|

시장보고서

상품코드

1851621

지카바이러스 검사 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Zika Virus Testing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

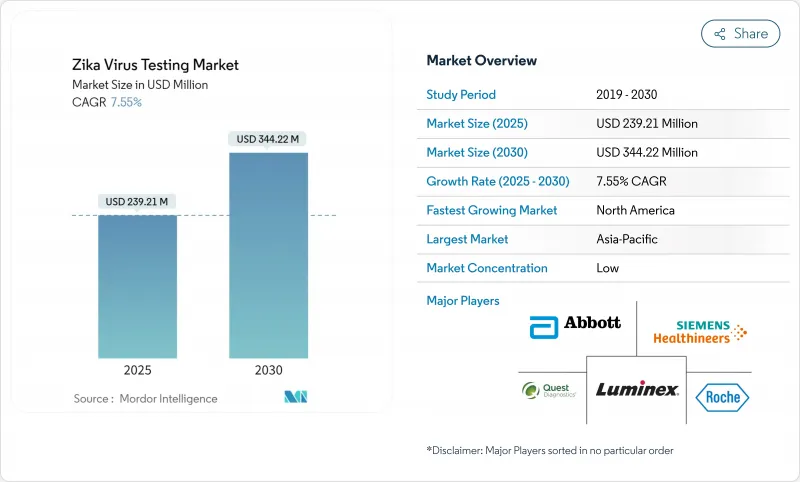

지카바이러스 검사 시장 규모는 2025년에 2억 3,921만 달러, 2030년에는 3억 4,422만 달러에 이를 것으로 예측되며, 2025-2030년의 CAGR은 7.55%를 나타낼 전망입니다.

강력한 아르보바이러스 감시 의무, 기후에 의한 매개충의 확대, 해외도항 증가가 성장세를 지속시키고 있습니다. 검사실이 지카열, 뎅기열, 치구구니야열을 한번에 검출하는 멀티플렉스 분자 플랫폼을 채용해, 공유행 지역에서의 진단의 불확실성을 줄임으로써, 기술의 수렴이 가속화되고 있습니다. 인공지능을 활용한 분석 설계로 과거의 교차 반응성이 완화되고 개발 사이클이 단축되는 한편 국내 제조 전략은 유행 시대의 혼란에 대응하는 공급망의 회복력을 강화하고 있습니다.

세계의 지카바이러스 검사 시장 동향과 인사이트

지카 열 아웃 브레이크 발생률 상승

범미 보건기구(PAN AMERICAN HEALTH ORGANIZATION)는 2024년에 4만 891건의 확정 증례를 기록했으며, 이는 2023년부터 14% 급증하여 열대 지역에서 바이러스가 유행하고 있음을 뒷받침했습니다. 예측 가능한 계절적 급증은 트리아지 시에 지카열을 뎅기열이나 쿵쿵니아열과 구별하기 위한 신속 분자 카트리지를 조달하는 병원에 박차를 가합니다. 브라질은 지역별 사례의 84%를 차지하며 여전히 진원지입니다. WHO의 지침은 검사 시설이 유행과 유행 사이의 기준선 능력을 유지하고 연간 시약 수요를 안정화하도록 촉구하고 있습니다.

정부에 의한 감시와 자금 지원

지속적인 공공 투자는 지카바이러스 검사 시장을 지원합니다. CDC의 Epidemiology and Laboratory Capacity 프로그램은 2025년까지 중재 병원체의 할당을 둘러싸고 각 주에서 실험실 시약 구매를 보장합니다. 세계 은행의 유통 기금은 통합된 아르보바이러스 모니터링 네트워크를 강화하기 위해 카리브해 국가에 1,600만 달러를 제공했습니다. NIAID의 2025년 예산설명은 진단약의 연구개발에 중점을 두어 여러 해에 걸친 자금조달 전망을 제시했습니다.

유행 기세 감소

임상적인 의심이 희미해지고 예산이 다른 곳으로 이동함에 따라, 유행 사이의 코야스 상태는 일상 검사량을 억제합니다. WHO가 2024년 5월에 발표한 최신 정보는 핫스팟 이외의 환자 수가 침착하고 있음을 지적하고 있으며, 일부 실험실에서는 시약 재고가 고갈되었습니다. 제조업체 각사는 지카 열의 발생률이 낮아도 카트리지의 회전을 유지하는 멀티플렉스 패널로 수요의 계곡을 메우고 있지만, 수익의 변동은 여전히 역풍입니다.

부문 분석

분자 분석의 2024년 매출은 58.50%에 이르렀고, 급성기 진단의 우위성이 밝혀졌습니다. 포인트 오브 케어 분자 플랫폼 시장 규모는 2030년까지 연평균 복합 성장률(CAGR) 8.91%를 나타낼 것으로 예측됩니다. 혈청검사의 지카바이러스 검사 시장 점유율은 뎅기열의 교차반응성에 의해 침체되고 있지만, 집단 수준의 IgM 조사는 기준선 수요를 유지하고 있습니다. 등온 증폭 방법과 AI 큐레이션 프라이머는 런타임과 수동 단계를 단축하고 자원에 제한이 있는 실험실에서의 확장성을 향상시킵니다.

2세대 LAMP 카트리지는 동결건조 시약을 상온 운송에 활용하여 콜드체인 비용을 낮추고 있습니다. 디지털 PCR은 유병률이 낮은 감시를 위해 상승하고 있으며 혈액은행 스크리닝에 적합한 펨토그램 수준의 감도를 제공합니다. PRNT는 여전히 레퍼런스 등급이지만 BSL-3 센터의 한 줌으로 제한되며 상업적 풋 프린트는 제한적입니다. 혈청학 기업은 특이성을 되찾기 때문에 에피토프를 조작한 항원에 축족을 옮기고 있지만, 예측 기간 내에 분자의 우위성이 위협받지 않을 것 같습니다.

지역 분석

북미의 2024년 매출액의 42.23%는 CDC 보조금 흐름과 공급업체 투자 위험을 줄이는 신속한 긴급 사용 허가를 반영했습니다. 이 지역의 지카바이러스 검사 시장 규모는 혈액 은행과 불임 치료 클리닉에서의 스크리닝이 여행 관련 수입에 의해 유지되기 때문에 꾸준히 확대됩니다. 연방 정부의 비축은 낮은 빈도의 해에도 시약의 회전을 보장합니다.

아시아태평양은 각국 정부가 국민 모두 보험 제도의 확충 속에서 아르보바이러스 감시를 주류로 하고 있기 때문에 CAGR 7.19%로 성장을 선도하고 있습니다. 기후로 인한 예네코 서식지의 온대 위도로의 전환은 일본, 한국, 중국 북부의 조기 경계 분자 플랫폼 도입에 박차를 가하고 있습니다. 인도와 인도네시아의 도시에서는 타액 키오스크를 시험적으로 도입하고 실시간으로 양성을 지자체 대시보드에 보냅니다.

브라질을 중심으로 남미는 여전히 벌크 카트리지 수요를 견인하는 역학적 핫스팟입니다. PAHO가 조정하는 시약의 입찰은 지역 실험실 가격의 안정을 도모하면서 크로스 트레이닝 프로그램을 통해 분석 성능을 표준화하고 있습니다. 유럽에서는 지중해 모기 지역에서 여행자 검사와 출생 전 스크리닝에 중점을 둡니다. IVDR에 의한 하모나이제이션은 멀티플렉스 CE 마크 패널의 채용을 가속화하고 있습니다.

중동 및 아프리카에서는 중개 모기의 감시가 기증자의 지원을 받으면서 수요가 급증하고 있습니다. 나이지리아의 National Arbovirus Laboratory Network는 2024년 최초의 높은 처리량 NAAT 라인을 설치하여 새로운 비즈니스 기회를 제시했습니다. 걸프 국가는 이민 노동자의 유입을 스크리닝하기 위해 진단 약물을 조달하고 여행과 연계된 수입원을 추가합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 지카 열 아웃 브레이크 증가

- 정부 감시 및 자금 지원

- RT-PCR과 멀티플렉스 NAAT의 진보

- POC 검사를 ID 패널에 통합

- 임신 전 스크리닝 수요

- 벡터 감시/임상 검사 네트워크

- 시장 성장 억제요인

- 유행의 기세의 쇠퇴

- 뎅기 항체와의 교차 반응성

- 짧은 바이러스 검출 기간

- 항원 공급망의 병목

- 가치/공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 공급기업의 협상력

- 구매자의 협상력

- 대체품의 위협

- 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 검사 유형별

- 분자 검사(RT-PCR, NAAT)

- 혈청학적 검사(IgM/IgG ELISA)

- 플라크 감소 중화 검사(PRNT)

- 샘플 유형별

- 혈액/혈청

- 소변

- 타액 및 기타

- 최종 사용자별

- 병원 및 클리닉

- 진단 실험실

- 재택 케어 환경

- 연구 기관

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Roche Diagnostics

- Abbott Laboratories

- Thermo Fisher Scientific

- Quest Diagnostics

- ARUP Laboratories

- Eurofins Scientific

- DiaSorin

- Chembio Diagnostics

- Hologic Inc.

- Luminex Corporation

- Siemens Healthineers

- Altona Diagnostics

- Creative Diagnostics

- InBios International

- Biocan Diagnostics

- QIAGEN

- bioMerieux

- Bio-Rad Laboratories

제7장 시장 기회와 향후 전망

KTH 25.11.24The Zika virus testing market size is USD 239.21 million in 2025 and is forecast to reach USD 344.22 million in 2030, advancing at a 7.55% CAGR over 2025-2030.

Robust arboviral surveillance mandates, climate-driven vector expansion, and rising international travel sustain the growth momentum. Technology convergence is accelerating as laboratories adopt multiplex molecular platforms that detect Zika, dengue, and chikungunya in a single run, trimming diagnostic uncertainty in co-endemic regions. Artificial-intelligence-assisted assay design is mitigating historical cross-reactivity and shortening development cycles, while domestic manufacturing strategies are strengthening supply-chain resilience in response to pandemic-era disruptions.

Global Zika Virus Testing Market Trends and Insights

Rising Incidence of Zika Outbreaks

Pan American Health Organization recorded 40,891 confirmed cases in 2024, a 14% jump from 2023, confirming the virus's endemic status in tropical belts. Predictable seasonal surges spur hospitals to procure rapid molecular cartridges that distinguish Zika from dengue and chikungunya during triage. Brazil remains the epicenter at 84% of regional cases, while emergent clusters in Argentina and Colombia widen geographic test uptake. WHO guidance urges laboratories to maintain baseline capacity between epidemics, stabilizing annual reagent demand.

Government Surveillance & Funding

Sustained public investment is anchoring the Zika virus testing market. The CDC's Epidemiology and Laboratory Capacity program ring-fenced vector-borne allocations for FY 2025, guaranteeing reagent purchases for state labs. The World Bank's Pandemic Fund channeled USD 16 million to Caribbean nations to bolster integrated arboviral surveillance networks. NIAID's 2025 budget narrative earmarks diagnostics R&D, signalling multiyear funding visibility that reassures manufacturers of volume commitments.

Declining Epidemic Momentum

Inter-epidemic lulls curb routine testing volumes as clinical suspicion wanes and budgets shift elsewhere. WHO's May 2024 update flagged subdued case counts outside hotspots, prompting some laboratories to run down reagent stocks. Manufacturers bridge the demand trough with multiplex panels that preserve cartridge turnover even when Zika incidence dips, yet revenue variability remains a headwind.

Other drivers and restraints analyzed in the detailed report include:

- Advances in RT-PCR & Multiplex NAAT

- POC Test Integration into ID Panels

- Cross-reactivity with Dengue Antibodies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Molecular assays delivered 58.50% revenue in 2024, underscoring their primacy in acute-phase diagnosis. The Zika virus testing market size for point-of-care molecular platforms is forecast to expand at 8.91% CAGR through 2030, supported by CLIA-waived systems that slot into emergency rooms and obstetric clinics. The Zika virus testing market share for serology trails due to dengue cross-reactivity, though population-level IgM surveys sustain baseline demand. Isothermal amplification and AI-curated primers are shrinking run times and manual steps, enhancing scalability in resource-constrained laboratories.

Second-generation LAMP cartridges leverage lyophilized reagents for ambient shipping, lowering cold-chain costs. Digital PCR is emerging for low-prevalence surveillance, offering femtogram-level sensitivity suited to blood-bank screening. PRNT remains reference-grade yet limited to a handful of BSL-3 centers, constraining its commercial footprint. Serology firms are pivoting toward epitope-engineered antigens to claw back specificity, but molecular dominance is unlikely to be challenged within the forecast window.

The Zika Virus Testing Market Report is Segmented by Test Type (Molecular Tests, Serologic Tests, PRNT), Sample Type (Blood/Serum, Urine, Saliva & Others), End-User (Hospitals & Clinics, Public-Health/Diagnostic Laboratories, Point-Of-Care Settings & Home Testing, Research Institutes), and Geography (North America, South America, Europe, APAC, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America's 42.23% revenue in 2024 reflects CDC grant flows and rapid Emergency Use Authorizations that de-risk vendor investment. The Zika virus testing market size in the region will advance steadily as travel-linked importations sustain screening in blood banks and fertility clinics. Federal stockpiles guarantee reagent turnover even during low-incidence years.

Asia-Pacific leads in growth at 7.19% CAGR as governments mainstream arboviral surveillance within universal healthcare expansions. Climate-driven Aedes range shifts toward temperate latitudes spur Japan, South Korea, and northern China to adopt early-warning molecular platforms. Urban megacities in India and Indonesia are piloting saliva kiosks that transmit real-time positives to municipal dashboards.

South America, anchored by Brazil, remains the epidemiological hotspot that drives bulk cartridge demand. PAHO-coordinated reagent tenders create price stability for regional labs while cross-training programs standardize assay performance. Europe focuses on traveler testing and antenatal screening in Mediterranean mosquito zones. Harmonization under IVDR is accelerating adoption of multiplex CE-marked panels.

The Middle East and Africa exhibit nascent but fast-rising demand as vector surveillance gains donor support. Nigeria's National Arbovirus Laboratory Network installed its first high-throughput NAAT line in 2024, signaling emerging opportunities. Gulf nations procure diagnostics to screen migrant labor inflows, adding a travel-linked revenue stream.

- Roche

- Abbott Laboratories

- Thermo Fisher Scientific

- Quest Diagnostics

- ARUP Laboratories

- Eurofins

- DiaSorin

- Chembio Diagnostics

- Hologic

- Luminex

- Siemens Healthineers

- Altona Diagnostics

- Creative Diagnostics

- InBios International

- Biocan Diagnostics

- QIAGEN

- bioMerieux

- Bio-Rad Laboratories

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising incidence of Zika outbreaks

- 4.2.2 Government surveillance & funding

- 4.2.3 Advances in RT-PCR & multiplex NAAT

- 4.2.4 POC test integration into ID panels

- 4.2.5 Pre-conception screening demand

- 4.2.6 Vector-surveillance/clinical-lab networks

- 4.3 Market Restraints

- 4.3.1 Declining epidemic momentum

- 4.3.2 Cross-reactivity with dengue antibodies

- 4.3.3 Short viraemic detection window

- 4.3.4 Antigen supply-chain bottlenecks

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power - Suppliers

- 4.7.3 Bargaining Power - Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Test Type (Value)

- 5.1.1 Molecular Tests (RT-PCR, NAAT)

- 5.1.2 Serologic Tests (IgM/IgG ELISA)

- 5.1.3 Plaque-Reduction Neutralisation Test (PRNT)

- 5.2 By Sample Type (Value)

- 5.2.1 Blood / Serum

- 5.2.2 Urine

- 5.2.3 Saliva & Others

- 5.3 By End-User (Value)

- 5.3.1 Hospitals & Clinics

- 5.3.2 Diagnostic Laboratories

- 5.3.3 Home care Settings

- 5.3.4 Research Institutes

- 5.4 By Geography (Value)

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 GCC

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Roche Diagnostics

- 6.3.2 Abbott Laboratories

- 6.3.3 Thermo Fisher Scientific

- 6.3.4 Quest Diagnostics

- 6.3.5 ARUP Laboratories

- 6.3.6 Eurofins Scientific

- 6.3.7 DiaSorin

- 6.3.8 Chembio Diagnostics

- 6.3.9 Hologic Inc.

- 6.3.10 Luminex Corporation

- 6.3.11 Siemens Healthineers

- 6.3.12 Altona Diagnostics

- 6.3.13 Creative Diagnostics

- 6.3.14 InBios International

- 6.3.15 Biocan Diagnostics

- 6.3.16 QIAGEN

- 6.3.17 bioMerieux

- 6.3.18 Bio-Rad Laboratories

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment