Asia enable greenfield deployments that skip legacy bar-code steps and implement RFID-RTLS convergence from day one. Many of these facilities integrate asset management with national digital-health clouds, allowing real-time drug authentication across regional supply chains. As capital investment aligns with universal health-coverage goals, vendors report multi-year master contracts covering hundreds of new hospitals.

Europe shows steady uptake led by the EU-MDR mandate, EUDAMED database roll-outs, and national sustainability targets that favour lifecycle optimisation. Germany and the United Kingdom drive early deployments, but funding mechanisms in Eastern Europe are catching up as structural funds emphasise digital transformation. Cybersecurity expectations anchored in GDPR elevate demand for on-premises or hybrid clouds with local data residency, nudging platform suppliers to broaden configuration options. With Brexit adding customs complexity for cross-channel medical trade, British providers rely on traceability to avoid port delays and product waste.

- Stanley Healthcare (Stanley Black & Decker)

- CenTrak Inc.

- AiRISTA Flow Inc.

- GE HealthCare Technologies Inc.

- IBM Corporation

- Infor Inc.

- Motorola Solutions Inc.

- Siemens Healthineers AG

- Accenture plc

- Sonitor Technologies AS

- Zebra Technologies Corporation

- Johnson Controls (Tyco International)

- Honeywell International Inc.

- Impinj Inc.

- Alien Technology LLC

- HID Global Corporation

- Ascom Holding AG

- Midmark Corporation (Versus RTLS)

- Trimble Inc. (Atrius)

- Cerner Corporation (Oracle Health)

- TagMaster AB

- Radianse LLC

- Kontakt.io Inc.

- Litum IoT Technologies

- Elpas Ltd. (Securitas)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for RFID to curb drug counterfeiting

- 4.2.2 Efficiency pressures from nursing?staff shortages

- 4.2.3 Patient-safety regulations (e.g., UDI, EU-MDR)

- 4.2.4 AI-based predictive maintenance embedded in tags

- 4.2.5 Pay-for-performance reimbursement tied to asset traceability

- 4.3 Market Restraints

- 4.3.1 Data-privacy and cybersecurity concerns

- 4.3.2 High upfront RTLS/RFID infrastructure cost

- 4.3.3 Radio-interference with critical wireless medical devices

- 4.3.4 Fragmented legacy CMMS slowing integration

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Technology

- 5.1.1 RFID

- 5.1.2 Real-Time Location Systems (RTLS)

- 5.1.3 Bluetooth Low Energy (BLE) and Wi-Fi

- 5.1.4 Infrared and Ultrasound

- 5.2 By Component

- 5.2.1 Hardware (Tags, Readers, Gateways)

- 5.2.2 Software (Analytics, Middleware)

- 5.2.3 Services (Deployment, Managed, Training)

- 5.3 By Application

- 5.3.1 Equipment and Device Tracking

- 5.3.2 Inventory/Supply-Chain Management

- 5.3.3 Patient and Staff Tracking

- 5.3.4 Bed and Capacity Management

- 5.3.5 Environmental and Condition Monitoring

- 5.4 By End-user

- 5.4.1 Hospitals and Clinics

- 5.4.2 Laboratories and Diagnostic Centers

- 5.4.3 Pharmaceutical and Biotech Manufacturing

- 5.4.4 Long-Term Care and Assisted-Living Facilities

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Malaysia

- 5.5.4.7 Singapore

- 5.5.4.8 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Stanley Healthcare (Stanley Black & Decker)

- 6.4.2 CenTrak Inc.

- 6.4.3 AiRISTA Flow Inc.

- 6.4.4 GE HealthCare Technologies Inc.

- 6.4.5 IBM Corporation

- 6.4.6 Infor Inc.

- 6.4.7 Motorola Solutions Inc.

- 6.4.8 Siemens Healthineers AG

- 6.4.9 Accenture plc

- 6.4.10 Sonitor Technologies AS

- 6.4.11 Zebra Technologies Corporation

- 6.4.12 Johnson Controls (Tyco International)

- 6.4.13 Honeywell International Inc.

- 6.4.14 Impinj Inc.

- 6.4.15 Alien Technology LLC

- 6.4.16 HID Global Corporation

- 6.4.17 Ascom Holding AG

- 6.4.18 Midmark Corporation (Versus RTLS)

- 6.4.19 Trimble Inc. (Atrius)

- 6.4.20 Cerner Corporation (Oracle Health)

- 6.4.21 TagMaster AB

- 6.4.22 Radianse LLC

- 6.4.23 Kontakt.io Inc.

- 6.4.24 Litum IoT Technologies

- 6.4.25 Elpas Ltd. (Securitas)

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-Space and Unmet-Need Assessment