|

시장보고서

상품코드

1850118

마케팅 자동화 소프트웨어 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Marketing Automation Software Market - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

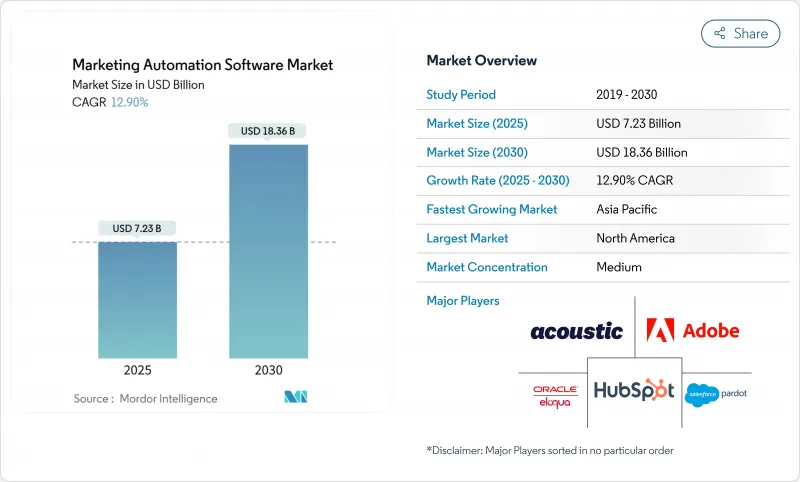

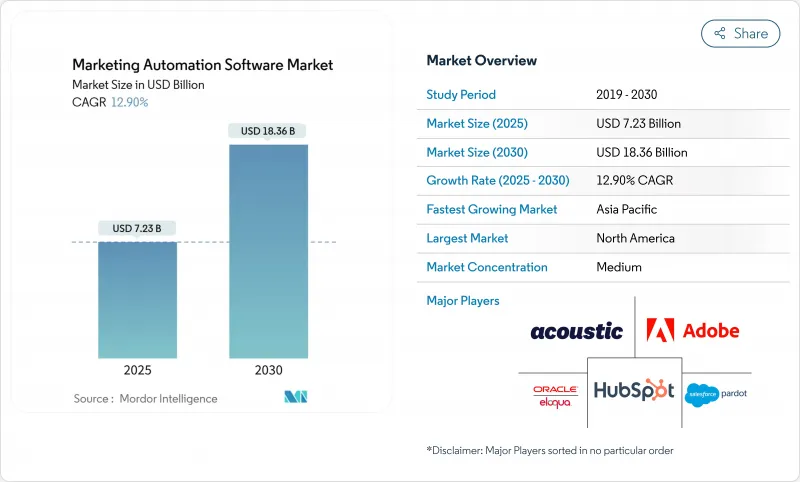

마케팅 자동화 소프트웨어 세계 시장 규모는 2025년에 72억 3,000만 달러, 2030년에는 183억 6,000만 달러에 이르고 CAGR은 12.9%를 나타낼 전망입니다.

이 성장은 기존 CRM 시스템에 연결하고 채널을 통해 실시간 캠페인을 오케스트레이션하는 AI 기반 참여 허브로 빠르게 전환하는 기업의 모습을 반영합니다. 진화하는 일반 AI는 사본을 만들고, 쿠폰을 선택하고, 밀리초 단위로 배달 시간을 설정할 수 있게 되었으며, 브랜드는 인원을 늘리지 않고 'One to One' 메시징을 확장할 수 있습니다. 또한 개인정보보호 규정이 강화되어 기업은 동의 추적 및 데이터 리니지를 자동화할 필요가 있습니다. 반면 중견 시장의 구매자는 자본 지출을 피하기 위해 클라우드 구독 모델을 활용하여 사용자 기반을 확대하고 마케팅 자동화 소프트웨어 시장의 모든 지역에서 공급업체 경쟁을 격화시키고 있습니다.

세계 마케팅 자동화 소프트웨어 시장 동향과 통찰

신흥아시아에서 SMB 퍼스트 클라우드 도입 급증

아시아태평양의 중소기업은 현재 연간 매출의 3-5%를 디지털 업그레이드에 충당하고 있으며, 클라우드 네이티브 마케팅 스택을 성장 계획에 필수적인 것으로 자리잡고 있습니다. 각 지역의 정책 입안자가 'AI 기본법'을 기초하고 직원의 스킬 업에 자금을 제공함으로써 컴플라이언스 리스크를 저감하고 신입 사원 입사시의 마찰을 경감합니다. 스마트 팩토리 시스템에 대한 제조업 지출은 2024년에 48% 증가하여 업스트림 생산 데이터와 동기화되는 고객을 위한 자동화에 대한 파급 수요가 탄생했습니다. 이러한 순풍은 고성장 아시아 경제 전반에 걸쳐 마케팅 자동화 소프트웨어 시장을 공동으로 끌어올립니다.

캠페인 ROI를 높이는 AI를 활용한 하이퍼 개인화

일반 AI는 고객별 메시징을 제한한 컨텐츠의 병목 현상을 해결합니다. 조기 도입 기업은 이미 캠페인 개시 사이클을 단축하고, 의도를 예측하고 자산을 자동 생성하는 예측 모델에 예산을 돌리고 있으며, 이 능력은 세계적인 AI 특허의 급증(전년대비 62.7% 증가)에 지지되고 있습니다. 벤더는 대규모 언어 모델의 코파일럿을 핵심 플랫폼에 번들하여 사용을 가속화하고 개방률, 전환율 및 수명 가치를 측정할 수 있는 증가를 제공합니다.

중공업 제조에서 멀티 벤더 MarTech 스택의 통합 오버 헤드

공장 운영자는 오랜 로터 사이클과 맞춤형 데이터 모델을 갖춘 레거시 ERP 및 현장 시스템을 운영하므로 최신 참여 도구를 통합하려면 대규모 인터페이스 작업이 필요합니다. 통합 프로젝트는 그린필드의 도입과 비교하여 예산이 최대 60% 팽창하기 때문에 Time-to-Value가 길어져 비용에 민감한 제조업 바이어의 의욕을 깎고 있습니다.

부문 분석

2024년 매출은 소프트웨어가 69.2%를 차지하고 마케팅 자동화 소프트웨어 시장에 진입하는 티켓 역할을 명확히 했습니다. 그러나 AI 모듈, 데이터 클린룸, 옴니채널 허브가 보급됨에 따라 통합, 최적화 및 거버넌스를 위해 전문 파트너와 계약하는 기업이 늘고 있습니다. 그 결과 서비스 CAGR은 14.0를 나타내고, 제품을 능가하며 2030년까지 마케팅 자동화 소프트웨어 시장 규모의 더 큰 부분을 획득할 것으로 예측됩니다.

라이선스 중심 거래에서 성과 중심 프로그램으로의 전환을 반영하여 컨설팅 팀은 현재 전체 프로젝트 비용의 30-40%를 흡수하고 있습니다. 2025년도 2분기 Oracle의 클라우드 서비스 매출액 59억 달러는 플랫폼 도입에 따른 판매 후 가치 창출의 규모를 보여줍니다.

클라우드 구독은 2024년 지출액의 66.3%를 차지하며 CIO가 탄력성, 자동 패치 적용, 신속한 AI 기능 추가를 평가하기 때문에 CAGR 13.9%로 성장할 것으로 예측됩니다. 따라서 클라우드 서비스와 관련된 마케팅 자동화 소프트웨어 시장 규모는 분기별로 확대되고 있습니다. 그럼에도 불구하고 은행, 통신 사업자, 공공기관은 여전히 기밀 데이터 세트를 On-Premise에 두고 있기 때문에 PII 이외의 워크로드를 퍼블릭 클라우드로 마이그레이션하는 한편, 핵심인 대장을 프라이빗 인프라에 고정하는 하이브리드 모델이 대두하고 있습니다. Microsoft의 2024년 클라우드 매출은 1,374억 달러로, 참여 스위트를 강화하는 확장 가능한 백엔드에 대한 수요가 정착되어 있다는 증거입니다.

마케팅 자동화 소프트웨어 시장은 구성 요소별(소프트웨어, 서비스), 배포별(클라우드 기반, On-Premise), 조직 규모별(대기업, 중소기업), 용도별(캠페인 관리, 메일 마케팅 등), 최종 사용자 가상별(은행, 금융서비스 및 보험(BFSI), 소매, 전자상거래 등), 지역별로 분류됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

지역별 분석

북미는 성숙한 클라우드 인프라, 활발한 벤처 자금 조달 장면, 포춘 500개 마케팅 담당자들 사이에서 이른 무버의 우위성 등에 힘입어 2024년 매출의 37.5%를 차지했습니다. 2025년에 시행되는 주 수준의 개인정보보호법이 동의 오케스트레이션을 포함한 플랫폼의 채택을 가속시키고 자동화를 억제하는 것보다 오히려 정착시킵니다. 기타 혜택으로 이 지역에는 구현 주기를 단축하는 파트너 생태계가 충실합니다.

아시아태평양은 가장 빠르게 성장하고 있으며 연간 15.8%로 확대되고 있습니다. 이는 클라우드가 적당한 가격으로 이용할 수 있게 된 것과 디지털 네이티브 중소기업 인구가 증가한 것 때문입니다. 한국의 AI세액 공제나 반도체 수출 프로그램 등 정부 우대조치는 인프라에 두께를 갖게 하고 실시간 개인화 워크로드의 대기 시간을 저하시킵니다. 중국의 13억 명의 WeChat 사용자는 임베디드 미니 앱의 자동화에 대응할 수 있는 사용자를 늘리고 레거시 채널에 비해 플랫폼 성장률을 높입니다.

유럽, 남미, 중동 및 아프리카는 모두 다양한 비즈니스 기회의 기반을 형성하고 있습니다. EU에서는 GDPR(EU 개인정보보호규정)의 영향으로 컴플라이언스 기능이 가장 중요한 과제가 되고 있지만 마케팅 업무의 인력 부족이 본격적인 전개를 저해하고 있습니다. 라틴아메리카 기업은 On-Premise에서 클라우드 스위트로 이동하고 걸프 지역의 은행은 은행 계좌가 없는 계층에 접근하기 위해 AI 채팅 주도의 온보딩을 시험적으로 도입하고 있습니다. 이러한 추세를 종합하면 거시적 환경이 이질적임에도 불구하고 마케팅 자동화 소프트웨어 시장은 수익이 증가할 것으로 예측됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 신흥 아시아 국가에서 중소기업용 클라우드 도입 급증

- AI를 활용한 하이퍼 퍼스널라이제이션으로 캠페인의 ROI를 향상

- 컴포저블 CDP와 CRM 스위트의 통합

- BFSI에서의 컴플라이언스 주도의 옴니 채널 전개

- 중국 본토의 WeChat 미니 앱 자동화 도입 붐

- 시장 성장 억제요인

- 중공업 제조업에서 멀티 벤더 MarTech 스택 통합의 오버 헤드

- EMEA 전역의 마케팅 오퍼레이션에서 중견기업의 인력 부족

- SaaS 구독 피로가 중소기업의 툴 이탈률을 상승시킨다

- 밸류체인 분석

- 기술의 전망

- 업계 생태계 분석

- 디지털 전환과 CRM 컨버전스의 영향

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측(가치관)

- 구성요소별

- 소프트웨어

- 서비스

- 전개별

- 클라우드 기반

- On-Premise

- 조직 규모별

- 대기업

- 중소기업

- 용도별

- 캠페인 관리

- 메일 마케팅

- 리드 관리

- 분석 및 보고서

- 소셜 미디어 마케팅

- 모바일 마케팅

- 인바운드 마케팅

- 판매 활성화

- 기타 용도

- 최종 사용자별

- BFSI

- 소매업 및 전자상거래

- IT 및 통신

- 헬스케어

- 제조업

- 미디어 및 엔터테인먼트

- 정부

- 교육

- 기타 최종 사용자 분야

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 싱가포르

- 인도네시아

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 칠레

- 기타 남미

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 이스라엘

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- Vendor Positioning Analysis

- 기업 프로파일

- HubSpot, Inc.

- Adobe Systems Inc.

- Oracle Corporation(Eloqua)

- Acoustic LP

- Salesforce Inc.(Pardot and Marketing Cloud)

- Microsoft Corporation

- IBM Corporation

- ActiveCampaign LLC

- Klaviyo Inc.

- Act-On Software

- SAP SE

- SugarCRM Inc.(Salesfusion)

- Zoho Corp.(Zoho Marketing Autom.)

- Mailchimp(Intuit)

- Keap

- Omnisend

- Thryv Holdings

- Drip

- Oracle NetSuite

- Braze Inc.

제7장 시장 기회와 장래의 전망

SHW 25.11.07The global marketing automation software market size stands at USD 7.23 billion in 2025 and is on track to reach USD 18.36 billion by 2030, reflecting a solid 12.9% CAGR.

This growth mirrors enterprises' rapid pivot toward AI-driven engagement hubs that bolt onto existing CRM systems and orchestrate real-time campaigns across channels. Advancing generative AI now writes copy, selects offers and times delivery in milliseconds, letting brands scale "one-to-one" messaging without ballooning headcount. Demand also rises as privacy regulations tighten, pushing firms to automate consent tracking and data lineage. Meanwhile, mid-market buyers rely on cloud subscription models to bypass capital outlays, widening the user base and intensifying vendor competition in every region of the marketing automation software market.

Global Marketing Automation Software Market Trends and Insights

SMB-first cloud adoption surge across emerging Asia

Small and medium enterprises in Asia-Pacific now devote 3-5% of annual revenue to digital upgrades, positioning cloud-native marketing stacks as an essential plank of growth plans. Regional policymakers draft "AI Basic Laws" and fund workforce skilling, lowering compliance risk and reducing onboarding friction for newcomers. Manufacturing outlays on smart-factory systems rose 48% in 2024, creating spill-over demand for customer-facing automation that syncs with upstream production data. These tailwinds jointly lift the marketing automation software market across high-growth Asian economies.

AI-powered hyper-personalization boosting campaign ROI

Generative AI removes the content bottleneck that once limited customer-specific messaging. Early adopters already compress campaign launch cycles and re-route budgets toward predictive models that anticipate intent and auto-generate assets, a capability underpinned by soaring global AI patent activity (+62.7% YoY). Vendors bundle large-language-model co-pilots into core platforms, accelerating usage and adding measurable lift in open rates, conversions and lifetime value.

Multi-vendor MarTech stack integration overheads in heavy-industry manufacturing

Plant operators run legacy ERP and shop-floor systems with long rotor cycles and bespoke data models, so layering in modern engagement tools demands extensive interface work. Integration projects inflate budgets by up to 60% versus green-field deployments, lengthening time-to-value and dampening appetite among cost-sensitive manufacturing buyers.

Other drivers and restraints analyzed in the detailed report include:

- Integration of composable CDPs with CRM suites

- Compliance-led omnichannel expansion in BFSI

- Mid-market talent shortage in marketing ops across EMEA

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software retained 69.2% revenue in 2024, underscoring its role as the entry ticket to the marketing automation software market. Yet as AI modules, data-clean rooms and omnichannel hubs proliferate, enterprises increasingly contract specialized partners for integration, optimization and governance. Consequently, services are forecast to clock a 14.0% CAGR, outpacing product, and capturing a larger slice of the marketing automation software market size by 2030.

Consulting teams now absorb 30-40% of total project spend, reflecting the move from license-centric deals to outcome-centric programs. Oracle's cloud services revenue of USD 5.9 billion in Q2 FY2025 illustrates the scale of post-sale value creation that accompanies platform uptake.

Cloud subscriptions held 66.3% of 2024 spend and will advance at 13.9% CAGR as CIOs prize elasticity, auto-patching and rapid AI feature drops. The marketing automation software market size linked to cloud offerings therefore widens each quarter. Nevertheless, banks, telcos and public bodies still keep sensitive datasets on-premise, giving rise to hybrid models that shuttle non-PII workloads to public clouds while anchoring core ledgers on private infrastructure. Microsoft tallied USD 137.4 billion in cloud revenue in 2024, evidence of entrenched demand for scalable back-ends that power engagement suites.

Marketing Automation Software Market is Segmented by Component (Software, Services), Deployment (Cloud-Based, On-Premises), Organization Size (Large Enterprises, Smes), Application (Campaign Management, Email Marketing, and More), End-User Vertical (BFSI, Retail and E-Commerce, and More), by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America contributed 37.5% of 2024 revenue, sustained by mature cloud infrastructure, an active venture funding scene and early-mover advantage among Fortune 500 marketers. Sweeping state-level privacy acts effective in 2025 accelerate adoption of platforms with in-built consent orchestration, further entrenching automation rather than curtailing it. The region additionally benefits from dense partner ecosystems that shorten implementation cycles.

Asia-Pacific is the fastest-growing territory, expanding 15.8% per year as cloud affordability intersects with large digitally native SME populations. Government incentives, such as Korea's AI tax credits and semiconductor export programs, add infrastructure depth and lower latency for real-time personalization workloads. China's 1.3 billion WeChat users amplify the addressable audience for embedded mini-app automation, translating into outsized platform growth relative to legacy channels.

Europe, South America, the Middle East and Africa together form a diversified opportunity base. In the EU, GDPR heritage keeps compliance features top-of-mind, yet a shortage of marketing operations talent inhibits full-scale rollouts. Latin American firms leapfrog on-premise by moving straight to cloud suites, while Gulf-region banks pilot AI chat-led onboarding to reach unbanked segments. Collectively, these trends channel incremental revenue into the marketing automation software market despite heterogeneous macro conditions.

- HubSpot, Inc.

- Adobe Systems Inc.

- Oracle Corporation (Eloqua)

- Acoustic L.P.

- Salesforce Inc. (Pardot and Marketing Cloud)

- Microsoft Corporation

- IBM Corporation

- ActiveCampaign LLC

- Klaviyo Inc.

- Act-On Software

- SAP SE

- SugarCRM Inc. (Salesfusion)

- Zoho Corp. (Zoho Marketing Autom.)

- Mailchimp (Intuit)

- Keap

- Omnisend

- Thryv Holdings

- Drip

- Oracle NetSuite

- Braze Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increase in SMB-first Cloud Adoption Surge Across Emerging Asia

- 4.2.2 AI-Powered Hyper-Personalization Boosting Campaign ROI

- 4.2.3 Integration of Composable CDPs with CRM Suites

- 4.2.4 Compliance-Led Omnichannel Expansion in BFSI

- 4.2.5 Adoption of WeChat Mini-App Automation Boom in Mainland China

- 4.3 Market Restraints

- 4.3.1 Multi-Vendor MarTech Stack Integration Overheads in Heavy-Industry Manufacturing

- 4.3.2 Mid-Market Talent Shortage in Marketing Ops Across EMEA

- 4.3.3 SaaS Subscription Fatigue Driving Higher Tool Churn in SMBs

- 4.4 Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Industry Ecosystem Analysis

- 4.7 Impact of Digital-Transformation Shift and CRM Convergence

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 Cloud-based

- 5.2.2 On-Premise

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By Application

- 5.4.1 Campaign Management

- 5.4.2 Email Marketing

- 5.4.3 Lead Management

- 5.4.4 Analytics and Reporting

- 5.4.5 Social Media Marketing

- 5.4.6 Mobile Marketing

- 5.4.7 Inbound Marketing

- 5.4.8 Sales Enablement

- 5.4.9 Other Applications

- 5.5 By End-user Vertical

- 5.5.1 BFSI

- 5.5.2 Retail and E-commerce

- 5.5.3 IT and Telecom

- 5.5.4 Healthcare

- 5.5.5 Manufacturing

- 5.5.6 Media and Entertainment

- 5.5.7 Government

- 5.5.8 Education

- 5.5.9 Other End-user Verticals

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Nordics

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Singapore

- 5.6.3.6 Indonesia

- 5.6.3.7 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Chile

- 5.6.4.4 Rest of South America

- 5.6.5 Middle East

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.5.4 Israel

- 5.6.5.5 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Egypt

- 5.6.6.3 Nigeria

- 5.6.6.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Vendor Positioning Analysis

- 6.5 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.5.1 HubSpot, Inc.

- 6.5.2 Adobe Systems Inc.

- 6.5.3 Oracle Corporation (Eloqua)

- 6.5.4 Acoustic L.P.

- 6.5.5 Salesforce Inc. (Pardot and Marketing Cloud)

- 6.5.6 Microsoft Corporation

- 6.5.7 IBM Corporation

- 6.5.8 ActiveCampaign LLC

- 6.5.9 Klaviyo Inc.

- 6.5.10 Act-On Software

- 6.5.11 SAP SE

- 6.5.12 SugarCRM Inc. (Salesfusion)

- 6.5.13 Zoho Corp. (Zoho Marketing Autom.)

- 6.5.14 Mailchimp (Intuit)

- 6.5.15 Keap

- 6.5.16 Omnisend

- 6.5.17 Thryv Holdings

- 6.5.18 Drip

- 6.5.19 Oracle NetSuite

- 6.5.20 Braze Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment