|

시장보고서

상품코드

1851465

비즈니스 분석 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Business Analytics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

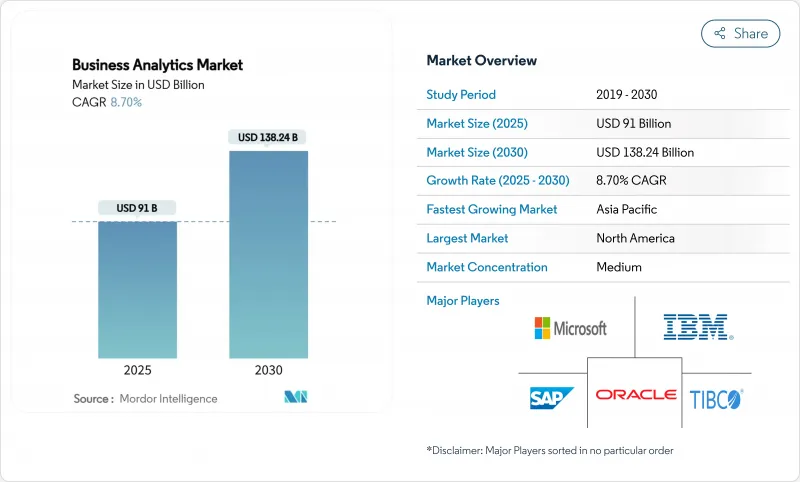

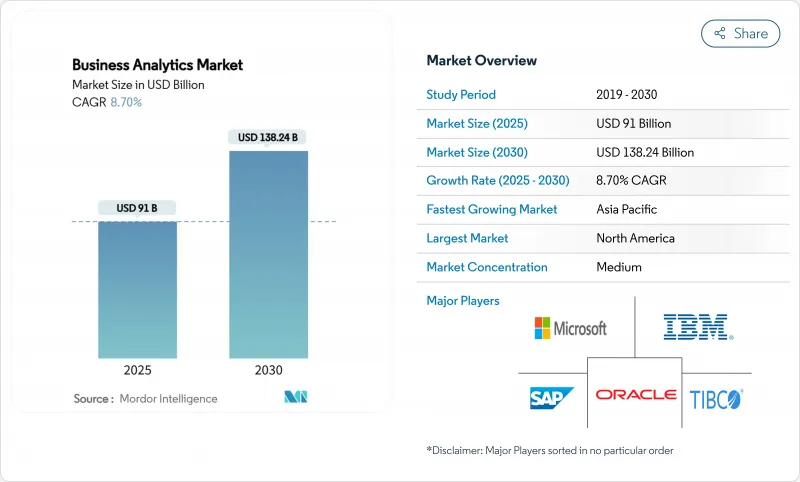

비즈니스 분석 시장의 2025년 시장 규모는 910억 달러, 2030년에는 CAGR 8.70%로 성장하고 1,382억 4,000만 달러에 이를 것으로 예측됩니다.

클라우드 네이티브 플랫폼, AI 자동화, 디지털 변환의 광범위한 추진이 이러한 확장을 지원합니다. 각 업계의 조직은 현재 비효율적인 발견, 고객 참여의 강화, 의사결정 주기를 단축하기 위해 일상적인 워크플로우에 분석를 통합하고 있습니다. 인공지능과 확립된 분석 스택의 융합으로 분석 분야는 레트로스펙티브 보고서에서 실시간 예측 인텔리전스로 전환하고 있으며, 클라우드의 보급으로 모든 규모의 기업에 대한 진입 장벽이 낮아지고 있습니다. 기존 기업 소프트웨어 공급업체는 클라우드 전문가와 보다 신속한 배포와 간단한 사용자 경험을 약속하는 AI First 신흥 기업의 속도에 맞게 포트폴리오를 새롭게 하고 있으며, 경쟁의 치열함이 계속되고 있습니다. 인재 부족, 데이터 주권에 관한 규칙, 초기 비용의 높이가 계속해서 성장을 억제하고 있지만, 데이터 중심 업무로의 구조적 전환은 아직 지연되지 않았습니다.

세계 비즈니스 분석 시장 동향 및 통찰

분석 플랫폼에 AI 및 ML 배포

인공지능은 비즈니스 분석 플랫폼에서 볼트 온 기능에서 핵심 기능으로 이동합니다. Snowflake Cortex 및 Microsoft 365 Copilot의 Analyst 에이전트와 같은 새로운 릴리스는 자연 언어를 해석하고 SQL을 자동으로 생성하며 이전에는 데이터 사이언스자가 필요했던 예측 통찰력을 드러냅니다. 이러한 기능을 채택한 기업은 마케팅, 공급망, 재무 팀에서 생산성이 30-50% 향상된 것으로 보고되었습니다. 모델 교육 비용이 낮아짐에 따라 플랫폼 공급업체는 생성형 AI를 통합하여 액세스 범위를 넓히고 데이터 준비를 자동화하며 인간 코딩 없이 자율 에이전트가 복잡한 분석 파이프라인을 오케스트레이션하는 '에이전트 분석' 시대의 도래를 알립니다.

빅데이터와 클라우드 보급

데이터의 양, 속도 및 유형은 증가의 길을 따라갑니다. 6,000개가 넘는 조직이 매주 275페타바이트 이상의 데이터를 BigQuery에서 상호작용하고 있으며, 탄력적인 클라우드 스토리지와 컴퓨팅이 분석의 기본 기반이 되고 있음을 돋보이게 합니다. ClickHouse와 AWS의 5년 계약과 같은 공동 혁신 프로그램은 금융 및 전자상거래 워크로드에 특화된 솔루션을 가속화하고 있습니다. 클라우드 프레임워크는 또한 현지화된 IoT 데이터 처리와 중앙 집중식 대시보드의 페어링을 가능하게 하여 산업 환경에서 장비 효율성을 10% 향상시키고 예기치 않은 다운타임을 30% 줄일 수 있습니다.

데이터 주권에 대한 제한

GDPR(EU 개인정보보호규정), CLOUD법, 새로운 국내법 사이에 상충되는 규칙이 존재하기 때문에 다국적 기업은 지역 고유의 데이터 스택을 구축할 수밖에 없습니다. 하이퍼스케일러와 지역 제공업체가 제공하는 소블린 클라우드는 이 문제를 해결하고 있지만, 기업은 분석의 일관성을 깨지 않고 규제 당국을 만족시키기 위해 여러 공급업체와 통제를 잘 사용하고 있습니다.

부문 분석

클라우드 부문은 2024년 매출의 65.4%를 차지했고 CAGR은 10.7%를 나타내고 2030년에는 비즈니스 분석 시장 규모의 더 큰 부분을 차지하게 될 것으로 예상됩니다. 자본 지출 감소, 탄력적인 스케일링, 데이터 레이크 및 AI 서비스와의 신속한 통합이 그 매력을 더욱 향상시키고 있습니다. 보안 인증 및 자동화된 컴플라이언스 기능은 현재 금융, 헬스케어, 정부 워크로드를 다루며 On-Premise 지지자의 마지막 아성을 침식하고 있습니다.

엄격한 대기 시간, 레거시와의 통합, 규제상의 의무 등이 있는 경우에는 On-Premise의 도입도 뿌리 깊지만 그 점유율은 해마다 후퇴하고 있습니다. 하이브리드 블루프린트는 방화벽 내부에 민감한 워크로드를 남기고 버스트 처리를 클라우드로 마이그레이션하여 과도적인 경로를 제공합니다. 공급업체는 마이그레이션 툴킷, 관리 서비스 및 소비 기반 가격 설정을 번들로 망설이고 있는 고객을 클라우드로 유도하고 시장 리더이자 성장 엔진인 클라우드 지위를 강화하고 있습니다.

기술적 분석은 2024년 매출의 32.7%를 차지했고 비즈니스 분석 시장에서 가장 큰 점유율을 차지하지만 예측기술은 CAGR 8.8%로 전체 카테고리를 상회합니다. 조직은 '무슨 일이 일어났는가' 대시보드에서 해지 위험을 신고하고 재고를 최적화하고 고장이 발생하기 전에 유지 보수 작업자를 라우팅하는 미래를 향한 모델로 진화합니다. Generic AI는 복잡한 시계열 모델을 자동 코딩하고 비기술 사용자를 위한 시나리오 시뮬레이션을 표시하여 예측 워크플로를 향상시킵니다.

진단 분석은 근본 원인을 설명하고 예측 알고리즘을 특징으로 하는 교량의 역할을 합니다. 처방 도구는 예산과 인원과 같은 제약 하에서 최선의 행동을 권장하고 루프를 닫습니다. 최적화된 생산 일정으로 소비자 제품 제조업체가 매주 최대 20만 달러를 절약한 초기 성공 사례는 보다 광범위한 도입에 박차를 가하고 있습니다. 툴킷이 성숙함에 따라 예측 레이어와 처방 레이어가 공동으로 과거 데이터를 전체 기능의 자동화된 컨텍스트를 의식적인 의사 결정으로 변환하게 됩니다.

비즈니스 분석 시장은 배포 모델(On-Premise, 클라우드), 분석 유형(기술형, 진단형, 기타), 조직 규모(대기업, 중소기업), 최종 사용자 산업(은행, 금융서비스 및 보험(BFSI), 의료 및 생명 과학 등), 지역별로 구분됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

지역 분석

북미는 성숙한 기술 생태계, 풍부한 인재, 조기 클라우드 도입으로 2024년 매출의 27.4%를 차지했습니다. 기업은 AI 가속기, 스트리밍 파이프라인 및 자동화된 거버넌스로 기존 플랫폼을 개선하고 확립된 데이터 자산으로부터 효율성을 높입니다. 미국은 지출을 이끌고 캐나다는 천연 자원 및 금융 서비스 분야에서 분석를 활용합니다. 멕시코는 수출 지향 제조업과 국경을 넘어 물류를 지원하기 위해 클라우드 플랫폼을 채택하고 있습니다.

아시아태평양은 CAGR 10.3%로 가장 급성장하고 있으며, 정부의 AI 전략, 모바일의 보급, 그린필드에서의 클라우드 도입이 그 요인이 되고 있습니다. 중국은 이 지역의 비즈니스 분석 시장의 37.5%를 차지하며, 대규모 디지털 결제 생태계와 산업 업그레이드 프로그램에 의해 지원되고 있습니다. 베트남, 필리핀 등 고성장 국가에서는 중소기업이 SaaS 분석를 도입하여 레거시 시스템을 비약적으로 향상시키고 있으며 연간 성장률은 19%를 넘고 있습니다. 인도, 일본, 한국, 태국은 공공 부문의 보조금을 노동력 기술과 데이터 에코시스템 개발을 향해 플랫폼 벤더에게 비옥한 토양을 만들어 내고 있습니다.

유럽은 강력한 개인 정보 보호 규정과 업계의 디지털화 자금에 의해 지원되고 꾸준히 전진하고 있습니다. 독일, 프랑스, 영국은 제조 효율성과 재무 컴플라이언스에 분석를 도입하고 남유럽 국가들은 관광 및 소매 분석 이용 사례를 확대하고 있습니다. 소블린 클라우드의 프레임워크와 프라이버시 강화 기술이 GDPR(EU 개인정보보호규정) 주도 수요에 대응. 중동 및 아프리카는 특히 걸프 국가에서 스마트시티 구상의 혜택을 받고 남미는 브라질과 아르헨티나에 클라우드를 도입함으로써 견인력을 늘리고 있지만 인프라 격차와 통화 변동이 도입 경사를 약화시키고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 빅데이터와 클라우드의 보급

- 실시간 의사 결정의 필요성

- 분석 플랫폼에 AI/ML 도입

- 데이터 주도형 컴플라이언스에 대한 규제 강화

- IoT를 많이 사용하는 산업을 위한 엣지 분석

- 프라이버시를 보호하는 데이터 클린 룸

- 시장 성장 억제요인

- 높은 초기 비용과 ROI 불확실성

- 고급 분석의 인력 부족

- 데이터 주권에 관한 제한

- ESG 데이터의 품질 격차

- 공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 시장의 거시경제 요인 평가

제5장 시장 규모와 성장 예측

- 전개 모델별

- On-Premise

- 클라우드

- 분석 유형별

- 기술적

- 진단

- 예측

- 처방적

- 기업 규모별

- 대기업

- 중소기업(SME)

- 최종 사용자 업계별

- 은행, 금융서비스 및 보험(BFSI)

- 헬스케어 및 생명과학

- 제조업

- 소매 및 전자상거래

- 통신 및 IT

- 정부·공공 부문

- 에너지 및 유틸리티

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 동남아시아

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 이집트

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 이동과 자금 조달 활동

- 시장 점유율 분석

- 기업 프로파일

- Microsoft Corp.

- SAP SE

- Oracle Corp.

- IBM Corp.

- Salesforce Inc.(Tableau)

- SAS Institute Inc.

- TIBCO Software Inc.

- Qlik Tech Intl.

- MicroStrategy Inc.

- Infor Inc.

- Google LLC(Looker)

- Amazon Web Services(QuickSight)

- Domo Inc.

- Sisense Ltd.

- ThoughtSpot Inc.

- Alteryx Inc.

- Zoho Corp.(Zoho Analytics)

- Board International

- GoodData Corp.

- Yellowfin BI

- Pyramid Analytics

- Logi Analytics(InsightSoftware)

- Teradata Corp.

- Informatica Inc.

- Palantir Technologies

- Snowflake Inc.

- Databricks Inc.

제7장 시장 기회와 장래의 전망

SHW 25.11.21The business analytics market is valued at USD 91 billion in 2025 and is forecast to reach USD 138.24 billion by 2030, reflecting an 8.70% CAGR over the period.

Cloud-native platforms, AI-driven automation, and a widespread push for digital transformation underpin this expansion. Organizations across industries now embed analytics into day-to-day workflows to uncover inefficiencies, sharpen customer engagement, and shorten decision cycles. The convergence of artificial intelligence with established analytics stacks is shifting the discipline from retrospective reporting toward real-time predictive intelligence, while pervasive cloud adoption lowers entry barriers for firms of every size. Competitive intensity remains lively as incumbent enterprise software vendors revamp portfolios to match the pace set by cloud specialists and AI-first start-ups that promise faster deployment and simpler user experiences. Talent shortages, data-sovereignty rules, and high initial costs continue to temper growth yet have not derailed the structural migration toward data-centric operations.

Global Business Analytics Market Trends and Insights

AI and ML infusion into analytics platforms

Artificial intelligence has shifted from a bolt-on feature to a core capability within business analytics platforms. New releases such as Snowflake Cortex and Microsoft 365 Copilot's Analyst agent interpret natural language, auto-generate SQL, and surface predictive insights that once required a data scientist. Companies adopting these capabilities report 30-50% productivity lifts in marketing, supply-chain, and finance teams. As model training costs fall, platform vendors embed generative AI to widen access and automate data preparation, ushering in an era of "agentic analytics" where autonomous agents orchestrate complex analysis pipelines without human coding.

Proliferation of big data and cloud adoption

Volume, velocity, and variety of data keep rising. More than 6,000 organizations exchange upward of 275 petabytes each week on BigQuery, highlighting how elastic cloud storage and compute have become the default substrate for analytics. Joint innovation programs, such as the five-year agreement between ClickHouse and AWS, accelerate purpose-built solutions for finance and e-commerce workloads. Cloud frameworks also let firms pair localized IoT data processing with centralized dashboards, delivering 10% gains in equipment efficiency and 30% reductions in unplanned downtime in industrial settings.

Data-sovereignty restrictions

Conflicting rules among GDPR, the CLOUD Act, and emerging national laws force multinationals to architect region-specific data stacks. Deployments must ensure local processing, encrypted transfers, and auditable consent, adding cost and complexity.Sovereign-cloud offerings from hyperscalers and regional providers address the issue, yet organizations still juggle multiple vendors and controls to satisfy regulators without fracturing analytical coherence.

Other drivers and restraints analyzed in the detailed report include:

- Need for real-time decision-making

- Edge analytics for IoT-heavy industries

- Talent shortage in advanced analytics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The cloud segment accounts for 65.4% of 2024 revenue, and its 10.7% CAGR means it will command an even larger slice of the business analytics market size by 2030. Lower capital expenditure, elastic scaling, and rapid integration with data lakes and AI services cement its appeal. Security certifications and automated compliance features now cover finance, healthcare, and government workloads, eroding the last strongholds of on-premise advocates.

On-premise deployments persist where strict latency, legacy integration, or regulatory mandates prevail, but their share recedes every year. Hybrid blueprints, in which sensitive workloads stay behind the firewall while burst processing moves to the cloud, offer a transitional path. Providers bundle migration toolkits, managed services, and consumption-based pricing to nudge hesitant customers toward the cloud, reinforcing its position as both market leader and growth engine.

Descriptive analytics retained 32.7% of 2024 revenue, the largest slice of the business analytics market, yet predictive techniques outpace all categories with an 8.8% CAGR. Organizations evolve from "what happened" dashboards to forward-looking models that flag churn risk, optimize inventory, and route maintenance crews before breakdowns occur. Generative AI enhances predictive workflows by auto-coding complex time-series models and surfacing scenario simulations for non-technical users.

Diagnostic analytics serves as a bridge, explaining root causes and feeding features into forecasting algorithms. Prescriptive tools close the loop by recommending the best action under constraints such as budget or staffing. Early success stories like a consumer-products maker saving up to USD 200,000 weekly through optimized production schedules fuel wider adoption. As toolkits mature, predictive and prescriptive layers will jointly convert historical data into automated, context-aware decisions across functions.

Business Analytics Market is Segmented by Deployment Model (On-Premises, Cloud), Analytics Type (Descriptive, Diagnostic, and More), Organization Size (Large Enterprises, Smes), End-User Industry (BFSI, Healthcare and Life Sciences, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America holds 27.4% of 2024 revenue thanks to a mature technology ecosystem, abundant talent, and early cloud adoption. Enterprises refine existing platforms with AI accelerators, streaming pipelines, and automated governance, squeezing incremental efficiency from established data assets. The United States leads spending, and Canada leverages analytics in natural-resources and financial-services verticals. Mexico adopts cloud platforms to support export-oriented manufacturing and cross-border logistics.

Asia Pacific is the fastest-growing region at a 10.3% CAGR, fueled by government AI strategies, widespread mobile adoption, and greenfield cloud deployments. China commands 37.5% of the regional business analytics market, backed by large-scale digital payment ecosystems and industrial upgrade programs. High-growth economies such as Vietnam and the Philippines exceed 19% annual expansion as SMEs embrace SaaS analytics to leapfrog legacy systems. India, Japan, South Korea, and Thailand channel public-sector grants into workforce upskilling and data-ecosystem development, creating fertile ground for platform vendors.

Europe advances steadily underpinned by strong privacy regulations and industry digitization funding. Germany, France, and the United Kingdom deploy analytics for manufacturing efficiency and financial compliance, while southern nations expand tourism and retail analytics use cases. Sovereign-cloud frameworks and privacy-enhancing technologies address GDPR-driven demands. The Middle East and Africa benefit from smart-city agendas, especially in the Gulf states, whereas South America gains traction through cloud uptake in Brazil and Argentina, although infrastructure gaps and currency volatility temper the slope of adoption

- Microsoft Corp.

- SAP SE

- Oracle Corp.

- IBM Corp.

- Salesforce Inc. (Tableau)

- SAS Institute Inc.

- TIBCO Software Inc.

- Qlik Tech Intl.

- MicroStrategy Inc.

- Infor Inc.

- Google LLC (Looker)

- Amazon Web Services (QuickSight)

- Domo Inc.

- Sisense Ltd.

- ThoughtSpot Inc.

- Alteryx Inc.

- Zoho Corp. (Zoho Analytics)

- Board International

- GoodData Corp.

- Yellowfin BI

- Pyramid Analytics

- Logi Analytics (InsightSoftware)

- Teradata Corp.

- Informatica Inc.

- Palantir Technologies

- Snowflake Inc.

- Databricks Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of big data and cloud adoption

- 4.2.2 Need for real-time decision-making

- 4.2.3 AI/ML infusion into analytics platforms

- 4.2.4 Regulatory push for data-driven compliance

- 4.2.5 Edge analytics for IoT-heavy industries

- 4.2.6 Privacy-preserving data clean rooms

- 4.3 Market Restraints

- 4.3.1 High upfront cost and ROI uncertainty

- 4.3.2 Talent shortage in advanced analytics

- 4.3.3 Data-sovereignty restrictions

- 4.3.4 ESG-data quality gaps

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assesment of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 On-Premise

- 5.1.2 Cloud

- 5.2 By Analytics Type

- 5.2.1 Descriptive

- 5.2.2 Diagnostic

- 5.2.3 Predictive

- 5.2.4 Prescriptive

- 5.3 By Organisation Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Mid-sized Enterprises (SMEs)

- 5.4 By End-user Industry

- 5.4.1 Banking, Financial Services and Insurance (BFSI)

- 5.4.2 Healthcare and Life Sciences

- 5.4.3 Manufacturing

- 5.4.4 Retail and E-commerce

- 5.4.5 Telecom and IT

- 5.4.6 Government and Public Sector

- 5.4.7 Energy and Utilities

- 5.4.8 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Southeast Asia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Funding Activity

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Microsoft Corp.

- 6.4.2 SAP SE

- 6.4.3 Oracle Corp.

- 6.4.4 IBM Corp.

- 6.4.5 Salesforce Inc. (Tableau)

- 6.4.6 SAS Institute Inc.

- 6.4.7 TIBCO Software Inc.

- 6.4.8 Qlik Tech Intl.

- 6.4.9 MicroStrategy Inc.

- 6.4.10 Infor Inc.

- 6.4.11 Google LLC (Looker)

- 6.4.12 Amazon Web Services (QuickSight)

- 6.4.13 Domo Inc.

- 6.4.14 Sisense Ltd.

- 6.4.15 ThoughtSpot Inc.

- 6.4.16 Alteryx Inc.

- 6.4.17 Zoho Corp. (Zoho Analytics)

- 6.4.18 Board International

- 6.4.19 GoodData Corp.

- 6.4.20 Yellowfin BI

- 6.4.21 Pyramid Analytics

- 6.4.22 Logi Analytics (InsightSoftware)

- 6.4.23 Teradata Corp.

- 6.4.24 Informatica Inc.

- 6.4.25 Palantir Technologies

- 6.4.26 Snowflake Inc.

- 6.4.27 Databricks Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment