|

시장보고서

상품코드

1850224

단백질체학 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Proteomics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

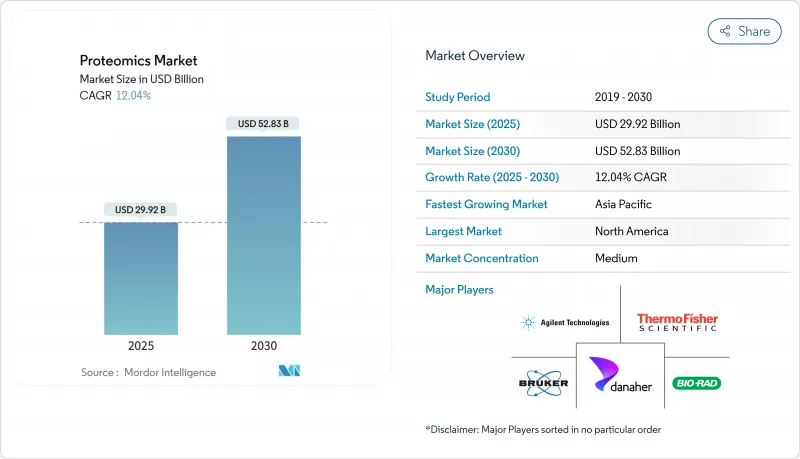

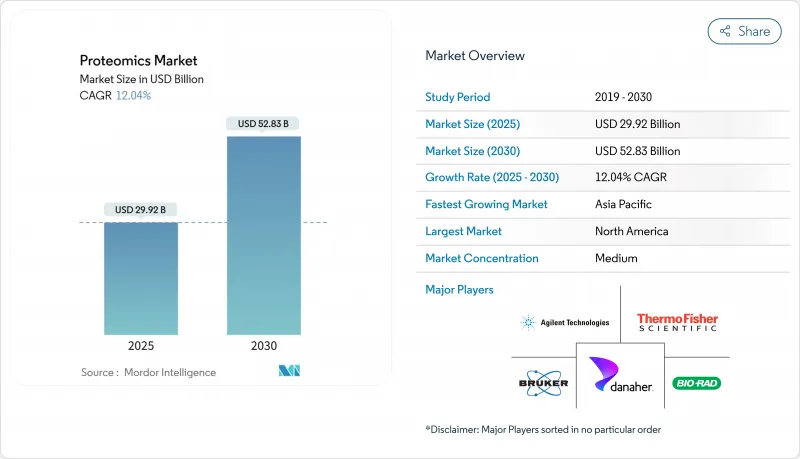

단백질체학 시장 규모는 2025년에 299억 2,000만 달러로 평가되었고, 2030년에는 528억 3,000만 달러로 확대될 것으로 예측되며, CAGR은 12.04%를 나타낼 전망입니다.

고속 대량 분석 시스템의 급속한 도입, 인공지능 기반 단일 세포 워크플로우, 그리고 정밀의학 프로그램에 단백질체학 분석 결과를 통합하는 추세가 확장을 주도하고 있습니다. 제약사들은 표적 발견, 선도물질 최적화, 바이오마커 검증 전반에 단백질체학을 적용하고 있으며, 계약 연구 기관(CRO)들은 전문 서비스를 확대하고 있습니다. 지역별로는 지속적인 R&D 자금 지원과 확고한 바이오의약품 인프라가 북미의 주도적 위치를 공고히 하는 반면, 중국, 인도, 일본, 한국에 걸친 활발한 투자가 아시아태평양 지역을 가장 빠르게 성장하는 시장으로 자리매김하게 합니다. 경쟁 역학은 플랫폼 통합에 집중됩니다. 대형 벤더들은 틈새 혁신 기업들을 인수하여 의약품 개발 고객의 프로젝트 기간을 단축하는 종단간 시약, 장비 및 분석 솔루션을 제공합니다.

세계의 단백질체학 시장 동향 및 인사이트

맞춤형 및 정밀 의학에 대한 수요 증가

증가하는 임상 증거는 단백질 기반 바이오마커와 질병 계층화를 연결하여 대규모 코호트 연구에 단백질체학 패널의 일상적 포함을 촉진하고 있습니다. 영국 바이오뱅크 프로그램이 60만 개 샘플에서 5,400개 단백질을 프로파일링하기 위해 선택한 써모 피셔 사이언티픽의 올링크 플랫폼은 이러한 변화를 보여주는 사례로, 치료제 선택을 안내하는 다차원 데이터셋을 생성합니다. 단백질체 적합도 점수는 이제 유전적 위험 지표를 보완하며 생활습관 개입에 대한 반응성을 입증해 예방 의료 계획 수립의 가치를 강조하고 있습니다. 순환 단백질 시그니처에서 도출된 장기별 노화 시계는 조기 개입 전략 수립에 기여하고 있습니다. 제약 업계 관계자들은 이러한 인사이트이 동반진단 개발에 핵심적이라고 평가하며 차세대 분석 플랫폼에 대한 지속적인 수요를 강화하고 있습니다.

연구개발비와 공적자금 증가

바이오제약사와 공공 자금을 통합하는 컨소시엄 자금 모델은 과거 엘리트 학술 기관에만 국한되던 인프라를 확장하고 있습니다. 14개 바이오제약사가 자금을 지원하는 영국 바이오뱅크의 단백질체학 이니셔티브는 산업계 협력이 이전에는 불가능했던 대규모 단백질체학 연구를 주도하는 패러다임 전환을 보여줍니다. 중국, 일본, 한국의 정부 보조금은 고해상도 질량 분석기 설치 및 클라우드 기반 데이터 허브를 지원하여 신생 연구실의 진입 장벽을 낮춥니다. 벤처 캐피털은 AI 기반 단백질체학 소프트웨어 기업으로 유입되어 분석 시간을 며칠에서 몇 분으로 단축하고 사용자 접근성을 확대하는 자동화된 패턴 인식 도구의 개발을 가속화합니다.

장비의 높은 자본 비용과 운영 비용

최상위 오비트랩(Orbitrap) 또는 이온 이동도 트랩(trapped-ion-mobility) 플랫폼은 시스템당 100만 달러를 상회하며, 연간 유지보수 계약 비용이 구매가의 10%를 추가로 발생시킬 수 있습니다. 연구실은 소모품, 진공 인프라, 환경 제어 장치에 대한 예산도 편성해야 합니다. E3 방법과 같은 대학 차원의 이니셔티브가 시료 전처리 비용을 절감하지만, 하드웨어 지출은 중견 기관에게 여전히 장벽으로 작용합니다. 공유 시설 모델과 CRO 아웃소싱은 진입 비용을 완화하지만 실험 유연성을 제한할 수 있습니다.

부문 분석

2024년 단백질체학 시장 점유율에서 시약 부문이 69.78%를 차지했으며, 이는 시료 용해, 농축, 표지, 정량화 단계 전반에 걸쳐 소모성 및 필수성을 반영한 결과입니다. 검출 특이성을 향상시키는 생체정합성 태그의 높은 채택률은 지속적인 재주문 물량을 유지합니다. 기기 하위 부문은 단일 세포 분석을 위해 설계된 초고해상도 분광기에 대한 프리미엄 가격 정책으로 혜택을 보고 있습니다. 소프트웨어 및 서비스 부문은 실험실이 증가하는 데이터 양에 직면하고 생물정보학 병목 현상을 해소하는 AI 기반 분석 플랫폼을 추구함에 따라 13.56%의 연평균 복합 성장률(CAGR)로 성장하고 있습니다. 품질 관리 대시보드와 자동화된 주석을 통합하는 클라우드 네이티브 파이프라인은 비전문가들의 접근성을 확대하여 전체 단백질체학 시장 확장을 지원합니다.

구독형 라이선싱 도입은 공급업체 수익을 가속화하는 한편, 관리형 서비스 계약은 장비 모니터링, 데이터 저장, 규정 준수 보고를 예측 가능한 비용으로 묶어 제공합니다. CRO(계약 연구 기관)는 모듈형 소프트웨어를 활용해 신속한 연구 결과를 제공함으로써, 소규모 바이오테크 기업들이 고가의 하드웨어 설치 없이도 신약 발굴을 수행할 수 있게 합니다. 다중 오믹스 통합이 일상화됨에 따라 전사체 및 단백체 계층을 공동 분석하는 하이브리드 워크플로는 이질적 데이터셋을 조화시킬 수 있는 미들웨어에 의존하며, 이는 단백체학 시장 내 전문 분석 솔루션 수요를 더욱 촉진합니다.

2024년 단백질체학 시장 점유율의 30.69%를 차지한 질량 분석 플랫폼은 이온 광학 및 검출기 설계의 지속적인 혁신으로 80 kDa까지의 단백질에 대해 200,000 이상의 분해능을 구현했습니다. 비행시간-오비트랩 하이브리드 시스템은 인구 규모 코호트 연구를 지원하는 스캔 속도에서 ppm 미만의 질량 정확도를 제공합니다. 차세대 시퀀싱과 연계된 단백질체학 시장 규모는 단백질 상호작용 네트워크 매핑에서 DNA 인코딩 라이브러리와 리보솜 디스플레이 시스템의 활용도가 수렴함에 따라 연평균 13.71% 성장할 것으로 전망됩니다. 시퀀싱 기반 판독값은 번역 후 변형에 대한 직교적 검증을 제공하고 고다중 정량화를 지원합니다.

두 번째 단락 : 마이크로플루이딕 기반 분리 및 공간 분해능 단백질 어레이와 같은 보완적 방법이 조직 맥락 분석에서 주목받고 있습니다. 초고압 변형을 포함한 크로마토그래피 업그레이드의 통합은 프런트엔드 분리를 향상시키고 시료 이월을 줄여, 저농도 펩타이드 식별에 대한 신뢰도를 높입니다. 공급업체들은 이제 LC-MS, 모세관 전기영동, 이미징 기반 워크플로우 간 이관을 간소화하는 크로스플랫폼 키트를 패키징하여 단백질체학 시장 내 종단적 연구를 위한 방법 연속성을 보장합니다.

지역 분석

북미는 확고한 바이오제약 기업 기반, 지속적 국립보건원(NIH) 자금 지원, 대규모 정밀의학 코호트 덕분에 2024년 글로벌 매출의 44.31%를 유지했습니다. 미국은 테르모 피셔 사이언티픽(Thermo Fisher Scientific)과 같은 선도적 공급업체를 보유하고 있으며, 해당 기업은 기술 폭을 확대하기 위해 평균 30억 9천만 달러 규모의 전략적 인수합병 54건을 완료했습니다. 캐나다는 공공-민간 유전체학 이니셔티브를 통해 확장 중이며, 멕시코는 지역 제네릭 제조사에 서비스를 제공하는 틈새 CRO 역량을 구축하고 있습니다.

유럽은 독일, 영국, 프랑스가 주요 기여국으로 11.96%의 연평균 성장률(CAGR)을 기록했습니다. 영국 바이오뱅크의 프로테옴 프로그램은 범유럽 협력을 보여주는 사례로, 제약 스폰서를 위해 다중 오믹스 데이터셋을 해석하는 계약 분석 제공업체 생태계를 뒷받침합니다. 독일은 국내 정밀 계측기 공학을 활용해 고성능 LC-MS 시스템을 수출하는 반면, 프랑스와 이탈리아는 단백질체학 종결점을 통합한 임상시험 네트워크를 확장하며 대륙 전체의 단백질체학 시장을 강화하고 있습니다.

아시아태평양 지역은 2030년까지 연평균 13.84% 성장률로 가장 빠르게 성장하는 지역으로 전망됩니다. 중국의 5개년 계획은 생명공학을 전략적 핵심 분야로 지정했으며, 신개념 진단 패널에 대한 특허 부여는 국내 혁신 역량을 입증합니다. 인도는 비용 효율적인 CRO(계약 연구 기관) 허브에 투자를 유치하고 프로테오게노믹스 공동 학위 프로그램을 설립해 인재 부족을 해소합니다. 일본은 로봇 기반 시료 전처리 기술을 선도하는 반면, 한국은 AI 기반 생물정보학 스타트업에 보조금을 지원합니다. 호주의 전환 연구 연합은 농업유전체학과 희귀질환 진단에 집중하며 접근 가능한 단백질체학 시장을 확대하고 있습니다. 중동 및 아프리카 지역은 3차 병원에서 점진적으로 도입 중이며, 브라질은 백신 관련 프로테옴 연구를 통해 남미 지역 도입을 주도하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 맞춤형 및 정밀 의학에 대한 수요 증가

- 연구개발비와 공적자금 증가

- 고속 대량 분석(MS) 및 액체 크로마토그래피-질량 분석(LC-MS) 플랫폼의 급속한 발전

- 신약 개발 파이프라인에서 단백질체학 활용 확대

- 인공지능(AI) 기반 단일 세포 단백질체학 기술의 혁신적 발전

- 농업 유전체학 및 식품 안전 분야에서의 단백질체학 활용 확대

- 시장 성장 억제요인

- 장비의 높은 자본 및 운영 비용

- 숙련된 바이오인포매틱스 전문가와 단백질체학 전문가의 부족

- 데이터 분석의 복잡성 및 워크플로우 표준 부재

- 천연 막 단백질 연구의 제한된 처리량

- 공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 컴포넌트별

- 기기

- 시약

- 소프트웨어 및 서비스

- 기술별

- 질량 분석

- 분광법

- 크로마토그래피

- 차세대 시퀀싱

- 단백질 마이크로어레이

- 마이크로플루이딕스

- X선 결정 구조 분석

- 기타 기술

- 용도별

- 신약 개발

- 임상 진단

- 바이오마커 발견

- 정밀의학 및 맞춤형 의료

- 농업과 환경 단백질체학

- 기타 용도

- 최종 사용자별

- 제약 및 생명공학 기업

- 학술연구기관

- 계약연구기관

- 기타 최종 사용자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- Competitive Benchmarking

- 시장 점유율 분석

- 기업 프로파일

- Agilent Technologies Inc.

- Alamar Biosciences, Inc.

- Bioneer Corporation

- Bioinformatics Solutions Inc.

- Bio-Rad Laboratories Inc.

- Bruker Corporation

- Creative Proteomics

- Danaher Corporation

- Evosep

- GE Healthcare

- Illumina Inc.

- Merck KGaA

- Nautilus Biotechnology

- Olink Holding AB

- Oxford Nanopore Technologies

- Promega Corporation

- Proteome Factory AG

- Proteome Sciences PLC

- QIAGEN NV

- Revvity, Inc.

- Seer Inc.

- Shimadzu Corporation

- SomaLogic Inc.

- Thermo Fisher Scientific Inc.

- Waters Corporation

제7장 시장 기회와 장래의 전망

HBR 25.11.17The proteomics market size is estimated at USD 29.92 billion in 2025 and is projected to advance to USD 52.83 billion by 2030, reflecting a 12.04% CAGR.

Expansion is propelled by rapid adoption of high-throughput mass-spectrometry systems, AI-enabled single-cell workflows, and growing integration of proteomic readouts into precision-medicine programs. Pharmaceutical firms are embedding proteomics across target discovery, lead optimization, and biomarker validation, while contract research organizations (CROs) scale specialized services. Regionally, continued R&D funding and entrenched biopharma infrastructure anchor North American leadership, whereas vigorous investment across China, India, Japan, and South Korea positions Asia-Pacific as the fastest-growing arena. Competitive dynamics centre on platform consolidation: large vendors acquire niche innovators to deliver end-to-end reagent, instrument, and analytics solutions that shorten project timelines for drug-development customers.

Global Proteomics Market Trends and Insights

Rising Demand for Personalized & Precision Medicine

Growing clinical evidence links protein-based biomarkers with disease stratification, fostering routine inclusion of proteomic panels in large cohort studies. Thermo Fisher Scientific's Olink platform's selection for the UK Biobank's programme to profile 5,400 proteins across 600,000 samples exemplifies this shift, creating multidimensional datasets that guide therapeutic selection. Proteomic fitness scores now complement genetic risk metrics and have demonstrated responsiveness to lifestyle interventions, underscoring value for preventive-care planning. Organ-specific ageing clocks derived from circulating protein signatures are informing early intervention strategies. Pharma stakeholders view these insights as pivotal for companion-diagnostic development, reinforcing sustained demand for next-generation assay platforms.

Increasing R&D Expenditure and Public Funding

Consortia funding models that pool biopharma and public financing are scaling infrastructure once limited to elite academic centres. The UK Biobank's proteomics initiative, funded by 14 biopharmaceutical companies, represents a paradigm shift where industry collaboration drives large-scale proteomic studies that were previously unfeasible. Government grants across China, Japan, and Korea subsidize high-resolution mass-spectrometry installations and cloud-based data hubs, lowering barriers for start-up laboratories. Venture capital flows toward AI-native proteomic software firms, accelerating automated pattern-recognition tools that cut analysis times from days to minutes and broaden user access.

High Capital & Operating Cost of Instruments

Top-tier Orbitrap or trapped-ion-mobility platforms routinely exceed USD 1 million per system, and annual service contracts may add 10% of purchase price. Labs must also budget for consumables, vacuum infrastructure, and environmental controls. Although university-level initiatives such as the E3 method reduce sample-prep costs, hardware outlays remain a hurdle for mid-tier institutions. Shared-facility models and CRO outsourcing mitigate entry costs yet can constrain experimental flexibility.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Advances in High-Throughput MS & LC-MS Platforms

- Growing Adoption in Drug-Discovery Pipelines

- Shortage of Skilled Bioinformaticians & Proteomics Experts

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Reagents accounted for 69.78% of the proteomics market share in 2024, reflecting their consumable nature and indispensability across sample lysis, enrichment, labelling, and quantitation steps. High adoption of bioorthogonal tags that improve detection specificity sustains robust reorder volumes. The instruments sub-segment benefits from premium pricing on ultrahigh-resolution spectrometers designed for single-cell assays. Software and services are growing at a 13.56% CAGR as laboratories confront rising data volumes and seek AI-driven analytics platforms that remove bioinformatics bottlenecks. Cloud-native pipelines that integrate quality-control dashboards with automated annotation broaden accessibility for non-specialists, supporting overall proteomics market expansion.

Second paragraph: Adoption of subscription licensing accelerates vendor revenue, while managed-service contracts bundle instrument monitoring, data storage, and compliance reporting into predictable fees. CROs leverage modular software to offer rapid-turnaround studies, allowing smaller biotech companies to conduct discovery without installing costly hardware. As multi-omics integration becomes routine, hybrid workflows that co-analyze transcriptomic and proteomic layers rely on middleware capable of harmonizing heterogeneous datasets, further fueling demand for specialized analytics solutions within the proteomics market.

Mass-spectrometry platforms captured 30.69% of the proteomics market share in 2024, owing to continuous innovation in ion-optics and detector design that extends resolving power past 200,000 for proteins up to 80 kDa. Time-of-flight-Orbitrap hybrids deliver sub-ppm mass accuracy at scan speeds supporting population-scale cohort studies. The proteomics market size tied to next-generation sequencing is forecast to expand at 13.71% CAGR, reflecting the converging utility of DNA-encoded libraries and ribosome-display systems in mapping protein-interaction networks. Sequencing-based readouts provide orthogonal validation of post-translational modifications and support high-multiplex quantitation.

Second paragraph: Complementary methods such as microfluidic-based separation and spatially resolved protein arrays gain traction for tissue-context analysis. Integration of chromatography upgrades, including ultra-high-pressure variants, enhances front-end separation and reduces sample carry-over, boosting confidence in low-abundance peptide identification. Vendors now package cross-platform kits that streamline transfer between LC-MS, capillary electrophoresis, and imaging-based workflows, ensuring method continuity for longitudinal studies within the proteomics market.

The Proteomics Market Report is Segmented by Component (Instruments and More), Technology (Mass Spectrometry and More), Application (Drug Discovery & Development and More), End-User (Pharmaceutical & Biotechnology Companies and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 44.31% of global revenue in 2024 due to an entrenched biopharma enterprise, sustained National Institutes of Health funding, and large-scale precision-medicine cohorts. The United States hosts leading vendors such as Thermo Fisher Scientific, which has closed 54 strategic acquisitions, averaging USD 3.09 billion, to deepen technology breadth. Canada expands through public-private genomics initiatives, while Mexico builds niche CRO capabilities serving regional generics manufacturers.

Europe recorded 11.96% CAGR with Germany, the United Kingdom, and France as principal contributors. The UK Biobank's proteome programme exemplifies pan-European collaboration and underpins an ecosystem of contract-analysis providers that interpret multi-omic datasets for pharma sponsors. Germany leverages domestic precision-instrument engineering to export high-performance LC-MS systems, whereas France and Italy scale clinical trial networks that integrate proteomics endpoints, strengthening the proteomics market across the continent.

Asia-Pacific is positioned as the fastest-growing region at 13.84% CAGR through 2030. China's Five-Year Plan earmarks biotechnology as a strategic pillar, and patent grants for novel diagnostic panels validate domestic innovation capacity. India draws investment into cost-effective CRO hubs and establishes joint-degree programmes in proteogenomics to alleviate talent shortages. Japan pioneers robotics-enabled sample preparation, while South Korea subsidizes AI-native bio-informatics start-ups. Australia's translational research alliances focus on agrigenomics and rare-disease diagnostics, broadening the addressable proteomics market. Middle East and Africa show progressive adoption in tertiary hospitals, and Brazil leads South American uptake through vaccine-related proteome studies.

- Agilent Technologies

- Alamar Biosciences, Inc.

- Bioneer

- Bioinformatics Solutions Inc.

- Bio-Rad Laboratories

- Bruker

- Creative Proteomics

- Danaher

- Evosep

- GE Healthcare

- Illumina

- Merck

- Nautilus Biotechnology

- Olink Holding AB

- Oxford Nanopore Technologies

- Promega

- Proteome Factory AG

- Proteome Sciences PLC

- QIAGEN

- Revvity, Inc.

- Seer

- Shimadzu

- SomaLogic

- Thermo Fisher Scientific

- Waters Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for personalized & precision medicine

- 4.2.2 Increasing R&D expenditure and public funding

- 4.2.3 Rapid advances in high-throughput MS & LC-MS platforms

- 4.2.4 Growing adoption of proteomics in drug discovery pipelines

- 4.2.5 AI-enabled single-cell proteomics breakthroughs

- 4.2.6 Expanding use of proteomics in agri-genomics & food safety

- 4.3 Market Restraints

- 4.3.1 High capital & operating cost of instruments

- 4.3.2 Shortage of skilled bioinformaticians & proteomics experts

- 4.3.3 Data-analysis complexity & lack of workflow standards

- 4.3.4 Limited throughput for native membrane-protein studies

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Component

- 5.1.1 Instruments

- 5.1.2 Reagents

- 5.1.3 Software and Services

- 5.2 By Technology

- 5.2.1 Mass Spectrometry

- 5.2.2 Spectroscopy

- 5.2.3 Chromatography

- 5.2.4 Next-Generation Sequencing

- 5.2.5 Protein Microarrays

- 5.2.6 Microfluidics

- 5.2.7 X-ray Crystallography

- 5.2.8 Other Technologies

- 5.3 By Application

- 5.3.1 Drug Discovery & Development

- 5.3.2 Clinical Diagnostics

- 5.3.3 Biomarker Discovery

- 5.3.4 Precision and Personalized Medicine

- 5.3.5 Agricultural & Environmental Proteomics

- 5.3.6 Other Applications

- 5.4 By End-User

- 5.4.1 Pharmaceutical & Biotechnology Companies

- 5.4.2 Academic & Research Institutes

- 5.4.3 Contract Research Organizations

- 5.4.4 Other End-Users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Competitive Benchmarking

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Agilent Technologies Inc.

- 6.4.2 Alamar Biosciences, Inc.

- 6.4.3 Bioneer Corporation

- 6.4.4 Bioinformatics Solutions Inc.

- 6.4.5 Bio-Rad Laboratories Inc.

- 6.4.6 Bruker Corporation

- 6.4.7 Creative Proteomics

- 6.4.8 Danaher Corporation

- 6.4.9 Evosep

- 6.4.10 GE Healthcare

- 6.4.11 Illumina Inc.

- 6.4.12 Merck KGaA

- 6.4.13 Nautilus Biotechnology

- 6.4.14 Olink Holding AB

- 6.4.15 Oxford Nanopore Technologies

- 6.4.16 Promega Corporation

- 6.4.17 Proteome Factory AG

- 6.4.18 Proteome Sciences PLC

- 6.4.19 QIAGEN N.V.

- 6.4.20 Revvity, Inc.

- 6.4.21 Seer Inc.

- 6.4.22 Shimadzu Corporation

- 6.4.23 SomaLogic Inc.

- 6.4.24 Thermo Fisher Scientific Inc.

- 6.4.25 Waters Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment