|

시장보고서

상품코드

1851103

통신 API : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Telecom API - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

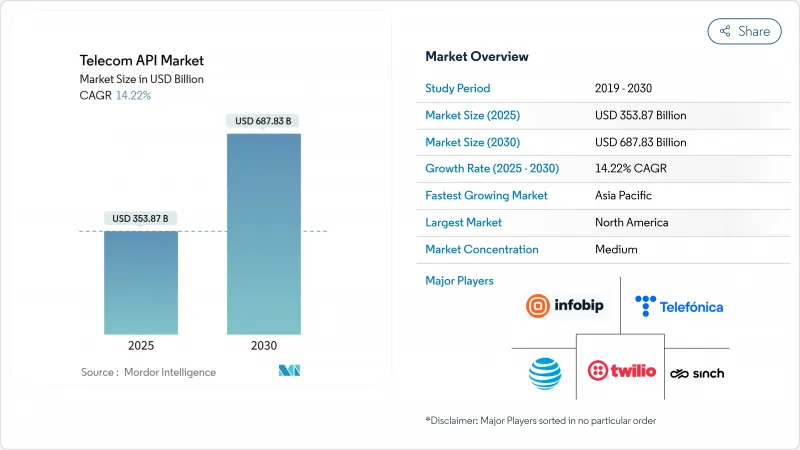

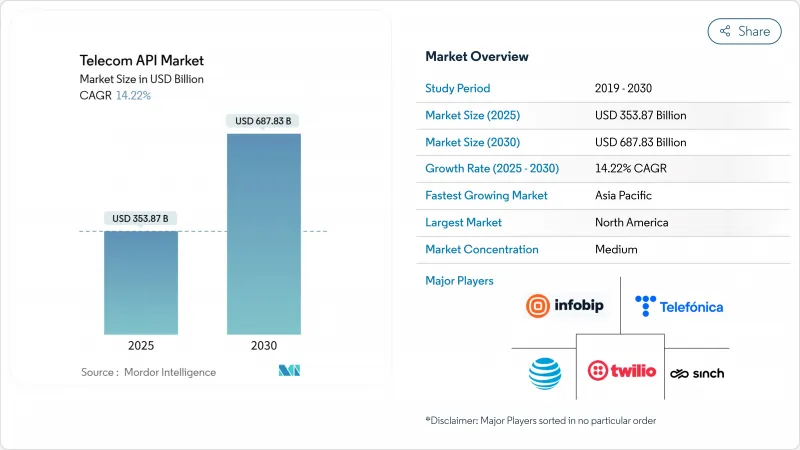

통신 API 시장 규모는 2025년에 3,538억 7,000만 달러, 2030년에는 6,878억 3,000만 달러에 이를 것으로 예상되며, 예측기간(2025-2030년)의 CAGR은 14.22%를 나타낼 전망입니다.

통신 부문의 프로그래머블 네트워크로의 전환, 5G 기능의 수익화, CPAaS(Communications Platform as a Service)의 급속한 보급을 반영합니다. GSMA Open Gateway와 같은 표준화 노력, 5G 네트워크 슬라이싱을 위한 퀄리티 온 디맨드 API의 보급, 임베디드 실시간 통신에 대한 기업 수요 등이 성장의 주요 요인이 되고 있습니다. 경쟁의 격화는 통합을 촉진합니다. 장비 공급업체와 통신 사업자는 네트워크 API를 풀링하기 위해 합작 투자 회사를 설립했으며 CPAaS 전문가는 기업 인수 전략을 통해 규모를 확대하고 있습니다. 또한 클라우드 민첩성과 데이터 주권 요구사항 간의 균형을 이루는 하이브리드 클라우드 배포도 시장의 이점을 제공하여 운영자는 네트워크 기능을 개발자 생태계에 신속하게 노출할 수 있게 되었습니다.

세계의 통신 API 시장 동향과 인사이트

기업에서의 CPaaS 도입 급증

Twilio의 2025년 1분기 매출액이 11억 7,000만 달러, 활성 고객 수가 33만 5,000개를 넘었음을 알 수 있듯이 기업은 옴니채널 커뮤니케이션을 고객 워크플로우에 계속 통합하고 있습니다. 이동통신사도 사내 효율성을 향상시키고 있습니다. AT&T의 MuleSoft를 중심으로 한 프로그램은 온보딩 사이클을 1년에서 6주로 단축하여 연간 200만 시간의 작업 시간을 절약했습니다. API 재사용으로 인한 경제적 보상은 개발자의 경험과 지속적인 통합 파이프라인에 대한 경영진의 초점을 강화합니다. 일반 인공지능을 활용한 코딩 어시스턴트는 내부 팀의 진입 장벽을 낮추고, 개인화된 메시징은 SMS, RCS 및 음성 채널에서 지속적인 트래픽을 촉진합니다.

Open Gateway 및 CAMARA로 네트워크 API 표준화

현재 49개 사업자 그룹이 GSMA Open Gateway를 지원하고 있으며 장치 검증, 지연 제어, 위치 정보 서비스 등의 기능의 통합 인터페이스에 대한 업계 합의를 보여주고 있습니다. Telefonica의 상용화를 통해 개발자는 프라이버시 관리를 유지하면서 핀테크 및 스트리밍 앱에 통신 기능을 통합할 수 있습니다. T-Mobile의 CAMARA 호환 Quality-on-Demand API는 건강 관리, 물류 및 소매에 낮은 지연 배포를 가능하게 합니다. 표준화는 소프트웨어 기업의 통합 비용을 줄이고 네트워크 지원 용도 시장 출시 시간을 단축합니다.

심각화하는 API 보안 침해 및 불법 시그널링

API 통화량은 2024년에 167% 급증했으며 플랫폼이 공격 벡터에 노출된 결과 Dell, GitHub, TracFone에서 침해가 발생했으며 후자는 1,600만 달러의 위약금을 지불했습니다. 설문 조사에 따르면 조직의 95%가 API 보안 인시던트에 직면했고 23%가 데이터 유출을 입었습니다. 가입자의 ID와 시그널링 시스템은 여러 도메인을 가로지르기 때문에 통신 사업자는 여전히 높은 표적이 되고 있습니다. 효과적인 완화 방법으로는 제로 트러스트 정책, 지속적인 런타임 보호, 통신 사업자와 클라우드 공급자 간의 위협 인텔리전스 공유 등이 있습니다.

부문 분석

메시징 API는 2024년에 35.67%의 통신 API 시장 점유율을 유지해 2조 2,000억 메시지에 달한 기업용 A2P 트래픽이 그 중심이 되었습니다. 메시징 통신 API 시장 규모는 기업이 인증 및 프로모션을 위해 SMS, MMS, 풍부한 커뮤니케이션 서비스를 선호함에 따라 꾸준히 확대될 것으로 예측됩니다. RCS의 성장에는 눈에 띄는 것이 있습니다. Infobip사는 A2P RCS의 매출이 2029년까지 42억 달러에 달할 것으로 예상했습니다. 한편, 결제 API는 CAGR 17.45%로 가장 급속히 확대되고 있습니다. 이는 임베디드 금융 모델이 통신 사업자의 도달범위와 핀텍 기능을 융합시키기 때문입니다. 음성, IVR 및 WebRTC API는 기업이 멀티모달 지원을 고객 경험 플랫폼에 통합하기 때문에 관련성을 유지합니다. 개발자는 또한 가입자 식별 API와 사기 감지 API를 활용하여 모바일 트랜잭션의 보안을 강화하고 있습니다.

수요 패턴은 부가가치 기능으로 계속 전환하고 있습니다. 일반 AI 채팅봇은 컨텍스트 메시징을 추진하고 위치 기반 API는 스마트 시티 배포에서 하이퍼로컬 마케팅을 가능하게 합니다. 스팸에 대한 규제가 강화됨에 따라 운영자는 인증된 발신자 ID에 프리미엄을 부과하여 수익의 다양화를 강화하고 있습니다. 클라우드 컨택 센터 공급업체와의 긴밀한 협력을 통해 메시징 API는 의료, 은행, 소매 등 기업의 혁신 과제의 중심이 되었습니다.

하이브리드 환경은 2024년에 49.85% 시장 점유율을 획득했고 CAGR 15.45%로 가장 높은 성장 궤도를 달성할 전망입니다. 하이브리드 전개 통신 API 시장 규모는 네트워크 코어가 On-Premise에 머무르는 반면, 과금, 분석, 노출 계층의 마이크로서비스가 퍼블릭 클라우드로 전환됨에 따라 확대될 것으로 예측됩니다. 사업자의 예로는 VIVA Bahrain의 하이브리드 클라우드 코어와 PCCW Global의 판매 API를 위한 멀티클라우드 전략이 있습니다. APAC는 로컬 데이터 스토리지에 대한 규제를 의무화하고 있으며 하이브리드 배포가 더욱 진행되고 있습니다.

운영자는 공급업체의 잠금을 피하고 비용 최적화를 위해 워크로드를 동적으로 이동하기 위해 클라우드에 민감하지 않은 컨테이너 오케스트레이션을 지원합니다. 에지 노드는 하이브리드 토폴로지를 확장하여 AI 추론 및 컴퓨터 비전 작업에 밀리초 단위의 대기 시간을 제공합니다. 순수한 퍼블릭 클라우드 모델은 그린필드의 MVNO에 여전히 적합하지만 통합의 복잡성과 예측할 수 없는 이글레스 요금은 티어원 사업자의 광범위한 채용을 제한하고 있습니다. On-Premise 전용 전략은 보안이 강조되는 정부 기관의 네트워크에는 적합하지만 대규모 API 이코노미에 필요한 탄력성이 부족합니다.

통신 API 시장 보고서는 서비스 유형별(메시징/SMS-MMS-RCS API, 음성/IVR & 음성 제어 API, 기타), 배포 유형별(하이브리드, 멀티클라우드, 기타 배포 모드), 최종 사용자별(기업 개발자, 사내 통신 개발자, 파트너 개발자, 롱테일 개발자), 비즈니스 모델별(캐리어에 직접 연결, 애그리게이터 주도의 CPaaS, Platform-As-A)로 분류됩니다.

지역 분석

북미는 2024년 매출의 34.06%를 차지하며, CPaaS의 높은 보급률과 광범위한 5G 커버리지를 반영했습니다. AT&T, T-Mobile, Verizon의 Aduna 벤처와의 협업을 통해 핀테크 및 헬스케어 용도의 보안을 높이는 번호 인증과 SIM 스왑 API에 대한 통일 액세스가 가능해졌습니다. Twilio의 2024년 매출은 44억 6,000만 달러로, 프로그래머블 통신에 대한 기업 투자가 견조하다는 것을 뒷받침했습니다. 기술 샌드박스를 장려하는 정부의 틀은 통신 API 시장에서 지속적인 실험을 지원합니다.

아시아태평양은 모바일 퍼스트 경제가 5G 도입과 디지털 서비스의 보급을 촉진하고 2030년까지 연평균 복합 성장률(CAGR)이 가장 빠른 17.51%를 나타낼 것으로 예측되고 있습니다. 2024년 2분기 지역 통신 사업자의 총 매출은 1,477억 달러에 이르렀으며, 72%의 사업자가 플러스 성장을 보고했습니다. 2028년까지 5G 가입률이 88%를 나타낼 것으로 예측되는 중국과 퀄리티 온디맨드 API를 공개하는 호주, 일본, 한국의 대처는 적극적인 확대를 보이고 있습니다. 스마트 매뉴팩처링과 전자정부에 대한 정부의 지령은 저지연과 보안기능에 대한 수요를 높이고, 통신 API 시장을 지역의 디지털 의제의 백본으로 삼고 있습니다.

유럽에서는 GDPR(EU 개인정보보호규정)에 따른 보안 조치가 API 서비스에 대한 고객의 신뢰를 높이고 있기 때문에 꾸준한 성장을 보여줍니다. 독일 텔레콤의 AI 폰 로드맵은 장치, AI 및 통신 기능의 융합에 대한 지역 통신 사업자의 관심을 보여줍니다. 유럽의 통신 사업자와 하이퍼스케일러 간의 공동 프로젝트는 에지의 전개와 CAMARA API의 표준화를 가속화합니다. 중동, 아프리카, 라틴아메리카의 신흥 시장도 네트워크 근대화 투자와 클라우드 파트너십 전략에 힘입어 디지털 서비스 개시까지 시장 투입 기간을 단축하고 비슷한 궤도를 따릅니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 기업에 있어서 CPaaS 도입의 급증

- 오픈 게이트웨이와 CAMARA에 의한 네트워크 API의 표준화

- QoS 온디맨드 API를 추진하는 5G의 수익화 압력

- 낮은 대기 시간의 슬라이싱 API를 필요로 하는 엣지 컴퓨팅 워크로드

- ID 및 과금 API를 필요로 하는 IoT 플릿의 확대

- 진입 장벽을 낮추는 Gen-AI 지원 개발 툴

- 시장 성장 억제요인

- 심각화하는 API 보안 침해와 시그널링 사기

- 레거시 OSS/BSS 업그레이드의 병목

- OTT CPaaS 경쟁에 의한 마진 압축

- 하이퍼스케일러와의 불투명한 수익 분배 모델

- 가치/공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 경쟁 기업 간 경쟁 관계

- 대체품의 위협

- 거시경제 영향 분석

- 통신 업계에서 API 이용 사례

제5장 시장 규모와 성장 예측

- 서비스 유형별

- 메시징/SMS-MMS-RCS API

- 음성/IVR 및 음성 제어 API

- 결제 API

- WebRTC API

- 위치 및 매핑 API

- 가입자 ID 관리 및 SSO API

- 기타 서비스

- 배포 유형별

- 하이브리드

- 멀티 클라우드

- 기타 배포 모드

- 최종 사용자별

- 기업 개발자

- 내부 통신 개발자

- 파트너 개발자

- 롱테일 개발자

- 비즈니스 모델별

- 직접 통신사 노출

- 어그리게이터 주도형 CPAaS

- Platform-as-a-Service(PaaS)

- API 마켓플레이스/익스체인지

- 지역별

- 북미

- 남미

- 유럽

- 아시아태평양

- 중동 및 아프리카

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 공급업체 능력 매트릭스

- 주요 공급업체의 주요 사례

- 기업 프로파일

- ATandT Inc.

- Telefonica SA

- Twilio Inc.

- Infobip Ltd.

- Sinch AB

- Verizon Communications Inc.

- Orange SA

- Deutsche Telekom AG

- Ribbon Communications

- Huawei Technologies Co. Ltd.

- Telefonaktiebolaget LM Ericsson

- Cisco Systems Inc.

- Google LLC(Apigee)

- Vodafone Group Plc

- Nokia Corp.

- Vonage Holdings Corp.

- MessageBird BV

- Bandwidth Inc.

- Telnyx LLC

- Syniverse Technologies LLC

제7장 시장 기회와 향후 전망

KTH 25.11.20The Telecom API Market size is estimated at USD 353.87 billion in 2025, and is expected to reach USD 687.83 billion by 2030, at a CAGR of 14.22% during the forecast period (2025-2030).

Uptake reflects the telecom sector's pivot to programmable networks, monetization of 5G capabilities, and the rapid spread of Communications Platform as a Service (CPaaS). Key forces behind growth include standardization efforts such as GSMA Open Gateway, the proliferation of quality-on-demand APIs for 5G network slicing, and enterprise demand for embedded real-time communications. Competitive intensity has prompted consolidation: equipment vendors and carriers have formed joint ventures to pool network APIs, while CPaaS specialists scale through enterprise acquisition strategies. The market also benefits from hybrid cloud deployments that balance cloud agility with data-sovereignty requirements, positioning operators to quickly expose network functions to developer ecosystems.

Global Telecom API Market Trends and Insights

Surge in CPaaS adoption among enterprises

Enterprises continue embedding omnichannel communications into customer workflows, illustrated by Twilio's Q1 2025 revenue of USD 1.17 billion and an active customer base exceeding 335,000. Operators improve internal efficiency as well: AT&T's MuleSoft-centered program cut onboarding cycles from one year to six weeks and saved 2 million work hours annually. The economic payoff from API reuse reinforces management's focus on developer experience and continuous integration pipelines. Generative-AI-powered coding assistants lower entry barriers for in-house teams, and personalized messaging fuels sustained traffic on SMS, RCS, and voice channels.

Open Gateway and CAMARA standardization of network APIs

Forty-nine operator groups now back GSMA Open Gateway, signaling an industry consensus on unified interfaces for capabilities such as device verification, latency control, and location services. Telefonica's commercial launch shows developers integrating telecom features into fintech and streaming apps while retaining privacy controls. T-Mobile's CAMARA-compliant Quality-on-Demand APIs enable low-latency deployments in healthcare, logistics, and retail. Standardization lowers integration costs for software firms and accelerates time-to-market for network-aware applications.

Escalating API-security breaches and signaling fraud

API call volumes leapt 167% in 2024, exposing platforms to attack vectors that resulted in breaches at Dell, GitHub, and TracFone, the latter paying USD 16 million in penalties. Research shows 95% of organizations faced API security incidents, with 23% suffering data loss. Telecom players remain high-value targets because subscriber identity and signaling systems traverse multiple domains. Effective mitigations include zero-trust policies, continuous runtime protection, and threat-intelligence sharing between carriers and cloud providers.

Other drivers and restraints analyzed in the detailed report include:

- Monetization pressure on 5G driving QoS-on-demand APIs

- Edge-computing workloads need low-latency slicing APIs

- Legacy OSS/BSS upgrade bottlenecks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Messaging APIs retained 35.67% Telecom API market share in 2024, anchored by enterprise A2P traffic that reached 2.2 trillion messages. The Telecom API market size for messaging is forecast to expand steadily as businesses prioritize SMS, MMS, and Rich Communication Services for authentication and promotions. RCS growth is striking: Infobip projects A2P RCS revenue climbing to USD 4.2 billion by 2029. Meanwhile, Payment APIs are scaling fastest at 17.45% CAGR because embedded finance models blend telecom reach with fintech capabilities. Voice, IVR, and WebRTC APIs retain relevance as enterprises integrate multi-modal support into customer-experience platforms. Developers also leverage subscriber-identity and fraud-detection APIs to boost security for mobile transactions.

Demand patterns continue shifting toward value-added functionality. Generative-AI chatbots drive contextual messaging, and location-based APIs enable hyperlocal marketing in smart-city rollouts. As regulation tightens against spam, operators charge premiums for verified sender IDs, reinforcing revenue diversification. Close collaboration with cloud contact-center vendors keeps messaging APIs central to enterprise transformation agendas across healthcare, banking, and retail.

Hybrid environments captured 49.85% market share in 2024 and delivered the highest growth trajectory at 15.45% CAGR, underscoring operator priorities around sovereignty and latency. Telecom API market size for hybrid deployments is projected to expand as network cores stay on-premises while microservices for billing, analytics, and exposure layers move to public cloud. Operator examples include VIVA Bahrain's hybrid cloud core and PCCW Global's multi-cloud strategy for wholesale APIs. Regulatory mandates for local data storage in APAC further sustain hybrid uptake.

Operators favor cloud-agnostic container orchestration to avoid vendor lock-in and to dynamically shift workloads for cost optimization. Edge nodes extend hybrid topologies, offering developers single-digit-millisecond latency for AI inference and computer-vision tasks. Pure public-cloud models remain suitable for greenfield MVNOs, but integration complexity and unpredictable egress fees limit broad adoption for tier-one operators. On-premises-only strategies persist for security-sensitive government networks yet lack the elasticity required for large-scale API economies.

The Telecom API Market Report is Segmented by Service Type (Messaging/SMS-MMS-RCS API, Voice/IVR & Voice Control API, and More), Deployment Type (Hybrid, Multi-Cloud, and Other Deployment Modes), End-User (Enterprise Developer, Internal Telecom Developer, Partner Developer, and Long-Tail Developer), Business Model (Direct Carrier Exposure, Aggregator-Led CPaaS, Platform-As-A-Service [PaaS], and More), and Geography.

Geography Analysis

North America accounted for 34.06% of 2024 revenue, reflecting high CPaaS penetration and extensive 5G coverage. Collaboration among AT&T, T-Mobile, and Verizon in the Aduna venture allows unified access to Number Verification and SIM Swap APIs that raise security for fintech and healthcare applications. Twilio's USD 4.46 billion 2024 revenue underscores robust enterprise spending on programmable communications, while developer-first cultures spur quick uptake of new network features. Government frameworks that encourage technology sandboxes support continuous experimentation in the Telecom API market.

Asia-Pacific is forecast to register the fastest 17.51% CAGR through 2030 as mobile-first economies escalate 5G rollouts and digital-services adoption. Combined regional telco revenue hit USD 147.7 billion in Q2 2024, with 72% of operators reporting positive growth. China's projected 88% 5G subscription rate by 2028 and initiatives in Australia, Japan, and South Korea to expose quality-on-demand APIs illustrate aggressive expansion. Government mandates for smart manufacturing and e-governance increase demand for low-latency and security features, making the Telecom API market the backbone of regional digital agendas.

Europe shows steady growth because GDPR-aligned security practices elevate customer trust in API services. Deutsche Telekom's AI-phone roadmap demonstrates regional operator interest in converging devices, AI, and telecom capabilities. Collaborative projects among European carriers and hyperscalers accelerate edge deployments and standardized CAMARA APIs. Emerging markets in the Middle East, Africa, and Latin America ride similar trajectories, backed by network-modernization investments and cloud-partnership strategies that lower time-to-market for digital-service launches.

- ATandT Inc.

- Telefonica SA

- Twilio Inc.

- Infobip Ltd.

- Sinch AB

- Verizon Communications Inc.

- Orange SA

- Deutsche Telekom AG

- Ribbon Communications

- Huawei Technologies Co. Ltd.

- Telefonaktiebolaget LM Ericsson

- Cisco Systems Inc.

- Google LLC (Apigee)

- Vodafone Group Plc

- Nokia Corp.

- Vonage Holdings Corp.

- MessageBird B.V.

- Bandwidth Inc.

- Telnyx LLC

- Syniverse Technologies LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in CPaaS adoption among enterprises

- 4.2.2 Open Gateway and CAMARA standardisation of network APIs

- 4.2.3 Monetisation pressure on 5G driving QoS-on-demand APIs

- 4.2.4 Edge-computing workloads need low-latency slicing APIs

- 4.2.5 IoT fleet expansion demanding ID and billing APIs

- 4.2.6 Gen-AI-assisted dev-tools lowering entry barriers

- 4.3 Market Restraints

- 4.3.1 Escalating API-security breaches and signalling fraud

- 4.3.2 Legacy OSS/BSS upgrade bottlenecks

- 4.3.3 Margin compression from OTT CPaaS competitors

- 4.3.4 Unclear revenue-share models with hyperscalers

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Intensity of Competitive Rivalry

- 4.7.5 Threat of Substitute Products

- 4.8 Macroeconomic Impact Analysis

- 4.9 API Use Cases in Telecom Industry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Messaging/SMS-MMS-RCS API

- 5.1.2 Voice/IVR and Voice Control API

- 5.1.3 Payment API

- 5.1.4 WebRTC API

- 5.1.5 Location and Mapping API

- 5.1.6 Subscriber ID Mgmt and SSO API

- 5.1.7 Other Services

- 5.2 By Deployment Type

- 5.2.1 Hybrid

- 5.2.2 Multi-cloud

- 5.2.3 Other Deployment Modes

- 5.3 By End-User

- 5.3.1 Enterprise Developer

- 5.3.2 Internal Telecom Developer

- 5.3.3 Partner Developer

- 5.3.4 Long-tail Developer

- 5.4 By Business Model

- 5.4.1 Direct Carrier Exposure

- 5.4.2 Aggregator-led CPaaS

- 5.4.3 Platform-as-a-Service (PaaS)

- 5.4.4 API Marketplace/Exchange

- 5.5 By Geography

- 5.5.1 North America

- 5.5.2 South America

- 5.5.3 Europe

- 5.5.4 Asia Pacific

- 5.5.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Vendor Capability Matrix

- 6.5 Key Case Studies of Major Vendors

- 6.6 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.6.1 ATandT Inc.

- 6.6.2 Telefonica SA

- 6.6.3 Twilio Inc.

- 6.6.4 Infobip Ltd.

- 6.6.5 Sinch AB

- 6.6.6 Verizon Communications Inc.

- 6.6.7 Orange SA

- 6.6.8 Deutsche Telekom AG

- 6.6.9 Ribbon Communications

- 6.6.10 Huawei Technologies Co. Ltd.

- 6.6.11 Telefonaktiebolaget LM Ericsson

- 6.6.12 Cisco Systems Inc.

- 6.6.13 Google LLC (Apigee)

- 6.6.14 Vodafone Group Plc

- 6.6.15 Nokia Corp.

- 6.6.16 Vonage Holdings Corp.

- 6.6.17 MessageBird B.V.

- 6.6.18 Bandwidth Inc.

- 6.6.19 Telnyx LLC

- 6.6.20 Syniverse Technologies LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment