|

시장보고서

상품코드

1852205

뇌 컴퓨터 인터페이스 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Brain-computer Interface - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

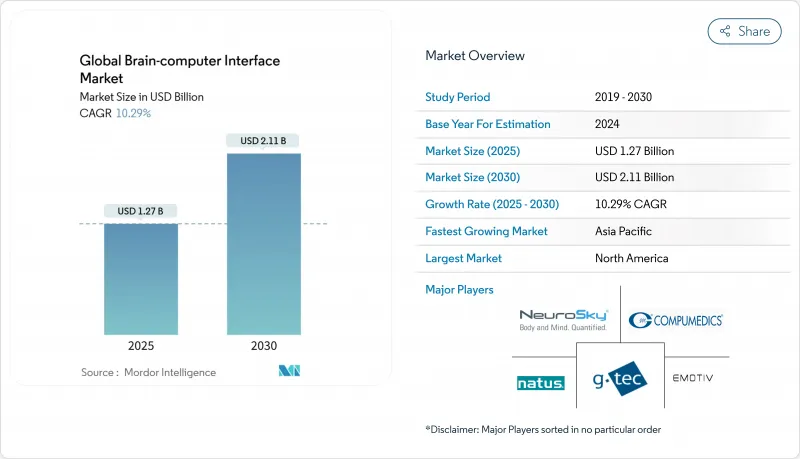

뇌 컴퓨터 인터페이스 세계 시장 규모는 2025년에 12억 7,000만 달러, 예측 기간(2025-2030년) CAGR은 10.29%를 나타내고, 2030년에는 21억 1,000만 달러에 달할 것으로 예측됩니다.

자본 유입, 성숙하고 있는 하드웨어 플랫폼, 신경 디코딩과 첨단 인공지능의 조합이 이 확대를 지원하는 주요한 힘이 되고 있습니다. 벤처 기업의 자금 조달은 상용화의 타임라인을 지속적으로 단축하고, 병원은 임베디드 솔루션의 조기 채택을 가속화, 소비자 헤드셋은 게임, 복지, 인간과 기계의 공생으로 뇌 컴퓨터 인터페이스 시장의 범위를 넓히고 있습니다. 하이브리드 신호 아키텍처와 소프트웨어 정의 기능이 제품 차별화를 더욱 뒷받침하고, 정부 자금에 의한 임상시험이 안전성과 윤리 기준을 밀어붙인다. 수요 측면에서 신경퇴행성 질환의 유병률 증가 및 커뮤니케이션 지원 도구에 대한 기대 증가는 임상 사용자를 수익 창출의 핵심으로 삼고 있습니다.

세계 뇌 컴퓨터 인터페이스 시장 동향과 통찰

커뮤니케이션 지원 기술에 대한 수요 급증

미국 국립위생연구소(National Institutes of Health)가 지원하는 조사에 의해 마비 환자의 명료한 발화가 99%의 단어 수준의 정확도로 회복되었습니다(2). 그 후, 싱크론은 스텐트 로드 임플란트와 일반 AI 모델을 결합하여 더 많은 사용자에게 핸즈프리 텍스트 입력을 허용했습니다. 병원은 간호사이클의 단축과 환자의 자율성 스코어의 향상을 보고하고 있으며, ALS뿐만 아니라 외상성 척수 손상이나 뇌간졸중(사용자 데이터)으로 임상적 대처 가능한 풀을 확대하고 있습니다. 미국 민간 보험 회사는 음성 디코딩 임플란트에 대한 초기 상환 사례를 검토하기 시작했으며 내구성있는 QOL 향상에 대한 지불자의 인식이 높아지고 있음을 보여줍니다. 유럽 교육 병원에서는 현재 집학적인 신경 재활 프로그램에 언어 모델 강화 BCI를 통합하고 있으며, 지역 전체에서 중기적인 채택이 강화되고 있습니다.

EEG 기반 웨어러블 헤드셋의 급속한 보급

게임 스튜디오, e스포츠 주최자, 소비자 웰니스 브랜드는 건식 전극 헤드셋을 대화형 타이틀, 피트니스 프로그램 및 명상 플랫폼에 통합합니다. 스트리머는 신경 입력에 의한 풀 게임 플레이의 제어를 입증하고 경쟁 리그는 집중력과 감정 상태의 데이터를 코칭을 위해 시도하고 있습니다. 이러한 도입은 저지연 신호 추출의 알고리즘을 갈고, 소형화를 가속화하고, 의료 관계자 이외의 청중에게 뇌와 컴퓨터의 상호 작용의 일상적인 이점을 교육합니다. 출하량이 늘어나면 규모 경제가 단가를 낮추기 시작하여 공급업체는 구독 기반 분석을 번들로 제공하여 사용자 1인당 수익을 늘릴 수 있습니다.

수술 위험과 규제 장애물

이식 가능한 시스템은 우수한 신호 충실도를 제공하지만 두개골과 혈관 수술을 수반하기 때문에 시행 할 수있는 센터는 제한적입니다. 전극의 이동, 감염, 장치의 회수에 관한 보고는 임상의와 보험자의 사이에 경계심을 안게 합니다. 규제기관은 장기간의 안전성 모니터링을 요구하고, 시장 출시까지의 시간을 연장하고, 시험 예산을 팽창시키고 있습니다. 이러한 장애로 인해 초기 채택은 자금력있는 대학 병원과 부유 한 자기 부담 환자에 국한되어 광범위한 보급이 지연되었습니다. 공급업체는 스텐트와 같은 전달 도구를 개선하고 가역성 임플란트를 개발함으로써 대응하고 있지만, 여전히 수년에 걸쳐 승인 경로를 탐색해야 합니다.

부문 분석

비침습성 헤드셋과 전극 어레이는 2024년 매출의 76.50%를 차지했으며 뇌 컴퓨터 인터페이스 시장에서 많은 개발자들에게 진입점 역할을 명확히 했습니다. 드라이 전극과 저에너지 블루투스를 탑재한 제품 출시로 셋업 시간이 단축되어 쾌적성이 향상되어 가상현실 게임이나 원격 신경 피드백 등 일상적인 사용 시나리오가 가능해졌습니다. 병원은 수술 위험 회피를 평가하고 소비자 브랜드는 규제 장애물의 낮음을 활용하여 선반에 배치를 가속화하고 있습니다. 경쟁의 격화에도 불구하고, 가격 하락과 S/N비의 개선이 2자리 성장을 계속 지지하고 있습니다.

소프트웨어 및 알고리즘 계층은 CAGR 12.10%로 확대되어 이 속도는 하드웨어를 능가합니다. 트랜스포머 기반 디코더, 트랜스퍼 학습, 자기 교정 프레임워크는 정보 전달율을 3자리 증가시킵니다. 이러한 발전은 2030년까지 19억 달러에서 51억 달러로 증가할 것으로 예상되는 새로운 SaaS 하위 부문을 생성합니다. 서비스 제공업체는 사내 전문가가 없는 임상 구매자에게 클라우드 대시보드, 전기 유지보수 계약 및 규정 준수 감사를 제공합니다. 이러한 활동은 공급업체를 순수한 하드웨어 이익 압축으로부터 보호하는 균형 잡힌 수익 믹스를 유지합니다.

모터/출력 플랫폼은 2024년 지출의 50.90%를 차지하며 마비 환자의 커서 조작, 휠체어 내비게이션, 의지 조작의 회복에 대한 임상 우선순위를 반영합니다. 초 이하의 응답 속도가 가능한 비침습적 딥러닝 디코더의 실증 실험이 성공해, 집중 치료실 이외에의 소구가 퍼졌습니다. 소비자 개발자들은 이러한 혁신을 증강현실 헤드셋과 스마트 홈 디바이스의 제스처리스 입력에 적응시켜 이 분야의 성숙을 강화하고 있습니다.

EEG, 근전도, 기능적 근적외선 분광법 또는 집속 초음파를 결합한 하이브리드 아키텍처는 CAGR 13.56%의 기세입니다. 여러 신경 신호와 말초 신호를 융합시켜 신뢰성을 높여 단일 모달리티 시스템의 장애인 아티팩트를 보정합니다. 뇌졸중 재활 실험실에서는 뇌와 근육의 하이브리드 훈련을 2주간 실시한 후 환자의 83%가 측정 가능한 손의 기능을 되찾았습니다. 부품 비용이 낮아짐에 따라, 하이브리드 회로는 실험실에서 모듈형 소비자 액세서리로 이동할 것으로 보입니다.

지역 분석

북미는 2024년 매출의 48.54%를 차지하며 여전히 뇌 컴퓨터 인터페이스 시장의 핵심입니다. 미국 국립위생연구소(National Institutes of Health)의 자금, 풍부한 벤처풀, 전문 수술팀이 음성 해독, 양방향 감각, 우울증의 신경조절에 이르는 지속적인 시험 파이프라인을 지원하고 있습니다. 이 지역은 진료 보상 시험을 임상 워크플로우에 통합하고 지불자의 수락을 가속화하는 조기 도입 의료 시스템의 혜택을 받고 있습니다. 개인정보보호법은 급속히 진화하고 있으며, 안전한 데이터 아키텍처에 조기에 투자하는 기업에게는 컴플라이언스 오버헤드와 경쟁 우위를 모두 창출하고 있습니다.

아시아태평양의 CAGR은 가장 빠른 12.56%로 중국 정부가 브레인 머신 인터페이스를 전략적 산업으로 지정한 것을 뒷받침하고 있습니다. 국가로부터의 보조금이 산학 컨소시엄을 뒷받침하는 한편, 새로운 표준화 단체가 신호 취득 프로토콜이나 윤리 가이드 라인에 임하고 있습니다. 중국 신흥기업은 이미 베이징어 음성 해독으로 71%의 정확성을 입증하고 있으며, 이 지역의 기세를 강조하고 있습니다. 일본의 고령화 사회는 신경 퇴행성 질환의 관리라는 구조적인 수요 드라이버를 추가하고, 한국의 전자 기기 메이저는 센서의 소형화에 관한 전문 지식을 제공합니다.

유럽에서는 공공 의료 제도가 기분 향상 시험과 뇌졸중 회복 프로그램에 자금을 제공하고 있으며 큰 점유율을 차지하고 있습니다. 국민건강서비스(National Health Service)에 의한 650만 파운드의 초음파 기반 BCI 시험은 정신건강 상태에 대한 비의약품적 접근에 대한 정책 수준의 헌신을 강화합니다. 곧 시행되는 EU의 AI법에서는 많은 AI 대응 의료기기가 고위험으로 분류되기 때문에 벤더는 다른 지역에서의 경쟁 차별화 요인이 될 수 있는 엄격한 사이버 보안과 성능 검증 절차를 채택해야 합니다. 중동, 아프리카, 남미에서는 모바일 연결과 국경을 넘는 교육 파트너십을 활용하여 원격 재활과 원격 신경 모니터링에 투자하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- EEG 기반의 웨어러블 헤드셋의 e스포츠 및 게임 기업에 의한 급속한 채택

- 신경 기술의 중심지(실리콘 밸리, 로잔, 비엔나)에 있어서의 VC의 고액 자금 조달이 제품 상용화 일정 가속화

- 기술 향상을 위한 정부에 의한 R&D 활동의 활성화

- 일본과 EU의 고령화 사회에 있어서의 신경 변성 질환의 유병률 증가, 임상 시험 촉진

- 시장 성장 억제요인

- 이식형 BCI 시스템의 채택을 제한하는 수술 리스크와 규제상의 장애물

- 신경 데이터 수집에 대한 데이터 프라이버시 우려

- 공적 의료 제도에 있어서의 BCI에 근거한 재활 치료에 대한 상환 코드의 희소성

- 대중 시장용 EEG 장치에 있어서의 모발과 두피의 임피던스에 의한 신호 정확도 문제

- 공급망 분석

- 기술의 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 대체품의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 업계 간 경쟁

제5장 시장 규모와 성장 예측

- 구성요소별

- 하드웨어

- 침습적

- 비침습적

- 기타

- 소프트웨어 & 알고리즘

- 서비스

- 하드웨어

- 인터페이스 유형별

- 모터/출력 BCI

- 통신 BCI

- 패시브/모니터링 BCI

- 하이브리드 BCI

- 용도별

- 신경 보철과 운동 기능 회복

- 통신 및 제어

- 기타

- 최종 사용자별

- 병원&클리닉

- 연구 및 학술기관

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동?아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 6. 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- g.tec medical engineering GmbH

- Blackrock Neurotech

- Emotiv, Inc.

- NeuroSky, Inc.

- Kernel

- Paradromics, Inc.

- MindMaze SA

- Cognixion

- CTRL-Labs(Meta Platforms)

- NextMind (Snap Inc.)

- OpenBCI

- Synchron Inc.

- Neurable

- BrainCo, Inc.

- Interaxon Inc. (Muse)

- Bitbrain Technologies

- Cyberkinetics

- Nihon Kohden Corporation

- Compumedics Ltd

- Alea Neurotherapeutics

제7장 시장 기회와 장래의 전망

SHW 25.11.19The Global Brain-computer Interface Market size is estimated at USD 1.27 billion in 2025, and is expected to reach USD 2.11 billion by 2030, at a CAGR of 10.29% during the forecast period (2025-2030).

Capital inflows, maturing hardware platforms, and the pairing of neural decoding with advanced artificial intelligence are the primary forces behind this expansion. Venture funding continues to shorten commercialization timelines, hospitals accelerate early adoption of implantable solutions, and consumer-facing headsets extend the reach of the Brain-Computer Interface market into gaming, well-being, and human-machine symbiosis. Hybrid signal architectures and software-defined features further support product differentiation, while government-funded clinical trials push forward standards for safety and ethics . On the demand side, rising prevalence of neuro-degenerative disorders and heightened expectations for assistive communication tools keep clinical users at the core of revenue generation.

Global Brain-computer Interface Market Trends and Insights

Surging demand for assistive communication technologies

National Institutes of Health-backed research restored intelligible speech for a paralyzed patient with 99% word-level accuracy [2]. Synchron subsequently paired its Stentrode implant with a generative-AI model, enabling hands-free texting for additional users. Hospitals report shorter caregiver cycles and higher patient-autonomy scores, expanding the clinical addressable pool beyond ALS to traumatic spinal-cord injury and brain-stem stroke (user data). Private insurers in the United States have begun reviewing early reimbursement cases for speech-decoding implants, indicating growing payer recognition of durable quality-of-life gains. European teaching hospitals now integrate language-model-enhanced BCIs in multidisciplinary neuro-rehabilitation programs, reinforcing mid-term adoption across the region.

Rapid adoption of EEG-based wearable headsets

Gaming studios, e-sports organizers, and consumer-wellness brands integrate dry-electrode headsets into interactive titles, fitness programs, and meditation platforms. Streamers demonstrate full-gameplay control with neural inputs, while competitive leagues trial concentration and emotional-state data for coaching. These deployments sharpen algorithms for low-latency signal extraction, accelerate miniaturization, and educate non-medical audiences on everyday benefits of brain-computer interaction. As shipments grow, economies of scale begin to lower unit costs, allowing vendors to bundle subscription-based analytics that deepen revenue per user.

Surgical risks and regulatory hurdles

Implantable systems deliver superior signal fidelity yet involve cranial or vascular procedures that few centers can perform. Reports of electrode migration, infection, and device retrieval create caution among clinicians and insurers. Regulatory agencies require lengthy safety monitoring, stretching time-to-market and inflating trial budgets. These obstacles confine early adoption to well-funded academic hospitals and wealthy self-pay patients, slowing broad penetration. Vendors respond by refining stent-like delivery tools and developing reversible implants but must still navigate multi-year approval pathways.

Other drivers and restraints analyzed in the detailed report include:

- High VC funding in neuro-tech hubs

- Rising R&D activities by government

- Data-privacy concerns over neural data collection

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Non-invasive headsets and electrode arrays generated 76.50% of 2024 revenue, underscoring their role as the entry point for many developers in the Brain-Computer Interface market. Product launches with dry electrodes and low-energy Bluetooth have reduced setup times and improved comfort, enabling everyday usage scenarios such as virtual-reality gaming and remote neurofeedback. Hospitals appreciate the avoidance of surgical risk, and consumer brands leverage lower regulatory hurdles to speed shelf placement. Price declines and improved signal-to-noise ratios continue to support double-digit growth despite intensifying competition.

Software and algorithm layers are expanding at a 12.10% CAGR, a pace that outstrips hardware because every incremental headset installation yields recurring licensing opportunities. Transformer-based decoders, transfer learning, and self-calibrating frameworks raise information-transfer rates by triple-digit percentages. These advances create an emergent SaaS sub-segment forecast to climb from USD 1.9 billion to USD 5.1 billion by 2030. Service providers follow close behind, offering cloud dashboards, electrode-maintenance contracts, and compliance audits to clinical buyers who lack in-house specialists. Together, these activities sustain a balanced revenue mix that shields vendors from pure hardware margin compression.

Motor/output platforms accounted for 50.90% of spending in 2024, reflecting clinical priorities around restoring cursor control, wheelchair navigation, and prosthetic manipulation for paralysis patients. Successful demonstrations of non-invasive deep-learning decoders capable of sub-second response rates have widened appeal beyond the intensive-care unit. Consumer developers adapt these breakthroughs to gesture-less input for augmented-reality headsets and smart-home devices, reinforcing the segment's maturity.

Hybrid architectures, combining EEG, electromyography, functional near-infrared spectroscopy, or focused ultrasound, are on course for 13.56% CAGR. They lift reliability by fusing multiple neural and peripheral signals, thereby compensating for artifacts that hamper single-modality systems. Experimental stroke-rehabilitation rigs illustrate the benefit: after two weeks of hybrid brain-muscle training, 83% of patients regained measurable hand function. As component costs fall, hybrid circuitry will migrate from the laboratory into modular consumer accessories.

The Brain Computer Interface Market Report Segments by Component (Hardware, Software & Algorithm and Services), by Interface (Motor BCI, Communication BCI, and More), by Application (Neuro-Prosthetics & Motor Restoration and More), by End User (Hospitals & Clinics, Research & Academic Institutes, and Others) and by Geography ( Northa America, Europe and More) the Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 48.54% of 2024 revenue and remains the anchor of the Brain-Computer Interface market. National Institutes of Health funding, deep venture pools, and specialized surgical teams underpin a continuous trial pipeline that spans speech decoding, bidirectional sensation, and neuromodulation for depression. The region benefits from early adopter health systems that integrate reimbursement studies into clinical workflows, accelerating payer acceptance. Privacy legislation is evolving rapidly, creating both compliance overhead and competitive advantage for firms that invest early in secure data architectures.

Asia-Pacific delivers the fastest 12.56% CAGR, propelled by Chinese government designation of brain-machine interfaces as a strategic industry. State grants encourage industrial-academic consortia, while new standards bodies tackle signal-acquisition protocols and ethical guidelines. Chinese start-ups have already demonstrated 71% accuracy in decoding Mandarin speech, underscoring regional momentum. Japan's aging demographics add a structural demand driver for neuro-degenerative disease management, and South-Korean electronics majors contribute sensor miniaturization expertise.

Europe holds a significant share, with public-health systems funding mood-enhancement trials and stroke-recovery programs. The National Health Service's GBP 6.5 million ultrasound-based BCI trial reinforces policy-level commitment to non-pharma approaches for mental-health conditions. The forthcoming EU AI Act classifies many AI-enabled medical devices as high-risk, compelling vendors to adopt rigorous cyber-security and performance-validation procedures that can become competitive differentiators in other regions. Smaller but growing markets in the Middle East, Africa, and South America invest in tele-rehabilitation and remote neuromonitoring, leveraging mobile connectivity and cross-border training partnerships.

- g.tec medical engineering

- Blackrock Neurotech

- Emotiv, Inc.

- NeuroSky, Inc.

- Kernel

- Paradromics, Inc.

- MindMaze SA

- Cognixion

- CTRL-Labs (Meta Platforms)

- NextMind (Snap Inc.)

- OpenBCI

- Synchron

- Neurable

- BrainCo, Inc.

- Interaxon Inc. (Muse)

- Bitbrain Technologies

- Cyberkinetics

- Nihon Kohden

- Compumedics

- Alea Neurotherapeutics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid adoption of EEG-based wearable headsets by eSports and gaming companies

- 4.2.2 High VC funding in neuro-tech hubs (Silicon Valley, Lausanne, Vienna) accelerating product commercialization timelines

- 4.2.3 Rising R&D Activities by Government to Improve the Technology

- 4.2.4 Rising prevalence of neuro-degenerative disorders in ageing populations of Japan and EU spurring clinical trials

- 4.3 Market Restraints

- 4.3.1 Surgical risks and regulatory hurdles limiting adoption of implantable BCI systems

- 4.3.2 Data-privacy concerns over neural data collection

- 4.3.3 Scarcity of reimbursement codes for BCI-based rehabilitation therapies in public healthcare systems

- 4.3.4 Signal accuracy challenges due to hair & scalp impedance in mass-market EEG devices

- 4.4 Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Threat of Substitutes

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Bargaining Power of Suppliers

- 4.6.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Component (Value)

- 5.1.1 Hardware

- 5.1.1.1 Invasive

- 5.1.1.2 Non-invasive

- 5.1.1.3 Others

- 5.1.2 Software & Algorithms

- 5.1.3 Services

- 5.1.1 Hardware

- 5.2 By Interface Type (Value)

- 5.2.1 Motor / Output BCI

- 5.2.2 Communication BCI

- 5.2.3 Passive / Monitoring BCI

- 5.2.4 Hybrid BCI

- 5.3 By Application (Value)

- 5.3.1 Neuro-prosthetics & Motor Restoration

- 5.3.2 Communication & Control

- 5.3.3 Others

- 5.4 By End-User (Value)

- 5.4.1 Hospitals & Clinics

- 5.4.2 Research & Academic Institutes

- 5.4.3 Others

- 5.5 By Geography (Value)

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia- Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 6. Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 g.tec medical engineering GmbH

- 6.4.2 Blackrock Neurotech

- 6.4.3 Emotiv, Inc.

- 6.4.4 NeuroSky, Inc.

- 6.4.5 Kernel

- 6.4.6 Paradromics, Inc.

- 6.4.7 MindMaze SA

- 6.4.8 Cognixion

- 6.4.9 CTRL-Labs (Meta Platforms)

- 6.4.10 NextMind (Snap Inc.)

- 6.4.11 OpenBCI

- 6.4.12 Synchron Inc.

- 6.4.13 Neurable

- 6.4.14 BrainCo, Inc.

- 6.4.15 Interaxon Inc. (Muse)

- 6.4.16 Bitbrain Technologies

- 6.4.17 Cyberkinetics

- 6.4.18 Nihon Kohden Corporation

- 6.4.19 Compumedics Ltd

- 6.4.20 Alea Neurotherapeutics