|

시장보고서

상품코드

1850136

비료 첨가제 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Fertilizer Additives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

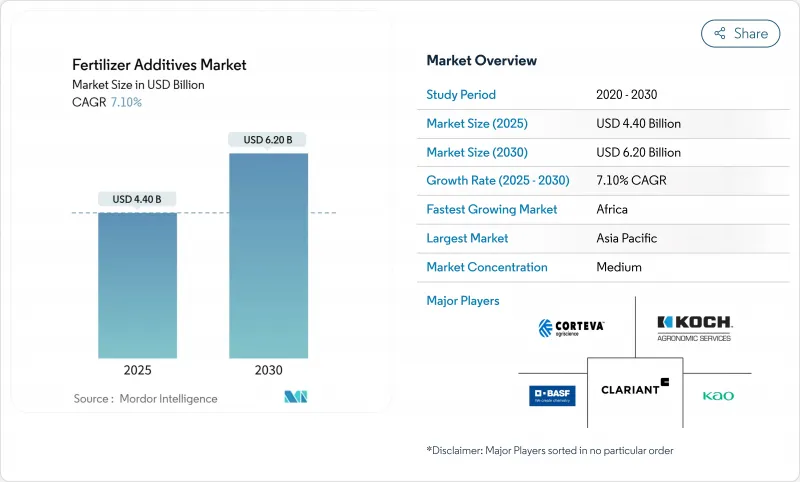

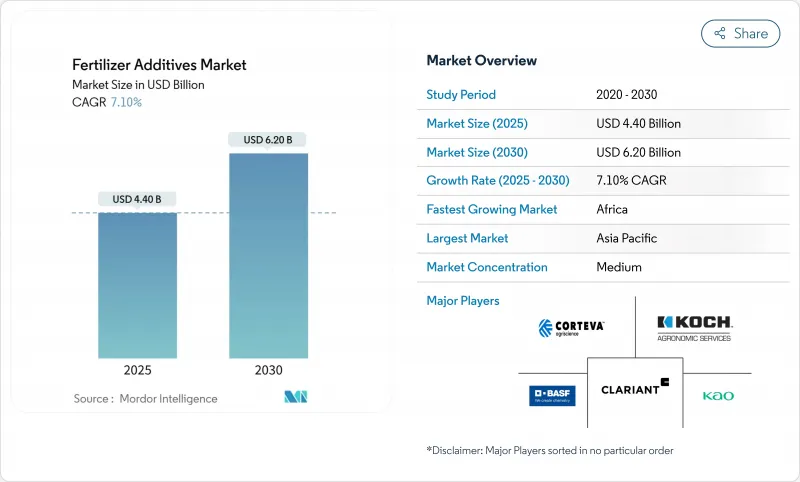

비료 첨가제 시장은 2025년에는 44억 달러, 2030년에는 62억 달러에 이르고, 예측 기간 동안 7.10%의 연평균 복합 성장률(CAGR)로 성장할 것으로 예상됩니다.

성장은 더욱 엄격해진 영양소 사용 규정, 정밀 농업의 급증, 투입 비용의 상승 등이 있어, 생산자는 질소나 인산의 시용 단위를 보호하는 첨가제를 요구하게 됩니다. 효율성 향상 제품은 현재 미국의 옥수수 재배 면적의 37% 를 차지하는 가변 비율 기술과 결합되어 경작지와 관개 시설 모두에 미세 주입 정확도를 제공합니다. 두 지역 모두 플랜트 게이트에서 플랜터 박스까지 유동성을 유지하기 위해 고결 방지제와 코팅제에 의존합니다. 그린 암모니아 프로젝트가 증가하고 -33℃의 저장 온도에서도 활성을 유지하는 약제가 요구되는 가운데, 수요는 저온 암모니아 물류 주변에도 형성되고 있습니다. 공급업체 간의 집중은 완만하며, 생물학적 안정제, 바이오폴리머 코팅, 디지털 투여 지원을 하나의 성능 패키지로 정리한 혁신적인 공급업체가 활약할 여지가 있습니다.

세계 비료 첨가제 시장 동향과 통찰

집약형 농업 지역에서 비료 소비 증가

곡물 수요의 급증은 이미 최대 강도로 경작하고 있는 지역의 첨가제량을 증가시킵니다. OECD-FAO Outlook은 세계 곡물 수요가 2032년까지 31억 톤에 이를 것으로 보이며, 대부분 아시아와 아프리카에서 온 것입니다. 첨가제는 습도가 높은 관개 시스템에서 증가하는 양분 손실을 방지하고 500만 에이커 이상의 농지가 관개 중 휘발을 줄이는 강화된 제형으로 가동되고 있는 worldfertilizer.com. 물방울이나 피벗 시스템을 사용하는 생산자는 90% 가까운 양분 사용 효율을 달성하고 고습도 하에서도 혼합액의 유동성을 유지하는 고결방지제 및 코팅제의 추가 보급을 추진하고 있습니다. 식품 안보를 향한 자본 유입은 첨가물 공급업체에게 예측 가능한 장기 수요 곡선을 생성합니다.

효율성 향상 비료(EEF) 수요

198억 달러의 부가가치 비료는 바이오 자극제, 억제제 및 방출 제어 코팅제를 타이밍과 작물에 맞게 단일 과립에 통합한 것입니다. NBPT와 같은 우레아제 억제제는 Duromide 안정제와 결합하여 암모니아 손실을 54% 줄이고 생산자가 여분의 경로 없이 고단백질 곡물을 얻을 수 있도록 도와줍니다. 미국 바이오스티뮬란트의 매출은 2026년까지 3배의 12억 달러가 되어 기존의 영양 프로그램에 생물학적 제제가 포함됩니다. 고분자 코팅 된 방출 제어 약물은 전달 창을 더욱 강화하고 비료 첨가제 시장을 공급과 뿌리 수요를 동기화하는 보다 스마트한 다층 필름으로 향하게합니다.

작물 투입 자재의 비용 상승

2025년 초 비료가격은 11% 상승하여 곡물가격이 침체하는 가운데 농가의 이폭을 압박했습니다. UAN28의 출하 가격은 톤당 354달러, DAP는 765달러, MAP는 810달러에 이르렀고, 자금을 벌이는 생산자에게는 프리미엄 첨가제 판매가 어려워졌습니다. 실험실 은행의 가용성 지수는 특히 질소와 인산의 범주에서 이미 농가 지출의 대부분을 차지하는 수요 파괴 위험을 시사합니다. 아프리카와 남아시아의 소규모 농부들은 가장 엄격한 트레이드오프에 직면하고 있으며, 투자 회수가 입증되었음에도 불구하고 효율성 향상을 위해 구매를 연기하는 경우가 많습니다.

부문 분석

2024년 비료 첨가제 시장에서는 고결방지제가 매출의 37%를 차지하며 가장 큰 비율을 차지했습니다. 이 이점은 습도가 높은 선적 시즌이나 창고에서 긴 대기 시간 동안 입자 흐름을 유지하기 위해 이 물질이 중요한 역할을 하기 때문입니다. 지방 아민 블렌드와 환원 계면활성제 시스템은 현재 철도 차량 내 압축을 견디는 더 얇고 유연한 필름을 만들어 초기 바이오 왁스를 능가하고 있습니다. 그러나 코팅제는 CAGR 9.8%로 성장의 왕관을 쓰고, 45일부터 90일의 스팬으로 방출되는 폴리머와 바이오폴리머 필름에 밀려나가고 있습니다. 이 2대 지도자는 신뢰성과 영양 타이밍이 구매 결정을 좌우하는 방법을 보여줍니다.

두 번째 범주도 진화하고 있습니다. 억제제는 아산화질소의 억제라는 규제의 요구에 부응하고, 조립 보조제는 엄격한 입자 공차를 요구하는 정밀 도포기의 전환을 획득하고 있습니다. 신흥의 하이브리드 제품은 고결방지제, 억제제, 코팅제의 기능을 단일 첨가제에 융합시킨 것으로, 혼입률을 삭감하고 공급 체인을 간소화합니다. 부식 방지제가 액체 비료에 사용되는 반면, 작업자의 노출 기준이 엄격한 지역에서는 제청제가 기세를 늘리고 있습니다. 비료 첨가제 시장은 단일 투여로 여러 어려움을 해결할 수 있는 다목적 화학물질에 계속 끌려가고 있습니다.

미립자 영양제는 활석 기반 컨디셔너, 왁스, 지방 아민 파우더 판매의 68%를 차지하고 안정적인 현금 흐름을 생산합니다. 벌크 터미널과 바지 연산자는 고형 고결 방지제에 의지하여 쌓기의 유동성을 유지합니다. 액제는 규모는 작은 것, CAGR 8.4%로 성장을 지속하고, 있으며, 관개 면적 증가와 드론 스프레이의 채용을 반영하고 있습니다. 액체 분산액은 너스 탱크에서 신속하게 용해되어 수율 맵에 맞는 가변 속도로 인라인 주입을 가능하게합니다.

마이크로캡슐은 이 두 극의 중간에 위치합니다. 활성 성분을 보호하고 방출을 지연시키고 폴리유산과 전분으로 만든 퇴비화 가능한 껍질로 다가오는 마이크로 플라스틱 규제를 충족시킵니다. 밀리켄의 마이크로 캡슐에 대한 노력은 차세대 배달 경로로의 자본 이동을 보여줍니다. 비료 첨가제 시장에서는 폼 팩터가 수렴하고 있습니다. 일부 공급업체는 현재 액체 시드 드레싱과 최고 드레스 패스용 컴패니언 드라이 코팅을 모두 포함하는 키트를 제공하고 있으며, 시즌을 통해 일관된 영양 제어를 보장합니다.

지역 분석

아시아 태평양 지역은 중국과 인도의 소규모 농장 덕분에 2024년 매출 39%를 기록하며 1위를 유지했습니다. 이 농장들은 약 30억 명의 인구에 서비스를 제공합니다. 중국이 인산염 수출을 일시적으로 제한함으로써 국내 첨가제 라인이 혜택을 받고 공급이 지역 채널로 재조합되어 수입 의존도가 떨어집니다. 인도의 화학 부문은 토양 실험실 및 농장 센서에 자금을 제공하는 디지털 농업 임무에 힘입어 2025년까지 500억 달러의 특수 매출을 달성하는 기세입니다. 비료 첨가제 시장 규모에서 국내 생산자는 통합 공급망을 활용하여 불안정한 운임 시장에도 불구하고 납품 비용을 낮게 유지하고 있습니다.

아프리카는 정부와 민간 자본이 새로운 생산 기지에 자금을 투입하고 있기 때문에 CAGR로 가장 빠른 10.5%를 나타냅니다. 나이지리아의 150만 톤 플랜트와 인드라마의 280만 톤 확장으로 견인되어 10년 후까지 영양염의 소비량은 760만 톤에서 1,360만 톤으로 급증할 것으로 보입니다. 서아프리카만으로도 2030년까지 460만 톤을 넘을 수 있습니다. 그러나 첨가제 공급업체는 흐름 컨디셔너를 농민 훈련과 함께 포장하고 수용 확대로 이어질 여지가 있다고 생각합니다.

북미와 유럽은 CAGR 5.2%와 4.5%로 성숙하면서도 혁신적인 성장을 보이고 있습니다. 영국 농장의 28%가 콩과 식물의 윤작을 이용하여 비료계획을 조정하고, 질소를 고정하여 화학합성농약의 살포를 억제하고 있습니다. EU의 탄소 국경 조정 메커니즘은 2026년에 도입되었으며, 비료 수입업체는 탄소 함량을 공개해야 합니다. 양 대륙에서는 생물학적 대체 비료가 점유율을 늘리고 있지만, 한랭지나 좁은 작제 기간에서도 그 성능 데이터가 안정되어 있기 때문에 화학 코팅제도 뿌리 깊은 인기를 자랑하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 고집약형 농업 지역에 있어서의 비료 소비량 증가

- 고효율 비료(EEF) 수요

- 영양소 이용 효율을 높이는 규제의 추진

- 마이크로 도징을 가능하게 하는 정밀 농업의 도입

- 새로운 코킹 방지 요구를 창출하는 극저온 저탄소 암모니아 물류

- 토양 미생물 친화적인 바이오 폴리머 코팅

- 시장 성장 억제요인

- 농작물의 투입 비용의 상승

- 첨가물에 관한 환경규제 강화

- 특수 계면활성제의 석유화학 원료의 휘발성

- 생물학적 대체품의 급속한 출현

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 기능별

- 억제제

- 코팅제

- 과립화 보조제

- 응집 방지제

- 제진제

- 부식 방지제

- 소포제

- 기타 틈새 기능

- 형태별

- 고체

- 액체

- 마이크로 캡슐화

- 용도별

- 우레아

- 질산암모늄

- 인산이암모늄(DAP)

- 인산일암모늄(MAP)

- 황산암모늄

- 트리플 수퍼인산(TSP)

- 포타시 혼합비료

- 기타 특수 비료

- 작물별

- 곡물

- 지방종자

- 과일 및 채소

- 잔디 및 관상용 식물

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 기타 북미

- 유럽

- 독일

- 프랑스

- 영국

- 스페인

- 이탈리아

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- BASF SE

- Corteva Agriscience

- Clariant International Ltd

- KAO Corporation

- Koch Agronomic Services

- Arkema(ArrMaz)

- Dorf Ketal Company LLC

- Michelman Inc.

- Novochem Group

- Lanxess AG

- Croda International Public Limited Company(Cargill, Incorporated)

- Hubei Forbon Technology Co., Ltd.

- Jiangsu Kolod Food Ingredients Co., Ltd.

- TIMAC AGRO INDIA PRIVATE LIMITED

- Nutrien Ltd.

- CF Industries

- The Mosaic Company

- Yara International

- ADM

- ICL Group

제7장 시장 기회와 장래의 전망

SHW 25.11.17The fertilizer additives market stood at USD 4.40 billion in 2025 and will advance to USD 6.20 billion by 2030, reflecting a steady 7.10% CAGR through the outlook period.

Growth rests on stricter nutrient-use rules, the surge of precision agriculture, and rising input costs that push growers toward additives that guard every unit of applied nitrogen or phosphate. Enhanced-efficiency products now pair with variable-rate technology, which already covers 37% of U.S. corn acres, bringing micro-dosing accuracy to fields and irrigation pivots alike. Asia-Pacific supplies the volume base, Africa supplies the pace, and both regions rely on anti-caking and coating chemistries to preserve flowability from the plant gate to the planter box. Demand is also forming around cryogenic ammonia logistics as green ammonia projects multiply, requiring agents that remain active at -33 °C storage temperatures. Moderate concentration among suppliers leaves room for innovators that combine biological stabilizers, biopolymer coatings, and digital dosing support into a single performance package.

Global Fertilizer Additives Market Trends and Insights

Rising Fertilizer Consumption in High-Intensity Farming Regions

Surging cereal demand lifts additive volumes in zones that already farm at maximum intensity. The OECD-FAO Outlook sees global cereals hitting 3.1 billion tons by 2032, most of it from Asia and Africa. Additives arrest nutrient losses that climb in humid, irrigated systems, and more than 5 million acres now run on enhanced formulations that cut volatilization during fertigation worldfertilizer.com. Growers using drip and pivot systems achieve nutrient-use efficiency near 90%, propelling further uptake of anti-caking and coating chemistries that keep blends free-flowing under high humidity. Capital inflows toward food security create predictable long-term demand curves for additive suppliers.

Demand for Enhanced-Efficiency Fertilizers (EEF)

Value-added fertilizers worth USD 19.8 billion merge biostimulants, inhibitors, and controlled-release coatings into single granules tailored for timing and crop phase. Urease inhibitors such as NBPT lower ammonia losses by 54% when matched with Duromide stabilizer, helping growers derive higher protein grain without extra passes. U.S. biostimulant sales will triple to USD 1.2 billion by 2026, embedding biologicals into conventional nutrient programs. Polymer-coated controlled-release variants further tighten delivery windows, nudging the fertilizer additives market toward smarter, multi-layer films that synchronize supply and root demand.

Rising Cost of Crop Inputs

Fertilizer prices rose 11% in early 2025, squeezing farm margins as grain prices lag. Delivered UAN28 reached USD 354 per ton, DAP USD 765, and MAP USD 810, making premium additives a harder sell for cash-strapped growers. Rabobank's affordability index signals demand destruction risk, especially in nitrogen and phosphate categories that already command the bulk of farm spend. Smallholders in Africa and South Asia face the harshest trade-offs, often deferring enhanced-efficiency purchases despite proven payback.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Push for Nutrient-Use Efficiency

- Cryogenic Low-Carbon Ammonia Logistics Creating New Anti-Caking Needs

- Tightening Environmental Regulations on Additives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Anti-caking products generated the largest slice of the fertilizer additives market in 2024, at 37% of revenue. This dominance stems from the material's vital role in preserving particle flow during humid shipping seasons and long warehouse layovers. Fatty amine blends and reduced-surfactant systems now outperform early bio-waxes by creating thinner, more flexible films that withstand compression in rail cars. Coating agents, however, wear the growth crown with a 9.8% CAGR, propelled by polymer and biopolymer films that meter release over 45- to 90-day spans. These twin leaders show how reliability and nutrient timing together move purchasing decisions.

Second-tier categories also evolve. Inhibitors answer regulatory calls to curb nitrous oxide, and granulation aids win converts in precision applicators that demand tight particle tolerances. Emerging hybrid products fuse anti-caking, inhibitor, and coating functions into single additives that cut inclusion rates and simplify supply chains. Corrosion prevention solutions enter liquid fertilizer service while dedusting agents gain momentum where worker exposure standards tighten. The fertilizer additives market continues to gravitate toward multi-purpose chemistries able to solve several pain points with one dose.

Granular nutrient blends keep solids on top, translating to 68% of revenues and steady cash flows for talc-based conditioners, waxes, and fatty amine powders. Bulk terminals and barge operators rely on solid anti-caking to keep piles free-flowing. Liquids, though smaller, are the climbers, logging an 8.4% CAGR that mirrors rising fertigation acres and drone spray adoption. Liquid dispersions dissolve quickly in nurse tanks, enabling inline injection at variable rates that match yield maps.

Micro-encapsulated formats sit between the two poles. They protect active ingredients, delay the release, and satisfy looming microplastic rules with compostable shells made from polylactic acid or starch. Milliken's push into microcapsules illustrates capital migration toward next-generation delivery routes. In the fertilizer additives market, form factors are converging; some suppliers now offer kits that include both liquid seed dressing and companion dry coating for top-dress passes, ensuring consistent nutrient control across the season.

The Fertilizer Additives Market Report is Segmented by Function (Inhibitors, Coating Agents, Granulation Aids, and More), Form (Solid, Liquid, and Micro-Encapsulated), Application (Urea, Ammonium Nitrate, Diammonium Phosphate (DAP), and More), Crop (Cereals and Grains, Oilseeds, and More) and Geography (North America, Europe, Asia-Pacific, and More). The Report Offers Market Forecasts in Terms of Value (USD).

Geography Analysis

Asia-Pacific retained the sales crown at 39% in 2024 thanks to dense small-plot farms in China and India that collectively serve nearly 3 billion people. Domestic additive lines benefit from China's temporary phosphate export limits, which reshuffle supply into local channels and dampen import reliance. India's chemicals sector is on track to touch USD 50 billion in specialty revenues by 2025, aided by the Digital Agriculture Mission that funds soil labs and on-farm sensors. Within the fertilizer additives market size, domestic producers leverage integrated supply chains to keep delivered costs low despite volatile freight markets.

Africa showcases the fastest 10.5% CAGR as governments and private capital pour funds into new production hubs. Consumption will jump from 7.6 million to 13.6 million tons of nutrients by decade's end, led by Nigeria's 1.5 million ton plant and Indorama's 2.8 million ton expansion. West Africa alone could exceed 4.6 million tons by 2030. Adoption still faces last-mile hurdles such as bagged product costs and rural financing gaps, but additive suppliers see room to package flow conditioners with farmer training to lift acceptance.

North America and Europe register mature yet innovative growth at 5.2% and 4.5% CAGR. Precision agriculture underpins most incremental demand; 28% of U.K. farms adjust fertilizer plans using legume rotations to fix nitrogen and curb synthetic application. The EU Carbon Border Adjustment Mechanism, coming in 2026, will require fertilizer importers to disclose embedded carbon, advantaging local low-emission formulations. Across both continents, biological alternatives gain a share, yet chemical coatings persist because their performance data remain robust under colder climates and tight planting windows.

- BASF SE

- Corteva Agriscience

- Clariant International Ltd

- KAO Corporation

- Koch Agronomic Services

- Arkema (ArrMaz)

- Dorf Ketal Company LLC

- Michelman Inc.

- Novochem Group

- Lanxess AG

- Croda International Public Limited Company (Cargill, Incorporated)

- Hubei Forbon Technology Co., Ltd.

- Jiangsu Kolod Food Ingredients Co., Ltd.

- TIMAC AGRO INDIA PRIVATE LIMITED

- Nutrien Ltd.

- CF Industries

- The Mosaic Company

- Yara International

- ADM

- ICL Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising fertilizer consumption in high-intensity farming regions

- 4.2.2 Demand for enhanced-efficiency fertilizers (EEF)

- 4.2.3 Regulatory push for nutrient-use efficiency

- 4.2.4 Precision-agriculture adoption enabling micro-dosing

- 4.2.5 Cryogenic low-carbon ammonia logistics creating new anti-caking needs

- 4.2.6 Soil-microbiome friendly biopolymer coatings

- 4.3 Market Restraints

- 4.3.1 Rising cost of crop inputs

- 4.3.2 Tightening environmental regulations on additives

- 4.3.3 Petrochemical feedstock volatility for specialty surfactants

- 4.3.4 Rapid emergence of biological substitutes

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Function

- 5.1.1 Inhibitors

- 5.1.2 Coating Agents

- 5.1.3 Granulation Aids

- 5.1.4 Anti-Caking Agents

- 5.1.5 Dedusting Agents

- 5.1.6 Corrosion Inhibitors

- 5.1.7 Anti-Foaming Agents

- 5.1.8 Other Niche Functions

- 5.2 By Form

- 5.2.1 Solid

- 5.2.2 Liquid

- 5.2.3 Micro-encapsulated

- 5.3 By Application

- 5.3.1 Urea

- 5.3.2 Ammonium Nitrate

- 5.3.3 Diammonium Phosphate (DAP)

- 5.3.4 Mono-Ammonium Phosphate (MAP)

- 5.3.5 Ammonium Sulfate

- 5.3.6 Triple Superphosphate (TSP)

- 5.3.7 Potash Blends

- 5.3.8 Other Specialty Fertilizers

- 5.4 By Crop

- 5.4.1 Cereals and Grains

- 5.4.2 Oilseeds

- 5.4.3 Fruits and Vegetables

- 5.4.4 Turf and Ornamentals

- 5.4.5 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 France

- 5.5.2.3 United Kingdom

- 5.5.2.4 Spain

- 5.5.2.5 Italy

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East

- 5.5.4.1 Saudi Arabia

- 5.5.4.2 United Arab Emirates

- 5.5.4.3 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Egypt

- 5.5.5.3 Rest of Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 BASF SE

- 6.4.2 Corteva Agriscience

- 6.4.3 Clariant International Ltd

- 6.4.4 KAO Corporation

- 6.4.5 Koch Agronomic Services

- 6.4.6 Arkema (ArrMaz)

- 6.4.7 Dorf Ketal Company LLC

- 6.4.8 Michelman Inc.

- 6.4.9 Novochem Group

- 6.4.10 Lanxess AG

- 6.4.11 Croda International Public Limited Company (Cargill, Incorporated)

- 6.4.12 Hubei Forbon Technology Co., Ltd.

- 6.4.13 Jiangsu Kolod Food Ingredients Co., Ltd.

- 6.4.14 TIMAC AGRO INDIA PRIVATE LIMITED

- 6.4.15 Nutrien Ltd.

- 6.4.16 CF Industries

- 6.4.17 The Mosaic Company

- 6.4.18 Yara International

- 6.4.19 ADM

- 6.4.20 ICL Group