|

시장보고서

상품코드

1850341

수의 수술기구 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Veterinary Surgical Instruments - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

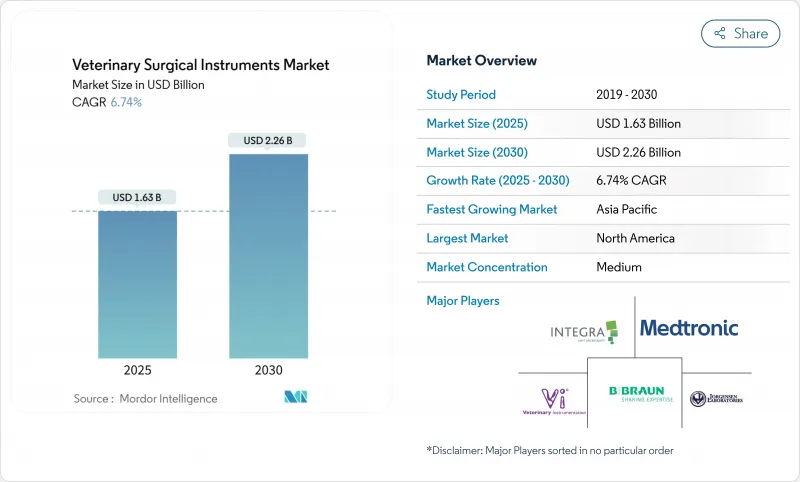

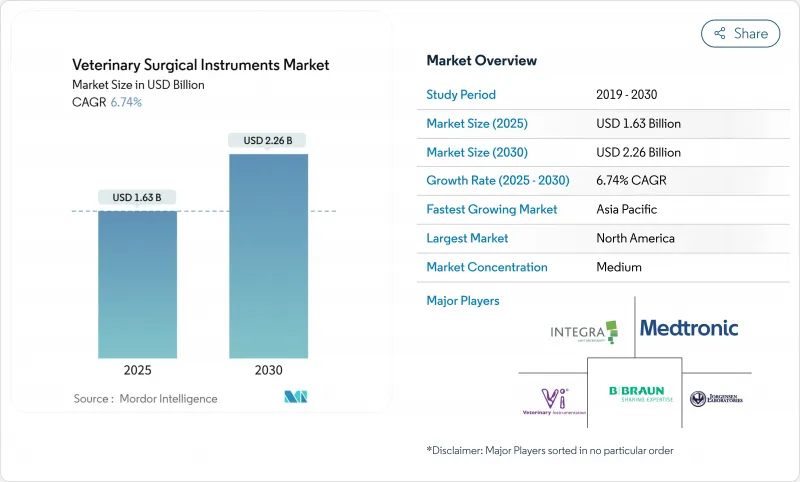

수의 수술기구 시장은 2025년에 16억 3,000만 달러로 평가되었으며, 2030년에 22억 6,000만 달러에 이를것으로 예측되며, CAGR은 6.74%를 나타낼 전망입니다.

반려동물 수요 증가, 전기수술 분야의 급속한 혁신, 확대되는 반려동물 보험 적용 범위가 수익 성장을 주도하고 있습니다. 정밀 기반 프로토콜, 특히 최소 침습 수술은 병원들이 고해상도 영상 장비, 양극성 전기수술, 3D 프린팅 정형외과 임플란트로의 업그레이드를 촉진하고 있습니다. 아시아태평양 지역은 가처분 소득 증가, 정부 주도 인프라 프로그램, 도시 반려동물 인구 증가로 가장 강력한 성장 모멘텀을 보이고 있습니다. 정형외과 수술은 맞춤형 임플란트와 AI 기반 계획의 지원으로 차세대 성장 동력으로 부상하고 있습니다. 그러나 높은 자본 비용과 전 세계적으로 인증된 전문의 부족은 도입률을 위협하며, 신규 장비에 대한 교육과 유연한 자금 조달의 중요성을 강조합니다.

세계의 수의 수술기구 시장 동향 및 인사이트

동물의 최소 침습 수술 동향

복강경 및 관절경 시술 수요가 수의 수술기구 시장을 변화시키고 있습니다. 트로카, 캐뉼라, 고화질 내시경이 개복 수술을 대체할 경우 회복 기간이 최대 65% 단축되고 합병증 발생률이 감소합니다. 미국 전문 클리닉은 중성화 수술의 42%에서 최소 침습 수술(MIS)을 도입했으며, 정형외과 전문의의 56%는 관절 진단을 정밀화하기 위해 관절경을 활용합니다. 회복 기간 단축을 강조하는 클리닉은 수술 수락률이 높아지며, 이로 인해 유통업체들은 MIS 준비 키트 공급을 우선시하고 있습니다. 제조사들은 90분 이상 지속되는 시술 중 외과의 피로를 최소화하는 인체공학적 기구 핸들로 대응하고 있습니다.

반려동물 소유율 및 반려동물 보험 보급률 증가

2024년 기준 미국 9,400만 가구가 반려동물을 키웠으며, 이 중 440만 명의 소유자가 동물 보험에 가입해 보험 가입 반려동물당 수의학 지출이 40% 증가했습니다. 이러한 행동은 정형외과적 수복, 심장 중재술, 첨단 치과 시술 건수를 직접적으로 끌어올린다. 한편 보험사는 인증 기구를 사용하는 병원에 보상금을 지급함으로써 조달에 영향을 미치며, 간접적으로 프리미엄 기구 구매를 촉진합니다. 런던, 뉴욕, 상하이 같은 도시는 고가 수요가 집중된 클러스터를 형성하여 공급업체가 AI 기반 전기 수술 플랫폼을 광범위하게 출시하기 전에 시범 운영할 수 있게 합니다.

첨단 장비의 도입을 막는 고비용

프리미엄 전기 수술 타워는 연기 배출 장치 및 양극성 집게와 함께 번들로 제공될 경우 50,000달러를 초과할 수 있습니다. 유지보수 계약, 팁 교체, 기술자 교육은 총 소유 비용을 기본 메스 세트보다 훨씬 높게 끌어올려 고급 의뢰 병원과 농촌 진료소 간의 기술 격차를 확대합니다. 임대, 사용량 기반 요금제, 리퍼비시드 옵션이 주목받고 있지만 인도, 브라질, 동남아시아에서는 도입이 여전히 고르지 않습니다.

부문 분석

봉합사 및 스테이플러는 2024년 매출의 33.7%를 차지하며 여전히 우위를 점하고 있습니다. 그러나 전기 수술 시스템은 9.80%의 연평균 성장률(CAGR)로 가장 빠르게 성장하는 분야로, 2030년까지 수의 수술기구 시장 규모에 약 2억 5천만 달러를 추가할 전망입니다. 수의 수술기구 시장은 인체공학적으로 설계된 핸들과 풋 스위치 통합으로 2시간에 걸친 종양 절제술 시 피로를 줄여주는 장점을 제공합니다. 휴대용 가위, 바늘 집게, 롱게르는 여전히 필수적이지만, 수요는 이제 날카로움을 오래 유지하는 고급 강종과 미세 톱니 모양 날에 집중되고 있습니다.

미국과 호주의 수의 교육 병원은 개를 대상으로 한 경피적 승모판 수리술과 같은 심장학 분야 최초 사례를 발표하며 전기 수술의 확대되는 임상 적용 범위를 입증했습니다. 이러한 근거는 개인 동물병원들이 초급형 단극식 대신 중급형 양극식 발생기를 선택하도록 유도합니다. 공급업체들은 트로카 세트와 연기 추출기를 묶어 판매함으로써 2024년부터 2025년 사이 동물병원당 평균 판매액을 28% 증가시킬 전망입니다.

지역 분석

북미 지역은 2024년 글로벌 매출의 38.0%를 차지했습니다. AI 지원 영상 기술의 조기 도입과 반려동물 보험 문화로 인해 동물병원은 10년에 한 번이 아닌 5-7년마다 장비를 업그레이드할 수 있습니다. 미국 수의사의 30%는 이미 진단 과정에서 어떤 형태의 인공지능을 활용하고 있으며, 이는 수술 계획 수립에 활용되는 데이터 수집량을 증가시킵니다. 그럼에도 중서부 및 산악 지역에서는 수의사 부족이 심각하여 진료 부담이 가중되고, 복잡한 시술을 수행하는 일반 개업의들을 위한 원격 멘토링이 확대되고 있습니다.

아시아태평양 지역은 연평균 복합 성장률(CAGR) 10.23%로 가장 빠르게 성장하는 지역입니다. 중국 2025 의료기구 박람회에서 인공지능 통합 정형외과 로봇이 소개되며 고정밀 시스템에 대한 투자자 관심이 고조되었습니다. 인도 민간 병원 체인들은 장비 비용 분산을 위한 구독형 서비스 계약을 실험 중입니다. 지방 정부는 인수공통전염병 감시와 수의병원 확장을 연계하여 2선 도시의 오토클레이브 및 내시경 지원금을 해제하고 있습니다. 이러한 정책으로 유통망이 확대되고 핵심 부품 납기 시간이 단축되고 있습니다.

유럽은 인증된 기구 추적성과 멸균 재처리 기록을 요구하는 엄격한 복지 규정을 유지합니다. CVS 그룹의 2024년 5,470만 달러 규모 업그레이드 투자는 해당 지역이 추적 가능한 로트 번호가 있는 고성능 합금으로 재고를 전환하려는 의지를 보여줍니다. 한편, 라틴 아메리카와 중동·아프리카 지역은 반려동물 소유 증가로 수요가 가속화되고 있습니다. 브라질이 수술기구 수입을 주도하는 반면, 걸프 시장은 말 수술을 우선시하여 초장형 뼈 플레이트 및 후두경 장치에 대한 요구 사항을 높이고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 동물에서 최소 침습 수술 동향

- 반려동물 사육 증가와 반려동물 보험의 보급률

- 동물 질병 부담 증가 및 중성화 수술 프로그램 확대가 수술 건수 증가 촉진

- 동물 의료를 위한 연구개발(R&D) 지출 및 제품 혁신 증가

- 정부 정책 및 동물 복지 규정과 연계된 수의 의료 인프라 확장

- 프리미엄 기구 예산 확보를 위한 클리닉 기업화

- 시장 성장 억제요인

- 고급 수술기구와 수술의 높은 비용

- 인정 수의사의 부족

- 엄격한 규제 승인

- 소규모 병원의 제한된 멸균 인프라로 인한 복잡한 재사용 수술 도구 도입 제약

- 규제와 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 봉합사 및 스테이플러

- 휴대용

- 메스

- 집게

- 가위

- 견인기

- 전기 수술기구

- 기타 제품

- 트로카 및 캐뉼라

- 흡입 및 세척

- 휴대용

- 동물별

- 반려동물

- 개

- 고양이

- 가축

- 소

- 돼지

- 가금

- 반려동물

- 용도별

- 연조직 수술

- 치과 수술

- 정형외과

- 안과 수술

- 기타 용도

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- B. Braun SE

- Medtronic

- Integra LifeSciences Corporation

- Jorgensen Laboratories

- Kshama Surgical

- Accesia AB

- GerVetUSA

- Arch Medical Solutions Company(gSource)

- Orthomed(UK) Ltd

- Johnson and Johnson

- Eickemeyer

- World Precision Instruments

- Dentalaire International

- SAI Infusion Technologies

- Granim Healthcare(DRE Veterinary)

- Amerisource Bergen Corporation

- Surgical Holdings

- Aspen Surgical Products, Inc.

- IndoSurgicals Private Limited

- Rajindra Surgical Industries

제7장 시장 기회와 장래의 전망

HBR 25.11.19The veterinary surgical instruments market is valued at USD 1.63 billion in 2025 and is forecast to reach USD 2.26 billion by 2030, advancing at a 6.74% CAGR.

Companion-animal demand, rapid innovations in electrosurgery, and expanding pet insurance coverage are propelling revenue. Precision-based protocols, particularly minimally invasive surgery, are pushing clinics to upgrade to high-definition visualization, bipolar electrosurgery, and 3D-printed orthopedic implants. Asia-Pacific shows the strongest momentum thanks to rising disposable income, government-led infrastructure programs, and a growing urban pet population. Orthopedic surgery is emerging as the next growth engine, supported by custom implants and AI-guided planning. Still, high capital costs and a global shortfall of board-certified surgeons threaten adoption rates, underscoring the importance of training and flexible financing for new equipment.

Global Veterinary Surgical Instruments Market Trends and Insights

Minimally-invasive surgery trend in animals

Demand for laparoscopic and arthroscopic procedures is transforming the veterinary surgical instruments market. Recovery times fall by up to 65% and complication rates decline when trocars, cannulas, and HD endoscopes replace open techniques. U.S. specialty clinics report 42% MIS adoption for spays, while 56% of orthopedic specialists deploy arthroscopy to refine joint diagnostics. Clinics that market shorter convalescence periods see higher case acceptance, pushing distributors to prioritize MIS-ready kits. Manufacturers respond with ergonomic instrument handles that minimize surgeon fatigue during procedures lasting beyond 90 minutes.

Rising pet ownership and pet-insurance penetration

Ninety-four million U.S. households kept pets in 2024, and 4.4 million of those owners insured their animals, triggering 40% higher veterinary outlays per insured pet. This behavior directly lifts procedure volumes for orthopedic repair, cardiac interventions, and advanced dentistry. Insurers, meanwhile, influence procurement by reimbursing clinics that use certified devices, indirectly accelerating premium instrument purchases. Cities such as London, New York, and Shanghai form dense clusters of high-end demand, allowing suppliers to pilot AI-enabled electrosurgery platforms before wider rollout.

High costs limiting adoption of advanced instruments

Premium electrosurgery towers can top USD 50,000 when bundled with smoke evacuators and bipolar forceps. Maintenance contracts, tip replacements, and technician training push total cost of ownership far above basic scalpel sets, widening the technology gap between high-end referral hospitals and rural practices. Leasing, pay-per-use, and refurbished options are gaining traction, but uptake remains uneven in India, Brazil, and South-East Asia.

Other drivers and restraints analyzed in the detailed report include:

- Growing disease burden and spay-neuter programs

- Intensifying R&D and product innovation

- Shortage of board-certified veterinary surgeons

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Sutures and staplers continued to command 33.7% of 2024 sales. Yet electrosurgery systems are the fastest climber with a 9.80% CAGR that will add roughly USD 250 million to the veterinary surgical instruments market size by 2030. The veterinary surgical instruments market benefits from ergonomically contoured handles and foot-switch integration that lessen fatigue during two-hour tumor resections. Handheld scissors, needle holders, and rongeurs remain essential, but demand now centers on premium steel grades and micro-serrated edges that prolong sharpness.

Veterinary teaching hospitals in the United States and Australia have publicized cardiology firsts such as transcatheter mitral-valve repair in dogs, demonstrating electrosurgery's widening clinical scope. This evidence base nudges private clinics toward mid-range bipolar generators instead of entry-level monopolar units. Suppliers bundle trocar sets and smoke extractors, boosting average sale value per clinic by 28% between 2024 and 2025.

The Veterinary Surgical Instruments Market Report is Segmented by Product (Sutures and Staplers, Handheld Instruments, Electro-Surgery Instruments, Other Products), Animal (Companion Animals and Farm Animals), Application (Soft-Tissue Surgery, Dental Surgery, Orthopedic Surgery, Ophthalmic Surgery, and Other Applications), and Geography (North America, Europe and More). The Market and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 38.0% of global sales in 2024. Early adoption of AI-assisted imaging and a pet-insurance culture enable clinics to upgrade every five to seven years instead of once a decade. Thirty percent of U.S. veterinarians already use some form of artificial intelligence during diagnosis, increasing data capture that feeds back into surgical planning. Nonetheless, the veterinarian shortage is acute in Midwest and Mountain states, stretching case loads and pushing tele-mentoring for general practitioners undertaking complex procedures.

Asia-Pacific is the fastest-growing territory at 10.23% CAGR. China's 2025 medical-device fair introduced an AI-integrated orthopedic robot, reinforcing investor appetite for high-precision systems. India's private chain hospitals are experimenting with subscription-based service contracts to spread equipment costs. Regional governments link zoonotic-disease surveillance with veterinary-hospital expansion, unlocking grants for autoclaves and endoscopes in tier-two cities. These policies are broadening distributor networks and compressing delivery times for critical parts.

Europe maintains stringent welfare regulations that require certified instrument traceability and sterile reprocessing logs. The CVS Group's USD 54.7 million spend on upgrades in 2024 underlines the region's willingness to rotate stock toward high-performance alloys with traceable lot numbers. Meanwhile, Latin America and the Middle East and Africa show accelerating demand as pet ownership climbs. Brazil leads surgical-instrument imports, while Gulf markets prioritize equine surgery, raising requirements for extra-long bone plates and laryngoscopic devices.

- B. Braun

- Medtronic

- Integra LifeSciences

- Jorgensen Laboratories

- Kshama Surgical

- Accesia AB

- GerVetUSA

- Arch Medical Solutions Company (gSource)

- Orthomed (UK) Ltd

- Johnson & Johnson

- Eickemeyer Veterinary Equipment

- World Precision Instruments

- Dentalaire International

- SAI Infusion Technologies

- Granim Healthcare (DRE Veterinary)

- Amerisource Bergen Corporation

- Surgical Holdings

- Aspen Surgical Products, Inc.

- IndoSurgicals Private Limited

- Rajindra Surgical Industries

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Minimally-invasive surgery trend in Animals

- 4.2.2 Rising Pet Ownership and Pet Insurance Penetration

- 4.2.3 Rising Animal Disease burden and spay/neuter programs are boosting surgical volumes

- 4.2.4 Increasing R&D Expenditure and Product Innovation for Animal Healthcare

- 4.2.5 Expansion of Veterinary healthcare Infrastructure Coupled with Government Inititiaves and Animal Welfare Regulations

- 4.2.6 Clinic corporatization unlocking budgets for premium instruments

- 4.3 Market Restraints

- 4.3.1 High Cost of Advanced Surgical Instruments and Procedures

- 4.3.2 Shortage of board-certified veterinary surgeons

- 4.3.3 Stringent Regulatory Approvals

- 4.3.4 Limited sterilization infrastructure in smaller clinics curbs adoption of complex reusable surgical tools

- 4.4 Regulatory and Technological Outlook

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value-USD)

- 5.1 Sutures and Staplers

- 5.1.1 Handheld Instruments

- 5.1.1.1 Scalpels

- 5.1.1.2 Forceps

- 5.1.1.3 Scissors

- 5.1.1.4 Retractors

- 5.1.2 Electro-surgery Instruments

- 5.1.3 Other Products

- 5.1.3.1 Trocars and Cannulas

- 5.1.3.2 Suction and Irrigation

- 5.1.1 Handheld Instruments

- 5.2 By Animal

- 5.2.1 Companion Animals

- 5.2.1.1 Dogs

- 5.2.1.2 Cats

- 5.2.2 Farm Animals

- 5.2.2.1 Bovine

- 5.2.2.2 Swine

- 5.2.2.3 Poultry

- 5.2.1 Companion Animals

- 5.3 By Application

- 5.3.1 Soft-Tissue Surgery

- 5.3.2 Dental Surgery

- 5.3.3 Orthopedic Surgery

- 5.3.4 Ophthalmic Surgery

- 5.3.5 Other Applications

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 B. Braun SE

- 6.3.2 Medtronic

- 6.3.3 Integra LifeSciences Corporation

- 6.3.4 Jorgensen Laboratories

- 6.3.5 Kshama Surgical

- 6.3.6 Accesia AB

- 6.3.7 GerVetUSA

- 6.3.8 Arch Medical Solutions Company (gSource)

- 6.3.9 Orthomed (UK) Ltd

- 6.3.10 Johnson and Johnson

- 6.3.11 Eickemeyer

- 6.3.12 World Precision Instruments

- 6.3.13 Dentalaire International

- 6.3.14 SAI Infusion Technologies

- 6.3.15 Granim Healthcare (DRE Veterinary)

- 6.3.16 Amerisource Bergen Corporation

- 6.3.17 Surgical Holdings

- 6.3.18 Aspen Surgical Products, Inc.

- 6.3.19 IndoSurgicals Private Limited

- 6.3.20 Rajindra Surgical Industries

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment