|

시장보고서

상품코드

1851650

데이터 레이크 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Data Lake - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

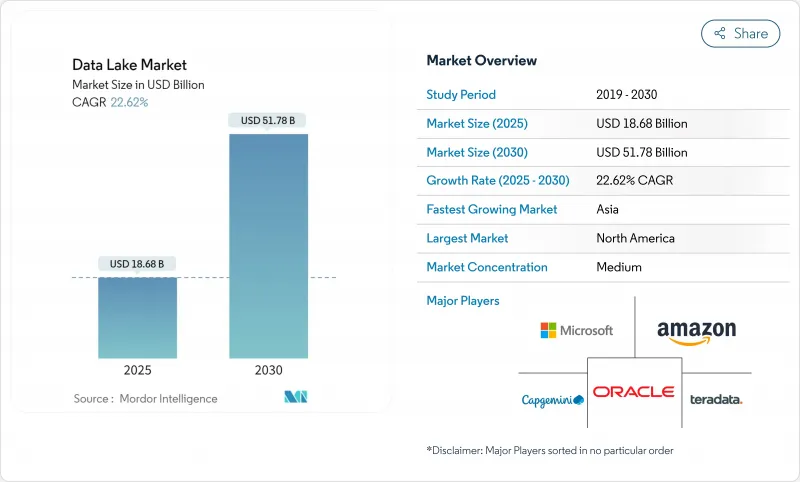

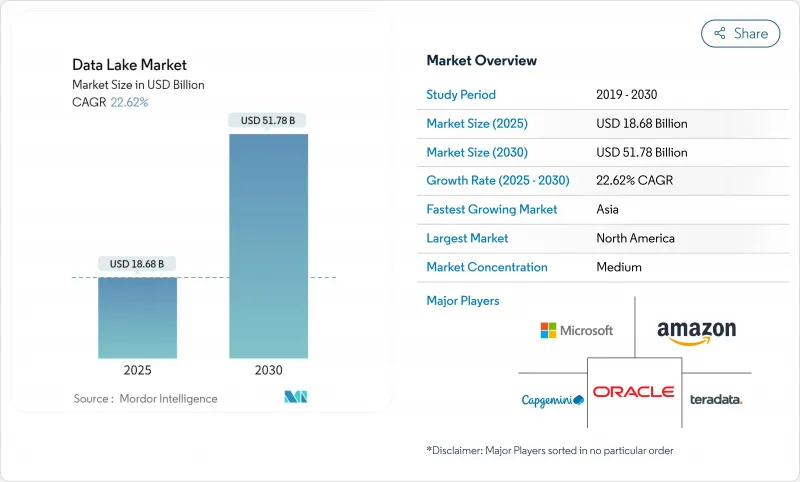

데이터 레이크 시장의 2025년 시장 규모는 186억 8,000만 달러로 평가되었고, 2030년에는 517억 8,000만 달러에 이를 것으로 예상되며 CAGR은 22.62%를 나타낼 전망입니다.

생성형 AI 파이프라인에서 생성되는 비정형 데이터 양의 급증, 확대되는 규제 기록 보관 의무, 그리고 레이크하우스 아키텍처로의 전환이 성장의 원동력입니다. 레이크하우스 아키텍처는 레이크와 웨어하우스의 공간을 단일 계층으로 통합합니다. 포춘 500대 기업들은 레이크하우스 도입 후 총비용의 35-40% 절감 효과를 보고하고 있으며, 실시간 ESG 및 리스크 스트레스 워크로드가 산업 및 금융 분야로 활용 사례를 확장하고 있습니다. 서버리스 오픈 테이블 형식이 이제 멀티클라우드 이동성 전략의 핵심이 되었으며, 혁신을 저해하지 않으면서도 ‘스왑’ 함정을 방지하기 위한 자동화된 거버넌스 계층이 등장하고 있습니다.

세계의 데이터 레이크 시장 동향 및 인사이트

생성형 AI 워크로드로 인한 비정형 및 다중 모드 데이터 폭발

생성형 AI 애플리케이션은 방대한 이미지, 오디오, 텍스트 페이로드를 생성하며, 이는 스키마 온 리드(schema-on-read) 스토리지를 요구합니다. 기업들은 2025년까지 전 세계 175제타바이트 데이터 영역의 30%가 실시간 처리가 필요할 것으로 예상하는데, 이는 경직된 웨어하우스에 부적합한 프로필입니다. 따라서 데이터 레이크는 프롬프트 엔지니어링 루프에 사용되는 다중 모달 코퍼스의 기본 착륙 지점이 됩니다. 구글 클라우드의 레이크하우스 설계도는 벡터 인덱싱과 결합된 네이티브 형식 스토리지가 파운데이션 모델의 미세 조정을 가속화하면서 저장 비용을 절감하는 방식을 보여줍니다. 도입을 지연하는 기업은 AI 워크로드에 대한 혁신 주기가 느려지고 단위 비용이 높아질 위험이 있습니다.

유럽의 데이터 거주지 의무화, 클라우드 기반 레이크 채택 가속화

EU 데이터 거버넌스 법안과 데이터 법안은 조직이 민감한 워크로드를 현지화하도록 강제합니다. 하이퍼스케일러들은 이에 대응 중입니다. AWS는 내장형 데이터 위치 제어 기능을 갖춘 주권 클라우드 리전에 78억 유로를 투자하고 있습니다. 기업들은 이제 거주 규정을 충족하면서도 연방형 엔진을 통해 쿼리 가능한 지역 분할형 데이터 레이크를 전개하며, 감사 보고서에서 국경을 넘는 데이터 사용을 드러낼 수 있는 계보 정보가 풍부한 메타데이터 카탈로그에 대한 수요를 촉발하고 있습니다.

메타데이터 드리프트로 인한 “데이터 늪” 생성

데이터 수집 속도가 카탈로그 업데이트 속도를 앞지르면 데이터 레이크는 검색 불가능한 저장소로 전락합니다. 2025년까지 전 세계 데이터 양은 163제타바이트에 달할 전망이며, 이로 인해 컨텍스트가 누락된 사일로화된 파일의 위험이 높아집니다. 기업들은 유니티 카탈로그(Unity Catalog)와 같은 자동 계보 추적기를 도입하여 대응하고 있습니다. 이 도구는 모든 읽기-쓰기 작업을 기록하고 고아 자산을 표시합니다. 이와 유사한 통제 수단이 없다면, 레이크하우스 통합으로 예상되는 비용 절감 효과가 거버넌스 관리 부담으로 인해 상쇄될 수 있습니다.

부문 분석

솔루션은 2024년 데이터 레이크 시장 매출의 70%를 차지하며, 이는 130억 8천만 달러 규모의 데이터 레이크 시장으로 환산됩니다. 이러한 우위는 기업들이 AI 준비 환경의 핵심을 이루는 스토리지 엔진, 쿼리 가속기, 거버넌스 제품군을 표준화함에 따라 발생합니다. 벤더들은 비용 최적화 대시보드, 자동 계층화, 네이티브 오픈 테이블 지원을 번들로 제공하며, 워크로드가 진화함에 따라 관련성을 유지합니다.

서비스 하위 부문은 2030년까지 연평균 25.8%의 성장률로 급성장 중이며, 이는 마이그레이션 설계도, 성능 튜닝, 연중무휴 관리 운영에 대한 수요를 반영합니다. 많은 기업이 기존 Hadoop 환경을 재구축할 인력이 부족해 예측 가능한 SLA 결과를 보장하는 전문 업체와 계약합니다. 인재 시장이 좁아지면서 전문 서비스 예약은 전체 데이터 레이크 시장보다 빠르게 성장할 것입니다.

2024년 클라우드 전개는 즉각적인 확장성과 통합 보안을 추구하는 기업들로 인해 데이터 레이크 시장 점유율의 65%를 차지했습니다. Amazon S3와 같은 탄력적 객체 저장소는 자본 지출(CapEx)을 제거하면서 콜드 데이터를 저비용 클래스로 자동 계층화하는 라이프사이클 자동화를 제공합니다. 이후 분석 엔진은 수요에 따라 가동되어 컴퓨팅 비용을 프로젝트 진행 속도에 맞춰 조정합니다.

하이브리드 및 멀티클라우드 구성은 2030년까지 연평균 24% 성장률로 확대될 전망입니다. 오픈 테이블 형식은 단일 메타데이터 정의가 온프레미스와 퍼블릭 클라우드 버킷에 걸쳐 적용되도록 하여 복제 요구를 대폭 줄입니다. 지역별 규정 준수 규칙은 기업들이 규제 대상 워크로드를 주권 클라우드 지역에 배치하면서도 크로스클라우드 패브릭을 통해 쿼리할 수 있도록 하여 하이브리드 전략을 더욱 촉진합니다. 결과적으로 하이브리드 환경의 데이터 레이크 시장 규모는 주권 클라우드 출시와 발맞춰 증가하고 있습니다.

지역 분석

북미는 2024년 매출의 38%를 차지했으며 아키텍처 성숙도 측면에서 계속해서 기준을 제시하고 있습니다. 금융 기관들은 진화하는 스트레스 테스트 템플릿을 충족하기 위해 시계열 보존 기간을 연장하고 있으며, 병원 네트워크는 AI 기반 진단을 뒷받침하는 다중 모드 환자 그래프를 구축하고 있습니다. 벤처 캐피털도 거버넌스 스타트업 창업을 촉진하여 활기찬 생태계를 보장합니다.

아시아태평양 지역은 2030년까지 연평균 24.1% 성장률(CAGR)을 기록하며 가장 빠르게 확장되는 지역입니다. 일본, 인도, 싱가포르 정부는 주권 클라우드 프로젝트를 후원하여 지역 규정 준수 레이크 존 수요를 촉진하고 있습니다. 중국 통신사는 용량 계획을 위해 방대한 5G 로그를 분석하는 반면, 인도네시아 핀테크 기업들은 사이버 범죄 억제를 위해 사기 정보 레이크를 공유합니다. 일본의 와사비(Wasabi)처럼 아시아태평양(APAC) 본사를 설립하는 벤더들은 예상되는 36% IaaS 성장세를 포착하려는 목표를 가지고 있습니다.

유럽은 엄격한 데이터 주권 규정 하에서 도입을 가속화하고 있습니다. 유럽 데이터 전략(European Strategy for Data)은 현지 호스팅 투자를 촉진하며, AWS는 거주지 규정 충족을 위해 2025년 말까지 브란덴부르크(Brandenburg) 지역을 개설할 예정입니다. 제조업체들은 CSRD 보고를 위해 실시간 Scope-3 배출량을 저장하고, 은행들은 감사 준비가 완료된 레이크 내에서 바젤 III 계산을 정교화합니다. 유럽 은행 감독청(EBA)의 2025년 스트레스 테스트 템플릿은 레이크하우스가 충족해야 하는 기술적 요구 사항을 강화합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 생성형 AI 워크로드에서 발생하는 비정형 및 다중 모달 데이터의 폭발적 증가

- 유럽의 데이터 거주지 의무화로 가속화되는 클라우드 기반 레이크 도입

- 포춘 500대 기업을 위한 총소유비용(TCO) 35-40% 절감을 주도하는 레이크하우스 통합

- 서버리스 테이블 형식으로 멀티클라우드 이동성 확보

- 산업 부문의 실시간 ESG 범위-3 데이터 수집 요구 사항

- 금융 서비스 분야의 규제 스트레스 테스트로 10년 단위 틱 데이터 보존 요구

- 시장 성장 억제요인

- 메타데이터 드리프트로 인한 “데이터 스왑” 발생 및 거버넌스 비용 증가

- 신흥 지역의 숙련된 레이크 엔지니어링 인재 부족

- 지연 시간에 민감한 워크로드, 여전히 레이크보다 웨어하우스를 선호

- 불투명한 소비 기반 클라우드 가격 정책으로 인한 예산 예측 복잡화

- 기술의 전망

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제공별

- 솔루션

- 데이터 검색 및 카탈로그

- 데이터 통합과 ETL/ELT

- 분석 및 시각화 도구

- 거버넌스 및 보안 플랫폼

- 서비스

- 전문 서비스(컨설팅, 통합)

- 관리형 서비스

- 솔루션

- 전개별

- 클라우드

- 퍼블릭 클라우드

- 프라이빗 클라우드

- 하이브리드/멀티클라우드

- 온프레미스

- 클라우드

- 조직 규모별

- 대기업

- 중소기업(SME)

- 비즈니스 기능별

- 운영 및 공급망

- 금융 및 위험

- 판매 및 마케팅

- 인적 자원

- 업계별

- IT 및 텔레콤

- BFSI

- 헬스케어 및 생명과학

- 소매 및 전자상거래

- 제조업 및 공업

- 미디어 및 엔터테인먼트

- 정부 및 공공 부문

- 에너지 및 유틸리티

- 기타(교육, 접객)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 칠레

- 페루

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 뉴질랜드

- 기타 아시아태평양

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 기타 아프리카

- 북미

제6장 경쟁 구도

- Strategic Developments

- Vendor Positioning Analysis

- 기업 프로파일

- Amazon Web Services(AWS)

- Microsoft Corporation

- Google LLC

- IBM Corporation

- Oracle Corporation

- Snowflake Inc.

- SAP SE

- Cloudera Inc.

- Teradata Corporation

- Informatica Inc.

- Databricks Inc.

- Hitachi Vantara LLC

- Dell Technologies Inc.

- Atos SE

- SAS Institute Inc.

- Zaloni Inc.

- Dremio Corporation

- Qubole Inc.

- Talend SA

- HPE(Ezmeral)

제7장 시장 기회와 장래의 전망

HBR 25.11.17The data lakes market is valued at USD 18.68 billion in 2025 and is on track to reach USD 51.78 billion by 2030, registering a 22.62% CAGR.

Growth stems from surging unstructured data volumes generated by generative-AI pipelines, expanding regulatory record-keeping mandates, and the shift toward lakehouse architectures that collapse lake and warehouse footprints into a single tier. Fortune 500 firms report 35-40% total-cost savings after embracing lakehouses, while real-time ESG and risk-stress workloads are extending use cases into industrial and financial domains. Serverless open-table formats now anchor multi-cloud portability strategies, and automated governance layers are emerging to prevent "swamp" pitfalls without throttling innovation.

Global Data Lake Market Trends and Insights

Explosion of unstructured and multimodal data from GenAI workloads

Generative-AI applications create vast image, audio, and text payloads that demand schema-on-read storage. Enterprises expect 30% of the global 175 zettabyte data sphere to require real-time processing by 2025, a profile unsuited to rigid warehouses. Data lakes therefore become the default landing zone for multi-modal corpora used in prompt-engineering loops.Google Cloud's lakehouse blueprint shows how native-format storage paired with vector indexing accelerates foundation-model fine-tuning while lowering storage bills. Firms delaying adoption risk slower innovation cycles and higher unit-costs on AI workloads.

Data-residency mandates in Europe accelerating cloud-based lake adoption

The EU Data Governance Act and Data Act compel organizations to localize sensitive workloads. Hyperscalers are responding: AWS is investing EUR 7.8 billion in a sovereign-cloud region that ships with embedded data-location controls. Enterprises now deploy region-segmented data lakes that meet residency rules yet remain queryable through federated engines, sparking demand for lineage-rich metadata catalogs capable of surfacing cross-border data usage in audit reports.

Metadata drift creating "data swamps"

When ingestion outpaces catalog updates, data lakes devolve into unsearchable repositories. By 2025, global data volume will reach 163 zettabytes, heightening the risk of siloed files with missing context. Enterprises are responding by adopting automated lineage trackers such as Unity Catalog, which logs every read-write and flags orphaned assets. Without similar controls, governance overhead can erase savings projected from lakehouse consolidation.

Other drivers and restraints analyzed in the detailed report include:

- Lakehouse convergence delivering 35-40% TCO savings

- Serverless table formats unlocking multi-cloud portability

- Skilled lake-engineering talent shortfall in emerging regions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions generated 70% of data lakes market revenue in 2024, equating to a data lakes market size of USD 13.08 billion. The dominance comes from enterprises standardizing on storage engines, query accelerators, and governance suites that form the backbone of AI-ready environments. Vendors bundle cost-optimizer dashboards, automated tiering, and native open-table support, maintaining relevance as workloads evolve.

The services sub-segment is racing ahead at a 25.8% CAGR to 2030, reflecting demand for migration blueprints, performance tuning, and 24X7 managed operations. Many firms lack staff who can re-platform legacy Hadoop estates, so they contract specialists that promise predictable SLA outcomes. The tight talent market ensures professional-services bookings will keep growing faster than the overall data lakes market

Cloud deployments captured 65% of the data lakes market share in 2024 as organizations sought instant scalability and integrated security. Elastic object stores like Amazon S3 eliminate CapEx while delivering lifecycle automation that auto-tiers cold data to low-cost classes. Analytics engines then spin up on demand, keeping compute spend aligned with project tempo.

Hybrid and multi-cloud configurations are expanding at 24% CAGR to 2030. Open-table formats let one metadata definition span on-prem and public-cloud buckets, slashing replication needs. Regional compliance rules further fuel hybrid strategies, as firms pin regulated workloads in sovereign regions yet still query them through cross-cloud fabrics. As a result, the data lakes market size for hybrid environments is rising in lockstep with sovereign-cloud launches.

The Data Lakes Market Report is Segmented by Offering (Solutions, and Services), Deployment (Cloud, and Hybrid/Multi-Cloud), Organization Size (Large Enterprises, and SMEs), Business Function (Operations and Supply-Chain, Finance and Risk, and More), End-User Vertical (IT and Telecom, Healthcare and Life Sciences, and More), and Geography (North America, Asia, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 38% of 2024 revenue and continues to set benchmarks in architecture maturity. Financial institutions lengthen time-series retention to meet evolving stress-test templates, while hospital networks build multimodal patient graphs that underpin AI-driven diagnostics. Venture capital also fuels governance-start-up formation, ensuring a vibrant ecosystem.

Asia-Pacific is the fastest-expanding region, clocking a 24.1% CAGR through 2030. Governments in Japan, India, and Singapore sponsor sovereign-cloud projects, spurring demand for region-compliant lake zones. Telcos in China analyze massive 5G logs for capacity planning, whereas Indonesian fintechs share fraud-intelligence lakes to curb cybercrime. Vendors establishing APAC headquarters, such as Wasabi in Japan, aim to catch the projected 36% IaaS upturn.

Europe accelerates adoption under strict data-sovereignty mandates. The European Strategy for Data drives investment in local hosting, and AWS will open a Brandenburg region by late 2025 to satisfy residency rules. Manufacturers store real-time Scope-3 emissions for CSRD reporting, and banks refine Basel III calculations inside audit-ready lakes. The European Banking Authority's 2025 stress-test templates reinforce technical requirements that lakehouses fulfill.

- Amazon Web Services (AWS)

- Microsoft Corporation

- Google LLC

- IBM Corporation

- Oracle Corporation

- Snowflake Inc.

- SAP SE

- Cloudera Inc.

- Teradata Corporation

- Informatica Inc.

- Databricks Inc.

- Hitachi Vantara LLC

- Dell Technologies Inc.

- Atos SE

- SAS Institute Inc.

- Zaloni Inc.

- Dremio Corporation

- Qubole Inc.

- Talend SA

- HPE (Ezmeral)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosion of Unstructured and Multimodal Data from GenAI Workloads

- 4.2.2 Data-Residency Mandates in Europe Accelerating Cloud-based Lake Adoption

- 4.2.3 Lakehouse Convergence Driving 35-40% TCO Savings for Fortune-500 Firms

- 4.2.4 Serverless Table Formats Unlocking Multi-Cloud Portability

- 4.2.5 Real-Time ESG Scope-3 Data Capture Requirements in Industrial Sector

- 4.2.6 Regulatory Stress-Testing in Financial Services Demanding Decade-Scale Tick Data Retention

- 4.3 Market Restraints

- 4.3.1 Metadata Drift Creating "Data Swamps" and Raising Governance Cost

- 4.3.2 Skilled Lake Engineering Talent Shortfall in Emerging Regions

- 4.3.3 Latency-Sensitive Workloads Still Favoring Warehouses over Lakes

- 4.3.4 Opaque Consumption-Based Cloud Pricing Complicating Budget Forecasts

- 4.4 Technological Outlook

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Offering

- 5.1.1 Solutions

- 5.1.1.1 Data Discovery and Cataloging

- 5.1.1.2 Data Integration and ETL/ELT

- 5.1.1.3 Analytics and Visualization Tools

- 5.1.1.4 Governance and Security Platforms

- 5.1.2 Services

- 5.1.2.1 Professional Services (Consulting, Integration)

- 5.1.2.2 Managed Services

- 5.1.1 Solutions

- 5.2 By Deployment

- 5.2.1 Cloud

- 5.2.1.1 Public Cloud

- 5.2.1.2 Private Cloud

- 5.2.1.3 Hybrid/Multi-Cloud

- 5.2.2 On-Premise

- 5.2.1 Cloud

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Mid-Size Enterprises (SMEs)

- 5.4 By Business Function

- 5.4.1 Operations and Supply-Chain

- 5.4.2 Finance and Risk

- 5.4.3 Sales and Marketing

- 5.4.4 Human Resources

- 5.5 By End-User Vertical

- 5.5.1 IT and Telecom

- 5.5.2 BFSI

- 5.5.3 Healthcare and Life Sciences

- 5.5.4 Retail and E-commerce

- 5.5.5 Manufacturing and Industrial

- 5.5.6 Media and Entertainment

- 5.5.7 Government and Public Sector

- 5.5.8 Energy and Utilities

- 5.5.9 Others (Education, Hospitality)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Peru

- 5.6.2.5 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 Australia

- 5.6.4.5 New Zealand

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Rest of Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Strategic Developments

- 6.2 Vendor Positioning Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.3.1 Amazon Web Services (AWS)

- 6.3.2 Microsoft Corporation

- 6.3.3 Google LLC

- 6.3.4 IBM Corporation

- 6.3.5 Oracle Corporation

- 6.3.6 Snowflake Inc.

- 6.3.7 SAP SE

- 6.3.8 Cloudera Inc.

- 6.3.9 Teradata Corporation

- 6.3.10 Informatica Inc.

- 6.3.11 Databricks Inc.

- 6.3.12 Hitachi Vantara LLC

- 6.3.13 Dell Technologies Inc.

- 6.3.14 Atos SE

- 6.3.15 SAS Institute Inc.

- 6.3.16 Zaloni Inc.

- 6.3.17 Dremio Corporation

- 6.3.18 Qubole Inc.

- 6.3.19 Talend SA

- 6.3.20 HPE (Ezmeral)

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment