|

시장보고서

상품코드

1852065

보조생식기술(ART) 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Assisted Reproductive Technology (ART) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

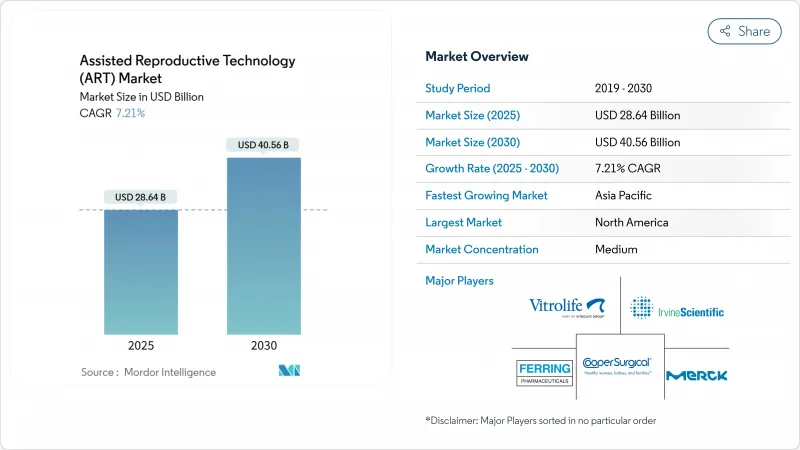

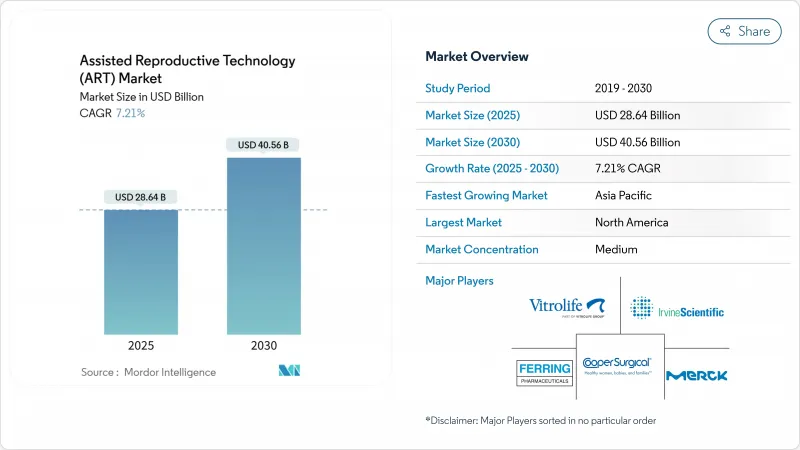

세계의 보조생식기술 시장 규모는 2025년 286억 4,000만 달러로, CAGR 7.21%를 반영하여 2030년까지 405억 6,000만 달러로 확대될 것으로 예측됩니다.

인공지능(AI)이 배아 선택에 있어서 70-97%의 정밀도를 달성하고, 임상 판단을 개선하는 동시에 검사실의 작업량을 삭감하기 때문에 도입이 가속됩니다. Astorg는 Hamilton Thorne을 54%의 프리미엄으로 인수하기로 합의했으며, 미션 크리티컬 실험실 플랫폼에 대한 신뢰를 제시했습니다. 미국에서는 고용자 부담의 불임치료 급여금이 노동자의 40-42%를 커버하게 되어, 지불 대상이 되는 환자층이 확대되어, 보조생식기술 시장의 수익이 안정되고 있습니다. 지역별로는 아시아태평양의 급속한 클리닉 전개와 중국의 불임치료 정책 지원이 급성장을 견인하고 유럽은 국경을 넘어 품질기준을 조화시키는 2027년 인간 유래 물질 규제와 정책에 대비하고 있습니다.

세계 보조생식기술(ART) 시장 동향과 통찰

세계 불임증 유병률 상승

아시아태평양의 여성 불임은 현저하게 증가해, 다낭성 난소 증후군(PCOS)이 주요 요인으로 꼽힙니다. 중동국가의 인구불임률은 38.5%로 임상불임률의 3.8%를 훨씬 웃돌아 잠재 수요가 큰 것으로 나타났습니다. 도시 지역의 스트레스, 식생활 변화, 직업 유해 물질 등 라이프 스타일의 변화는 연령층을 넘어 생식에 관한 건강을 더욱 먹고 있습니다. 정책 입안자들은 불임을 조직적 개입이 필요한 공중 보건 문제로 파악할 수 있게 되었습니다. 이러한 요인이 결합되어 보조생식기술 시장의 장기적인 수량 성장이 유지됩니다.

보조생식기술 절차의 수용 확대

인도의 조직화된 클리닉 체인은 현재 국내 체외수정(IVF) 주기의 35-40%를 차지하고 있으며, 이는 10년 전에는 없었기 때문에 낙인의 저하와 브랜드 주도의 통합을 나타내고 있습니다. 폴란드가 2025년에 체외수정(IVF)의 변제를 부활시킴으로써, EU 회원국 모두가 체외수정(IVF)에 자금을 제공하게 되었습니다. 미국 기업은 인재 획득을 위해 불임치료를 추진해, 종업원의 66%가 생식의료에 관한 특전을 중시해 취업처를 결정했습니다. LGBTQIA+ 인구, 한부모, 유명인들이 불임 치료를 지원하고 불임 치료 인지도를 높입니다. 사회적 개방성은 환자 유입을 촉진하고 보조생식기술 시장의 지불자 구성을 안정시킵니다.

높은 치료비와 제한된 보험 적용

미국의 체외수정(IVF)은 1주기당 평균 1만 2,000-2만 5,000달러로, 통상 2.5주기가 필요하므로 많은 가구는 3만 달러를 넘는 지출을 부담하게 됩니다. 불임 치료의 부분적인 보험 적용을 의무화하는 것은 미국의 21개 주 뿐이며 큰 격차가 있습니다. 치료에 들어가는 직원의 28% 가까이 부채를 갖고 있으며 사회에서 소외된 그룹에 불균형한 부담을 강요하고 있습니다. 국제적으로는 주기의 비용은 EU의 많은 나라에서 4,000유로부터, 선진 아시아에서는 보다 높은 레벨까지 다양해, 후속 케어를 단편화할 수 있는 국외에의 의료 투어리즘에 박차를 가하고 있습니다. 보다 광범위한 상환이 없으면 비용은 보조생식기술 시장 진입의 가장 큰 장벽입니다.

부문 분석

기기 및 장치는 2024년 매출액의 53.45%를 차지했고, 배양, 영상, 배우자의 마이크로매니퓰레이션을 위한 고액 자본 자산에 대한 실험실의 의존을 부조하고 있습니다. 소프트웨어 및 AI 솔루션은 클리닉이 이식 확률을 높이는 예측 분석을 추구하는 가운데 2030년까지 연평균 복합 성장률(CAGR) 9.65%로 성장할 것으로 보입니다. 공급업체는 EmbryoScope에 iDAScore를 결합하는 등 현미경 및 AI 알고리즘을 번들로 통합하여 의사결정 지원 워크플로우를 제공합니다. 자동화의 선구자인 Conceivable Life Sciences는 최초의 완전 로봇 IVF 실험실인 AURA를 도입하여 인력을 줄이면서 연간 2,000 사이클을 처리하고 있습니다.

반복 소모품은 여전히 중요합니다. 배양액의 매출은 채란 때마다 새로운 배치가 만들어지므로 불황기에서도 수익을 안정시킬 수 있습니다. 한편, 보조생식기술 기술 시장 규모는 제조업체가 지속적인 소프트웨어 업데이트 및 원격 교정을 위한 구독 모델을 도입하고 있기 때문에 검사실 서비스 계약과 관련하여 확대되고 있습니다. 이러한 하드웨어와 소프트웨어의 하이브리드 제공은 스위칭 비용을 심화시켜보다 안정적인 현금 흐름을 창출하고 개인 자금 자본을 끌어들입니다.

디지털화는 또한 머신러닝 모델에 공급하는 데이터 공유 네트워크를 촉진하여 채용 기업과 후발 기업의 성능 격차를 확대합니다. AI 할당 프로토콜을 사용하는 클리닉에서는 표준화된 모범 사례로 체인 획득 후 성공률이 13.6% 높다고 보고되었습니다. 2025년부터 2030년까지 제품 로드맵은 단일 장비에서 일회용 및 고유 데이터 세트를 모두 수익화하는 클라우드 지원 에코시스템에 대한 명확한 축족을 보여줍니다.

체외수정(IVF)의 2024년 점유율은 64.34%로 기술적 우위성을 유지해 수십년에 걸친 노하우와 광범위한 상환의 혜택을 받고 있습니다. 그러나 선택적 동결전수 전략은 동결배 교환주기의 CAGR을 9.57%로 밀어 올립니다. 냉동 배아 교환 사이클은 염색체 스크리닝을 허용하고 호르몬 관련 자궁 내막의 스트레스 없이 유연한 스케줄을 구성 할 수 있습니다. 유리화 + 단일 배아 이식 프로토콜 후 다태 임신의 감소가 클리닉에서 보고되었습니다.

새로운 과학이 기술 스택을 재구성하고 있습니다. Fertilo로 대표되는 인공 다능성 줄기 세포법은 치료 기간을 3일로 단축하는 한편, 난소 자극에 대한 노출을 80% 감소시킬 수 있습니다. 체외 배우자 형성 연구는 심각한 남성 요인과 동성 커플에게 새로운 부모가 될 길을 열 수있는 실험실에서 자라는 배우자를 시사합니다. 현재 인공수정은 보다 복잡성이 낮은 옵션으로 존속하고 있지만, 지불자가 투자액당 전체적인 성공률을 높게 인식하고 있기 때문에 체외수정(IVF)의 변종에 점유율을 드러내고 있습니다.

임상의는 유리화 배아, PGT-A 유전학적 검사, AI 스코어링을 조합한 기술 번들을 환자 고유의 예후 예측에 맞추어 조정하는 것이 늘어나고 있으며, 유산 위험을 줄이면서 생아 출생당 비용을 최적화하고 있습니다. 이러한 개인화는 노인 환자가 치료 가능성을 조사하게 되고 보조생식기술 시장이 더욱 확대될 것입니다.

지역 분석

북미는 2024년 매출액의 45.43%를 차지했으며, 프리미엄 가격과 높은 주기 비용을 흡수하는 고용주 급여의 상승에 지지되고 있습니다. 이 지역의 보조생식기술 시장 규모는 현재 진행중인 자동화 시험과 생물 의학 회랑 주변에 모이는 소프트웨어 벤더의 생태계를 반영합니다. 반면 캐나다의 단일 보험 제도는 제한된 주기만을 다루기 때문에 일부 환자는 미국의 민간 서비스를 요구하게 되어 국경을 넘어서는 흐름이 유지되고 있습니다.

아시아태평양은 2030년까지의 CAGR이 8.65%로 예측되며 지역별로는 가장 빠릅니다. 인도에서는 매년 60-70개의 체외수정(IVF) 시설이 신설되어 가격에 민감한 도시 부부에 어필하는 브랜드화된 품질 보증에 의해 조직 체인이 꾸준히 점유율을 획득하고 있습니다. 중국 정부는 출생률 감소로 불임 치료를 추진하고, 지방 보조금을 제공하며, 보다 많은 클리닉 인가를 승인하고 있습니다. 아시아태평양의 보조생식기술 시장 규모는 2028년까지 135억 달러에 이를 것으로 예측되며, 저렴한 가격과 유능한 케어를 모두 요구하는 외국인 환자를 끌어들이는 비용 재정 거래에 지지되고 있습니다.

유럽은 성숙하면서도 발전도상의 양상을 나타내고 있습니다. 2025년에 폴란드 정책이 철회된 후 공적 자금이 보편화되었기 때문에 국가별 격차는 해소되었지만 대기 환자 수에는 큰 변동이 있습니다. 인구동태적으로 유럽의 출생률은 여성 1인당 1.46명으로 여전히 대체 출생률보다 낮아 수요가 장기화되고 있습니다. 2027년 SoHO 규정은 품질 지표와 추적성을 표준화하고 EU 지역 내의 환자를 고용량 센터로 원활하게 유도할 수 있습니다. 스페인, 덴마크, 벨기에는 이미 대량의 외국인 주기를 받아들이고 있으며 EU의 데이터 등록을 공유함으로써 투명성과 치료 성적이 향상되고 보조생식기술 시장에서 유럽의 역할이 강화될 수 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 A

제2장 소개

- 조사의 전제조건과 시장의 정의

- 조사 범위

제3장 조사 방법

제4장 주요 요약

제5장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 세계 불임 인구 증가

- 보조생식기술의 수용 확대

- 생식의료에서 급속한 기술 혁신

- 국경을 넘은 불임 치료 서비스의 성장

- 배아 선별에서 인공지능의 통합

- 고용주 부담 불임치료 급여 확대

- 시장 성장 억제요인

- 높은 치료비와 한정된 보험 적용

- 엄격히 진화하는 규제 프레임워크

- 배아 조작에 관한 윤리적 및 종교적 우려

- 임상적 편차와 불확실한 성공률

- 규제 상황

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제6장 시장 규모와 성장 예측

- 제품 및 서비스별

- 계측기기

- 시약 및 미디어

- 소프트웨어 및 AI 솔루션

- 기술별

- 체외수정(IVF)

- 인공수정(AI-IUI)

- 동결배이식(FER)

- 기타 기술

- 수속별

- 신선 비 기증자

- 신선 기증자

- 냉동 기증자

- 냉동 비 기증자

- 최종 사용자별

- 불임 치료 클리닉

- 병원 및 수술센터

- 크라이오뱅크 및 연구기관

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제7장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- CooperSurgical Inc.

- Vitrolife AB

- FUJIFILM Irvine Scientific Inc.

- Ferring BV

- Merck KGaA(EMD Serono)

- Hamilton Thorne Ltd.

- Thermo Fisher Scientific Inc.

- Cook Medical Inc.

- Genea Biomedx

- Bloom IVF Centre

- Esco Medical

- Memmert GmbH Co.KG

- Laboratoire CCD

- Nidacon International AB

- Microm Ltd.

- Progyny Inc.

- OvaScience Inc.

- CCRM Fertility

- Igenomix

- Gyntics Medical Products

제8장 시장 기회와 장래의 전망

- 화이트 스페이스 및 미충족 요구 평가

The assisted reproductive technology market size generated USD 28.64 billion in 2025 and is forecast to advance to USD 40.56 billion by 2030, reflecting a 7.21% CAGR.

Adoption accelerates as artificial intelligence (AI) reaches 70-97% accuracy in embryo selection, improving clinical decisions while cutting laboratory workload. Private-equity capital flows underscore sector resilience, exemplified by Astorg's agreement to buy Hamilton Thorne at a 54% premium, signalling confidence in mission-critical laboratory platforms. Employer-sponsored fertility benefits now cover 40-42% of United States workers, broadening the paying patient pool and stabilising revenues for the assisted reproductive technology market. Regionally, Asia-Pacific's rapid clinic roll-out and China's fertility policy support drive the fastest growth, while Europe readies for the 2027 Regulation on Substances of Human Origin that will harmonise quality standards across borders.

Global Assisted Reproductive Technology (ART) Market Trends and Insights

Rising Global Infertility Prevalence

Female infertility in Asia-Pacific rose markedly, with polycystic ovary syndrome (PCOS) cited as a major driver. Demographic infertility in some Middle-Eastern countries stands at 38.5%, far above the 3.8% clinical infertility rate, indicating large latent demand. Lifestyle shifts-urban stress, dietary change, occupational toxins-further erode reproductive health across age groups. Policymakers increasingly frame infertility as a public-health issue requiring systematic intervention. Together, these factors sustain long-run volume growth for the assisted reproductive technology market.

Increasing Acceptance of Assisted Reproductive Procedures

Organised Indian clinic chains now capture 35-40% of national IVF cycles-up from zero 10 years ago-showing stigma decline and brand-led consolidation. All EU members fund IVF after Poland reinstated reimbursement in 2025, signalling pan-European support. U.S. companies promote fertility benefits to attract talent; 66% of employees weigh reproductive-health perks in job decisions. Visibility rises as LGBTQIA+ populations, single parents and celebrity advocates normalise usage. Societal openness drives patient inflows and stabilises payer mix for the assisted reproductive technology market.

High Treatment Costs and Limited Insurance Coverage

United States IVF averages USD 12,000-25,000 per cycle, with 2.5 cycles typically needed, thrusting many households above USD 30,000 in expenses. Only 21 U.S. states mandate partial infertility coverage, leaving sizeable gaps. Nearly 28% of employees entering treatment incur debt, disproportionately burdening marginalized groups. Internationally, cycle costs vary from EUR 4,000 in many EU states to higher levels in developed Asia, spurring outbound medical tourism that can fragment follow-up care. Without broader reimbursement, cost remains the steepest barrier to assisted reproductive technology market participation.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Technological Innovations in Reproductive Medicine

- Growth of Cross-Border Fertility Services

- Stringent and Evolving Regulatory Frameworks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Instruments & Equipment generated 53.45% of 2024 revenue, underscoring laboratories' dependence on high-value capital assets for incubating, imaging and micromanipulating gametes. Software & AI Solutions will grow at 9.65% CAGR to 2030 as clinics chase predictive analytics that boost implantation odds. Vendors increasingly bundle microscopes with AI algorithms-such as EmbryoScope+ paired with iDAScore-to offer an integrated decision-support workflow. Automation pioneers including Conceivable Life Sciences deploy AURA, the first fully robotic IVF lab, processing 2,000 cycles a year while slashing headcount.

Recurring consumables remain crucial. Culture media sales track cycle volume because every retrieval triggers new batches, stabilising revenue even during downturns. Meanwhile, the assisted reproductive technology market size linked to laboratory service contracts is expanding as manufacturers introduce subscription models for continuous software updates and remote calibration. These hybrid hardware-software offerings deepen switching costs and create stickier cash flows, attracting private-equity capital.

Digitalisation also fosters data-sharing networks that feed machine-learning models, widening performance gaps between adopters and laggards. Clinics using AI allocation protocols have reported 13.6% higher success rates after chain acquisition due to standardised best practices. Over 2025-2030, product roadmaps show a clear pivot from stand-alone instruments toward cloud-enabled ecosystems that monetise both disposables and proprietary datasets.

In-Vitro Fertilisation preserved technological primacy with 64.34% 2024 share, benefiting from decades of know-how and broad reimbursements. Yet elective freeze-all strategies fuel a 9.57% CAGR for Frozen Embryo Replacement cycles, which allow chromosomal screening and flexible scheduling without hormone-related endometrial stress. Clinics report fewer multiple pregnancies after vitrification plus single-embryo transfer protocols-an increasingly mandated quality metric.

Emerging science reshapes the technology stack. Induced-pluripotent-stem-cell methods, exemplified by Fertilo, could lower ovarian stimulation exposure by 80% while compressing treatment duration to three days. Research into in-vitro gametogenesis hints at lab-grown gametes that may open new parenthood routes for severe male-factor or same-sex couples. For now, artificial insemination persists as a lower-complexity option but surrenders share to IVF variants as payers recognise higher overall success per investment.

Clinicians increasingly tailor technology bundles-combining vitrified embryos, PGT-A genetic testing and AI scoring-to patient-specific prognostics, reducing miscarriage risk while optimising cost per live birth. That personalisation further enlarges the assisted reproductive technology market as older patients consider treatment viable.

The Assisted Reproductive Technology Market Report is Segmented by Product & Service (Instruments & Equipment, and More), Technology (In-Vitro Fertilisation (IVF), and More), Procedure (Fresh Non-Donor, and More), End User (Fertility Clinics, and More), Geography (North America, Europe, Asia-Pacific, The Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America controlled 45.43% of 2024 revenue, buoyed by premium pricing and rising employer benefits that absorb high cycle costs. The assisted reproductive technology market size in this region also reflects ongoing automation pilots and an ecosystem of software vendors clustered around biomedical corridors. U.S. reimbursement expansion through corporate plans continues to offset uneven state mandates, whereas Canada's single-payer system covers limited cycles, prompting some patients to seek private U.S. services and sustaining cross-border flows.

Asia-Pacific is projected to exhibit an 8.65% CAGR to 2030, the fastest among regions. India opens 60-70 new IVF facilities annually, with organised chains steadily capturing share through branded quality guarantees that appeal to price-sensitive urban couples. China's government promotes fertility following birth-rate declines, offering provincial subsidies and approving more clinic licences. The assisted reproductive technology market size for Asia-Pacific is forecast to reach USD 13.5 billion by 2028, supported by cost arbitrage that attracts foreign patients seeking both affordability and competent care.

Europe presents a mature yet evolving picture. Universal public funding after Poland's policy reversal in 2025 eliminates national gaps, yet waiting lists vary widely. Demographically, Europe's fertility rate of 1.46 births per woman remains below replacement, prolonging demand. The 2027 SoHO regulation will standardise quality metrics and traceability, potentially smoothing intra-EU patient redirection to high-capacity centers. Spain, Denmark and Belgium already host large volumes of foreign cycles, and shared EU data registries could enhance transparency and outcomes, reinforcing Europe's role in the assisted reproductive technology market.

- The Cooper Companies

- Vitrolife

- FUJIFILM Irvine Scientific Inc.

- Ferring Pharmaceuticals

- Merck

- Hamilton Thorne Ltd.

- Thermo Fisher Scientific

- Cook Group

- Genea Biomedx

- Bloom IVF Centre

- Esco Lifesciences

- Memmert

- Laboratoire CCD

- Nidacon International

- Microm Ltd.

- Progyny Inc.

- Ovascience

- CCRM Fertility

- Igenomix

- Gyntics Medical Products

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 A

2 Introduction

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

3 Research Methodology

4 Executive Summary

5 Market Landscape

- 5.1 Market Overview

- 5.2 Market Drivers

- 5.2.1 Rising Global Infertility Prevalence

- 5.2.2 Increasing Acceptance of Assisted Reproductive Procedures

- 5.2.3 Rapid Technological Innovations in Reproductive Medicine

- 5.2.4 Growth of Cross-Border Fertility Services

- 5.2.5 Integration of Artificial Intelligence in Embryo Selection

- 5.2.6 Expansion of Employer-Sponsored Fertility Benefits

- 5.3 Market Restraints

- 5.3.1 High Treatment Costs and Limited Insurance Coverage

- 5.3.2 Stringent and Evolving Regulatory Frameworks

- 5.3.3 Ethical And Religious Concerns Regarding Embryo Manipulation

- 5.3.4 Clinical Variability and Uncertain Success Rates

- 5.4 Regulatory Landscape

- 5.5 Porter's Five Forces Analysis

- 5.5.1 Threat Of New Entrants

- 5.5.2 Bargaining Power Of Buyers

- 5.5.3 Bargaining Power Of Suppliers

- 5.5.4 Threat Of Substitutes

- 5.5.5 Competitive Rivalry

6 Market Size & Growth Forecasts (Value, USD)

- 6.1 By Product & Service

- 6.1.1 Instruments & Equipment

- 6.1.2 Reagents & Media

- 6.1.3 Software & AI Solutions

- 6.2 By Technology

- 6.2.1 In-Vitro Fertilisation (IVF)

- 6.2.2 Artificial Insemination (AI-IUI)

- 6.2.3 Frozen Embryo Replacement (FER)

- 6.2.4 Other Technology

- 6.3 By Procedure

- 6.3.1 Fresh Non-Donor

- 6.3.2 Fresh Donor

- 6.3.3 Frozen Donor

- 6.3.4 Frozen Non-Donor

- 6.4 By End User

- 6.4.1 Fertility Clinics

- 6.4.2 Hospitals & Surgical Centres

- 6.4.3 Cryobanks & Research Institutes

- 6.5 Geography

- 6.5.1 North America

- 6.5.1.1 United States

- 6.5.1.2 Canada

- 6.5.1.3 Mexico

- 6.5.2 Europe

- 6.5.2.1 Germany

- 6.5.2.2 United Kingdom

- 6.5.2.3 France

- 6.5.2.4 Italy

- 6.5.2.5 Spain

- 6.5.2.6 Rest of Europe

- 6.5.3 Asia-Pacific

- 6.5.3.1 China

- 6.5.3.2 Japan

- 6.5.3.3 India

- 6.5.3.4 Australia

- 6.5.3.5 South Korea

- 6.5.3.6 Rest of Asia-Pacific

- 6.5.4 Middle East & Africa

- 6.5.4.1 GCC

- 6.5.4.2 South Africa

- 6.5.4.3 Rest of Middle East & Africa

- 6.5.5 South America

- 6.5.5.1 Brazil

- 6.5.5.2 Argentina

- 6.5.5.3 Rest of South America

- 6.5.1 North America

7 Competitive Landscape

- 7.1 Market Concentration

- 7.2 Market Share Analysis

- 7.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 7.3.1 CooperSurgical Inc.

- 7.3.2 Vitrolife AB

- 7.3.3 FUJIFILM Irvine Scientific Inc.

- 7.3.4 Ferring B.V.

- 7.3.5 Merck KGaA (EMD Serono)

- 7.3.6 Hamilton Thorne Ltd.

- 7.3.7 Thermo Fisher Scientific Inc.

- 7.3.8 Cook Medical Inc.

- 7.3.9 Genea Biomedx

- 7.3.10 Bloom IVF Centre

- 7.3.11 Esco Medical

- 7.3.12 Memmert GmbH + Co.KG

- 7.3.13 Laboratoire CCD

- 7.3.14 Nidacon International AB

- 7.3.15 Microm Ltd.

- 7.3.16 Progyny Inc.

- 7.3.17 OvaScience Inc.

- 7.3.18 CCRM Fertility

- 7.3.19 Igenomix

- 7.3.20 Gyntics Medical Products

8 Market Opportunities & Future Outlook

- 8.1 White-Space & Unmet-Need Assessment