|

시장보고서

상품코드

1850075

마취 모니터링 기기 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Anesthesia Monitoring Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

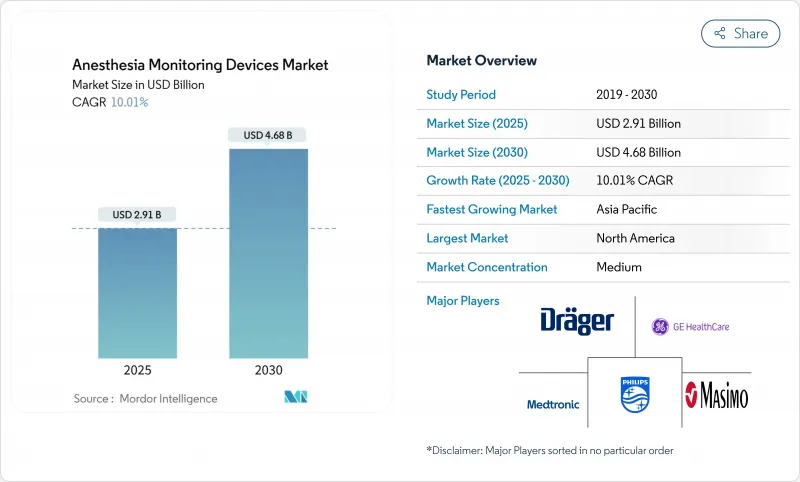

마취 모니터링 기기 시장의 2025년 시장 규모는 29억 1,000만 달러로 추정되고, 2030년에는 46억 8,000만 달러에 이를 전망이며, CAGR 10.01%로 성장할 것으로 예측됩니다.

성장 요인은 수술 건수 증가, 인공지능을 활용한 예측 분석, 주술기에 보다 깊은 경계를 필요로 하는 고령화입니다. 통합 워크스테이션은 환기, 가스 공급 및 다중 매개변수 추적을 하나의 실적로 통합하고 수술실 워크플로우를 간소화하기 위해 여전히 마취 모니터링 기기 시장의 핵심이 되었습니다. 동시에 AI를 구사한 고급 모니터는 뇌 활동이나 침해 수용 추적 등 특수한 용도에 수요를 견인해 반응적 케어에서 예측적 케어로의 시프트를 시사하고 있습니다. 외래 환자로의 전환은 또 다른 기폭제입니다. 치료가 외래수술센터(ASC)로 이동함에 따라 병원 수준의 정확도 기준을 충족하는 휴대용 시스템이 중요해집니다. 지역별로는 북미가 상환과 조기 기술 도입으로 안정을 공급하고 있지만, 아시아태평양이 가장 급성장하고 있는 지역이며, 이것은 수입 의존을 삭감하는 정책적 뒷받침이 있는 현지화 추진 덕분입니다.

세계의 마취 모니터링 기기 시장 동향 및 인사이트

마취 기술 개발 및 기록 관리 자동화

자동화된 마취정보관리 시스템(AIMS)은 수작업에 의한 의료진의 실수를 40% 절감하여 임상의가 환자 진료에 전념할 수 있도록 합니다. Philips의 IntelliSpace Critical Care and Anesthesia는 실시간 바이탈을 전자 의료 기록에 직접 입력하는 터치 조작에 최적화된 대시보드로 이 트렌드를 보여줍니다. 폐쇄 루프 컨트롤러는 이미 혈행 역학 안정성에서 수동 적정을 능가하고 있으며, 과거의 머신러닝 피드백에 의해 구동되는 정밀 프로토콜의 단계를 설정했습니다. 이러한 이익은 안전 마진의 향상과 관리 부하와 관련된 임상의의 소진 증후군의 감소라는 두 가지 목적에 부합합니다. 결과적으로 병원은 통합 AIMS를 데이터 풍부한 마취 모니터링 기기 시장 전략의 핵심으로 취급합니다.

무통 수술에 대한 수요 증가

오피오이드를 절약한 신속한 회복에 대한 환자의 기대는 객관적인 침해 수용 지표에 의존하는 멀티모달 기술에 박차를 가하고 있습니다. NOL 지수(R) 핑거 프로브는 4개의 광전식 근전도 채널을 0-100의 통증 점수로 변환하여 마취과 의사가 진통제를 조정할 때 유용합니다. 검증 연구에서는 적외선의 파장과 개별화된 알고리즘이 개인의 반응을 정규화하고 주술기 의료에 있어서의 공평성의 우려에 대답하기 때문에 인종에 관계없이 균일한 정밀도가 확인되고 있습니다. 당일 퇴원이 보통인 ASC에서는 NOL 모니터링은 호흡 억제를 억제하고 동원을 가속화하는 ERAS 경로와 연동하고 있습니다. 결과적으로, 통증이없는 프로토콜은 환자 중심의 결과를 따라 센서에 대한 투자로 마취 모니터링 기기 시장을 강화합니다.

높은 자본 비용 및 선행 기술 선호

경제적 평가에 따르면 BIS 모니터링은 회피되는 리콜 사건 1건당 10,000-2만 5,000달러의 비용이 들고, 보편적으로 채용된 경우 연간 지출에 10억 달러를 올릴 수 있습니다. TIVA는 또한 저유량 흡입 전략보다 변동비가 높고 자원에 제한이 있는 시스템이 레거시 모니터를 선호하게 됩니다. 예산의 압박, 훈련의 오버헤드, 규제의 타성에 의해 첨단 디바이스의 도입이 늦어지고, 루틴 케이스에서는 기본 모니터로 충분한 마취 모니터링 기기 시장의 발판이 되고 있습니다.

부문 분석

2024년 마취 모니터링 기기 시장에서는 통합 워크스테이션이 41.34%의 점유율을 차지했으며, 병원이 가스 공급, 인공호흡기 및 모니터를 통합한 단일 콘솔 솔루션을 요구했기 때문입니다. 어드밴스드 모니터는 설치 대수가 적지만, 뇌와 통증의 지표에 대응하는 AI 모듈을 활용하여 기존의 극장에 뒷받침함으로써 2030년까지 연평균 복합 성장률(CAGR) 10.78%로 확대될 전망입니다. 기본 모니터 및 소모품은 특히 신흥 시장 및 중복성 백업으로 저비용 레이어를 유지합니다. GE Healthcare의 Aisys(TM) CS2는 신선한 가스 공급을 자동화하고 워크스테이션 플랫폼이 지속가능성과 비용 절감을 통합하고 마취 모니터링 기기 시장에서 필수적인 앵커가 되는 방법을 보여줍니다.

소모품은 자본 사이클보다 수기 횟수에 연동한 꾸준한 성장을 보여줍니다. 사이버 보안은 구매 기준을 형성합니다. 통합된 워크스테이션은 흩어져 있는 단일 파라미터 장비에 비해 공격 표면을 감소시킵니다. 그 결과, 조달팀은 임상 성능과 함께 사이버 내성을 평가하게 되었으며, 마취 모니터링 기기 업계에서의 통합 솔루션의 매력을 더욱 향상시키고 있습니다.

지역 분석

북미는 2024년 마취 모니터링 기기 시장의 38.68% 매출을 창출했습니다. 이것은 조기 AI 도입, 상환 범위, 통합 공급업체 기반이 배경에 있습니다. CISA와 같은 기관에 의한 규제의 명확화와 사이버 보안 가이던스가 조달 결정을 가속화하고, 주요 벤더는 국내 제조 거점을 활용해 공급망 쇼크를 회피하고 있습니다.

아시아태평양은 중국과 인도가 현지화를 가속화하고 있기 때문에 2030년까지 연평균 복합 성장률(CAGR)이 10.86%로 선도할 것으로 예측됩니다. 중국의 기기 시장은 2024년 363억 5,000만 달러에서 2029년 556억 7,000만 달러로 증가할 예정입니다. 이는 수입 의존도를 85%에서 50% 이하의 기준치로 줄이는 Made in China 2025의 인센티브에 의해 지원됩니다. 인도에서는 개조품의 수입을 제한하고 2030년까지 500억 달러의 의료기술 분야를 목표로 하여 국산 마취 모니터링 플랫폼에 길을 열고 있습니다. 이러한 움직임은 지역 OEM 및 세계 합작 파트너의 마취 모니터링 기기 시장 규모를 확대합니다.

유럽은 EU 의료기기 규제 하에서 1자리대 중반의 성장을 유지하고 구매자의 신뢰를 강화하는 에코디자인과 시판 후 조사를 향해 공급업체를 뒷받침하고 있습니다. 중동 및 아프리카는 걸프의 의료 관광 회랑과 관련된 병원 건설 프로젝트를 유치하고 다국어 사용자 인터페이스를 갖춘 통합 워크 스테이션에 대한 수요를 유발합니다. 남미에서는 브라질과 아르헨티나에서 공립 병원의 현대화가 가속화되고 있지만, 환율 변동으로 인해 조달주기가 불안정합니다. 전반적으로, 마취 모니터링 기기 시장은 지리적 다양화에 의해 지역 특유의 충격으로부터 보호되며, 두 자리의 세계 확장을 유지하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 마취 기술 및 자동 기록 관리 개발

- 통증이 없는 수술에 대한 수요 증가

- 고령화에 의한 수술 건수 증가

- 수술 중 모니터링을 위한 AI 구동형 예측 분석

- 통각 모니터링을 추진하는 오피오이드 절약 프로토콜

- 분산형 외래 진료 환경용 휴대용 모니터

- 시장 성장 억제요인

- 높은 자본 비용 및 기존 기술에 대한 편향

- 개발 도상 지역에서의 숙련 마취과 의사의 부족

- 네트워크화된 마취 워크스테이션에서 사이버 보안 위험

- 비만 환자에 있어서 정밀도의 한계가 채용 제한

- 밸류체인 및 공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 제품별

- 기본 마취 모니터

- 통합 마취 워크스테이션

- 고급 마취 모니터

- 소모품 및 액세서리

- 감시 파라미터별

- 산소화(SpO2)

- 환기(EtCO2)

- 순환(혈압/심전도)

- 신경근전달(EMG/TOF)

- 뇌 활동(EEG/BIS)

- 최종 사용자별

- 병원

- 외래수술센터(ASC)

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Medtronic PLC

- GE HealthCare Technologies Inc.

- Koninklijke Philips NV

- Dragerwerk AG & Co. KGaA

- Masimo Corporation

- Nihon Kohden Corporation

- Mindray Bio-Medical Electronics Co., Ltd.

- Smiths Group plc(Smiths Medical)

- B. Braun Melsungen AG

- Getinge AB

- Infinium Medical Inc.

- Schiller AG

- Fukuda Denshi Co., Ltd.

- Shenzhen Comen Medical Instruments Co., Ltd.

- Criticare Systems Inc.

- Spacelabs Healthcare Inc.

- EIZO Corporation

- Heyer Medical AG

- SternMed GmbH

- RWD Life Science Co., Ltd.

- Axcent Medical GmbH

제7장 시장 기회 및 향후 전망

AJY 25.11.05The anesthesia monitoring devices market is valued at USD 2.91 billion in 2025 and is forecast to reach USD 4.68 billion by 2030, advancing at a 10.01% CAGR.

Growth rests on higher surgical volumes, artificial-intelligence-enabled predictive analytics, and an aging population that requires deeper perioperative vigilance. Integrated workstations remain the backbone of the anesthesia monitoring devices market because they blend ventilation, gas delivery, and multi-parameter tracking in one footprint, streamlining operating-room workflows. At the same time, AI-enhanced advanced monitors are pulling demand toward specialized applications such as brain activity and nociception tracking, signalling a shift from reactive to anticipatory care. Outpatient migration is another catalyst; portable systems that meet hospital-grade accuracy standards are critical as procedures move to ambulatory surgery centers (ASCs). Regionally, North America supplies stability through reimbursement and early technology uptake, but Asia-Pacific is the fastest-growing zone thanks to policy-backed localization drives that cut import dependency.

Global Anesthesia Monitoring Devices Market Trends and Insights

Development in Anesthesia Technology & Automated Record-keeping

Automated anesthesia information management systems (AIMS) slash manual charting errors by 40%, freeing clinicians to focus on patient care . Philips' IntelliSpace Critical Care and Anesthesia illustrates this trend with touch-optimized dashboards that feed real-time vitals directly into electronic health records . Closed-loop controllers already outmatch manual titration for hemodynamic stability, setting the stage for precision protocols driven by historical machine-learning feedback . Such gains meet a dual objective: higher safety margins and lower clinician burnout tied to administrative load. As a result, hospitals treat integrated AIMS as the core of a data-rich anesthesia monitoring devices market strategy.

Increasing Demand for Pain-free Surgeries

Patient expectations around rapid, opioid-sparing recovery are fueling multimodal techniques that hinge on objective nociception metrics. The NOL Index(R) finger probe converts four photoplethysmography channels into a 0-100 pain score, assisting anesthesiologists in tailoring analgesia . Validation studies confirm uniform accuracy across racial groups because infrared wavelengths and personalized algorithms normalize individual responses, answering equity concerns in perioperative care. In ASCs, where same-day discharge is the norm, NOL monitoring dovetails with ERAS pathways to curb respiratory depression and hasten mobilization. Consequently, pain-free protocols bolster the anesthesia monitoring devices market as facilities invest in sensors that align with patient-centric outcomes.

High Capital Cost & Preference for Conventional Techniques

Economic assessments show BIS monitoring costs USD 10,000-25,000 per avoided recall event, potentially adding USD 1 billion in annual spend if universally adopted. TIVA also presents higher variable expenses than low-flow inhalational strategies, leading resource-constrained systems to favor legacy monitors. Budget pressures, training overhead, and regulatory inertia slow advanced-device uptake, placing a drag on the anesthesia monitoring devices market where basic monitors suffice for routine cases.

Other drivers and restraints analyzed in the detailed report include:

- Rising Surgical Volumes from Aging Population

- AI-driven Predictive Analytics for Intra-operative Monitoring

- Shortage of Skilled Anesthesiologists in Developing Regions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Integrated workstations dominated with 41.34% share of the anesthesia monitoring devices market in 2024 as hospitals demanded single-console solutions that house gas delivery, ventilators, and monitors. Advanced monitors, though smaller in installed base, expand 10.78% CAGR by 2030, leveraging AI modules for brain and pain metrics that retrofit onto existing theaters. Basic monitors and consumables sustain the lower-cost layer, particularly in emerging markets and as redundancy backups. GE Healthcare's Aisys(TM) CS2 automates fresh-gas delivery, illustrating how workstation platforms integrate sustainability and cost savings, making them indispensable anchors within the anesthesia monitoring devices market.

Consumables show steady growth tied to procedure counts rather than capital cycles. Cyber-security is shaping purchase criteria; unified workstations reduce attack surfaces compared with disparate single-parameter devices. Consequently, procurement teams increasingly assess cyber-resilience alongside clinical performance, further buttressing integrated solutions' appeal in the anesthesia monitoring devices industry.

The Anesthesia Monitoring Devices Market Report Segments the Industry Into by Product (Basic Anesthesia Monitor, Integrated Anesthesia Workstation, and More), Parameter Monitored (Oxygenation, Ventilation, Circulation, and More), by End User (Hospitals, Ambulatory Surgery Centers, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 38.68% revenue for the anesthesia monitoring devices market in 2024 on the back of early AI adoption, reimbursement coverage, and a consolidated supplier base. Regulatory clarity and cybersecurity guidance from agencies such as CISA speed procurement decisions, while major vendors leverage domestic manufacturing footprints to navigate supply-chain shocks.

Asia-Pacific leads with a 10.86% CAGR through 2030 as China and India escalate localization. China's device market is slated to climb from USD 36.35 billion in 2024 to USD 55.67 billion by 2029, supported by Made in China 2025 incentives that cut import reliance from 85% toward sub-50% thresholds. India restricts refurbished imports and aims for a USD 50 billion MedTech sector by 2030, opening avenues for indigenous anesthesia monitoring platforms. These moves enlarge the anesthesia monitoring devices market size across regional OEMs and global joint-venture partners.

Europe maintains mid-single-digit growth under the EU Medical Device Regulation, which nudges suppliers toward eco-design and post-market surveillance that strengthen buyer confidence. Middle East and Africa attract hospital-build projects tied to medical tourism corridors in the Gulf, spawning demand for integrated workstations with multilingual user interfaces. South America shows pockets of acceleration in Brazil and Argentina as public hospitals modernize, yet currency volatility keeps procurement cycles uneven. Altogether, geographic diversification cushions the anesthesia monitoring devices market against region-specific shocks and sustains double-digit global expansion.

- Medtronic

- GE HealthCare Technologies Inc.

- Koninklijke Philips

- Dragerwerk

- Masimo

- Nihon Kohden

- Mindray Bio-Medical Electronics Co., Ltd.

- Smiths Group plc (Smiths Medical)

- B. Braun

- Getinge

- Infinium Medical Inc.

- Schiller

- Fukuda Denshi Co., Ltd.

- Shenzhen Comen Medical Instruments Co., Ltd.

- Criticare Systems Inc.

- Spacelabs Healthcare

- EIZO Corporation

- Heyer Medical

- SternMed

- RWD Life Science Co., Ltd.

- Axcent Medical GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Development in Anesthesia Technology & Automated Record-keeping

- 4.2.2 Increasing Demand for Pain-free Surgeries

- 4.2.3 Rising Surgical Volumes from Aging Population

- 4.2.4 AI-driven Predictive Analytics for Intra-operative Monitoring

- 4.2.5 Opioid-sparing Protocols Driving Nociception Monitoring

- 4.2.6 Portable Monitors for Decentralized Ambulatory Settings

- 4.3 Market Restraints

- 4.3.1 High Capital Cost & Preference for Conventional Techniques

- 4.3.2 Shortage of Skilled Anesthesiologists in Developing Regions

- 4.3.3 Cyber-security Risks in Networked Anesthesia Workstations

- 4.3.4 Accuracy Limitations in Obese Patients Discouraging Adoption

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Basic Anesthesia Monitor

- 5.1.2 Integrated Anesthesia Workstation

- 5.1.3 Advanced Anesthesia Monitor

- 5.1.4 Consumables & Accessories

- 5.2 By Parameter Monitored

- 5.2.1 Oxygenation (SpO2)

- 5.2.2 Ventilation (EtCO2)

- 5.2.3 Circulation (BP/ECG)

- 5.2.4 Neuromuscular Transmission (EMG/TOF)

- 5.2.5 Brain Activity (EEG/BIS)

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgery Centers

- 5.3.3 Others

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Medtronic PLC

- 6.3.2 GE HealthCare Technologies Inc.

- 6.3.3 Koninklijke Philips NV

- 6.3.4 Dragerwerk AG & Co. KGaA

- 6.3.5 Masimo Corporation

- 6.3.6 Nihon Kohden Corporation

- 6.3.7 Mindray Bio-Medical Electronics Co., Ltd.

- 6.3.8 Smiths Group plc (Smiths Medical)

- 6.3.9 B. Braun Melsungen AG

- 6.3.10 Getinge AB

- 6.3.11 Infinium Medical Inc.

- 6.3.12 Schiller AG

- 6.3.13 Fukuda Denshi Co., Ltd.

- 6.3.14 Shenzhen Comen Medical Instruments Co., Ltd.

- 6.3.15 Criticare Systems Inc.

- 6.3.16 Spacelabs Healthcare Inc.

- 6.3.17 EIZO Corporation

- 6.3.18 Heyer Medical AG

- 6.3.19 SternMed GmbH

- 6.3.20 RWD Life Science Co., Ltd.

- 6.3.21 Axcent Medical GmbH

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment