|

시장보고서

상품코드

1851805

임상화학 분석기 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Clinical Chemistry Analyzers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

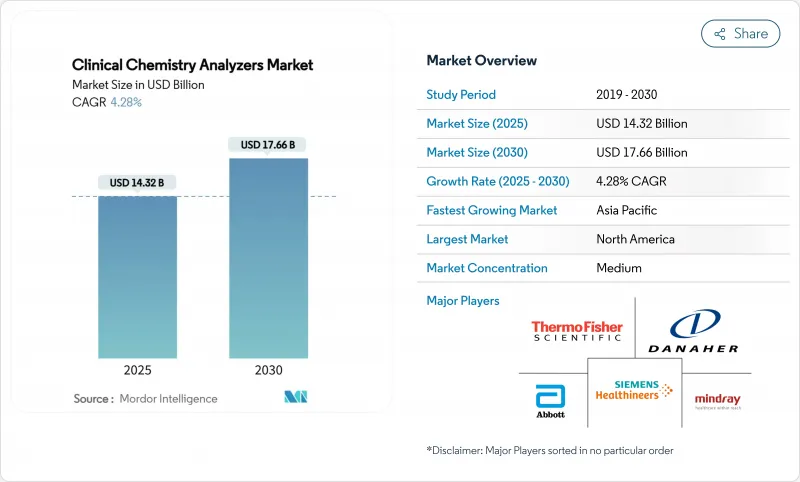

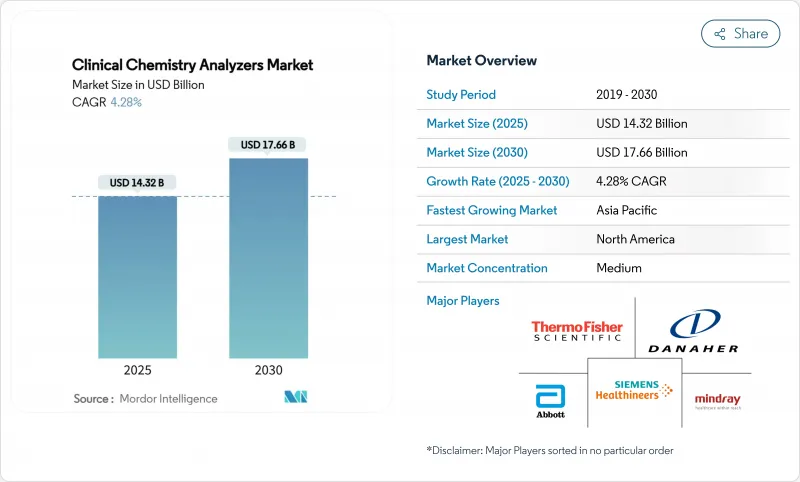

임상화학 분석기 시장 규모는 2025년에 143억 2,000만 달러, 2030년에는 176억 6,000만 달러에 이를 것으로 예상되며, 예측 기간 중 CAGR은 4.28%를 나타낼 전망입니다.

이러한 꾸준한 확장은 자동화, 인공지능, 데이터 중심 워크플로우가 점점 가치 창출을 정의하게 되는 성숙하면서도 탄력적인 분야를 반영합니다. 높은 처리량 장비에 대한 수요가 증가함에 따라 통합 인포매틱스에 대한 축족과 결합하여 조달 결정을 재구성하고 이전과 같은 검사량 증가에 대한 의존도를 완화하고 있습니다. 공급업체는 현재 시약 번들뿐만 아니라 가동 시간, 예지 보전 및 미들웨어의 상호 운용성으로 차별화를 도모하고 있습니다. 병원 통합, POC(Point-of-Care) 확대, 만성질환 감시가 1일 검사 건수를 좌우하는 한편, 설비투자 사이클에서는 검사 메뉴 확대에 맞추어 필드 업그레이드가 가능한 모듈형 분석기가 지지되고 있습니다. 신흥 지역의 가격 압력과 사이버 보안 강화는 여전히 역풍이지만, 중기 전망은 인구 역학 변화와 특수 바이오 마커의 일상 화학 플랫폼으로의 전환에 의해 지원되며 임상화학 분석기 시장의 지속적인 수요를 확실히하고 있습니다.

세계의 임상화학 분석기 시장 동향과 인사이트

고령화와 만성질환 부담

인구 역학의 급속한 노화로 인해 만성 질환 검사의 요구가 증가하고 있으며, 대사 패널, 심장 마커 및 신장 기능 분석에 대한 수요가 날마다 높아지고 있습니다. 당뇨병, 심혈관 장애, 만성 신장 질환의 스크리닝 및 모니터링 프로토콜은 더욱 엄격해지고 인구 증가보다 빠르게 검사량 곡선이 증가하고 있습니다. 자동 반복 및 반사 검사 옵션을 갖춘 고처리량 분석기는 이러한 검사량 증가에 대응하는 데 필요한 확장성을 제공하며, 실험실은 이에 비례하여 인원을 늘리지 않고 미래의 용량을 확보할 수 있습니다. 워크플로 시뮬레이터와 예측 분석을 패키징한 장비 공급업체는 자본 입찰에서 우위를 차지할 수 있습니다. 성숙한 헬스케어 시스템에서 성과보상형 상환으로 임상화학 분석기 시장은 예방의료 프로그램의 최전선 자원으로서 더욱 견고해집니다. 장기적으로는 인구동태의 기세로 일시적인 지출감퇴가 있어도 지속적인 검사량이 확보됩니다.

중환자 치료 현장에서 POC(Point-of-Care) 채용

응급실과 집중 치료실에서는 몇 시간이 아닌 몇 분 이내에 결과를 반환하는 환자에 가까운 화학 패널에 대한 의존도가 높아지고 있습니다. 고감도 심근 트로포닌, 젖산, 신진 대사 평가는 현재 신속한 방아쇠의 지침이되어 심근 경색과 패혈증의 경로에서 문에서 바늘까지의 시간을 단축하고 있습니다. 바이오메루에 의한 1억 1,100만 유로의 스핀칩 다이아그노스틱스 인수는 10분 이내의 심근 마커 회수를 목표로 한 전략적 투자의 전형입니다. 장치가 소형화됨에 따라 중앙 실험실과의 분석 격차가 줄어들면서 분산형 워크플로우는 시료 운송 지연과 입원 기간을 단축하여 지불자와 의료 제공업체의 가치를 높입니다. 그 결과, 벤치탑 시스템과 일회용 마이크로플루이딕스 카트리지는 임상화학 분석기 시장에서 고성장 틈새 시장으로 자리매김하고 있습니다.

숙련된 임상검사기사 부족

미국의 화학부문의 결원률은 17.3%, 실험실 전체의 결원률은 46%이며, 스킬 격차의 확대를 나타내고 있습니다. 채용 지연은 아기 붐 세대의 퇴직, 제한된 교육 프로그램의 능력, 그리고 전문직의 사회적인지도의 낮음에 기인합니다. 미들웨어의 자동화는 수작업을 줄이는 반면, 품질 관리 플래그와 복잡한 결과 해석을 감독하려면 여전히 면허가있는 직원이 필요합니다. 검사실은 크로스 트레이닝, 자격 요건 완화, 급여 할증 등으로 대응하고 있지만, 수급 미스매치는 여전히 계속되고 있습니다. 제조업체는 직관적인 사용자 인터페이스, 자동 검증 알고리즘 및 원격 진단이 노동력 부족에 대항하는 제품의 필수 조건이되어 임상화학 분석 장비 업계의 가치 제안을 강화하고 있습니다.

부문 분석

시약 부문은 2024년 임상화학 분석기 시장 규모의 58.51%를 차지하고 실험실 현금 흐름을 지원하는 소모품 모델이 정착되어 있음을 반영했습니다. 검량선, 대조군, 효소 기재에 대한 수요는 경상적인 검사량에 의해 지원되기 때문에 수익은 예측 가능합니다. 그러나 설비투자는 보다 빠른 처리량, AI를 활용한 유지보수, 통합된 분석 메뉴를 약속하는 완전 자동화 분석기 플랫폼에 기울고 있으며, 그 결과 2030년까지 분석기의 CAGR 예측은 8.25%를 나타낼 전망입니다. 장비 구매는 미들웨어 라이선스와 클라우드 대시보드가 총 솔루션 계약에 번들로 제공되는 경우가 늘어나 구성 요소 가격에서 결과 기반 조달로의 전환을 시사합니다.

벤치탑형 분석기의 출하대수는 POC(Point-of-Care)의 확대와 급성기 패널의 구급병동에의 재배치를 배경으로, 스탠드형 분석기를 웃도는 성장을 나타내고 있습니다. 벤더는 카트리지의 인체공학, 샘플 추적성, 가동 시간을 극대화하는 빠른 QC 잠금 해제 시간 등으로 차별화를 도모하고 있습니다. 시약 기술 혁신의 핵심은 장착 안정성 연장, 검사 당 플라스틱 양 감소, 재고 분석에 도움이 되는 바코드 팩 추적 기능을 갖춘 액체 안정 제제입니다. 고감도 심근 트로포닌과 신흥 패혈증 마커를 위한 특수 화학물질은 기초 대사 시약의 가격 하락을 부분적으로 상쇄해, 비싼 마진을 가져옵니다. 소모품이 기본적인 수익을 보장하는 반면 하드웨어 업그레이드가 점진적인 효율화를 가능하게 하는 균형 잡힌 생태계는 임상화학 분석기 시장의 장기적인 수요를 강화하고 있습니다.

지역 분석

북미는 2024년 매출의 34.32%를 차지하며 견조한 보험상환, 급속한 AI 도입, 차세대 분석기의 밀집한 설치 베이스가 그 기반이 되었습니다. FDA의 LDT 최종 규칙은 컴플라이언스 비용을 상승시키는 한편, 검증된 시스템과 문서를 대규모로 제공할 수 있는 기존 공급업체를 고정화하는 높은 규제의 장애물을 굳히고, 이 지역의 전체적인 매출세를 강화하고 있습니다. 유럽은 견조한 교체 수요로 이어지지만, IVDR 주도의 재인증 작업이 제조업체의 자원에 부담을 주기 때문에 이것을 극복해야 합니다.

아시아태평양의 CAGR은 7.71%로 활황을 보이며 미래의 세계 임상화학 분석기 시장 규모에 크게 기여할 것으로 예측됩니다. 중국은 지방 병원 통합 및 만성 질환 검진의 의무화에 힘입어 수량 기준 조달 방식이 공급업체의 가격 결정력에 도전하고 있음에도 불구하고 수량 성장을 이끌고 있습니다. 인도와 동남아시아 국가들은 민간 파트너십을 통해 농촌 지역에 대한 진단 보급 활동을 가속화하고 벤치탑형 및 반자동 분석기의 채용을 뒷받침하고 있습니다. 라틴아메리카와 중동 및 아프리카는 환율 변동의 영향을 받기 쉬운 것, 의료 보험의 확대와 검사 인프라의 현대화에 따라 1자리대 중반의 성장률을 나타내고 있습니다. 시약 팩의 크기, 대출 조건, 필드 서비스의 실적를 지역의 실정에 맞추어 조정하는 벤더가 불균형한 점유율을 획득하고 있으며, 임상화학 분석기 시장에서의 결정적인 성공 요인으로서 지역 특유의 실행력이 강조되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 고령화와 만성질환 부담

- 중환자 치료에 있어서 POC(Point-of-Care)의 채용

- AI를 활용한 하이 스루풋 오토메이션

- 폭넓은 대사/특수화학 검사 메뉴

- 에너지 효율 분석기 도입을 위한 지속가능성 추진

- 분석기 생성 데이터의 수익화

- 시장 성장 억제요인

- 숙련된 임상검사기사의 부족

- 높은 자본 비용과 유지 보수 비용

- 희토류 의존 시약 공급 위험

- 사이버 보안 및 컴플라이언스 오버헤드 증가

- 기술 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제품 유형별

- 분석기

- 바닥 설치형 고처리량

- 모듈식/통합 시스템

- 벤치탑

- 반자동

- 시약

- 교정제 및 대조군

- 소모품

- 기타(QC재료, 소프트웨어 라이선스)

- 분석기

- 검사 유형별

- 기본 대사 패널

- 전해질 패널

- 간 기능 패널

- 지질 프로파일

- 갑상선 기능 패널

- 신장 기능 패널

- 심장 마커

- 특수 화학 검사

- 최종 사용자별

- 병원

- 독립 진단 연구소

- 학술 및 연구 기관

- POC(Point-of-Care) 센터

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Abbott Laboratories

- Danaher Corp.(Beckman Coulter)

- F. Hoffmann-La Roche Ltd

- Siemens Healthineers

- Thermo Fisher Scientific

- Horiba Ltd

- Sysmex Corp.

- Mindray Medical

- Johnson & Johnson(Ortho Clinical)

- Elitech Group

- Hitachi High-Tech

- Randox Laboratories

- DIRUI Industrial

- Bio-Rad Laboratories

- Shenzhen Mindray Bio-Medical

- Agappe Diagnostics

- Xylem Analytics(YSI)

- Erba Mannheim

- Tecom Science

- Medica Corp.

- Diasys Diagnostics

제7장 시장 기회와 향후 전망

KTH 25.11.17The clinical chemistry analyzers market size stands at USD 14.32 billion in 2025 and is projected to reach USD 17.66 billion by 2030, advancing at a 4.28% CAGR during the forecast period.

The steady expansion reflects a maturing yet resilient space where automation, artificial intelligence, and data-centric workflows increasingly define value creation. Heightened demand for high-throughput instruments, combined with a pivot toward integrated informatics, is reshaping procurement decisions and softening the historic reliance on sheer test-volume growth. Vendors now differentiate by uptime, predictive maintenance, and middleware interoperability rather than reagent bundling alone. Hospital consolidation, point-of-care expansion, and chronic-disease surveillance continue to anchor daily test volumes, while capital investment cycles favor modular analyzers that can be field-upgraded as assay menus widen. Price pressures in emerging regions and stricter cybersecurity mandates remain headwinds, but the medium-term outlook is buoyed by demographic shifts and the migration of specialty biomarkers onto routine chemistry platforms, ensuring persistent demand for the clinical chemistry analyzers market.

Global Clinical Chemistry Analyzers Market Trends and Insights

Aging Population & Chronic-Disease Burden

Rapid demographic aging is intensifying chronic-disease testing needs, lifting daily demand for metabolic panels, cardiac markers, and renal function assays. Screening and monitoring protocols for diabetes, cardiovascular disorders, and chronic kidney disease have grown more stringent, producing test-volume curves that rise faster than population growth. High-throughput analyzers with auto-repeat and reflex testing options deliver the scalability required to keep pace with this influx, enabling laboratories to future-proof capacity without proportionate staffing increases. Instrument vendors that package workflow simulators and predictive analytics enjoy a competitive edge in capital tenders. In mature healthcare systems, pay-for-outcome reimbursement further cements the clinical chemistry analyzers market as a frontline resource for preventive care programs. Long term, demographic momentum ensures durable test volumes even amid episodic spending slowdowns.

Point-of-Care Adoption in Critical Care Settings

Emergency departments and intensive care units increasingly depend on near-patient chemistry panels that return results within minutes rather than hours. High-sensitivity cardiac troponin, lactate, and metabolic assessments now guide rapid triage, reducing door-to-needle times in myocardial infarction and sepsis pathways. bioMerieux's EUR 111 million move for SpinChip Diagnostics typifies strategic investment aimed at 10-minute cardiac marker turnaround. As device miniaturization narrows the analytical gap with central labs, decentralised workflows slash specimen transport delays and hospital length-of-stay, amplifying value for payers and providers. The resulting demand updraft positions benchtop systems and disposable microfluidic cartridges as high-growth niches within the clinical chemistry analyzers market.

Shortage of Skilled Lab Technologists

Vacancy rates of 17.3% in U.S. chemistry departments and 46% across total laboratory positions underline a widening skills gap. Recruitment lags stem from retiring baby-boom cohorts, limited training program capacity, and muted public visibility of the profession. While middleware automation eases manual workloads, oversight of quality-control flags and complex result interpretation still demands licensed staff. Laboratories respond with cross-training, relaxed credential prerequisites, and salary premiums, yet the supply-demand mismatch endures. For manufacturers, intuitive user interfaces, auto-verification algorithms, and remote diagnostics become product imperatives to counter workforce scarcity, reinforcing value propositions inside the clinical chemistry analyzers industry.

Other drivers and restraints analyzed in the detailed report include:

- AI-Enabled High-Throughput Automation

- Broader Metabolic/Specialty Chemistry Test Menu

- High Capital & Maintenance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The reagents segment accounted for 58.51% of clinical chemistry analyzers market size in 2024, reflecting the entrenched consumable model that underwrites laboratory cash flow. Revenues remain predictable as recurrent test volumes anchor demand for calibrators, controls, and enzyme substrates. Yet capital investments are tilting toward fully automated analyzer platforms that promise faster throughput, AI-backed maintenance, and consolidated assay menus, resulting in an 8.25% CAGR forecast for analyzers through 2030. Instrument purchases increasingly include middleware licenses and cloud dashboards bundled into total-solution contracts, signaling a shift from component pricing to outcome-based procurement.

Benchtop analyzers are outpacing floor-standing units in shipment growth, powered by point-of-care expansion and the repatriation of acute panels into emergency wards. Vendors differentiate via cartridge ergonomics, sample traceability, and rapid QC unlock times that maximize uptime. Reagent innovation centers on liquid-stable formulations with extended onboard stability, trimmed plastic volume per test, and barcoded pack tracking that feeds inventory analytics. Specialty chemicals for high-sensitivity cardiac troponin and emerging sepsis markers deliver premium margins, partially offsetting price erosion in basic metabolic reagents. The combined effect is a balanced ecosystem where consumables guarantee baseline revenue while hardware upgrades unlock step-change efficiency, fortifying long-term demand for the clinical chemistry analyzers market.

The Clinical Chemistry Analyzers Market Report is Segmented by Product Type (Analyzers [Floor-Standing High-Throughput, and More], Reagents, and Others), Types of Test (Basic Metabolic Panel, Liver Panel, Electrolyte Panels, and More), End User (Hospitals, Independent Diagnostic Laboratories, and More) and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 34.32% of 2024 revenue, anchored by robust reimbursement, rapid AI adoption, and a dense installed base of next-generation analyzers. The FDA's LDT Final Rule, while elevating compliance costs, cements a high regulatory bar that entrenches incumbent suppliers who can furnish validated systems and documentation at scale, bolstering overall sales momentum within the region. Europe follows with steady replacement demand but must navigate IVDR-driven re-certification workloads that tax manufacturer resources.

Asia-Pacific is forecast to post a vigorous 7.71% CAGR, driving outsized contribution to future global clinical chemistry analyzers market size. China leads volume growth, propelled by provincial hospital consolidation and chronic-disease screening mandates, even as volume-based-procurement schemes challenge vendor pricing power. India and Southeast Asian nations accelerate rural diagnostic outreach via public-private partnerships, boosting benchtop and semi-automated analyzer adoption. Latin America and the Middle East & Africa present mid-single-digit trajectories tied to health-insurance expansion and laboratory infrastructure modernization, albeit vulnerable to currency volatility. Vendors that tailor reagent pack sizes, financing terms, and field-service footprints to local realities capture disproportionate share, underscoring geography-specific execution as a decisive success factor in the clinical chemistry analyzers market.

- Abbott Laboratories

- Danaher Corp. (Beckman Coulter)

- Roche

- Siemens Healthineers

- Thermo Fisher Scientific

- HORIBA

- Sysmex Corp.

- Mindray Medical

- Johnson & Johnson (Ortho Clinical)

- Elitech Group

- Hitachi High-Tech

- Randox Laboratories

- DIRUI Industrial

- Bio-Rad Laboratories

- Shenzhen Mindray Bio-Medical

- Agappe Diagnostics

- Xylem Analytics (YSI)

- Erba Mannheim

- Tecom Science

- Medica Corp.

- Diasys Diagnostics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging Population & Chronic-Disease Burden

- 4.2.2 Point-Of-Care Adoption In Critical Care Settings

- 4.2.3 AI-Enabled High-Throughput Automation

- 4.2.4 Broader Metabolic/Specialty Chemistry Test Menu

- 4.2.5 Sustainability Push For Energy-Efficient Analyzers

- 4.2.6 Monetization Of Analyzer-Generated Data

- 4.3 Market Restraints

- 4.3.1 Shortage Of Skilled Lab Technologists

- 4.3.2 High Capital & Maintenance Costs

- 4.3.3 Rare-Earth-Dependent Reagent Supply Risk

- 4.3.4 Rising Cybersecurity & Compliance Overhead

- 4.4 Technological Outlook

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Analyzers

- 5.1.1.1 Floor-standing High-Throughput

- 5.1.1.2 Modular/Integrated Systems

- 5.1.1.3 Benchtop

- 5.1.1.4 Semi-automated

- 5.1.2 Reagents

- 5.1.2.1 Calibrators & Controls

- 5.1.2.2 Consumables

- 5.1.3 Others (QC Materials, Software Licenses)

- 5.1.1 Analyzers

- 5.2 By Types of Test

- 5.2.1 Basic Metabolic Panel

- 5.2.2 Electrolyte Panel

- 5.2.3 Liver Panel

- 5.2.4 Lipid Profile

- 5.2.5 Thyroid Function Panel

- 5.2.6 Renal Function Panel

- 5.2.7 Cardiac Markers

- 5.2.8 Specialty Chemistries

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Independent Diagnostic Laboratories

- 5.3.3 Academic & Research Institutes

- 5.3.4 Point-of-Care Centers

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Danaher Corp. (Beckman Coulter)

- 6.3.3 F. Hoffmann-La Roche Ltd

- 6.3.4 Siemens Healthineers

- 6.3.5 Thermo Fisher Scientific

- 6.3.6 Horiba Ltd

- 6.3.7 Sysmex Corp.

- 6.3.8 Mindray Medical

- 6.3.9 Johnson & Johnson (Ortho Clinical)

- 6.3.10 Elitech Group

- 6.3.11 Hitachi High-Tech

- 6.3.12 Randox Laboratories

- 6.3.13 DIRUI Industrial

- 6.3.14 Bio-Rad Laboratories

- 6.3.15 Shenzhen Mindray Bio-Medical

- 6.3.16 Agappe Diagnostics

- 6.3.17 Xylem Analytics (YSI)

- 6.3.18 Erba Mannheim

- 6.3.19 Tecom Science

- 6.3.20 Medica Corp.

- 6.3.21 Diasys Diagnostics

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment