|

시장보고서

상품코드

1851088

수막염균 백신 시장 : 시장 점유율 분석, 산업 동향 & 통계, 성장 예측(2025-2030년)Meningococcal Vaccines - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

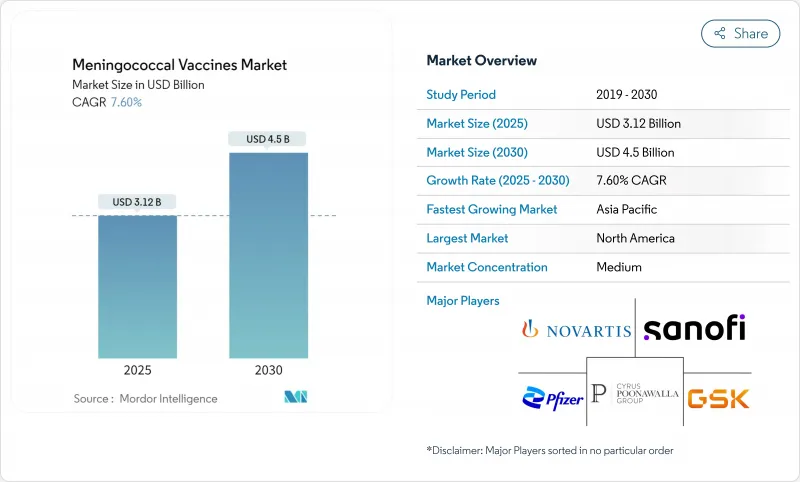

수막염균 백신 시장의 2025년 시장 규모는 31억 2,000만 달러로 추정되며, 2030년에는 45억 달러에 이르고, CAGR 7.60%를 나타낼 것으로 예측됩니다.

혈청군 A, B, C, W, Y를 결합한 5가 플랫폼은 제품 전략을 재정의하고 다회 주사 일정을 단일 주사로 압축하며 기존 1가 및 4가 브랜드에서 수요를 전환합니다. GSK는 2025년 2월 화이자가 발매한 펜브라야에 이어 5성분 주사약 펜멘비에서 처음으로 FDA 승인을 받았습니다. 제조업체는 현재 혼합 백신의 프리미엄 가격의 매력과 레거시 라인의 자기 잠식 간에 균형을 노리고 있습니다. 지역별로는 북미가 구매력을 유지하고 있지만 국가 예방접종 프로그램의 확대나 나이지리아에서의 실온 안정형 Men5CV와 같은 라스트 원 마일 딜리버리 모델의 대두를 배경으로 아시아태평양이 가장 빠르게 판매량을 늘리고 있습니다. 바이오테크놀러지 진출기업이 민간과 정부의 파트너십과 기술 이전을 활용하여 시장 투입까지의 시간을 단축하고 있기 때문에 경쟁의 격렬함이 증가하고 있습니다.

세계의 수막염균 백신 시장의 동향과 인사이트

예방접종 프로그램 증가와 정부의 대처

정부가 자금을 제공하는 백신 전개는 수막염균 예방접종을 정기적인 스케줄과 여행 요건에 통합함으로써 수요를 확대하고 있습니다. 중국의 국가예방접종 프로그램은 수막염균 결합형 제제를 포함한 WHO 승인의 백신 몇종을 전액 조성의 상태로 이행시켜 농촌에서의 접종 기회를 확대했습니다. 프랑스는 2024년 '2030년까지 수막염 박멸' 로드맵에 대한 WHO 최초의 하이레벨 포럼을 개최하여 저렴한 공급과 감시의 조화에 대한 새로운 목표를 설정했습니다. 사우디아라비아는 하지와 움라 순례자들에게 MenACWY의 증명을 의무화하고 있으며 외국인 여행자의 준수율은 54%에 불과하지만 세계적인 수요를 자극하고 있습니다. 이러한 협력 프로그램을 통해 예측 가능한 입찰 주기를 만들고 제조업체가 배치 크기를 최적화하고 수익을 예측할 수 있습니다.

민간과 정부의 파트너십 증가로 개발 비용 저하

백신 개발자들은 학술적 발견과 산업적 스케일업을 융합시킨 제휴를 통해 공동출자를 획득하는 경우가 늘고 있습니다. Serum Institute of India는 옥스포드 대학에서 키메라 단백질의 MenB 후보를 승인받고 Gavi 자격 시장에 저비용 부스터를 공급하는 것을 목표로 하고 있습니다. Gavi의 아프리카 백신 제조 액셀러레이터는 2024년 12억 달러를 현지 생산에 충당한 것으로 나타났으며 이 시프트는 장기 공급 안정화와 리드 타임 단축으로 이어질 것으로 기대되고 있습니다. PATH와 혈청연구소(Serum Institute)의 협력을 통해 Men5CV는 유럽과 미국의 벤치마크보다 높은 1회당 약 3달러로 시장에 출시되었습니다. 이러한 모델에서는 R&D 투자가 재분배되기 때문에 중소형 생명공학 기업은 엄청난 자본 지출 없이 신규 플랫폼을 개발할 수 있습니다.

콜드체인 저장 및 공급 물류의 높은 비용

전체 범위의 냉장은 특히 주위 온도가 30°C를 초과하는 경우 여전히 주요 비용 요인입니다. 네팔의 현장 조사에서 보냉 운송업체 1사당 평균 선적액은 1,704달러로 3분의 1 가까이가 운송 중에 동결로 인한 피해를 입었다고 보고되었습니다. 인도의 온도 관리 체인의 시험 운영은 물류비를 1회당 0.063달러에서 0.026달러로 줄였지만 자본 업그레이드와 대규모 교육이 필요했습니다. 능동형 보온 컨테이너를 통한 무인 항공기 물류는 유망하지만 규제 클리어런스 장애물 및 페이로드 용량 제한에 직면하고 있습니다. 인프라 격차가 계속되면 육상비 상승과 정기적인 재고 부족으로 인한 적시 공급이 제한됩니다.

부문 분석

4가 제제의 2024년 매출은 53.98%에 이르렀으며 북미와 유럽의 부스터 프로그램에서 우위를 유지하고 있습니다. 이 리더십은 수년간의 임상적 익숙성, 광범위한 보험 적용, 견고한 입찰 프레임워크가 수막염균 백신 시장을 지원하고 있음을 반영합니다. 그러나 목표를 좁힌 예방과 저비용이 평가되고 있는 2가 솔루션은 2030년까지의 CAGR 8.24%를 나타낼 전망입니다. 5가 백신 파이프라인은 공급업체가 5가지 주요 혈청군을 모두 한 번에 포함시켜야 하기 때문에 가장 빠르게 성장하는 '기타' 범주입니다.

5가 백신의 승인에 따른 기세는 구조적인 축으로 작용합니다. 간소화된 일정과 보다 광범위한 균주의 조합으로 미국의 일부 주들은 학교 요구사항을 재검토하게 되었습니다. 초기 모델링은 2028년까지 5가 백신이 4가 백신 수요의 거의 30%를 대체할 것으로 예상되어 수막염균 백신 시장의 수익 분포가 재구성될 가능성을 시사합니다. CanSino Biologics사는 2023년 2가 제제 매출액을 5억 6,170만 위안(7,850만 달러)으로 연간 266% 증가시켜 이 변화를 부각시켰습니다.

컨쥬게이트 제형은 2024년에 46.47%의 점유율을 차지하였으며, 소아용 프로토콜에 적합한 면역원성 및 집단 면역의 지속적인 이점에 의해 지원됩니다. 컨쥬게이트 백본과 단백질 항원을 조합한 복합형 제제는 CAGR 8.39%를 기록하여 수막염균 백신 시장 규모에서 보다 이익률이 높은 SKU공급 능력을 확대하는 추세에 있습니다. 다당류 주사제는 비용 우위성과 신속한 출시 일정으로 팬데믹 시 전략적 역할을 담당하고 있습니다.

최첨단 컨쥬게이션 화학물질은 5개의 다당체 부분을 돌연변이 디프테리아 단백질에 융합시켜 항원의 완전성을 유지하면서 10년 이상 기억 반응을 지속시킵니다. Men5CV의 실온 프로파일은 특히 아프리카에서 Gavi가 자금을 제공하는 활동에 유통 상의 이점을 제공합니다. 외막 소포(OMV)와 단백질 나노입자 구조물은 개발 도중에 있지만, 내열성과 교차 방어가 기대되며, 수막염균 백신 산업의 미래 툴킷을 확장할 수 있습니다.

지역 분석

북미는 보편적인 스케줄링, 광범위한 보험자 커버, 신속한 아웃브레이크 검출 시스템을 배경으로 2024년 세계 매출의 40.41%를 창출했습니다. 미국에서는 11-12세와 16세의 2회 MenACWY 시리즈를 실시하고, 고위험 집단에는 MenB를 추천하고 있습니다. FDA에 의한 펜멘비의 승인은 처방 검토와 민간 지급자와의 협상을 촉진하고 5가 백신의 보급을 가속시킬 수 있을 것으로 기대됩니다. 최근 발생한 ST-1466의 집단 감염은 노인에게 취약성이 남아 있음을 부각시키고 부스터의 대상 연령을 확대하는 논의를 촉구하고 있습니다.

유럽에서는 혈청군의 동향은 역동적이지만 백신접종은 성숙하고 있습니다. 2022년 감시에서는 1,149건의 침습적 사례가 발견되었으며, 그 중 혈청군 B는 62%로 여전히 우세했습니다. 프랑스가 WHO의 수막염 정상 회담을 주최함으로써 지역 협력이 다시 활성화되고 독일이 MenB를 정기적인 권장 사항에 추가함으로써 정책 진화가 부각되었습니다. 중동 순례와 관련된 여행 관련 클러스터는 계속 출국 시 클리닉에서 4가 부스터 수요에 박차를 가하고 있습니다. 보험 환급의 틀은 여전히 견고하지만, 5가 백신 예방 접종을 공동 조달 계약에 통합할 지의 여부는 추가 성장의 열쇠를 잡고 있습니다.

아시아태평양은 CAGR 8.56%로 가장 급성장하고 있는 지역으로, 중국의 정책 개선, 인도 물류 강화, 동남아시아의 아웃브레이크 경계가 그 원동력이 되고 있습니다. 이 지역의 "수막염균 백신 시장"은 공정한 접근에 초점을 맞추고 있습니다. 중국의 국가 계획은 2028년까지 완전한 컨쥬게이트 커버리지를 목표로 하고 있으며 인도네시아에서는 낙도로의 드론 배송 회랑을 시험적으로 도입하고 있습니다. 칸시노나 청두연구소와 같은 국내 업체들은 비용조정된 2가 백신과 4가백신을 공급하는 반면 다국적 기업은 수입관세를 피하기 위해 현지 충전 마감 라인을 준비하고 있습니다. 성공적인 폐렴 구균의 전개는 질병을 가로지르는 스케일 업을 위한 재현 가능한 청사진을 제공합니다.

나이지리아의 Men5CV 도입은 수막염 벨트에서 내열성 캠페인의 개념을 입증했습니다. Gavi, 유니세프, WHO는 긴급 비축을 유지하고 있지만, 감염 유행이 일어나기 쉬운 회랑 이외의 일상적인 프로그램에는 자금 부족이 계속되고 있습니다. 남미에서는 감시의 격차를 완화하고 특히 브라질과 칠레에서 MenACWY의 대상 확대에 관한 지역 전문가의 컨센서스에 의해 완만한 성장을 기록하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 예방접종 프로그램 증가와 정부의 대처

- 민간과 정부의 파트너십 증가로 개발 비용 저하

- 고소득 국가에서의 혈청군 W와 혈청군 Y의 아웃브레이크 발생률 증가

- 다가 Men5CV 및 5가 컨쥬게이트 플랫폼 도입

- 상온 안정형 Men5CV가 아프리카에서의 라스트 마일 딜리버리를 실현함

- MenB 부스터를 가속화하는 mRNA/단백질 나노입자 파이프라인

- 시장 성장 억제요인

- 콜드체인 보관 및 공급 물류의 높은 비용

- 신규 혈청군 콤보에 대한 엄격한 규제와 책임의 장애물

- COVID 백신 피로 후 청소년 부스터 준수율 저하

- 레거시 ACWY & B 브랜드에서의 5가 백신의 자기 잠식 리스크

- 규제 상황

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제품 유형별

- 2가

- 4가

- 기타

- 백신 유형별

- 다당류 백신

- 컨쥬게이트 백신

- 콤비네이션 백신

- 기타 유형

- 판매 채널별

- 공공

- 민간

- 연령층별

- 유아(0-2세)

- 어린이와 성인(2세 이상)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- GSK plc

- Pfizer Inc.

- Sanofi SA

- Merck & Co., Inc.

- Novartis AG

- Cyrus Poonawala Group(Serum Institute of India Ltd.)

- Bio-Manguinhos

- Biomed Pvt. Ltd.

- Johnson & Johnson(Janssen Vaccines)

- Bharat Biotech Int. Ltd.

- CSL Seqirus

- Bavarian Nordic A/S

- CanSino Biologics Inc.

- Incepta Vaccines Ltd.

- Moderna Inc.

- Valneva SE

- Chongqing Zhifei Biological Products Co.

- Sichuan Clover Biopharmaceuticals

- Panacea Biotec Ltd.

제7장 시장 기회와 미래 전망

CSM 25.11.20The meningococcal vaccines market is valued at USD 3.12 billion in 2025 and is forecast to reach USD 4.5 billion by 2030, advancing at a 7.60% CAGR.

Pentavalent platforms that combine serogroups A, B, C, W and Y are redefining product strategy, compressing multi-shot schedules into single injections and shifting demand away from older monovalent and quadrivalent brands. GSK registered the first FDA nod for a five-component shot, Penmenvy, in February 2025 , closely following Pfizer's Penbraya launch; both approvals have accelerated portfolio realignment among incumbents. Manufacturers now weigh the lure of premium pricing for combination vaccines against the cannibalization of legacy lines. Regionally, North America retains purchasing power, but Asia-Pacific delivers the fastest volume gains on the back of widening national immunization programs and emerging last-mile delivery models such as room-temperature-stable Men5CV in Nigeria. Competitive intensity is rising as biotechnology entrants leverage public-private partnerships and technology transfers to narrow time-to-market.

Global Meningococcal Vaccines Market Trends and Insights

Rising Immunization Programs & Government Initiatives

Government-financed vaccine roll-outs are scaling demand by integrating meningococcal shots into routine schedules and travel requirements. China's National Immunization Program has moved several WHO-endorsed vaccines, including meningococcal conjugates, into fully funded status, widening access across rural provinces . France convened WHO's first high-level forum on the "Defeating Meningitis by 2030" roadmap in 2024, unlocking new pledges for affordable supply and surveillance harmonisation. Saudi Arabia's requirement for MenACWY proof among Hajj and Umrah pilgrims continues to stimulate global demand, even though compliance audits show only 54% adherence among foreign travellers. These coordinated programs create predictable tender cycles that allow manufacturers to optimise batch sizes and forecast revenue horizons.

Increase in Public-Private Partnerships Lowering Development Costs

Vaccine developers are increasingly co-funded through alliances that blend academic discovery with industrial scale-up. Serum Institute of India licensed a chimeric protein MenB candidate from the University of Oxford, aiming to supply lower-cost boosters to Gavi-eligible markets . Gavi's African Vaccine Manufacturing Accelerator earmarked USD 1.2 billion in 2024 to local production, a shift expected to stabilize long-term supply and reduce lead times. PATH's collaboration with Serum Institute brought Men5CV to market at roughly USD 3 per dose, well below Western benchmarks, illustrating how risk-sharing compresses end-user prices. These models redistribute R&D exposure, enabling smaller biotechnology firms to advance novel platforms without prohibitive capital outlays.

High Cost of Cold-Chain Storage & Supply Logistics

Full-range refrigeration remains a principal cost driver, especially where ambient temperatures exceed 30 °C. Field studies in Nepal reported the average shipment value per insulated carrier at USD 1,704, with nearly one-third subject to freeze damage during transit. Controlled temperature chain pilots in India cut logistics expense from USD 0.063 to USD 0.026 per dose but demanded capital upgrades and extensive training. Drone-enabled distribution with active thermal containers shows promise yet faces regulatory clearance hurdles and limited payload capacity. Persistent infrastructure gaps translate into higher landed costs and periodic stockouts, constraining timely coverage.

Other drivers and restraints analyzed in the detailed report include:

- Growing Incidence of Serogroup W & Y Outbreaks in High-Income Nations

- Introduction of Multivalent Men5CV & Pentavalent Conjugate Platforms

- Waning Adolescent Booster Compliance Post-COVID Vaccine Fatigue

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Quadrivalent formulations generated 53.98% revenue in 2024, maintaining primacy across adolescent booster programs in North America and Europe. This leadership reflects long-standing clinical familiarity, extensive insurance coverage and robust tender frameworks anchoring the meningococcal vaccines market. Yet bivalent solutions, prized for targeted protection and lower cost, post an 8.24% CAGR through 2030. Pentavalent pipelines represent the fastest-rising "other" category as providers seek single-visit coverage for all five major serogroups.

Momentum around pentavalent approvals marks a structural pivot. Confluences of simplified schedules and broader strain breadth have prompted several states in the United States to reassess school requirements. Early modelling suggests pentavalent uptake could displace nearly 30% of quadrivalent demand by 2028, reshaping revenue distribution inside the meningococcal vaccines market. CanSino Biologics highlighted this shift with RMB 561.7 million (USD 78.5 million) bivalent sales in 2023, a 266% annual rise, signalling how local champions exploit domestic tenders for share gains.

Conjugate products held a 46.47% stake in 2024, underpinned by enduring immunogenicity and herd-immunity benefits that dovetail with paediatric protocols. Combination formats combining conjugate backbones with protein antigens are on a trajectory to post an 8.39% CAGR, opening capacity for higher-margin SKUs within the meningococcal vaccines market size. Polysaccharide shots retain a tactical role in outbreak surges because of cost advantages and quicker release timelines.

Cutting-edge conjugation chemistries now fuse five polysaccharide moieties to mutant diphtheria proteins, preserving antigen integrity while sustaining memory responses for a decade or longer. Men5CV's room-temperature profile adds a distribution benefit, particularly for Gavi-funded drives in Africa. Outer-membrane vesicle (OMV) and protein-nanoparticle constructs remain developmental but promise thermostability and cross-protection, potentially widening the meningococcal vaccines industry's future tool kit.

The Meningococcal Vaccines Market is Segmented by Product Type (Bivalent, Quadrivalent, and More), Vaccine Type (Polysaccharide Vaccines, and More), Sales Channel (Public and Private), Age Group (Infants (Aged 0-2 Years), and Children and Adults (Aged 2 Years and Above)) and Geography (North America, Europe, Asia-Pacific, and More). The Market and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 40.41% of global revenue in 2024 on the back of universal adolescent scheduling, broad payer coverage and rapid outbreak detection systems. The United States implements a two-dose MenACWY series at 11-12 and 16 years and recommends MenB for high-risk populations; Canada and Mexico track similar approaches with provincial variations. FDA approval of Penmenvy is expected to catalyse formulary reviews and private-payer negotiations, potentially accelerating pentavalent uptake. Recent ST-1466 outbreaks underscore residual vulnerability in older adults, prompting discussions on extending booster age brackets.

Europe displays mature uptake yet dynamic serogroup trends. Surveillance captured 1,149 invasive cases in 2022, of which serogroup B remained dominant at 62%. France's hosting of WHO's meningitis summit re-energised regional co-ordination, while Germany's inclusion of MenB into routine recommendations highlights policy evolution. Travel-linked clusters from Middle East pilgrimages continue to spur demand for quadrivalent boosters at point-of-departure clinics. Reimbursement frameworks remain robust, but incremental growth hinges on integrating pentavalent shots into joint procurement contracts.

Asia-Pacific is the fastest-expanding region at an 8.56% CAGR, driven by China's policy upgrades, India's logistic strengthening and Southeast Asian outbreak vigilance. The "meningococcal vaccines market" narrative in the region focuses on equitable access: China's national plan targets full conjugate coverage by 2028, while Indonesia pilots drone-delivery corridors to remote islands. Domestic producers such as CanSino and Chengdu Institute supply cost-adjusted bivalents and quadrivalents, whereas multinationals prepare local fill-finish lines to sidestep import tariffs. Successful pneumococcal roll-outs provide a replicable blueprint for cross-disease scale-up.

Africa and the Middle East represent sizeable latent demand, with Nigeria's Men5CV introduction providing proof of concept for thermostable campaigns in the meningitis belt. Gavi, UNICEF and WHO maintain emergency stockpiles, yet funding gaps persist for routine programs outside epidemic-prone corridors. South America records modest growth, constrained by surveillance disparities but buoyed by regional expert consensus on expanding MenACWY coverage, particularly in Brazil and Chile.

- GlaxoSmithKline

- Pfizer

- Sanofi

- Merck

- Novartis

- Cyrus Poonawala Group (Serum Institute of India Ltd.)

- Bio-Manguinhos

- Biomed Pvt. Ltd.

- Johnson & Johnson (Janssen Vaccines)

- Bharat Biotech Int. Ltd.

- CSL Seqirus

- Bavarian Nordic

- CanSino Biologics Inc.

- Incepta Vaccines Ltd.

- Moderna

- Valneva

- Chongqing Zhifei Biological Products Co.

- Sichuan Clover Biopharmaceuticals

- Panacea Biotec Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising immunization programs & government initiatives

- 4.2.2 Increase in public-private partnerships lowering development costs

- 4.2.3 Growing incidence of serogroup W & Y outbreaks in high-income nations

- 4.2.4 Introduction of multivalent Men5CV & pentavalent conjugate platforms

- 4.2.5 Room-temperature-stable Men5CV enabling last-mile delivery in Africa

- 4.2.6 mRNA / protein-nanoparticle pipeline accelerating MenB boosters

- 4.3 Market Restraints

- 4.3.1 High cost of cold-chain storage & supply logistics

- 4.3.2 Stringent regulatory & liability hurdles for novel serogroup combos

- 4.3.3 Waning adolescent booster compliance post-COVID vaccine fatigue

- 4.3.4 Cannibalization risk from pentavalent vaccines on legacy ACWY & B brands

- 4.4 Regulatory Landscape

- 4.5 Porters Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Bivalent

- 5.1.2 Quadrivalent

- 5.1.3 Others

- 5.2 By Vaccine Type

- 5.2.1 Polysaccharide Vaccines

- 5.2.2 Conjugate Vaccines

- 5.2.3 Combination Vaccines

- 5.2.4 Other Types

- 5.3 By Sales Channel

- 5.3.1 Public

- 5.3.2 Private

- 5.4 By Age Group

- 5.4.1 Infants (Aged 0-2 Years)

- 5.4.2 Children and Adults (Aged 2 Years and above)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global-level Overview, Market-level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 GSK plc

- 6.3.2 Pfizer Inc.

- 6.3.3 Sanofi SA

- 6.3.4 Merck & Co., Inc.

- 6.3.5 Novartis AG

- 6.3.6 Cyrus Poonawala Group (Serum Institute of India Ltd.)

- 6.3.7 Bio-Manguinhos

- 6.3.8 Biomed Pvt. Ltd.

- 6.3.9 Johnson & Johnson (Janssen Vaccines)

- 6.3.10 Bharat Biotech Int. Ltd.

- 6.3.11 CSL Seqirus

- 6.3.12 Bavarian Nordic A/S

- 6.3.13 CanSino Biologics Inc.

- 6.3.14 Incepta Vaccines Ltd.

- 6.3.15 Moderna Inc.

- 6.3.16 Valneva SE

- 6.3.17 Chongqing Zhifei Biological Products Co.

- 6.3.18 Sichuan Clover Biopharmaceuticals

- 6.3.19 Panacea Biotec Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment