|

시장보고서

상품코드

1907354

정형외과용 보조기 및 지지대 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Orthopedic Braces And Supports - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

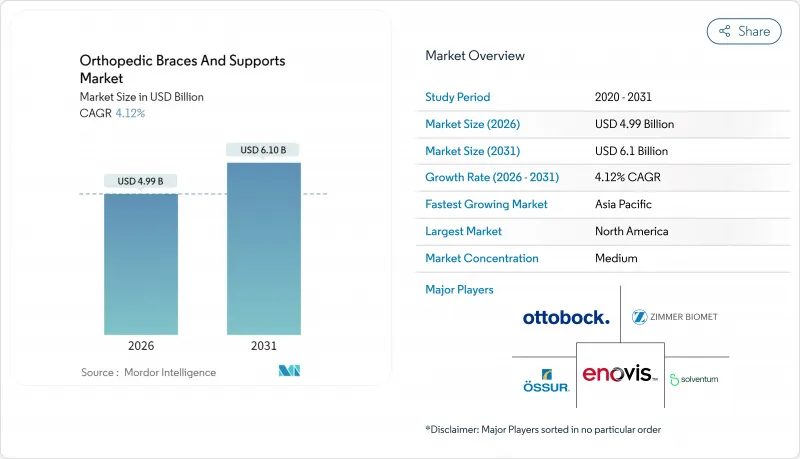

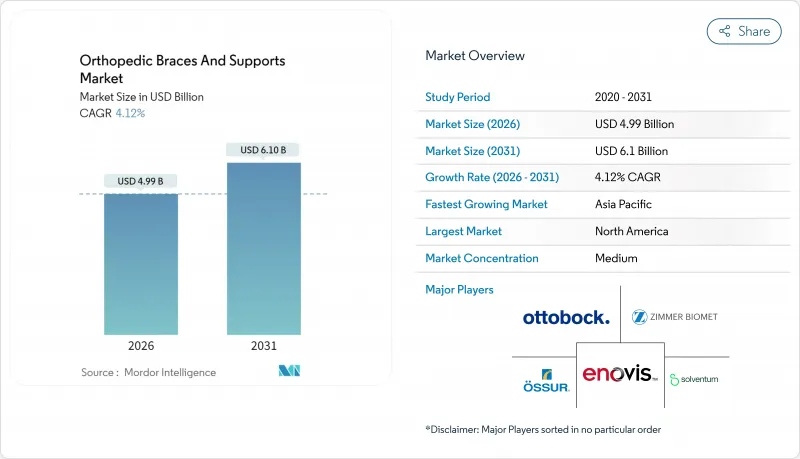

정형외과용 보조기 및 지지대 시장은 2025년 47억 9,000만 달러에서 2026년에는 49억 9,000만 달러로 성장해 2026년에서 2031년에 걸쳐 CAGR 4.12%로 성장할 것으로 예상되며, 2031년까지 61억 달러에 이를 것으로 예측됩니다.

꾸준한 확대는 고령화에 따른 골절 발생률의 상승, 예방적 장비 장착으로의 인지도 확대, 재택 재활 프로그램으로의 이행에 기인하고 있습니다. AI 탑재 얼라인먼트 시스템에서 환자 특화형 3D 프린팅 기술에 이르는 기술 진보로 정형외과용 보조기 및 지지대 시장은 범용품 제조에서 부가가치가 높은 스마트 디바이스로 전환하고 있습니다. 특히 북미의 비외과적 치료 단계를 포괄하는 상환제도 개혁은 입원기간 단축으로 이어지는 비용 효과적인 장비 수요를 뒷받침하고 있습니다. 주요 기업이 혁신에 중점을 두고 있는 한편, 저비용 아시아 제품의 가격 압력에 직면하고 있기 때문에 경쟁의 심각성은 적당합니다.

세계의 정형외과용 보조기 및 지지대 시장 동향 및 인사이트

골절 발생률 상승

원위 요골 골절, 손가락 골절, 고관절 골절은 각각 인구 10만 명당 212.0건, 117.1건, 112.9건의 발생률을 보이며, 안정화 장치에 대한 장기적 수요를 강조합니다. 보조기를 통한 조기 이동은 장애 위험을 낮추고 비용 효율적인 치료를 지원하며, 이는 만성 골절 후유증을 관리하는 지불자에게 중요한 제안입니다.

근골격계 질환 증가 경향

17억 명 이상이 근골격계 질환을 앓고 있으며, 요통이 정형외과 내원의 26%를 차지합니다. 요추 보조기와 물리치료 병행 시 12주 동안 통증 점수가 6.28에서 3.96으로 감소하고 오스웨스트리 지수 기능 점수가 46.56에서 33.13으로 개선되었다. 따라서 수요는 장기간 착용에 적합한 편안하고 조절 가능한 장치로 기울어지고 있습니다.

경미한 부상에 대한 무관심

치료 지연은 여전히 흔합니다. 인도 농촌 지역 어린이의 71%가 외상 후 늦게 내원하여 종종 결과를 악화시킵니다. 이러한 행동은 예방적 보조기 판매를 저해하고 장기적 성장을 억제합니다.

부문 분석

정형외과용 보조기 및 지지대 시장 매출의 55.78%를 하지 보조기가 차지했으며, 이는 높은 무릎, 발목, 고관절 부상률에 기반한 주도적 위상입니다. 전방 십자 인대 손상이 연간 10만 명당 17.5건 발생함에 따라 무릎 보조기가 최대 하위 클러스터를 형성합니다. 스포츠 의학 수요는 관절 치환 수술을 지연시키는 언로더(unloader) 디자인의 확산과 맞물려 골관절염 관리와 교차합니다. 3D 프린팅 발목 지지대와 조절 가능한 발 보조기는 소매 클리닉의 신속한 디지털 스캐닝 기술 지원으로 러닝 및 하이킹 커뮤니티에 침투하고 있습니다. 고관절 외전 보조기는 수술 후 관리용으로만 사용되던 것이 이제는 장기 요양 시설의 노인 낙상 예방 프로그램에서 예방적 목적으로 활용됩니다.

척추 보조기는 2024년 FDA 승인을 받은 신경자극 융합 자극기의 혜택을 받아 연평균 5.05% 성장률로 가장 빠르게 성장하는 분야입니다. 관성 센서가 내장된 스마트 벨트는 재활 프로그램을 향상시키는 자세 분석 데이터를 의료진에게 제공합니다. 상지 보조기 시장은 규모는 작지만, 첨단 작업장에서 반복성 긴장 손상(RSI)을 줄이기 위한 인체공학적 노력에 힘입어 성장하고 있습니다. 웨어러블 센서 통합으로 보조기는 수동적 지지 장치에서 능동적 코치로 변모하여 동작 교정을 유도하고 치료 순응도를 높입니다. 종합적으로 보조기 제품 구성은 연결형 솔루션으로 전환되며, 이는 정형외과 보조기 및 지지대 시장이 맞춤형 데이터 기반 치료로 나아가는 추세를 강화합니다.

2025년 병원 부문은 50.63%의 매출 점유율을 유지하며 광범위한 수술 역량과 정형외과·외상 분야 통합 구매 계약을 반영했습니다. 자본 예산은 상당한 연간 보조기 조달을 가능하게 하며, 이는 임상적으로 검증된 브랜드를 선호하는 가치분석 위원회 관할 하에 진행됩니다. 그러나 성장은 정형외과 및 외상 센터 쪽으로 기울어, 환자들이 전문적 노하우와 빠른 회복 경로를 추구함에 따라 2031년까지 연평균 5.18% 성장할 전망입니다. 이러한 센터들은 환자 체형에 맞춘 재고 관리 시스템에 투자하여 착용감을 개선하고 재고 손실을 줄입니다.

외래수술센터(ASC)가 성장을 가속시키고 있습니다. Zimmer Biomet-CBRE와 같은 파트너십은 변화하는 시술량을 포착하기 위해 새로운 외래 시설을 확장합니다. 2023년 270만 명의 수혜자를 지원한 메디케어 자금 지원에 힘입어 가정 간호 환경에서도 채택이 가속화됩니다. 원격 감독 보조기 맞춤 및 조정 프로토콜은 비용 효율적인 사후 관리를 가능하게 합니다. 다양한 최종 사용자 채널은 병원을 중심으로 한 주기적 변동성으로부터 정형외과용 보조기 및 지지대 시장을 보호합니다.

지역별 분석

북미는 2025년 매출의 40.21%를 차지했으며, 이는 비수술적 정형외과적 중재를 보상하는 강력한 보험 적용 범위와 CMS 프로그램에 기반합니다. 미국은 첨단 제조 기술을 통해 지역적 우위를 주도하며, 2024년 아시아에 29억 달러 상당의 정형외과 용품을 수출했습니다. 캐나다는 공공 자금 지원 관절 치환술 패키지를 통해 도입을 확대하고 있으며, 멕시코는 세구로 포풀라르(Seguro Popular) 확대를 통해 접근성을 넓히고 있습니다. 성숙한 시장 침투에도 불구하고, AI 기반 정렬 및 원격 재활과 같은 지속적인 기술 업그레이드로 인해 정형외과 보조기 및 지지대 시장은 중간 단일 자릿수 성장을 유지하고 있습니다.

유럽은 보편적 의료 시스템과 의료기기 규정(MDR) 하의 엄격한 시판 후 감시로 형성된 확고한 기반을 유지하고 있습니다. 독일은 브레멘과 바이에른 클러스터를 활용한 스마트 정형외과 연구를 통해 지역의 혁신 허브 역할을 수행합니다. 영국 의약품 및 의료제품 규제청(MHRA)은 MDR 일정에 부합하면서도 독립적인 심사 경로를 마련해 브렉시트 이후 공급 연속성을 유지하고 있습니다. 남유럽 국가들은 예산 제약 관리를 위해 비침습적 근골격계 치료에 점점 더 많은 자금을 할당하고 있습니다. 그 결과 유럽은 엄격한 임상적·경제적 가치 기준을 충족하는 프리미엄급, 증거 기반 기기를 계속 선호하고 있습니다.

아시아태평양 지역은 중산층 확대, 정부 보험 확대, 스포츠 참여 증가에 힘입어 2031년까지 5.26%의 가장 빠른 연평균 성장률(CAGR)을 기록할 전망입니다. 중국은 2025년까지 45만 5천 건의 관절 치환술과 100만 건의 골절 치료가 예상되며, 이는 재활 기간 중 보조기 수요를 촉진할 것입니다. 일본은 초고령 사회 관리를 위해 스마트 재활 기술 도입을 가속화하고 있으며, 호주는 광활한 지역을 아우르는 원격 보조기 사후관리 프로그램을 지원하는 원격의료 프로그램을 운영 중입니다. 인도, 태국, 말레이시아는 수입 의존도를 낮추기 위해 현지 제조를 장려하며 합작 투자 기회를 열어두고 있습니다. 환율 변동성과 입찰 기반 조달은 가격 책정에 어려움을 주지만, 물량 측면의 기회는 해당 지역 전체에서 정형외과용 보조기 및 지지대 시장을 매우 매력적으로 유지하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 골절 발생률 증가

- 근골격계 질환 증가 경향

- 교통사고 및 스포츠 부상 증가

- 스마트/3D 프린팅 보조기 기술 전환

- 코로나19 이후 재택 재활 서비스 붐

- 비수술적 정형외과 치료에 대한 묶음형 보험급여

- 시장 성장 억제요인

- 경미한 부상에 대한 무관심

- 차세대 보조기에 대한 인식 부족

- 검증되지 않은 DTC 전자상거래 보조기에 대한 의사 채택률 저조

- 아시아로부터의 상품 수입품에 의한 가격 압력

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제품별

- 하지 보조기 및 지지대

- 발목 및 발

- 고관절

- 무릎

- 척추 보조기 및 지지대

- 상지 보조기 및 지지대

- 팔꿈치

- 손과 손목

- 어깨

- 기타

- 하지 보조기 및 지지대

- 최종 사용자별

- 병원

- 정형외과, 외래수술센터(ASC)

- 재택 케어 환경

- 기타

- 용도별

- 인대 손상

- 예방의료 및 예방적 사용

- 수술 후 재활

- 골관절염 관리

- 기타

- 연령층별

- 소아

- 성인

- 고령자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Solventum

- Essity(BSN Medical)

- DJO LLC(Enovis)

- Ossur

- Ottobock

- Zimmer Biomet

- Bauerfeind

- Medi GmbH

- DeRoyal Industries

- Bird & Cronin

- Frank Stubbs

- ALCARE

- Becker Orthopedic

- Thuasne

- Tynor Orthotics

- Rehan Health

- Breg Inc.

- United Ortho

- OrthoPediatrics Corp.

제7장 시장 기회와 장래의 전망

HBR 26.02.04The orthopedic braces and supports market is expected to grow from USD 4.79 billion in 2025 to USD 4.99 billion in 2026 and is forecast to reach USD 6.1 billion by 2031 at 4.12% CAGR over 2026-2031.

Steady expansion stems from rising fracture incidence in aging populations, broader awareness of preventive bracing, and the shift toward home-based rehabilitation programs. Technological progress-from AI-enabled alignment systems to patient-specific 3-D printing-has moved the orthopedic braces and supports market away from commodity manufacturing and toward value-added smart devices. Reimbursement reforms that bundle non-surgical episodes of care, especially in North America, reinforce demand for cost-effective braces that shorten hospital stays. Competitive intensity remains moderate as leading firms emphasize innovation while facing pricing pressure from low-cost Asian imports.

Global Orthopedic Braces And Supports Market Trends and Insights

Rise in Bone-Fracture Incidence

Distal radius, finger, and hip fractures occur at 212.0, 117.1, and 112.9 cases per 100 000 person-years respectively, underscoring the long-term demand for stabilization devices. Early mobilization with braces lowers disability risk and supports cost-effective care, a crucial proposition for payers managing chronic fracture sequelae.

Growing Prevalence of Musculoskeletal Disorders

More than 1.7 billion individuals live with musculoskeletal ailments, with lower-back pain driving 26% of orthopedic visits. Lumbar bracing combined with physical therapy cut pain scores from 6.28 to 3.96 and improved function on the Oswestry Index from 46.56 to 33.13 over 12 weeks. Demand therefore skews toward comfortable, adjustable devices suited for long-term wear .

Negligence Toward Minor Injuries

Delayed treatment remains common; 71% of rural Indian children present late after trauma, often worsening outcomes. Such behavior curtails prophylactic brace sales and depresses long-term growth.

Other drivers and restraints analyzed in the detailed report include:

- Technological Shift to Smart/3-D-Printed Supports

- Home-Care Rehabilitation Boom Post-COVID

- Price Pressure from Commodity Asian Imports

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lower-extremity devices contributed 55.78% of 2025 revenue within the orthopedic braces and supports market, a leadership grounded in high knee, ankle, and hip injury rates. Knee braces form the largest subcluster, as anterior cruciate ligament injuries run 17.5 cases per 100,000 annually. Sports medicine demand intersects with osteoarthritis management, swelling uptake of unloader designs that delay joint-replacement surgery. 3-D-printed ankle supports and adjustable foot orthoses are penetrating running and hiking communities, aided by rapid-fit digital scanning in retail clinics . Hip abduction braces, once reserved for post-surgical protocols, now see prophylactic use among elderly fall-prevention programs in long-term care facilities.

Spinal braces remain the fastest-growing category at a 5.05% CAGR, benefiting from neurostimulation-enabled fusion stimulators cleared by the FDA in 2024. Smart belts with embedded inertial sensors supply clinicians with posture analytics that enhance rehabilitation programs. Upper-extremity devices, though smaller in volume, ride ergonomic initiatives to cut repetitive-strain injuries in high-tech workplaces. Wearable sensor integration changes braces from passive support to active coaches that prompt motion correction, encouraging compliance. Collectively, the orthotic product mix is shifting toward connected solutions, reinforcing the orthopedic braces and supports market's trajectory toward personalized, data-rich care.

Hospitals retained 50.63% revenue share in 2025, reflecting broad surgical capacity and integrated purchasing contracts across orthopedics and trauma. Capital budgets allow for significant annual brace procurement, often under value-analysis committees that favor clinically supported brands. Growth, however, tilts toward orthopedic and trauma centers, expected to expand 5.18% annually through 2031 as patients seek specialized expertise and faster recovery pathways. These centers invest in inventory systems that match patient anthropometrics, improving fit and reducing inventory write-offs.

Ambulatory surgery centers amplify momentum: partnerships such as Zimmer Biomet-CBRE scale new outpatient facilities to capture shifting procedure volumes. Home-care environments also accelerate adoption, buoyed by Medicare funding that covered 2.7 million beneficiaries in 2023. Tele-supervised brace fitting and adjustment protocols enable cost-effective follow-up care. Together, diversified end-user channels insulate the orthopedic braces and supports market from hospital-centric cyclicality.

The Orthopedic Braces and Supports Market is Segmented by Product (Lower Extremity Braces and Supports [Hip, Knee, and More], Spinal Braces and Supports, and More), End User (Hospitals, and More), Application (Ligament Injuries and More), Age Group (Adult and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 40.21% of 2025 revenue, underpinned by robust insurance coverage and CMS programs that reimburse non-surgical orthopedic interventions. The United States drives regional dominance through advanced manufacturing, exporting USD 2.9 billion in orthopedic goods to Asia in 2024. Canada scales adoption through publicly funded arthroplasty bundles, while Mexico widens access via Seguro Popular expansion. Despite mature penetration, ongoing technology upgrades-AI-enabled alignment and tele-rehabilitation-sustain mid-single-digit gains in the orthopedic braces and supports market.

Europe retains a well-established base shaped by universal healthcare systems and rigorous post-market surveillance under the Medical Device Regulation. Germany serves as the region's innovation hub, leveraging Bremen and Bavaria clusters for smart orthopedic research. The United Kingdom's Medicines and Healthcare products Regulatory Agency aligns with MDR timelines while carving independent review pathways, preserving supply continuity post-Brexit. Southern European nations increasingly allocate funds to non-invasive musculoskeletal care to manage budget constraints. As a result, Europe continues to favor premium, evidence-backed devices that meet strict clinical and economic value thresholds.

Asia-Pacific delivers the fastest 5.26% CAGR through 2031 on the back of middle-class expansion, government insurance rollouts, and rising sports participation. China forecasts 455 000 joint replacements and 1 million fracture repairs for 2025, driving brace demand during rehabilitation. Japan accelerates adoption of smart rehabilitation technology to manage its super-aged society, while Australia funds tele-health programs covering remote brace follow-ups across vast geographies. India, Thailand, and Malaysia incentivize local manufacturing to reduce dependence on imports, opening avenues for joint ventures. Currency volatility and tender-based procurement create pricing challenges, yet the volume opportunity keeps the orthopedic braces and supports market highly attractive across the region.

- Solventum

- Essity

- DJO LLC (Enovis)

- Ossur

- Ottobock

- Zimmer Biomet

- Bauerfeind

- Medi GmbH

- DeRoyal Industries

- Bird & Cronin

- Frank Stubbs

- ALCARE

- Beckton Dickinson

- Thuasne

- Tynor Orthotics

- Rehan Health

- Breg

- United Ortho

- OrthoPediatrics Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise In Bone Fracture Incidence

- 4.2.2 Growing Prevalence of Musculoskeletal Disorders

- 4.2.3 Rising Road-Traffic & Sports Injuries

- 4.2.4 Technological Shift to Smart/3-D-Printed Supports

- 4.2.5 Home-Care Rehabilitation Boom Post-COVID

- 4.2.6 Bundled Reimbursement for Non-Surgical Orthopedic Care

- 4.3 Market Restraints

- 4.3.1 Negligence Toward Minor Injuries

- 4.3.2 Lack Of Awareness of Next-Gen Braces

- 4.3.3 Low Physician Adoption of Unvalidated DTC E-Commerce Braces

- 4.3.4 Price Pressure from Commodity Asian Imports

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porters Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Lower-Extremity Braces and Supports

- 5.1.1.1 Ankle & Foot

- 5.1.1.2 Hip

- 5.1.1.3 Knee

- 5.1.2 Spinal Braces and Supports

- 5.1.3 Upper-Extremity Braces and Supports

- 5.1.3.1 Elbow

- 5.1.3.2 Hand & Wrist

- 5.1.3.3 Shoulder

- 5.1.3.4 Others

- 5.1.1 Lower-Extremity Braces and Supports

- 5.2 By End User

- 5.2.1 Hospitals

- 5.2.2 Orthopedic and Trauma Centers

- 5.2.3 Home-Care Settings

- 5.2.4 Others

- 5.3 By Application

- 5.3.1 Ligament Injuries

- 5.3.2 Preventive Care and Prophylactic Use

- 5.3.3 Post-operative Rehabilitation

- 5.3.4 Osteoarthritis Management

- 5.3.5 Others

- 5.4 By Age Group

- 5.4.1 Pediatric

- 5.4.2 Adult

- 5.4.3 Geriatric

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Solventum

- 6.3.2 Essity (BSN Medical)

- 6.3.3 DJO LLC (Enovis)

- 6.3.4 Ossur

- 6.3.5 Ottobock

- 6.3.6 Zimmer Biomet

- 6.3.7 Bauerfeind

- 6.3.8 Medi GmbH

- 6.3.9 DeRoyal Industries

- 6.3.10 Bird & Cronin

- 6.3.11 Frank Stubbs

- 6.3.12 ALCARE

- 6.3.13 Becker Orthopedic

- 6.3.14 Thuasne

- 6.3.15 Tynor Orthotics

- 6.3.16 Rehan Health

- 6.3.17 Breg Inc.

- 6.3.18 United Ortho

- 6.3.19 OrthoPediatrics Corp.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment