|

시장보고서

상품코드

1851799

서버리스 컴퓨팅 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Serverless Computing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

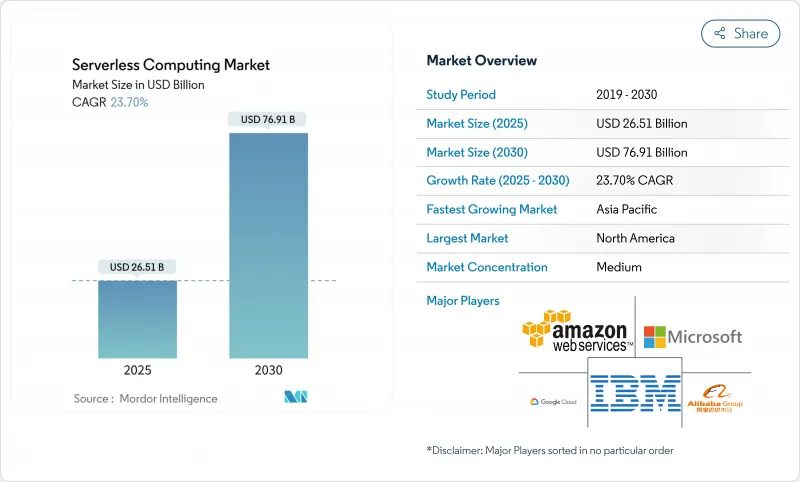

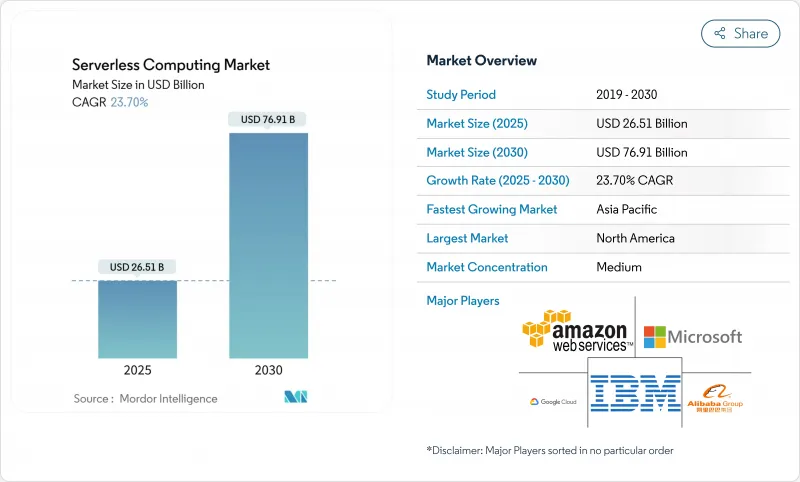

서버리스 컴퓨팅 시장의 2025년 시장 규모는 265억 1,000만 달러로, 2030년에는 769억 1,000만 달러에 이르고, CAGR 23.7%를 나타낼 것으로 예측됩니다.

수요가 증가하고 있는 이유는 개발 팀이 인프라를 관리하지 않고 코드를 작성하고 싶기 때문에 하이퍼스케일 클라우드에는 현재 견고한 관측 가능성, 보안 및 통합 기능이 번들로 제공됩니다. 이벤트 중심의 마이크로서비스, 에지 네이티브 5G 배포, 불규칙하게 확장하면서 초 이하의 응답이 요구되는 실시간 AI 워크로드에 의해 그 기세는 더욱 강해지고 있습니다. 기업은 비용 절감에서 혁신 목표로 전환하고 서버리스를 사용하여 새로운 디지털 제품을 가속화하고 DevSecOps를 자동화하며 데이터 주권 아키텍처를 지원합니다. 퍼블릭 클라우드는 여전히 지배적인 배포 모델이지만, 기업은 최상의 기능과 공급업체 위험의 균형을 고려하기 위해 멀티클라우드 전략이 상승하고 있습니다.

세계의 서버리스 컴퓨팅 시장 동향과 인사이트

북미 BFSI의 현대화로 가속화되는 이벤트 중심 마이크로 서비스로의 이동

은행과 보험 회사는 카드 스 와이프, 대출 견적 및 불법 신호에 거의 실시간으로 반응하는 세분화 된 서비스로 모노리스를 대체하려고합니다. 서버리스 기능을 사용함으로써 북미의 대형 금융기관은 개발 사이클을 35-40% 단축하고 인프라 비용을 28.3% 삭감했습니다. 이 모델의 실행당 과금은 결제 및 부유층 플랫폼에서 일반적인 불규칙한 거래량에 적합합니다. API 우선 설계는 각 기능이 개별적으로 로그, 암호화 및 버전 관리할 수 있으므로 규제 당국의 감사를 단순화할 수 있습니다. 제로 트러스트 규칙이 강화됨에 따라 BFSI 팀은 엄격한 감사 추적을 충족하면서 공격 대상 영역을 줄이는 임시 컴퓨팅을 선호합니다.

유럽의 소매 및 E-Commerce로 급증하는 DevSecOps 대응 멀티 클라우드·파이프라인에 대한 수요

유럽 소매업체는 GDPR(EU 개인정보보호규정)을 준수하면서 인스턴트 체크아웃 및 개인화된 혜택을 수용하기 위한 경쟁을 펼치고 있습니다. 89%는 잠금을 피하고 지역 데이터 레지던시를 유지하기 위해 서버리스 워크로드를 최소한 두 개의 클라우드에 분산시킵니다. 임베디드 정책 엔진은 커밋별로우코드를 스캔하고 보안 테스트를 CI/CD에 통합하며 비밀을 자동 암호화하여 취약성 창을 축소합니다. 보안을 좌천으로 전환하면 팀은 수정에 소요되는 시간을 단축하고 싱글 데이, 블랙 프라이데이 등 계절 피크 시 기능을 신속하게 푸시할 수 있습니다.

고도로 분산된 마이크로 기능에서의 디버깅과 관측 가능성의 격차

기존 APM 에이전트는 몇 밀리초 단위로 작동하는 임시 함수를 추적할 수 없으며 근본 원인 분석 시 맹점이 남아 있습니다. 회사는 서버리스 앱 문제를 해결하는 데 모놀리스의 2.4배가 걸린다고 보고했습니다. 이는 로그가 서비스간에 흩어져 콜드 스타트가 대기 시간의 비정상적인 값을 숨기기 때문입니다. 신흥 솔루션은 현재 경량 스팬 ID를 주입하고 개방형 표준 백엔드로 내보내고 있지만 성숙도는 주류 도구보다 늦습니다. 추적, 메트릭 및 로그가 원활하게 통합될 때까지 위험을 싫어하는 부서는 미션 크리티컬 시스템의 마이그레이션을 망설이는 것으로 보입니다.

부문 분석

기업이 턴키 운영을 선호하기 때문에 매니지드 서비스가 2024년 매출의 62%를 차지했지만, 기업이 복잡한 현대화 프로그램을 추진하고 있기 때문에 전문 서비스는 2030년까지 연평균 복합 성장률(CAGR)이 18.4%를 나타낼 전망입니다. 많은 규제 대상 기업들은 프로덕션 가동 전에 이벤트 스키마 재설계, 모노리스 리팩토링 및 컴플라이언스 검증을 위해 컨설팅 파트너를 채택하고 있습니다. 권고 팀은 서버리스 보안 패턴, 정책 애즈코드, FinOps 대시보드를 통합하여 비즈니스 가치를 극대화합니다.

또한 전문 서비스는 비동기 설계 및 관측 가능성 모범 사례에 대해 제품 팀을 교육하고 기업 문화의 변화를 지원합니다. 서버리스 실적가 애널리틱스, AI, 에지에 퍼지면서 지속적인 거버넌스와 플랫폼 엔지니어링이 번들된 계약에서의 개발 지원에 참여합니다. 이 진화는 통합자에게 이익률이 높은 성장을 유지하는 동시에 기업의 Time-to-Value를 향상시킵니다.

펑션 아즈 어 서비스는 2024년에 지출의 58%를 차지했고 2030년까지 서버리스 컴퓨팅 시장을 지원할 것으로 보입니다. 그러나 Backend-as-a-Service는 인증, 스토리지 및 실시간 동기화를 API 호출에 집계한 보다 고급 구조를 요구하는 팀에 의해 CAGR25%의 성장 부문이 되고 있습니다. 특히 모바일 개발자는 로그인 및 푸시 알림을 위한 원라인 통합을 높이 평가하며, 시작 주기를 몇 주에서 몇 시간으로 단축했습니다.

BaaS는 정형적인 태스크를 오프로드함으로써 FaaS를 보완하고 기능을 차별화된 로직에 집중시킵니다. 통합 API 게이트웨이는 두 패러다임에서 트래픽을 통일적으로 라우팅하고 서버리스 컨테이너는 더 긴 수명의 프로세스를 필요로 하는 성능 격차를 채웁니다. 아키텍트는 비용, 대기 시간 및 규정 준수 요구에 따라 다양한 추상화 기능을 결합하여 사용할 수 있습니다.

지역 분석

북미는 2024년 서버리스 수익의 38%를 차지하며, 풍부한 클라우드 인재, 적극적인 디지털 뱅킹 로드맵, 공격 대상 범위의 축소를 목적으로 한 에피메럴 컴퓨팅을 지지하는 미국 연방 정부의 제로 트러스트 지령에 지지되었습니다. 기업은 서버리스를 활용하여 레거시 스택을 현대화하고 고객의 개인화를 위해 이벤트 스트림을 채택하고 컴플라이언스 가능 로깅 파이프라인을 실행하고 있습니다. 캐나다는 특히 5G 엣지 기능을 통합하는 통신 사업자들 사이에서 이러한 패턴을 반영하고 있으며, 멕시코의 핀텍 신흥 기업은 결제 API를 안전하게 확장하기 위해 서버리스를 채택하고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 19.8%를 나타낼 것으로 예측되는 가장 빠르게 성장하는 지역입니다. 중국의 인터넷 대기업은 네이티브 서버리스 AI 서비스에 투자하고 인도의 급성장하는 SaaS 부문은 예측 불가능한 세계 수요를 관리하기 위해 종량 과금 모델을 채택하고 있습니다. 일본과 한국의 제조업은 예지보전을 위해 엣지 기능을 통합하고, 아세안의 핀테크와 전자상거래 기업은 저지연으로 지역 고객에게 도달하기 위해 멀티클라우드 서버리스 스택을 도입합니다. 5G MEC, 저렴한 클라우드 스팟, 개발자의 기술 향상과 함께 이 지역 전체의 도입이 가속화되고 있습니다.

GDPR(EU 개인정보보호규정)과 국가주권규칙을 충족하기 위해 기업이 멀티클라우드를 채택하면서 유럽은 강력한 지위를 유지하고 있습니다. 영국, 독일, 프랑스는 암호화, 감사, 레지던시에 대한 공통 청사진을 공유하는 소매, 은행 및 공공 부문의 조종사로 선도하고 있습니다. 북유럽 국가들은 환경 친화적인 데이터센터 통합 및 이벤트 기반 에너지 그리드로 한계를 넓히려고합니다. 공급업체는 현지화된 영역과 휴대용 런타임으로 대응하여 보다 엄격한 컴플라이언스 환경에도 불구하고 성장을 강화하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 북미 BFSI의 근대화로 가속하는 이벤트 구동형 마이크로서비스로의 변화

- 유럽의 소매 및 E-Commerce로 DevSecOps 대응의 멀티 클라우드 파이프라인에 대한 수요가 급증

- 엣지 네이티브인 5G MEC의 전개가 아시아 통신 사업자의 서버리스 채용을 촉진

- 실시간 AI/ML 추론 워크로드가 헬스케어에서 FaaS 이용을 촉진

- 정부에 의한 제로 트러스트 의무화에 의해 미국 연방 정부 IT에 있어서 서버리스 보안 툴 체인이 활성화

- LATAM의 핀텍 에코시스템에서 API 매니타이제이션 플랫폼의 급속한 확대

- 시장 성장 억제요인

- 고도로 분산된 마이크로 기능에 있어서 디버그와 관측 가능성의 갭

- 독자적인 이벤트 오케스트레이션 엔진에 의해 증폭되는 벤더 락 인 리스크

- 다중 지역 서버리스 데이터 스토어의 데이터 레지던시 준수 장애물

- 고주파 거래와 게임 워크로드에서의 콜드 스타트 지연 제약

- 밸류체인 분석

- 규제 전망

- 기술 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 투자분석

- 기술 스냅샷

- API 게이트웨이

- Function-as-a-Service(FaaS)

- Backend-as-a-Service(BaaS)

- Database-as-a-Service(DBaaS)

제5장 시장 규모와 성장 예측

- 서비스 모델별

- 전문 서비스

- 관리 서비스

- 서비스 유형별

- Function-as-a-Service(FaaS)

- Backend-as-a-Service(BaaS)

- API 게이트웨이

- Container-as-a-Service(CaaS)

- 배포 모델별

- 퍼블릭 클라우드

- 프라이빗 클라우드

- 하이브리드 클라우드

- 멀티 클라우드

- 최종 사용자 업계별

- IT 및 통신

- BFSI

- 소매 및 전자상거래

- 정부 및 공공 부문

- 헬스케어 및 생명과학

- 산업 및 제조업

- 미디어 및 엔터테인먼트

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 북유럽 국가

- 스웨덴

- 노르웨이

- 덴마크

- 핀란드

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 이집트

- 기타 아프리카

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN

- 기타 아시아태평양

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Amazon Web Services Inc.

- Microsoft Corp.

- Google LLC

- Alibaba Group Holding Ltd.

- IBM Corp.

- Oracle Corp.

- SAP SE

- VMware Inc.

- Red Hat Inc.

- Cloudflare Inc.

- Fastly Inc.

- Tencent Cloud

- Huawei Cloud

- Netlify Inc.

- Vercel Inc.

- DigitalOcean Inc.

- Iron.io

- TriggerMesh Inc.

- Serverless Inc.

- Stackery Inc.

제7장 시장 기회와 향후 전망

KTH 25.11.17The serverless computing market is valued at USD 26.51 billion in 2025 and is forecast to touch USD 76.91 billion by 2030, advancing at a 23.7% CAGR.

Demand is rising because development teams want to write code without managing infrastructure, and hyperscale clouds now bundle robust observability, security and integration capabilities. Momentum is reinforced by event-driven microservices, edge-native 5G deployments, and real-time AI workloads that scale irregularly yet require sub-second response. Enterprises are moving from cost savings to innovation goals, using serverless to speed new digital products, automate DevSecOps and support data-sovereign architectures. Public cloud remains the dominant deployment model, but multi-cloud strategies are gaining ground as enterprises look to balance best-of-breed features with vendor risk.

Global Serverless Computing Market Trends and Insights

Accelerating Shift to Event-Driven Microservices in North American BFSI Modernization

Banks and insurers are replacing monoliths with granular services that react to card swipes, loan quotes and fraud signals in near real time. Using serverless functions, leading North American institutions trimmed development cycles by 35-40% and shaved 28.3% off infrastructure spend, freeing budget for new digital features. The model's pay-per-execute billing fits irregular transaction volumes common in payments and wealth platforms. API-first designs also simplify regulatory audits because each function can log, encrypt and version individually. As zero-trust rules tighten, BFSI teams prefer ephemeral compute that reduces attack surface while meeting stringent audit trails.

Surging Demand for DevSecOps-Ready Multi-Cloud Pipelines Across European Retail and E-commerce

European retailers race to match instant checkout and personalized offers while obeying GDPR. Eighty-nine percent now distribute serverless workloads across at least two clouds to avoid lock-in and maintain regional data residency. Built-in policy engines scan code on every commit, integrate security tests into CI/CD and auto-encrypt secrets, shrinking vulnerability windows. By shifting security left, teams cut remediation time and push features faster during seasonal peaks such as Singles' Day and Black Friday.

Debugging and Observability Gaps in Highly Distributed Micro-Functions

Traditional APM agents cannot trace ephemeral functions that live for milliseconds, leaving blind spots during root-cause analysis. Enterprises report troubleshooting serverless apps takes 2.4 times longer than monoliths because logs scatter across services and cold-starts mask latency outliers. Emerging solutions now inject lightweight span IDs and export them to open-standard back ends, yet maturity lags mainstream tooling. Until traces, metrics and logs consolidate seamlessly, risk-averse sectors will hesitate to migrate mission-critical systems.

Other drivers and restraints analyzed in the detailed report include:

- Roll-out of Edge-Native 5G MEC Driving Serverless Adoption Among Asia Telecom Operators

- Real-Time AI/ML Inference Workloads Propelling Function-as-a-Service Uptake in Healthcare

- Vendor Lock-In Risk Amplified by Proprietary Event Orchestration Engines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Managed Services held 62% of 2024 revenue as organizations prioritized turnkey operations, but Professional Services is expanding at an 18.4% CAGR to 2030 as firms tackle complex modernization programs. Many regulated enterprises hire consulting partners to redesign event schemas, refactor monoliths and validate compliance before going live. Advisory teams integrate serverless security patterns, policy-as-code and FinOps dashboards to maximize business value.

Professional Services also support culture change, training product squads on asynchronous design and observability best practices. As serverless footprints widen to analytics, AI and edge, continuous governance and platform engineering join development assistance in bundled engagements. This evolution sustains high-margin growth for integrators while improving enterprise time-to-value.

Function-as-a-Service captured 58% of spending in 2024 and will keep anchoring the serverless computing market through 2030. Yet Backend-as-a-Service is the star growth segment at 25% CAGR as teams seek higher-level constructs that collapse authentication, storage and real-time sync into API calls. Mobile developers in particular appreciate one-line integration for login and push notifications, cutting launch cycles from weeks to hours.

BaaS complements FaaS by offloading boilerplate tasks, letting functions focus on differentiated logic. Unified API gateways route traffic uniformly across both paradigms, while serverless containers fill performance gaps that demand longer-lived processes. The spectrum of abstractions allows architects to mix and match for cost, latency and compliance needs.

The Serverless Computing Market Report is Segmented by Service Model (Professional Services and Managed Services), Service Type (Function-As-A-Service (FaaS), Backend-As-A-Service (BaaS), and More), Deployment Model (Public Cloud, Private Cloud, and More), End-User Industry (IT and Telecommunications, BFSI, and More), and Geography

Geography Analysis

North America drove 38% of 2024 serverless revenue, supported by abundant cloud talent, aggressive digital banking roadmaps, and U.S. federal zero-trust directives that favor ephemeral compute for reduced attack surface. Enterprises leverage serverless to modernize legacy stacks, employ event streams for customer personalization, and run compliance-ready logging pipelines. Canada mirrors these patterns, especially among telcos integrating 5G edge functions, while Mexico's fintech startups adopt serverless to scale payment APIs securely.

Asia Pacific is the fastest-growing region, projected at 19.8% CAGR to 2030. China's internet majors invest in native serverless AI services, and India's booming SaaS sector embraces the pay-as-you-go model to manage unpredictable global demand. Japanese and South Korean manufacturers integrate edge functions for predictive maintenance, whereas ASEAN fintech and e-commerce players deploy multi-cloud serverless stacks to reach regional customers with low latency. The confluence of 5G MEC, affordable cloud spots and developer upskilling accelerates uptake across the region.

Europe maintains a strong position as organizations adopt multi-cloud to satisfy GDPR and state sovereignty rules. The United Kingdom, Germany and France lead with retail, banking and public-sector pilots that share common blueprints for encryption, audit and residency. Nordic countries push boundaries with green data-center integrations and event-driven energy grids. Vendors respond with localized zones and portable runtimes, reinforcing growth despite stricter compliance landscapes.

- Amazon Web Services Inc.

- Microsoft Corp.

- Google LLC

- Alibaba Group Holding Ltd.

- IBM Corp.

- Oracle Corp.

- SAP SE

- VMware Inc.

- Red Hat Inc.

- Cloudflare Inc.

- Fastly Inc.

- Tencent Cloud

- Huawei Cloud

- Netlify Inc.

- Vercel Inc.

- DigitalOcean Inc.

- Iron.io

- TriggerMesh Inc.

- Serverless Inc.

- Stackery Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating shift to event-driven microservices in North American BFSI modernisation

- 4.2.2 Surging demand for DevSecOps-ready multi-cloud pipelines across European retail and e-commerce

- 4.2.3 Roll-out of edge-native 5G MEC driving serverless adoption among Asia telecom operators

- 4.2.4 Real-time AI/ML inference workloads propelling Function-as-a-Service uptake in healthcare

- 4.2.5 Government Zero-Trust mandates boosting serverless security toolchains in US federal IT

- 4.2.6 Rapid expansion of API monetisation platforms in LATAM fintech ecosystems

- 4.3 Market Restraints

- 4.3.1 Debugging and observability gaps in highly distributed micro-functions

- 4.3.2 Vendor lock-in risk amplified by proprietary event orchestration engines

- 4.3.3 Data residency compliance hurdles for multi-region serverless data stores

- 4.3.4 Cold-start latency constraints in high-frequency trading and gaming workloads

- 4.4 Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

- 4.9 Technology Snapshot

- 4.9.1 API Gateway

- 4.9.2 Function-as-a-Service (FaaS)

- 4.9.3 Backend-as-a-Service (BaaS)

- 4.9.4 Database-as-a-Service (DBaaS)

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Model

- 5.1.1 Professional Services

- 5.1.2 Managed Services

- 5.2 By Service Type

- 5.2.1 Function-as-a-Service (FaaS)

- 5.2.2 Backend-as-a-Service (BaaS)

- 5.2.3 API Gateway

- 5.2.4 Container-as-a-Service (CaaS)

- 5.3 By Deployment Model

- 5.3.1 Public Cloud

- 5.3.2 Private Cloud

- 5.3.3 Hybrid Cloud

- 5.3.4 Multi-Cloud

- 5.4 By End-user Industry

- 5.4.1 IT and Telecommunications

- 5.4.2 BFSI

- 5.4.3 Retail and E-commerce

- 5.4.4 Government and Public Sector

- 5.4.5 Healthcare and Life Sciences

- 5.4.6 Industrial and Manufacturing

- 5.4.7 Media and Entertainment

- 5.4.8 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Nordics

- 5.5.4.1 Sweden

- 5.5.4.2 Norway

- 5.5.4.3 Denmark

- 5.5.4.4 Finland

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Rest of Africa

- 5.5.7 Asia Pacific

- 5.5.7.1 China

- 5.5.7.2 India

- 5.5.7.3 Japan

- 5.5.7.4 South Korea

- 5.5.7.5 ASEAN

- 5.5.7.6 Rest of Asia Pacific

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amazon Web Services Inc.

- 6.4.2 Microsoft Corp.

- 6.4.3 Google LLC

- 6.4.4 Alibaba Group Holding Ltd.

- 6.4.5 IBM Corp.

- 6.4.6 Oracle Corp.

- 6.4.7 SAP SE

- 6.4.8 VMware Inc.

- 6.4.9 Red Hat Inc.

- 6.4.10 Cloudflare Inc.

- 6.4.11 Fastly Inc.

- 6.4.12 Tencent Cloud

- 6.4.13 Huawei Cloud

- 6.4.14 Netlify Inc.

- 6.4.15 Vercel Inc.

- 6.4.16 DigitalOcean Inc.

- 6.4.17 Iron.io

- 6.4.18 TriggerMesh Inc.

- 6.4.19 Serverless Inc.

- 6.4.20 Stackery Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment