|

시장보고서

상품코드

1850255

Wi-Fi 확장기 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Wi-Fi Range Extender - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

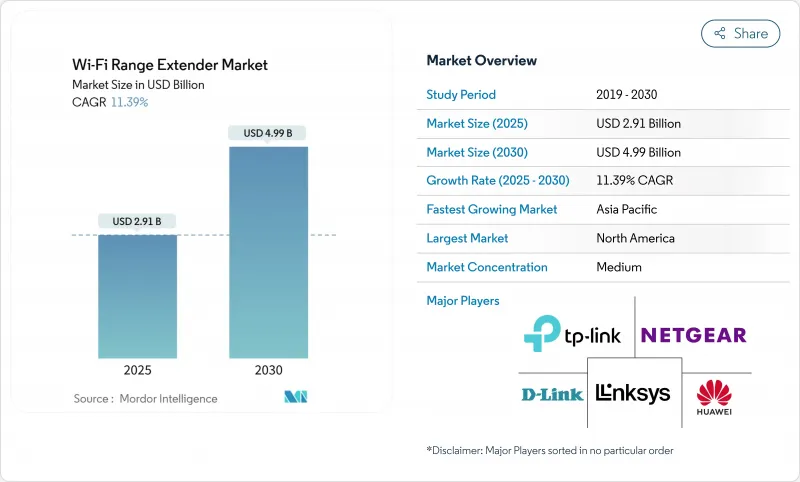

Wi-Fi 확장기 시장 규모는 2025년에 29억 1,000만 달러로 평가되었고 2030년에는 49억 9,000만 달러에 이를 것으로 예측되며, CAGR은 11.39%를 나타낼 전망입니다.

급증하는 스마트홈 보급, 하이브리드 근무 정책, 확대되는 규제 의무로 인해 무선 커버리지 요구사항이 표준 라우터의 범위를 훨씬 넘어설 정도로 확대되고 있습니다. 유럽연합의 2025년 사이버 보안 및 에너지 효율 규정을 충족하기 위한 제품 재설계는 개발 비용을 증가시키면서도 규정을 준수하는 브랜드에 보호 장벽을 구축하고 있습니다. 기업들은 이제 중단 없는 Wi-Fi 커버리지를 비즈니스 핵심 인프라로 간주하며, Wi-Fi 7로의 전환은 기존 기기들이 따라잡을 수 없는 성능 격차를 확대하고 있습니다. 동시에, 메시 네트워킹 솔루션과 반독점 조사가 Wi-Fi 범위 확장기 시장의 경쟁 전략을 재편하고 있습니다.

세계의 Wi-Fi 확장기 시장 동향 및 인사이트

스마트 홈 기기의 폭발적 증가

2024년에 연간 41억 대의 Wi-Fi 기기가 출하되면서 설치 기반이 211억 대로 증가했고, 단일 라우터의 커버리지 범위는 과부하 상태에 이르렀습니다. 다층 주택, 두꺼운 벽체, 확장되는 IoT 생태계로 인해 가정은 일관된 자동화 및 보안 성능을 위해 익스텐더 추가 설치가 불가피합니다. 기업 시설 역시 센서 기반 건물 관리 시스템을 위한 포괄적 커버리지가 필요해 동일한 밀집도를 보입니다. 지연 시간 급증 시 사용자 경험이 저하됨에 따라 가정과 기업 모두 커버리지 확장 솔루션에 추가 예산을 배정하고 있습니다.

BYOD와 하이브리드 워크 모델

호스피탈리티 체인 미첼스 앤 버틀러스(Mitchells & Butlers)는 영국 내 1,700개 장소에 8,000개의 액세스 포인트를 설치하며, 하이브리드 근무와 고객 기대가 Wi-Fi 커버리지를 확대하는 방식을 보여줍니다. 금융 및 의료 기업은 안전한 모바일 접속에 대한 규제적 요구에 직면하여, 구조화된 케이블링이 부족한 재활용 또는 임시 공간에서 전문적으로 관리되는 익스텐더 및 액세스 포인트 수요를 촉진합니다.

메시 Wi-Fi의 시장 잠식

TP-Link의 신규 Wi-Fi 7 메시 키트는 원활한 로밍과 실시간 관리를 '대중화'하며 단일 노드 확장기의 가치 제안을 약화시키고 있습니다. 기업은 통합 관리를 위해 메시를 선호하는 반면, 대중 시장 광고는 플러그 앤 플레이 이점을 강조하여 카테고리 경계 모호화와 가격 압박을 가속화하고 있습니다.

부문 분석

2030년까지 야외 설치는 13.30%의 연평균 성장률(CAGR)을 보이며, 이는 시립 Wi-Fi 및 캠퍼스 전체 커버리지 프로젝트를 반영합니다. 그러나 2024년 기준 실내 설치는 여전히 Wi-Fi 범위 확장기 시장 규모의 71%를 차지합니다. 경기장과 교통 허브에서는 밀집된 군중을 관리하기 위해 방향성 안테나가 장착된 내구성 강화형 확장기에 대한 수요가 증가하고 있습니다. 실내 부문 규모는 여전히 매출의 기반을 이루고 있으나, 많은 가정이 이미 최소 한 대 이상의 익스텐더를 보유함에 따라 물량 성장은 정체 국면에 접어들었습니다. 신흥 시장의 스마트홈 도입은 잔여 성장 동력을 제공하며, 가정이 연결형 보안 또는 엔터테인먼트 기기를 추가할 때 개조 수요가 급증합니다.

WiFi4EU 프로젝트와 프랑스 및 덴마크의 도시 안전 네트워크는 방수형 Wi-Fi 6 및 Wi-Fi 7 장비를 선호하여 공급업체 기회를 확대하고 있습니다. 이에 환경 내구성 전문성을 보유한 벤더들의 입지가 강화되고 있습니다. 반면 실내 장비 교체 주기는 비용 효율적인 Wi-Fi 5 또는 Wi-Fi 6 업그레이드에 의존하여 기존 칩 수요를 유지하고 있습니다.

익스텐더와 리피터는 2024년 매출의 54%를 차지하며 선두를 유지했으나, 기업들의 컨트롤러 기반 아키텍처로의 전환으로 액세스 포인트(AP) 시장이 연평균 16.90% 성장률을 보이고 있습니다. 기업들은 AP 중심 설계에 내장된 원격 펌웨어 관리 및 역할 기반 접근 보안 기능을 높이 평가합니다. 반면 소비자 채널에서는 빠른 해결을 위한 플러그 앤 플레이 방식의 리피터를 선호합니다.

스위스 소매업체 콘포라마(Conforama)는 아루바(Aruba) WLAN 솔루션을 도입해 옴니채널 재고 점검을 간소화했으며, 이는 중앙 집중식 AP 관리가 운영 마찰을 줄이는 방식을 보여줍니다. 반면, 세입자가 이더넷 백홀을 설치할 수 없는 아파트에서는 중가 리피터가 여전히 선호됩니다. AP와 메시 위성을 결합한 하이브리드 포트폴리오는 공급업체가 양측 수요를 모두 충족시켜 Wi-Fi 범위 확장기 시장의 다양성을 유지하는 데 도움이 됩니다.

Wi-Fi 확장기 시장 보고서는 유형(실내 Wi-Fi, 옥외 Wi-Fi), 제품(익스텐더 및 리피터, 액세스 포인트 등), 기술 표준(Wi-Fi 5(802.11ac), Wi-Fi 6/6E(802.11ax), 기타), 최종 사용자(가정용, 중소기업 등), 판매 채널(온라인(전자상거래, D2C), 오프라인 소매, 기타), 지역별로 분류됩니다.

지역 분석

북미는 성숙한 광대역 보급률과 초기 스마트홈 도입을 바탕으로 2024년 매출 점유율 40%를 유지했습니다. 포화 상태에 접어들며 성장은 완화되고 있으나, 하이브리드 근무 방식의 확산과 광범위한 단독주택이 교체 주기를 유지하고 있습니다. 캐나다의 농촌 지역 광대역 보조금과 멕시코의 디지털 포용성 지원금은 계속해서 판매량을 끌어올리고 있습니다. TP-Link 반독점 조사로 대표되는 미국의 규제 심사는 경쟁 역학을 재편할 수 있으나, 무선 연결에 대한 뿌리 깊은 의존도를 고려할 때 전체 수요에 타격을 주지는 않을 것입니다.

아시아태평양 지역은 2030년까지 연평균 13.80% 성장률로 가장 빠르게 성장하는 지역입니다. 중국의 거의 보편화된 FTTH(Fiber-to-the-Home)는 실내 Wi-Fi에 대한 기대를 높이지만, 두꺼운 콘크리트 벽과 같은 구조적 장벽이 신호 전파를 제한하여 익스텐더 판매를 촉진합니다. 인도의 스마트 시티 미션과 급속한 스마트폰 보급은 도시형 Wi-Fi 프로젝트를 촉진하는 반면, 일본과 한국은 공장 자동화와 몰입형 미디어에 초점을 맞춘 Wi-Fi 7 기업용 시범 사업을 주도하고 있습니다. 경제 발전 단계의 다양성으로 인해 공급업체들은 보급형 Wi-Fi 5와 플래그십 Wi-Fi 7 제품군을 모두 제공해야 합니다.

유럽은 선진적인 규제와 적당한 규모 성장이 공존합니다. 에너지 효율 및 사이버 보안 규정은 준수 비용을 증가시키지만 기존 업체에 유리한 진입 장벽을 구축합니다. 프랑스는 세계 최고 수준의 Wi-Fi 7 구축 밀도를 기록하며, 광섬유 속도 리더십을 사용자 경험 차별화로 전환하고 있습니다. 독일과 영국은 인더스트리 4.0 및 금융 서비스를 위한 안전한 기업용 WLAN을 강조하며 꾸준한 교체 주기를 창출합니다. WiFi4EU와 같은 EU 보조금은 농촌 및 지방자치단체 구축의 초석으로 남아 공공 부문의 지속적인 수요를 보장합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 스마트 홈 기기의 급증

- BYOD와 하이브리드 워크 모델

- 비디오 스트리밍 품질 경쟁

- Wi-Fi 7 업그레이드 주기 확산

- “어디서나 근무”를 위한 야외 커버리지 수요

- 건물 내 Wi-Fi 커버리지 의무화 규정 (EU)

- 시장 성장 억제요인

- 메시 Wi-Fi 시장 잠식

- 사이버 보안 및 개인정보 보호 우려

- 에너지 효율 규정 준수 비용

- 주요 업체에 대한 반독점 규제 심의

- 밸류체인 분석

- 규제 상황

- 기술 전망(Wi-Fi 6/6E/7, EasyMesh, MLO)

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 유형별

- 실내 Wi-Fi

- 야외 Wi-Fi

- 제품별

- 익스텐더와 리피터

- 액세스 포인트

- 전력선/Wi-Fi 콤보 유닛

- 고이득 안테나

- 기술 표준

- Wi-Fi 5(802.11ac)

- Wi-Fi 6/6E(802.11ax)

- Wi-Fi 7(802.11be)

- 최종 사용자별

- 주택

- 중소기업

- 대기업 및 캠퍼스

- 공공 및 지방자치단체

- 판매 채널별

- 온라인(전자상거래, D2C)

- 오프라인 소매

- B2B/기업 통합업체

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN

- 기타 아시아태평양

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- TP-Link Technologies Co. Ltd

- NETGEAR Inc.

- D-Link Corporation

- Linksys Group Inc.(벨킨)

- Huawei Technologies Co. Ltd

- Shenzhen Tenda Technology Co. Ltd

- AsusTek Computer Inc.

- Aruba Networks(HPE)

- Juniper Networks Inc.

- Ruckus Networks(CommScope)

- Motorola Solutions Inc.

- Ubiquiti Inc.

- Zyxel Communications Corp.

- Devolo GmbH

- Amped Wireless(Newo Corp.)

- Xiaomi Inc.

- Edimax Technology Co. Ltd

- Comfast(Shenzhen CF-Tech)

- Netis Systems Co. Ltd

- Belkin International

제7장 시장 기회와 장래의 전망

HBR 25.11.17The Wi-Fi range extender market size reached USD 2.91 billion in 2025 and is forecast to reach USD 4.99 billion by 2030, advancing at an 11.39% CAGR.

Surging smart-home adoption, hybrid-work policies and expanding regulatory mandates are extending wireless coverage requirements well beyond the reach of standard routers. Product redesigns to satisfy the European Union's 2025 cybersecurity and energy-efficiency rules are lifting development costs yet creating protective moats for compliant brands. Enterprises now regard uninterrupted Wi-Fi coverage as business-critical infrastructure, and the transition to Wi-Fi 7 is widening performance gaps that legacy devices cannot bridge. Simultaneously, mesh-networking solutions and antitrust investigations are reshaping competitive tactics in the Wi-Fi range extender market.

Global Wi-Fi Range Extender Market Trends and Insights

Smart-home Device Explosion

Annual shipments of 4.1 billion Wi-Fi devices in 2024 pushed the installed base to 21.1 billion and overloaded single-router footprints. Multi-story homes, thick walls and growing IoT ecosystems force households to add extenders for consistent automation and security performance. Corporate facilities mirror this density, requiring blanket coverage for sensor-driven building-management systems. As user experience degrades when latency spikes, both homeowners and enterprises allocate incremental budgets to coverage extension solutions.

BYOD and Hybrid Work Models

Hospitality chain Mitchells & Butlers installed 8,000 access points across 1,700 UK venues, underscoring how hybrid labor and guest expectations broaden Wi-Fi footprints. Finance and healthcare firms face regulatory imperatives for secure mobile access, driving demand for professionally managed extenders and access points in re-purposed or temporary spaces that lack structured cabling.

Mesh-Wi-Fi Cannibalisation

TP-Link's new Wi-Fi 7 mesh kits "democratize" seamless roaming and real-time management, eroding the value proposition of single-node extenders.Enterprises favor mesh for unified control while mass-market advertising stresses plug-and-play benefits, accelerating category blurring and price compression.

Other drivers and restraints analyzed in the detailed report include:

- Video-streaming Quality Race

- Wi-Fi 7 Upgrade Cycle Pull-through

- Cyber-security and Privacy Fears

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Outdoor deployments are growing at a 13.30% CAGR through 2030, reflecting municipal Wi-Fi and campus-wide coverage projects, yet indoor installs still account for 71% of the Wi-Fi range extender market size in 2024. Stadiums and transport hubs increasingly demand ruggedized extenders with directional antennas to manage dense crowds. The indoor segment's scale continues to anchor revenue, but volume growth is plateauing as many homes already own at least one extender. Smart-home adoption in emerging markets provides residual tailwinds, and retrofit demand spikes when families add connected security or entertainment gadgets.

Municipal projects under the WiFi4EU banner and city safety networks across France and Denmark favor weather-sealed Wi-Fi 6 and Wi-Fi 7 units, broadening supplier opportunities. Vendors with environmental-hardening expertise therefore gain traction. In contrast, indoor refresh cycles hinge on cost-effective Wi-Fi 5 or Wi-Fi 6 upgrades, sustaining legacy chip demand.

Extenders and repeaters retained 54% revenue leadership in 2024, yet enterprise migrations toward controller-based architectures are pushing access points at a 16.90% CAGR. Businesses appreciate remote firmware orchestration and role-based access security embedded in AP-centric designs. Consumer channels, however, favor plug-and-play repeaters for quick fixes.

Retailer Conforama Switzerland adopted Aruba WLAN solutions to streamline omnichannel inventory checks, illustrating how centralized AP management reduces operational friction. Conversely, mid-priced repeaters remain preferred in apartments where tenants cannot install Ethernet backhaul. Hybrid portfolios that couple APs with mesh satellites help vendors address both camps, keeping the Wi-Fi range extender market diversified.

The Wi-Fi Range Extender Market Report is Segmented by Type (Indoor Wi-Fi and Outdoor Wi-Fi), Product (Extenders and Repeaters, Access Points, and More), Technology Standard (Wi-Fi 5 [802. 11ac], Wi-Fi 6 / 6E [802. 11ax], and More), End User (Residential, Small and Medium Enterprises, and More), Sales Channel (Online [e-Commerce, D2C], Offline Retail, and More), and Geography.

Geography Analysis

North America retained 40% revenue share in 2024, building on mature broadband penetration and early smart-home uptake. Growth is moderating as saturation sets in, yet hybrid-work adoption and extensive single-family housing sustain replacement cycles. Canada's rural broadband subsidies and Mexico's digital-inclusion grants continue to lift volume. U.S. regulatory scrutiny, exemplified by the TP-Link antitrust probe, may re-shape competitive dynamics but is unlikely to dent overall demand given ingrained dependence on wireless connectivity.

Asia Pacific is the fastest-growing region with a 13.80% CAGR through 2030. China's near-universal fiber-to-the-home creates high expectations for in-unit Wi-Fi, yet structural barriers such as thick concrete walls constrain signal propagation, boosting extender sales. India's Smart Cities Mission and rapid smartphone adoption propel municipal Wi-Fi projects, while Japan and South Korea spearhead Wi-Fi 7 enterprise pilots focused on factory automation and immersive media. The diversity of economic stages requires suppliers to offer both entry-level Wi-Fi 5 and flagship Wi-Fi 7 skus.

Europe blends advanced regulation with moderate volume growth. Energy-efficiency and cybersecurity rules raise compliance costs but erect entry barriers that benefit incumbents. France posts the world's highest Wi-Fi 7 deployment density, translating fiber speed leadership into user-experience differentiation. Germany and the UK emphasize secure enterprise WLANs for Industry 4.0 and financial services, generating steady refresh cycles. EU subsidies such as WiFi4EU remain a cornerstone of rural and municipal roll-outs, ensuring durable public-sector demand.

- TP-Link Technologies Co. Ltd

- NETGEAR Inc.

- D-Link Corporation

- Linksys Group Inc. (Belkin)

- Huawei Technologies Co. Ltd

- Shenzhen Tenda Technology Co. Ltd

- AsusTek Computer Inc.

- Aruba Networks (HPE)

- Juniper Networks Inc.

- Ruckus Networks (CommScope)

- Motorola Solutions Inc.

- Ubiquiti Inc.

- Zyxel Communications Corp.

- Devolo GmbH

- Amped Wireless (Newo Corp.)

- Xiaomi Inc.

- Edimax Technology Co. Ltd

- Comfast (Shenzhen CF-Tech)

- Netis Systems Co. Ltd

- Belkin International

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Smart-home device explosion

- 4.2.2 BYOD and hybrid work models

- 4.2.3 Video-streaming quality race

- 4.2.4 Wi-Fi 7 upgrade cycle pull-through

- 4.2.5 "Work-from-anywhere" outdoor coverage needs

- 4.2.6 Mandatory in-building Wi-Fi coverage codes (EU)

- 4.3 Market Restraints

- 4.3.1 Mesh-Wi-Fi cannibalisation

- 4.3.2 Cyber-security and privacy fears

- 4.3.3 Energy-efficiency compliance costs

- 4.3.4 Antitrust scrutiny on leading vendors

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook (Wi-Fi 6/6E/7, EasyMesh, MLO)

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Indoor Wi-Fi

- 5.1.2 Outdoor Wi-Fi

- 5.2 By Product

- 5.2.1 Extenders and Repeaters

- 5.2.2 Access Points

- 5.2.3 Powerline/Wi-Fi Combo Units

- 5.2.4 High-gain Antennas

- 5.3 By Technology Standard

- 5.3.1 Wi-Fi 5 (802.11ac)

- 5.3.2 Wi-Fi 6 / 6E (802.11ax)

- 5.3.3 Wi-Fi 7 (802.11be)

- 5.4 By End User

- 5.4.1 Residential

- 5.4.2 Small and Medium Enterprises

- 5.4.3 Large Enterprises and Campuses

- 5.4.4 Public and Municipal

- 5.5 By Sales Channel

- 5.5.1 Online (e-commerce, D2C)

- 5.5.2 Offline Retail

- 5.5.3 B2B/Enterprise Integrators

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 ASEAN

- 5.6.4.6 Rest of Asia Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 TP-Link Technologies Co. Ltd

- 6.4.2 NETGEAR Inc.

- 6.4.3 D-Link Corporation

- 6.4.4 Linksys Group Inc. (Belkin)

- 6.4.5 Huawei Technologies Co. Ltd

- 6.4.6 Shenzhen Tenda Technology Co. Ltd

- 6.4.7 AsusTek Computer Inc.

- 6.4.8 Aruba Networks (HPE)

- 6.4.9 Juniper Networks Inc.

- 6.4.10 Ruckus Networks (CommScope)

- 6.4.11 Motorola Solutions Inc.

- 6.4.12 Ubiquiti Inc.

- 6.4.13 Zyxel Communications Corp.

- 6.4.14 Devolo GmbH

- 6.4.15 Amped Wireless (Newo Corp.)

- 6.4.16 Xiaomi Inc.

- 6.4.17 Edimax Technology Co. Ltd

- 6.4.18 Comfast (Shenzhen CF-Tech)

- 6.4.19 Netis Systems Co. Ltd

- 6.4.20 Belkin International

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment