|

시장보고서

상품코드

1850146

인공 장기 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Artificial Organ - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

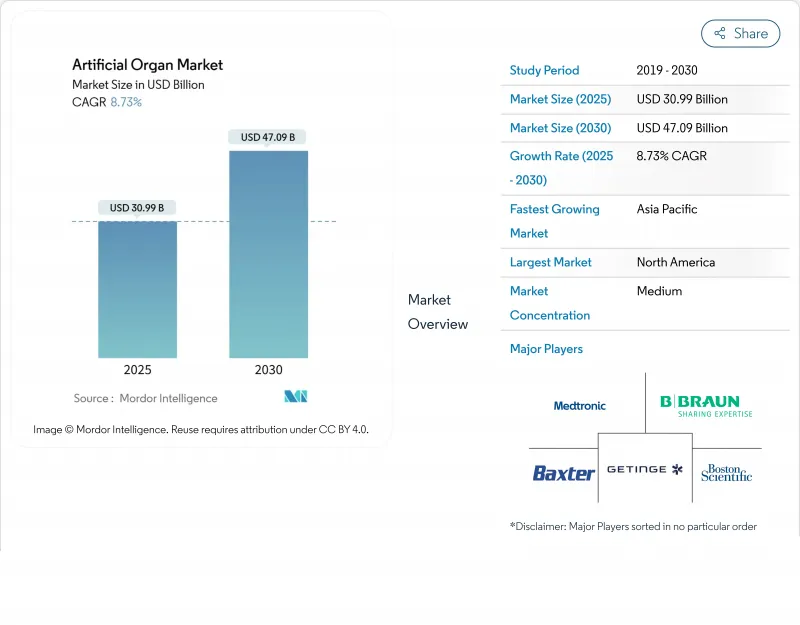

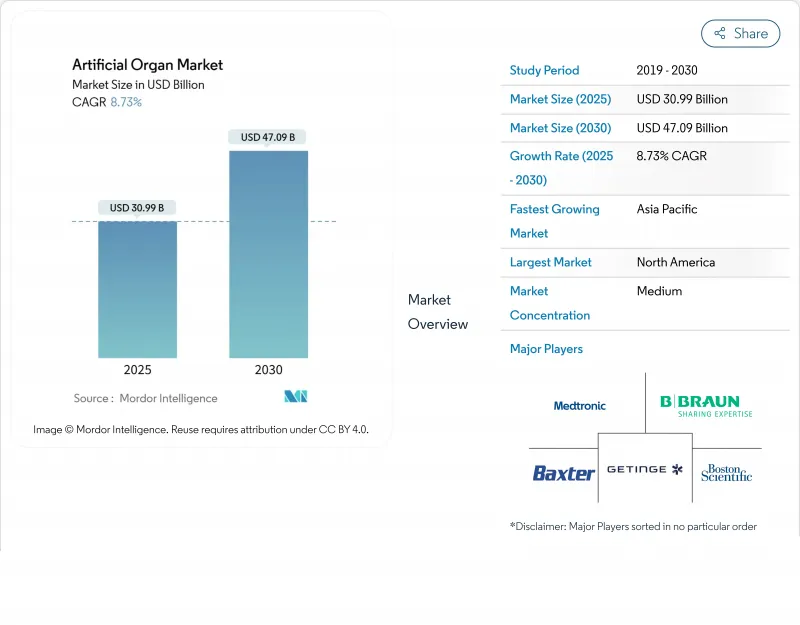

인공 장기 시장의 2025년 시장 규모는 309억 9,000만 달러로 평가되었고, 2030년에는 470억 9,000만 달러에 이를것으로 예측되며, CAGR은 8.73%를 나타낼 전망입니다.

만성 신장 질환, 심부전, 당뇨병 및 호흡기 질환의 급증으로 인한 강력한 수요가 기존 기증 장기 공급에 부담을 주고 있습니다. 생체 적합성 소재, 나노 규모 유체 관리 및 무선 센서 분야의 혁신은 제품 신뢰성을 높이고 이식 절차를 간소화하며 환자의 장기적 치료 결과를 개선했습니다. 특히 획기적 기기에 대한 신속 승인 절차 도입 등 보험급여 정책 변화는 시장 출시 기간을 단축하는 동시에 입원 기간을 단축하는 설계에 보상을 제공하고 있습니다. 원격 모니터링 플랫폼을 기반으로 한 가정 기반 치료 모델은 대형 병원을 넘어 임상 적용 범위를 확장하고 맞춤형 치료 조정을 가능하게 합니다. 이러한 요소들이 결합되어 인공 장기 시장은 향후 10년간 지속적인 두 자릿수 성장을 이룰 전망입니다.

세계의 인공 장기 시장 동향 및 인사이트

만성 질환과 장기 부전의 유병률 증가

신장, 심장 및 폐 질환 발생률이 장기 기증 증가율을 앞지르며, 미국 내 만성 신장 질환 성인 환자는 이미 3,550만 명에 달합니다. 말기 신장 질환 치료로 미국 메디케어 프로그램은 매년 1,300억 달러를 지출하며, 이는 이해관계자들을 내구성 있는 인공 대체 장치로 이끌고 있습니다. 역학 모델링에 따르면 2032년까지 8개 주요 경제권 인구의 최대 16.5%가 만성 신장 질환을 앓게 될 것으로 예상되며, 이로 인해 투석 수요가 75% 이상 증가할 전망입니다. 심장학 분야에서도 유사한 압박이 나타나고 있습니다. 이식 대기자 명단과 이용 가능한 심장 사이의 격차가 확대되면서 현재까지 인공 심장 이식 건수는 총 2,000명을 넘어섰습니다. 이처럼 임상적 긴급성이 인공 장기 시장 채택을 직접 촉진하고 있습니다.

연구개발 투자 증가

연방 보조금, 공공-민간 협력 및 벤처 캐피털이 제품 파이프라인을 가속화하고 있습니다. 미국 국립보건원(NIH)은 2024년 웨어러블 인공 신장 시스템 개선을 위해 459,824달러를 지원하며 공공 부문의 지속적인 지원을 입증했습니다. 대형 의료기술 기업들은 4D 바이오프린팅 및 자기 부상 펌프 기술 확보를 위해 틈새 혁신 기업을 인수하거나 협력하고 있으며, 광범위한 바이오기술 부문은 2030년까지 3조 2,000억 달러 규모에 이를 것으로 전망됩니다. 자본은 인공 장기 시장의 핵심 차별화 요소인 소형화, 혈액 적합성 코팅, AI 기반 제어 알고리즘에 집중되고 있습니다.

인공 장기 및 치료의 높은 비용과 제한적인 상환 옵션

전체 인공 심장은 이식당 20만 달러를 초과할 수 있으며, 특히 저소득 국가에서 보상 체계가 크게 다릅니다. 지급 기관들은 영구적 청구 코드 부여 전에 방대한 실세계 증거를 요구하는 경우가 많아 도입 속도를 늦추고 있습니다. 업계 단체들은 현재 규제 당국에 지급 경로 공식화를 촉구하며 로비 중이며, 이는 메디케어에 수명 주기 비용 절감 효과를 보상할 것을 요구하는 2025년 AI 정책 로드맵에 명시된 바와 같습니다. 혁신적인 가치 기반 계약이 등장하기 시작했지만, 인공 장기 시장의 단기적 가격 압박을 상쇄하기에는 여전히 부족합니다.

부문 분석

인공 신장 부문은 만성 신장 질환 환자 증가와 확고한 투석 생태계에 힘입어 2024년 인공 장기 시장 매출의 57%를 차지했습니다. 외래 환경에서의 지속적 신대체 요법에 대한 선호도 증가로 기기 활용도가 높은 수준을 유지하고 있습니다. 착용형 신장 시스템의 인공 장기 시장 규모는 2025년부터 2030년까지 연평균 14.4%의 성장률을 보일 것으로 예상되며, 이는 하루 8-10시간의 이동성을 허용하는 휴대용 나노전기운동 모듈에 힘입은 것입니다. 초기 임상 연구에 따르면 치료가 병원 내 세션에서 외래 자가 관리로 전환될 때 환자 만족도가 향상되는 것으로 나타났습니다.

의료진은 독소 제거와 호르몬 대체 기능을 결합한 카트리지를 시험 중이며, 이를 통해 말기 질환을 넘어선 적응증 확대를 모색하고 있습니다. 인공 췌장이 다음 주자로 부상 중이며, 성숙한 연속 혈당 모니터와 폐쇄형 인슐린 펌프의 혜택을 받고 있습니다. 한편 인공 폐는 코로나19 위기 동안 주목받았으며, 생체 인공 간 프로토타입은 급성 전격성 간부전을 목표로 합니다. 이러한 혁신들은 인공 장기 시장 내 단일 지배적 장기 부문에 대한 의존도를 낮추고 수익원을 다각화합니다.

기계식 플랫폼은 확립된 임상 프로토콜과 검증된 안전성 프로파일 덕분에 2024년 매출의 67%를 차지했습니다. 투석기, 막형 산소화기, 원심 펌프는 여전히 병원의 핵심 장비입니다. 그러나 전자식 및 바이오닉 구조가 빠르게 확장 중이며, 이 하위 부문은 2030년까지 연평균 11.2% 성장할 것으로 예상됩니다. 스마트 센서, 폐쇄 루프 소프트웨어 및 내장형 전력 관리 기술은 동적 유량 조절과 실시간 혈전 감지를 가능케 하며, 이는 이제 고급 심장 보조 장치에 기대되는 특성입니다. 결과적으로 병원 구매 기준은 점차 연결성과 AI 분석을 고려하게 되었으며, 이러한 변화는 전자 혁신 기업들을 인공 장기 시장 성장 동력의 중심에 위치시킵니다.

비전 기반 4D 바이오프린팅은 최첨단 기술로, 미세혈관 네트워크를 갖춘 맞춤형 연조직 이식편을 약속합니다. 이 분야의 성공은 완전 세포화 장기의 대량 맞춤화를 가속화하여 기계적 및 생물학적 패러다임을 연결할 것입니다.

인공 장기 시장 보고서는 장기 유형(인공 심장 (인공 심장 판막, 기타), 인공 신장 등), 기술(기계, 전자/바이오닉스 등), 고정 방법(완전 이식형, 기타), 최종 사용자(병원(병상 300개 이상), 병원(병상 300개 미만), 기타), 지역(북미, 유럽 등)으로 분류 시장 예측은 금액(달러)으로 제공됩니다.

지역별 분석

북미는 2024년 전 세계 매출의 45%를 차지했으며, 생명 유지 장치에 대한 강력한 메디케어 보장 및 대규모 투석 클리닉 설치 기반이 이를 뒷받침했습니다. 미국 단독으로 전 세계 의료 기기 소비의 40%를 차지하며, FDA 혁신적 설계로 지정된 이식 장치의 광범위한 파이프라인이 신속한 상용화를 촉진하고 있습니다. 현재 지불자 시범 사업은 원격 모니터링을 회원당 월 단위로 보상하여 병원에서의 치료에서 가정 치료로의 전환을 장려하고 있습니다.

아시아태평양 지역은 2030년까지 연평균 12.3% 성장률로 가장 빠르게 성장하는 지역입니다. 중국과 인도는 보편적 건강보험 적용 범위를 확대 중이며, 국가 조달 프로그램이 투석 카트리지 및 심실 보조 장치의 대량 구매 가격을 협상 중입니다. 일본의 인구 고령화는 심장 지원 수요를 가속화하는 반면, 한국의 풍부한 연구개발(R&D) 인센티브는 현지 기업들이 소형화된 구동 시스템을 수출하는 데 기여합니다. 현지 생산은 비용을 최대 30% 절감하여 접근성을 확대하고 중소득 계층 전반에 걸쳐 인공 장기 시장 채택을 촉진합니다.

유럽은 의료기기 규정(MDR) 하의 통일된 품질 기준 덕분에 여전히 영향력을 유지하고 있습니다. 독일과 영국은 생체 인공 심장판막과 장기간 착용형 인슐린 펌프의 조기 채택을 주도하는 반면, 유럽 장기이식학회(ESOT)의 새로운 이니셔티브는 첨단 치료에 대한 보험급여 조화를 모색하고 있습니다. 경제적 제약은 지속되나, EU 차원의 조율된 조달이 남부 및 동부 회원국으로의 확산을 지원할 전망입니다.

중동 및 아프리카와 남미는 매출 비중이 상대적으로 낮습니다. 사우디아라비아, 아랍에미리트, 브라질, 남아프리카공화국에서 도입이 가장 활발하며, 민간 네트워크가 정교한 임플란트 시술을 지원합니다. 공공병원 예산은 여전히 압박을 받고 있으나, 다국적 의료기기 공급업체와의 전략적 제휴로 의료진 교육 및 보증 범위가 개선되고 있습니다. 예측 기간 동안 다중센터 원격 중환자실 허브와 국경 간 서비스 모델이 접근성 격차를 좁혀 인공 장기 시장에서의 지역 참여도를 높일 것으로 전망됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 만성질환과 장기부전의 유병률 증가

- 연구개발 투자 증가

- 기증 장기 부족 및 윤리적 문제

- 전 세계 고령 인구 증가

- 기술과 생체 적합성의 발전

- 삶의 질 개선을 위한 환자 선호도

- 시장 성장 억제요인

- 인공 장기 및 시술 비용이 높고 보험 적용 범위가 제한적

- 기기 수명 및 생체 적합성 문제

- 인식 부족 및 숙련된 의료 전문가 부족

- 복잡한 외과 수술

- 공급망 분석

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 장기 유형별

- 인공 심장

- 인공 심장 판막

- 심실 보조 장치

- 심장 박동기 및 ICD

- 인공 신장

- 내장형 디바이스

- 웨어러블/휴대용 시스템

- 인공 췌장

- 인공 폐/ECMO

- 인공 내이 및 청성뇌간 임플란트

- 바이오 인공 간

- 기타 장기(각막, 비장, 방광, 기관)

- 인공 심장

- 기술별

- 기계

- 전자식/바이오닉스

- 웨어러블/외장

- 3D 바이오프린트 구조

- 고정 방법별

- 완전 이식형

- 부분 이식형

- 외장/경피

- 최종 사용자별

- 병원(병상 300개 이상)

- 병원(병상 300개 미만)

- 외래수술센터(ASC)

- 재택 케어와 원격 모니터링

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Medtronic plc

- Abbott Laboratories

- Boston Scientific Corp.

- Abiomed(Johnson & Johnson MedTech)

- SynCardia Systems LLC

- Berlin Heart GmbH

- CARMAT SA

- Jarvik Heart Inc.

- BiVACOR Pty Ltd

- Terumo Corp.

- Getinge AB

- Fresenius Medical Care AG

- AWAK Technologies Pte Ltd

- ALung Technologies Inc.

- Cochlear Ltd.

- Asahi Kasei Medical Co. Ltd

- B. Braun Melsungen AG

- Baxter International Inc.

- Edwards Lifesciences Corp.

- Tandem Diabetes Care

- 3D Systems Healthcare

제7장 시장 기회와 장래의 전망

HBR 25.11.19The artificial organs market is valued at USD 30.99 billion in 2025 and is on course to reach USD 47.09 billion by 2030, advancing at an 8.73% CAGR.

Strong demand stems from the rapid rise in chronic kidney disease, heart failure, diabetes and respiratory disorders, all of which strain existing donor-organ supply. Breakthroughs in biocompatible materials, nano-scale fluid management and wireless sensors have lifted product reliability, eased implantation and improved long-term patient outcomes. Shifts in reimbursement policies, especially the introduction of accelerated approval routes for breakthrough devices, are shortening time-to-market while rewarding designs that cut hospital stays. Home-based care models, powered by remote monitoring platforms, are expanding clinical reach beyond large hospitals and enabling personalized therapy adjustments. Together, these forces position the artificial organs market for durable double-digit growth through the decade.

Global Artificial Organ Market Trends and Insights

Increasing Prevalence of Chronic Diseases and Organ Failure

Kidney, cardiac and pulmonary diseases are climbing at rates that outpace organ donation, with 35.5 million adults in the United States already living with chronic kidney disease. End-stage renal disease treatment costs the US Medicare program USD 130 billion each year, pushing stakeholders toward durable artificial alternatives. Epidemiological modeling projects that up to 16.5% of the population in eight large economies will have chronic kidney disease by 2032, inflating dialysis demand by more than 75%. Similar pressures surface in cardiology, where a widening gap between listed transplant candidates and available hearts has pushed total artificial heart implant volume beyond 2,000 patients to date. As such, clinical urgency is directly feeding artificial organs market adoption.

Rising Investment in Research and Development

Federal grants, public-private alliances and venture capital are accelerating product pipelines. The National Institutes of Health awarded USD 459,824 in 2024 to refine the Wearable Artificial Kidney system, validating sustained public-sector support. Large med-tech firms are buying or partnering with niche innovators to gain access to 4D bioprinting and magnetically levitated pumps, while the broader biotechnology segment is forecast to reach USD 3.2 trillion by 2030. Capital is concentrating on miniaturization, hemocompatible coatings and AI-enabled control algorithms, key differentiators in the artificial organs market.

High Cost of Artificial Organs and Procedures Coupled with Limited Reimbursement Options

Total artificial hearts can exceed USD 200,000 per implant, and reimbursement frameworks vary widely, especially in low-income economies. Payers often require extensive real-world evidence before assigning permanent billing codes, slowing uptake. Trade groups now lobby regulators to formalize payment pathways, as outlined in a 2025 AI Policy Roadmap that calls on Medicare to reward life-cycle cost savings. Innovative value-based contracts are beginning to emerge but remain too scarce to offset near-term pricing pressure on the artificial organs market.

Other drivers and restraints analyzed in the detailed report include:

- Shortage of Donor Organs and Ethical Concerns

- Growing Aging Population Globally

- Device Longevity and Biocompatibility Issues

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The artificial kidney segment generated 57% of artificial organs market revenue in 2024, driven by the expanding chronic kidney disease population and the entrenched dialysis ecosystem. Growing preference for continuous renal replacement in outpatient settings keeps device utilization high. The artificial organs market size for wearable kidney systems is forecast to climb at a 14.4% CAGR from 2025-2030, supported by portable nanoelectrokinetic modules that permit 8-10 hours of daily mobility. Early clinical studies highlight improved patient satisfaction when therapy shifts from clinic-bound sessions to ambulatory self-care.

Clinicians are also trialing combined toxin removal and hormone-replacement cartridges, broadening indications beyond end-stage disease. Artificial pancreases are next in line, benefiting from mature continuous glucose monitors and closed-loop insulin pumps. Meanwhile, artificial lungs gained visibility during the COVID-19 crisis, and bio-artificial liver prototypes target acute fulminant hepatic failure. Together, these innovations diversify revenue streams and reduce reliance on a single dominant organ segment within the artificial organs market.

Mechanical platforms held 67% of 2024 revenue due to established clinical protocols and proven safety profiles. Dialysis machines, membrane oxygenators and centrifugal pumps remain hospital workhorses. Yet electronic and bionic architectures are scaling fast, and this sub-segment is predicted to grow at 11.2% CAGR through 2030. Smart sensors, closed-loop software and on-board power management allow dynamic flow regulation and real-time clot detection, properties now expected in premium cardiac support devices. As a result, hospital purchasing criteria increasingly consider connectivity and AI analytics, a shift that places electronic innovators at the center of artificial organs market momentum.

Vision-guided 4D bioprinting sits at the frontier, promising personalized soft-tissue grafts with microvascular networks. Success here would bring fully cellularized organs closer to mass-customization, bridging mechanical and biological paradigms.

The Artificial Organ Market Report is Segmented by Organ Type (Artificial Heart [Prosthetic Heart Valves, and More], Artificial Kidney, and More), Technology (Mechanical, Electronic / Bionics, and More), Fixation Method (Fully Implantable, and More), End User (Hospitals (>300 Beds), Hospitals (<300 Beds) and More) and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 45% of global revenue in 2024, anchored by robust Medicare coverage for life-sustaining devices and a large installed base of dialysis clinics. The United States alone represents 40% of worldwide medical device consumption, with an extensive pipeline of FDA breakthrough-designated implants facilitating faster commercialization. Payer pilots now reimburse remote monitoring on a per-member-per-month basis, encouraging migration from hospital to home.

Asia-Pacific is the fastest growing region, advancing at a 12.3% CAGR through 2030. China and India are scaling universal health-insurance coverage, and national procurement programs are negotiating bulk prices for dialysis cartridges and ventricular assist devices. Population aging in Japan accelerates cardiac support demand, while South Korea's well-funded R&D incentives help local firms export miniaturized drive systems. Local manufacturing cuts cost by up to 30%, broadening access and propelling artificial organs market adoption across mid-income segments.

Europe remains influential, thanks to uniform quality standards under the Medical Device Regulation. Germany and the United Kingdom drive early adoption of bioprosthetic heart valves and long-wear insulin pumps, whereas newer European Society for Organ Transplantation initiatives seek to harmonize advanced-therapy reimbursement. Economic constraints persist, yet coordinated procurement at the EU level is expected to support wider diffusion across Southern and Eastern member states.

Middle East and Africa plus South America account for a smaller slice of revenue. Uptake is strongest in Saudi Arabia, the United Arab Emirates, Brazil and South Africa, where private networks finance sophisticated implants. Public hospital budgets remain under pressure, but strategic partnerships with multinational device suppliers are improving clinician training and warranty coverage. Over the forecast horizon, multicenter tele-ICU hubs and cross-border service models should narrow the accessibility gap, lifting regional participation in the artificial organs market.

- Medtronic

- Abbott Laboratories

- Boston Scientific

- Abiomed (Johnson & Johnson MedTech)

- SynCardia Systems

- Berlin Heart

- CARMAT SA

- Jarvik Heart

- BiVACOR Pty Ltd

- Terumo Corp.

- Getinge

- Fresenius Medical Care AG

- AWAK Technologies Pte Ltd

- ALung Technologies Inc.

- Cochlear

- Asahi Kasei

- B. Braun

- Baxter

- Edwards Lifesciences Corp.

- Tandem Diabetes Care

- 3D Systems Healthcare

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Prevalence of Chronic Diseases and Organ Failure

- 4.2.2 Rising Investment in Research and Development

- 4.2.3 Shortage of Donor Organs and Ethical Concerns

- 4.2.4 Growing Aging Population Globally

- 4.2.5 Advancements in Technology and Biocompatibility

- 4.2.6 Patient Preference for Improved Quality of Life

- 4.3 Market Restraints

- 4.3.1 High Cost of Artificial Organs and Procedures Coupled with Limited Reimbursement Options

- 4.3.2 Device Longevity and Biocompatibility Issues

- 4.3.3 Limited Awareness and Skilled Healthcare Professionals

- 4.3.4 Complex Surgical Procedures

- 4.4 Supply-Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Organ Type

- 5.1.1 Artificial Heart

- 5.1.1.1 Prosthetic Heart Valves

- 5.1.1.2 Ventricular Assist Devices

- 5.1.1.3 Cardiac Pacemakers & ICDs

- 5.1.2 Artificial Kidney

- 5.1.2.1 Implantable Devices

- 5.1.2.2 Wearable / Portable Systems

- 5.1.3 Artificial Pancreas

- 5.1.4 Artificial Lungs/ECMO

- 5.1.5 Cochlear & Auditory Brain-stem Implants

- 5.1.6 Bio-artificial Liver

- 5.1.7 Other Organs (Cornea, Spleen, Bladder, Trachea)

- 5.1.1 Artificial Heart

- 5.2 By Technology

- 5.2.1 Mechanical

- 5.2.2 Electronic / Bionics

- 5.2.3 Wearable / Externally Worn

- 5.2.4 3D-Bioprinted Constructs

- 5.3 By Fixation Method

- 5.3.1 Fully Implantable

- 5.3.2 Partially Implantable

- 5.3.3 Externally Worn / Percutaneous

- 5.4 By End User

- 5.4.1 Hospitals (>300 Beds)

- 5.4.2 Hospitals (<300 Beds)

- 5.4.3 Ambulatory Surgical Centers

- 5.4.4 Home-care & Remote Monitoring

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Medtronic plc

- 6.3.2 Abbott Laboratories

- 6.3.3 Boston Scientific Corp.

- 6.3.4 Abiomed (Johnson & Johnson MedTech)

- 6.3.5 SynCardia Systems LLC

- 6.3.6 Berlin Heart GmbH

- 6.3.7 CARMAT SA

- 6.3.8 Jarvik Heart Inc.

- 6.3.9 BiVACOR Pty Ltd

- 6.3.10 Terumo Corp.

- 6.3.11 Getinge AB

- 6.3.12 Fresenius Medical Care AG

- 6.3.13 AWAK Technologies Pte Ltd

- 6.3.14 ALung Technologies Inc.

- 6.3.15 Cochlear Ltd.

- 6.3.16 Asahi Kasei Medical Co. Ltd

- 6.3.17 B. Braun Melsungen AG

- 6.3.18 Baxter International Inc.

- 6.3.19 Edwards Lifesciences Corp.

- 6.3.20 Tandem Diabetes Care

- 6.3.21 3D Systems Healthcare

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment