|

시장보고서

상품코드

1852147

탄소나노튜브 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Carbon Nanotubes - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

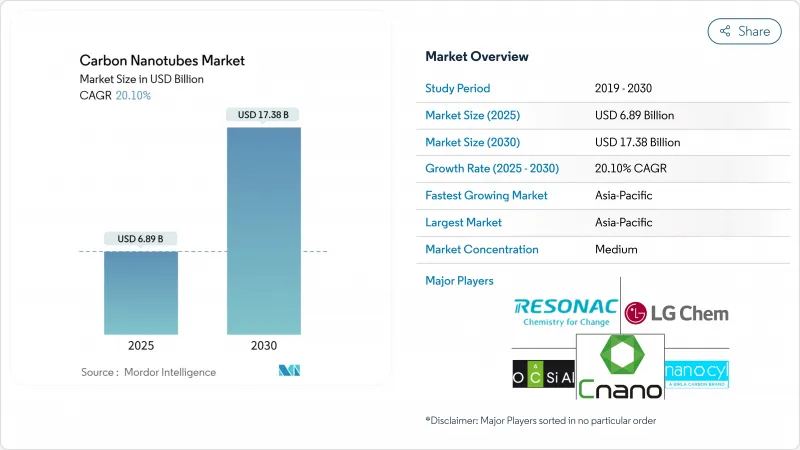

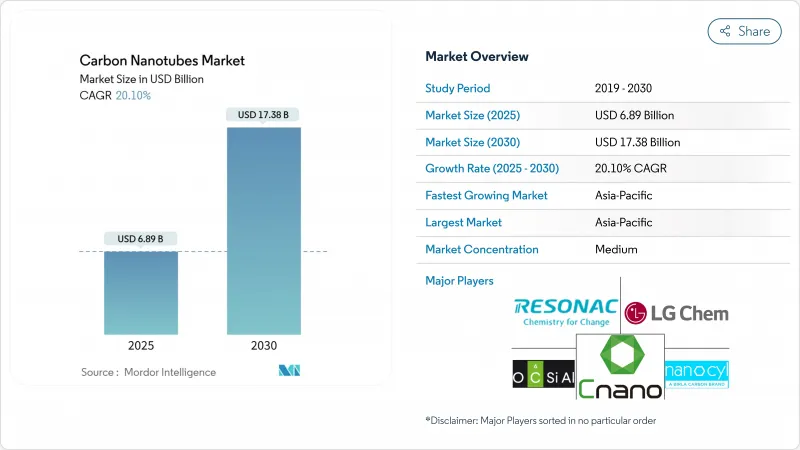

탄소나노튜브 시장 규모는 2025년에 68억 9,000만 달러, 예측기간(2025-2030년) CAGR은 20.10%를 나타내고, 2030년에는 173억 8,000만 달러에 달할 것으로 예측됩니다.

이 긍정적인 전망은 배터리, 항공우주 복합재료, 건강 관리 장비, 수용액 등에이 재료가 빠르게 채택되고 있음을 반영합니다. 멀티월 변종은 여전히 비용 효율적이기 때문에 생산자는 높은 순도와 균일성을 추구하면서 생산량을 확대하고 있습니다. 아시아태평양은 전기자동차와 일렉트로닉스의 클러스터에 지지되어 수요·생산 능력 모두에 계속 우세합니다. OCSiAl에 의한 Zyvex Technologies의 인수는 단층 탄소나노튜브의 규모와 지적 재산을 강화했습니다.

세계의 탄소나노튜브 시장 동향과 통찰

E모빌리티 붐이 CNT 수요를 가속

탄소나노튜브는 실리콘 부하가 20% 가까이에서도 전도성과 기계적 안정성을 확보하여 항속 거리 불안을 경감하는 300Wh/kg의 리튬 이온 팩을 가능하게 합니다. 자동차 제조업체는 또한 파워 일렉트로닉스에서 발생하는 열을 방산시키는 나노튜브 충전 열 인터페이스 패드를 지정하고 있으며, 다우와 커바이스의 2024년 제휴가 이 요구에 대응하고 있습니다. 동일한 전도성의 장점은 버스 바 및 배터리 팩 쉴드의 가능성을 확장합니다. 실리콘-CNT 복합 애노드를 제조하는 신흥 기업은 벤처 자금을 모으고 있으며 상업적인 자신감을 뒷받침하고 있습니다. 셀 제조업체가 공급망을 현지화함에 따라 나노튜브의 생산능력 향상이 기가팩토리 근처에 배치되어 재료와 배터리 생산의 통합이 강화되고 있습니다.

기술 국경을 확장하는 고 에너지 밀도 스토리지

그리드 스토리지 및 항공우주 분야에서는 보다 가볍고 안전한 배터리가 필요합니다. 탄소나노튜브 비계를 이용한 리튬 유황 전지는 황을 고정하여 다황화물의 셧링을 억제합니다. 비틀린 단층 탄소나노튜브 로프는 기계적 에너지로서 2.1MJ/kg을 축적하여 가연성 전해질을 피하면서 리튬 이온의 에너지 밀도를 상회합니다. 슈퍼커패시터·제조업체는 급속 충방전에 이상적인 낮은 등가 직렬 저항을 실현하기 위해서, 다층 전극을 채용하고 있습니다. 이러한 진보는 높은 전도성 등급과 분산 서비스의 안정적인 주문으로 이어집니다.

직업독성학과 규제 강화

서양 당국은 석면에 필적하는 섬유질이기 때문에 흡입 노출 제한 초안을 만들고 있습니다. 학술 그룹은 공기 중 질량과 종횡비를 폐 반응과 연관시키기 위해 선량 측정을 개선했습니다. 컴플라이언스 준수는 완전 밀폐형 반응기 및 자동 가방 포장 라인에 대한 투자를 촉진하여 신규 진출기업의 설비 투자액을 인상하고 있습니다. 안전처리 기록을 문서화한 기업은 기업의 지속가능성 지표가 중시되는 자동차 및 항공우주 프로그램에서 계약을 확보하고 있습니다.

부문 분석

멀티월 탄소나노튜브는 2024년 점유율의 90%를 차지했고, 이는 성숙한 화학 기상 성장법에 의한 생산과 벌크 첨가제와 동일한 가격대를 반영합니다. 이 부문의 CAGR은 20.51%로 예측되며 2030년까지 탄소나노튜브 시장 규모 확대의 3분의 2 이상을 지원합니다. 입자 기술자는 외경의 허용오차를 좁히고, 금속 촉매를 100ppm 이하로 줄이고, 전자기기나 의료기기의 임계치에 적합하게 하고 있습니다. 이러한 개선은 전도성 페이스트, 휴대폰 스피커, 슈퍼커패시터의 전극 채용을 촉진하고 양적 리더십을 강화합니다.

단층 탄소나노튜브의 점유율은 10% 미만에 그치고 있지만, 양자 및 반도체 틈새 분야에서는 프리미엄 가격을 유지하고 있습니다. 정전 촉매는 현재 직경 0.95nm에서 99.92%의 반도체 순도를 실현하여 플렉서블 기판상의 박막 트랜지스터를 가능하게 합니다. 갇힌 칼빈의 조사는 포토닉스를 위한 미래의 1차원 도체를 시사합니다. 틈새 장치가 상용화됨에 따라 탄소나노튜브 시장은 다층 벌크 수요를 구축하지 않고도 높은 수익 증분을 얻게 될 것으로 보입니다.

지역 분석

아시아태평양은 2024년 세계 수요의 54%를 차지했고 CAGR 21.51%로 주도권을 유지했습니다. 중국의 종합적인 배터리 공급 생태계는 장기 계약에 따라 기가팩토리에 공급하는 현지 나노 튜브 제조업체의 촉매제입니다. 일본 기업은 '초성장'법의 높은 종횡비와 배열 품질을 활용하여 디스플레이용 초클린 단층 등급을 전문으로 하고 있습니다. 한국과 인도에서는 정부 우대 조치로 2027년까지 생산 능력이 더욱 확대되고 지역 비용 우위가 확대됩니다.

북미는 총 매출에 크게 기여했습니다. 미국에서는 미시간주 생산을 위한 캐봇사에 5,000만 달러의 에너지부 보조금 교부 등의 노력으로 공급안전보장이 국내 배터리 및 방위분야 고객에게 가까워지고 있습니다. 항공우주용 복합재료와 고주파 커넥터는 국립연구소의 연구개발의 강점을 살린 주요 수요의 기둥입니다. 캐나다에서는 나노튜브의 제품별을 이용한 메탄수소 열분해에 중점을 둔 파일럿 플랜트가 가동되고 있어 기후정책과 제조정책을 연결하고 있습니다.

유럽도 매출 전체에 큰 점유율을 차지하고 있습니다. 독일과 프랑스의 자동차 제조업체들은 엄격한 재료 추적성을 요구하고 요람에서 게이트까지의 배출을 증명하기 위해 공급업체에 일하고 있습니다. 영국 대학은 반도체 상호 연결을 목표로 하는 벤처 기업을 스핀아웃시켜 국가의 나노 패브리케이션 허브에 의해 지원되고 있습니다. 그 주변에서는 중동의 해수담수화기관과 아프리카의 통신탑 설치업자가 물과 에너지의 과제를 해결하기 위해 나노튜브·코팅막과 전도성 코팅을 평가하여 새로운 수요를 개척하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- E모빌리티 붐이 CNT 수요 가속

- 고에너지 밀도 리튬 이온과 슈퍼커패시터 생산의 비약

- 항공우주 분야에서의 초경량 구조 컴포지트의 추진

- MEA와 아시아에 있어서의 해수담수화와 환경 센서의 보급

- 전도성 필라멘트의 적층 조형 통합

- 시장 성장 억제요인

- 구미의 노동독성학과 나노규제

- 열 응용에서 그래핀과 질화붕소 나노튜브의 경쟁

- 라이선싱 비용이 집중되는 특허 시케인

- 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

- 특허 분석

제5장 시장 규모와 성장 예측(금액 및 수량)

- 유형별

- 다중벽 탄소나노튜브 시장

- 단일벽 탄소나노튜브 시장

- 기타 유형(암 의자, 지그재그, 더블 월)

- 제조방법별

- 화학 기상 성장(CVD)

- 고압 일산화탄소(HiPco)

- 아크 방전

- 레이저 어블레이션

- 최종 이용 산업별

- 전기 및 전자

- 에너지

- 자동차

- 항공우주 및 방위

- 헬스케어

- 기타 산업(섬유, 건설, 플라스틱, 복합재료)

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 이탈리아

- 프랑스

- 스페인

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Applied Nanostructures, Inc.

- Arkema

- Cabot Corporation

- Carbon Solutions, Inc.

- CHASM

- Cheap Tubes

- Chengdu Organic Chemicals Co., Ltd.

- CNT Co., Ltd.

- FutureCarbon GmbH

- Hanwha Group

- Hyperion Catalysis International

- Jiangsu Cnano Technology Co., Ltd.

- Kumho Petrochemical

- LG Chem

- Meijo Nano Carbon Co.,Ltd

- Nano-C

- Nanocyl SA

- OCSiAl

- Raymor Industries Inc.

- Resonac Holdings Corporation

- Thomas Swan & Co., Ltd.

- Toray Industries, Inc.

- Zyvex Technologies

제7장 시장 기회와 장래의 전망

SHW 25.11.19The Carbon Nanotubes Market size is estimated at USD 6.89 billion in 2025, and is expected to reach USD 17.38 billion by 2030, at a CAGR of 20.10% during the forecast period (2025-2030).

The strong outlook reflects the material's rapid adoption in batteries, aerospace composites, healthcare devices and water solutions. Multi-walled variants remain cost-efficient, so producers are scaling output while pursuing higher purity and uniformity. Asia-Pacific continues to dominate both demand and production capacity, helped by the region's electric-vehicle and electronics clusters. Consolidation among leading suppliers is gathering pace, illustrated by OCSiAl's purchase of Zyvex Technologies, which strengthened single-walled carbon nanotube scale and intellectual-property depth.

Global Carbon Nanotubes Market Trends and Insights

E-mobility boom accelerating CNT demand

Rising electric-vehicle output is lifting graphite anode silicon content, and carbon nanotubes ensure conductivity and mechanical stability at silicon loads near 20%, enabling 300 Wh/kg lithium-ion packs that reduce range anxiety. Automakers also specify nanotube-filled thermal interface pads that dissipate heat generated by power electronics, a need addressed by Dow and Carbice's 2024 alliance. The same conductivity advantage opens opportunities in busbars and battery-pack shielding. Start-ups producing silicon-CNT composite anodes have attracted venture funding, underscoring commercial confidence. As cell makers localize supply chains, nanotube capacity additions are being colocated near gigafactories, tightening integration between materials and battery production.

High-energy-density storage pushing technical frontiers

Grid storage and aerospace sectors require lighter, safer cells. Lithium-sulfur batteries using carbon-nanotube scaffolds anchor sulfur and suppress polysulfide shuttling, which is central to Lyten's 200 MWh plant targeted for 2025 ramp-up. Twisted single-walled carbon nanotube ropes store 2.1 MJ/kg as mechanical energy, exceeding lithium-ion energy density while avoiding flammable electrolytes. Supercapacitor makers employ multi-walled electrodes to deliver low equivalent-series resistance, ideal for rapid charge-discharge duty. Together, these advances translate to steady orders for high-conductivity grades and dispersion services.

Occupational toxicology and tightening regulation

European and U.S. agencies are drafting inhalation-exposure limits, citing fiber-like dimensions comparable with asbestos. Academic groups are refining dosimetry to link airborne mass and aspect ratio to pulmonary response. Compliance drives investment in fully enclosed reactors and automated bagging lines, raising capex for newcomers. Companies with documented safe-handling records secure contracts in automotive and aerospace programs where corporate sustainability metrics weigh heavily.

Other drivers and restraints analyzed in the detailed report include:

- Aerospace composites raising performance bar

- Desalination & sensor innovations aiding water-stressed regions

- Competition from graphene and boron-nitride nanotubes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Multi-walled carbon nanotubes accounted for 90% of 2024 share, reflecting mature chemical vapor deposition output and price points aligned with bulk additives. The segment is forecast to log a 20.51% CAGR, underpinning more than two-thirds of the carbon nanotubes market size expansion through 2030. Particle engineers are narrowing outer-diameter tolerance and reducing metal catalysts below 100 ppm, meeting electronics and medical-device thresholds. These improvements encourage adoption in conductive pastes, cell-phone speakers and supercapacitor electrodes, reinforcing volume leadership.

Single-walled carbon nanotubes remain under 10% by share yet command premium pricing in quantum and semiconductor niches. Electrostatic catalysis now yields 99.92% semiconducting purity at 0.95 nm diameter, enabling thin-film transistors on flexible substrates. Research on confined carbyne suggests future one-dimensional conductors for photonics. As niche devices commercialize, the carbon nanotubes market will capture incremental high-margin revenue without displacing multi-walled bulk demand.

The Carbon Nanotubes Market Report Segments the Industry by Type (Multi-Walled Carbon Nanotubes, Single-Walled Carbon Nanotubes, and Other Types), Manufacturing Method (Chemical Vapor Deposition (CVD), High-Pressure Carbon Monoxide (HiPco), and More), End-Use Industry (Electrical and Electronics, Energy, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa).

Geography Analysis

Asia-Pacific held 54% of global demand in 2024, and its 21.51% CAGR will sustain leadership. China's integrated battery-supply ecosystem catalyzes local nanotube manufacturers that supply gigafactories under long-term contracts. Japanese firms specialize in ultra-clean single-walled grades for displays, leveraging the "super-growth" method's high aspect ratios and alignment quality. Government incentives across South Korea and India further expand capacity through 2027, widening the regional cost advantage.

North America contributed a significant share to the total revenue. U.S. initiatives, including a USD 50 million Department of Energy grant to Cabot Corporation for Michigan production, shift supply security closer to domestic battery and defense customers. Aerospace composites and high-frequency connectors are key demand pillars, drawing on national labs' R&D strengths. Canada hosts pilot plants focused on methane-to-hydrogen pyrolysis with nanotube coproducts, linking climate and manufacturing policies.

Europe also contributed a significant share to the overall sales. German and French automakers require stringent material traceability, pushing suppliers to certify cradle-to-gate emissions. British universities spin out ventures targeting semiconductor interconnects, supported by national nanofabrication hubs. At the periphery, Middle East desalination agencies and African telecom tower installers evaluate nanotube-coated membranes and conductive coatings to tackle water and energy challenges, fostering pockets of emerging demand.

- Applied Nanostructures, Inc.

- Arkema

- Cabot Corporation

- Carbon Solutions, Inc.

- CHASM

- Cheap Tubes

- Chengdu Organic Chemicals Co., Ltd.

- CNT Co., Ltd.

- FutureCarbon GmbH

- Hanwha Group

- Hyperion Catalysis International

- Jiangsu Cnano Technology Co., Ltd.

- Kumho Petrochemical

- LG Chem

- Meijo Nano Carbon Co.,Ltd

- Nano-C

- Nanocyl SA

- OCSiAl

- Raymor Industries Inc.

- Resonac Holdings Corporation

- Thomas Swan & Co., Ltd.

- Toray Industries, Inc.

- Zyvex Technologies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-mobility Boom Accelerating CNT Demand

- 4.2.2 Leap in High-Energy-Density Li-ion and Supercapacitor Production

- 4.2.3 Aerospace Push for Ultra-light Structural Composites

- 4.2.4 Desalination and Environmental Sensors Adoption in MEA and Asia

- 4.2.5 Additive Manufacturing Integration for Conductive Filaments

- 4.3 Market Restraints

- 4.3.1 Occupational Toxicology and Nano-regulation in Europe and United States

- 4.3.2 Competition from Graphene and Boron-Nitride Nanotubes in Thermal Apps

- 4.3.3 Patent Thickets Concentrating Licensing Costs

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

- 4.6 Patent Analysis

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Type

- 5.1.1 Multi-Walled Carbon Nanotubes

- 5.1.2 Single-Walled Carbon Nanotubes

- 5.1.3 Other Types (Armchair, Zigzag, Double-Walled)

- 5.2 By Manufacturing Method

- 5.2.1 Chemical Vapor Deposition (CVD)

- 5.2.2 High-Pressure Carbon Monoxide (HiPco)

- 5.2.3 Arc Discharge

- 5.2.4 Laser Ablation

- 5.3 By End-Use Industry

- 5.3.1 Electrical and Electronics

- 5.3.2 Energy

- 5.3.3 Automotive

- 5.3.4 Aerospace and Defense

- 5.3.5 Healthcare

- 5.3.6 Other Industries (Textiles, Construction, Plastics and Composites)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Spain

- 5.4.3.6 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Applied Nanostructures, Inc.

- 6.4.2 Arkema

- 6.4.3 Cabot Corporation

- 6.4.4 Carbon Solutions, Inc.

- 6.4.5 CHASM

- 6.4.6 Cheap Tubes

- 6.4.7 Chengdu Organic Chemicals Co., Ltd.

- 6.4.8 CNT Co., Ltd.

- 6.4.9 FutureCarbon GmbH

- 6.4.10 Hanwha Group

- 6.4.11 Hyperion Catalysis International

- 6.4.12 Jiangsu Cnano Technology Co., Ltd.

- 6.4.13 Kumho Petrochemical

- 6.4.14 LG Chem

- 6.4.15 Meijo Nano Carbon Co.,Ltd

- 6.4.16 Nano-C

- 6.4.17 Nanocyl SA

- 6.4.18 OCSiAl

- 6.4.19 Raymor Industries Inc.

- 6.4.20 Resonac Holdings Corporation

- 6.4.21 Thomas Swan & Co., Ltd.

- 6.4.22 Toray Industries, Inc.

- 6.4.23 Zyvex Technologies

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Increasing Demand for Energy Storage Devices