|

시장보고서

상품코드

1906115

사다리 시장 : 점유율 분석, 업계 동향, 통계, 성장 예측(2026-2031년)Ladder - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

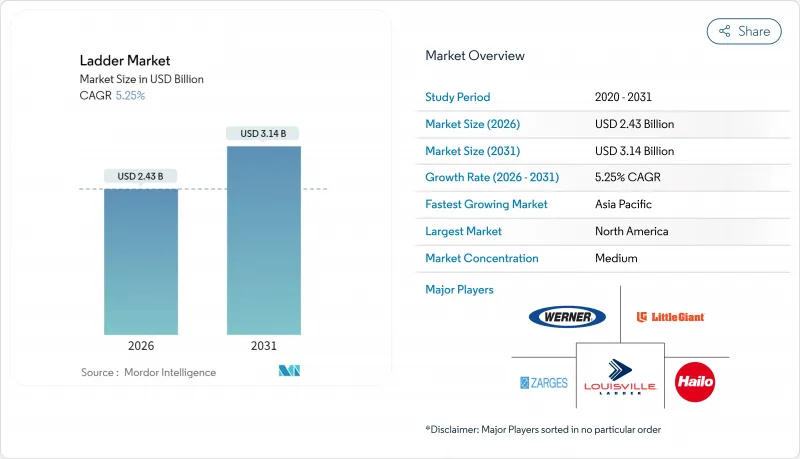

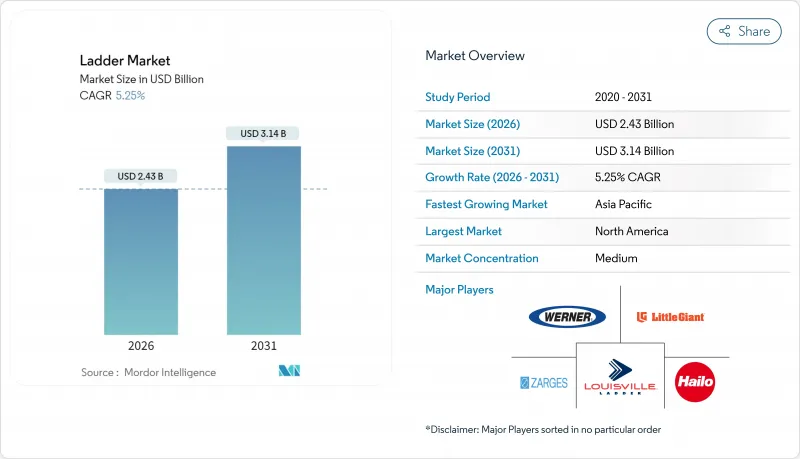

사다리 시장은 2025년 23억 1,000만 달러로 평가되었고, 2026년에는 24억 3,000만 달러에 달할 것으로 예상됩니다. 2026년에서 2031년에 걸쳐 CAGR 5.25%로 성장하고, 2031년까지 31억 4,000만 달러에 이를 것으로 예측되고 있습니다.

완만한 성장은 주택 개수, 미국 인프라 투자 고용법에 의한 인프라 지출, 전문업체의 지속적인 설비 갱신의 혜택을 계속 받는 성숙한 제품 카테고리를 반영합니다. ConstructConnect사는 2025년 미국 건설 지출 총액이 8.5% 증가하고, 이 동향은 상업 및 공공시설 현장에 있어서의 신규 및 교환용 사다리 수요를 지지하고 있습니다. 알루미늄은 중량 대 강도비의 우위성으로부터 주요 소재인 것을 계속하는 한편, 전력회사가 고전압 보수용으로 비도전 제품을 채택하는 움직임을 받아 유리 섬유 제품이 수량 기준의 성장을 견인합니다. 전자상거래 물류의 확대는 창고사업자로부터 요구되는 컴팩트한 신축식 구성의 매출을 지원하고 고정액세스시스템에 관한 안전규제는 OSHA의 2036년 준거기한보다 상당히 앞당겨 갱신구매를 촉진합니다. 경쟁의 격렬함은 중간 정도에 머물고 있습니다. 지역 브랜드가 전문적인 카탈로그의 충실도와 지역 밀착형의 유통망에 의해 대규모 다국적 기업과의 밸런스를 취하고 있기 때문입니다.

세계 사다리 시장 동향과 인사이트

주택 개수와 DIY 문화의 상승

미국에서는 주택 소유자가 개축을 우선하는 경향이 강해지고 있습니다. 2024년 11월의 주택가격 중앙값이 42만 400달러에 달했고, 주택 소유자들은 이사 대신 리모델링을 선택하고 있습니다. 주택 소유의 피크 연령층에 접하는 밀레니얼 세대는 온라인 튜토리얼이나 대형 소매점을 통한 프로 사양 공구의 보급에 의해 스스로 개수 프로젝트를 실시하는 것을 좋아하고 있습니다. 소셜 미디어의 보급에 의해 내장 도장, 천장 팬 교환, 다락방에의 액세스용의 사다리 구입을 촉진하는 개인 간 기술 공유가 활성화하고 있습니다. 원격근무나 하이브리드 근무의 보급에 의해 홈 오피스의 개조 수요가 늘어나고, 스텝 사다리나 다목적 관절식 설계의 사다리가 일상적인 가정용 공구 킷에 정착하고 있습니다. 유통업체에 따르면 소비자가 편의성과 수납 효율을 중시하는 경향 때문에 20파운드(약 9kg) 미만의 휴대용 사다리가 기존의 중량형 제품을 대체하고 있습니다. 이로 인해 신축 주택 건설이 둔화되어도 사다리 시장에는 안정적인 수요 기반이 형성되고 있습니다.

건설 현장에서 안전 규제 강화

미국 노동안전보건국(OSHA)의 개정 「보행 및 작업면 규칙」에서는 24피트(약 7.3m)를 넘는 신규 고정 사다리에 추락 방지 시스템의 탑재가 의무화되어 2036년까지 케이지 부착 사다리의 단계적 폐지가 정해져 있습니다. 건설업체는 향후 대규모 리노베이션을 피하기 위해 교체 프로그램을 가속화하고 있으며 케이블 슬리브가 내장된 케이지리스 수직 시스템의 판매가 증가하고 있습니다. 유럽의 EN 131 표준에 따른 프로용 및 비프로용 분류는 성능 수준과 시험 하중을 통해 사다리 산업을 더욱 세분화하여 프리미엄 SKU의 보급을 촉진하고 있습니다. 터너 구조와 같은 주요 건설 회사는 "사다리는 마지막"이라는 정책을 시행하고 있으며, 휴대용 사다리의 사용에는 서면 허가를 의무화, 특정 작업은 가드 레일이있는 플랫폼 모델로 이행하고 있습니다. 보험사는 현재 노동자재해보상보험료를 문서화된 사다리의 안전연수 및 기기의 경년 열화와 연동시키고 있으며, 고용주는 빨리 사다리의 교체를 촉구하고 있습니다. OSHA, ANSI 및 EN 규격의 제품 인증을 취득할 수 있는 제조업체는 세계 건설업체의 다지역에서의 사업 전개에 맞추어 경쟁 우위를 누리고 있습니다.

원재료 가격 변동

런던 금속 거래소의 알루미늄 현물 가격은 2025년 2분기까지 전년 대비 12% 상승하여 제련소의 이익률을 압박하는 에너지 비용의 인플레이션을 반영하고 있습니다. 밀 마감 코일을 소비하는 사다리 제조 업체는 종종 분기별 계약에 묶여 있기 때문에 스팟 가격의 급등은 즉시 조익률의 압축으로 이어집니다. 플랫폼 난간과 연장 지주에 사용되는 강관의 투입재료도 지정학적 이벤트에 의해 세계 무역의 흐름이 변화하기 때문에 유사한 변동에 직면하고 있습니다. 신흥 시장의 통화변동은 수입에 의존하는 조립업체의 구매력 예측 불가능성을 악화시키고 있습니다. 제조업체는 일부 비용을 대리점에 전가하지만 과도한 가격 인상은 가격에 민감한 주택 채널 수요를 둔화시킵니다. 리스크를 방어하기 위해 다국적 기업은 경량 구조용 폴리머의 채택을 추진하고 있습니다만, ANSI A14 프로토콜에 근거한 신소재의 인증에는 최대 18개월이 소요될 수 있어, 시장 보급을 지연시키고 있습니다.

부문 분석

2025년 시점에서 스텝 사다리는 사다리 시장 규모의 최대 점유율을 차지하여 7억 9,000만 달러(세계 수익의 34.02%)에 이르렀습니다. 페인트, 장식, 가벼운 작업의 인기는 사각 접촉으로 인한 안정성과 넓은 발판 폭에 기인합니다. 또한, 이 설계는 유리 섬유 구조에 대한 적응성이 높고 휴대성을 손상시키지 않고 절연 요건을 충족시킬 수 있습니다. 이러한 우위성에도 불구하고 컴팩트한 거주 공간과 이동형 노동력이 증가하는 가운데, 밴이나 옷장에 수납 가능한 접이식 도구를 요구하는 수요에 의해 신축식은 6.21%의 연평균 복합 성장률(CAGR)로 성장이 전망되고 있습니다.

안전성의 향상도 신축식 사다리의 성장을 지지하고 있습니다. 워너사가 2025년 4월에 발표한 신제품에서는 손가락 끼임 방지하는 원 버튼식 수납 기구와 적절한 전개 상태를 시인할 수 있는 락 인디케이터를 도입해, 이것에 의해 종래 이 카테고리를 고민해 온 EN 131-6 규격 적합성의 과제가 해소되었습니다. 건설업자는 현장의 최종 점검 작업에 있어서 대형 익스텐션 사다리의 이동에 따른 시간 손실이 비용 증가가 되기 때문에 신축식의 도달 거리를 높이 평가했습니다. 제품 진화는 가정용 시장에서 전통적인 스텝 사다리가 지위를 유지하면서도 다기능의 공간 절약형 형태가 점유율을 계속 확대하고 있음을 시사합니다. 특허 취득의 단판과 지주 접합부, 자동 락식 연결기를 채택하는 제조업체는 프리미엄 가격을 실현해, 프로 유저 커뮤니티에 있어서의 브랜드 충성도를 키우고 있습니다.

2025년 사다리 시장 점유율의 42.10%를 알루미늄이 차지했습니다. 이것은 주택과 상업시설 모두에서의 보급을 지원하는 최적의 강도 중량비를 반영합니다. 내식성과 재활용성은 기업 조달의 지속가능성 지침을 준수합니다. 한편, 무게는 무거운 것, 유리 섬유는 6.78%라는 가장 빠른 CAGR을 나타낼 것으로 예측되고 있습니다. 이 성장 페이스는 절연 안전성이 절대 조건이 되는 전력 회사의 현장 작업에 기인합니다.

통전 중의 전선 작업을 실시하는 전력 작업원에게는 30kV 내압 인정의 비전도성 사다리가 필수입니다. 유리 섬유 강화 폴리머(GFRP) 라미네이트는 페인트 알루미늄보다 우수한 자외선 열화 내성을 제공하면서 이 보호 기능을 제공합니다. 현장 조사에 의하면, 목재 폴 스텝을 10 피트의 유리 섬유제로 교환하는 것으로, 작업차의 적재 중량을 14% 삭감할 수 있어 주의 차축 제한을 채우고 연료비를 저감할 수 있습니다. 마찬가지로, 옥상에서 5G 안테나를 회전시키는 통신 기술자는 고주파 아크 방전의 위험을 피하기 위해 유리 섬유를 지정합니다. 공급망 데이터에 따르면, 유리 섬유 제품의 수주량은 아시아태평양의 재료량 증가의 약 28%를 차지하고 있으며, 절연 사다리 사양의 세계 표준화가 진행되고 있음을 시사하고 있습니다.

지역별 분석

북미는 2025년 세계 수익의 31.85%를 차지해 선두가 되었습니다. 주택 보수 수요의 급증에 더해, OSHA(미국 노동 안전 위생국)가 2036년에 다가오는 규제 대응 기한을 앞두고, 고정식 케이지로부터 케이블식 추락 방지 시스템에의 조기 갱신이 진행되었기 때문입니다. 미국의 단독주택의 개수 지출은 전년 대비 3.5% 증가하여 알루미늄 스텝 사다리와 유리 섬유제 포디움 유닛 수요를 지지했습니다. 캐나다의 유틸리티 회사는 28피트 절연 연장 사다리를 지정하는 네트워크 강화 프로그램을 가속화하고 멕시코의 마키라도라 확장은 산업 플랫폼의 주문을 견인했습니다. 건설 업계는 2025년에 8.5%의 성장이 예상되어 상업시설 인테리어 및 토목인프라 분야에서 사다리의 안정조달을 확고히 합니다.

아시아태평양은 공공 인프라 계획이 확대됨에 따라 2031년까지 연평균 복합 성장률(CAGR) 5.62%에서 가장 빠르게 성장하는 지역입니다. 인도가 2029년도까지 계획하는 1조 4,500억 달러의 지출은 교량 자리 점검과 지하철 가전 공사에서 휴대용 액세스 기기에 대한 의존도를 높입니다. 중국에서는 현장 작업의 기계화가 진행되고 있는 중에서도 천장 작업에 경량 솔루션이 여전히 필요하기 때문에 기본적인 사다리 수요는 견고합니다. 고소 작업차가 증가하고 있는 현장에서도 마찬가지입니다. 호주와 일본에서는 항만 시설의 근대화와 노후화된 송전선의 용량 확대에 따른 교환으로 주문이 지속되고 있습니다. 인도네시아 등 동남아 성장 시장에서는 수입 관세 회피를 위해 현지 조립이 가능한 중견 브랜드에 기회가 열리고 있습니다.

유럽은 성숙하면서도 안정된 시장 구조를 유지하고 있습니다. 독일과 프랑스의 리노베이션 촉진 프로그램은 에너지 효율적인 리노베이션이 우선되고, 다락방에 대한 빈번한 액세스와 외벽 보수가 필요하기 때문에 사다리 판매는 안정되어 있습니다. EN 131 표준의 "프로페셔널" 카테고리에서는 더 두꺼운 버팀대와 강화된 판으로 업그레이드해야 하며 평균 판매 가격 상승에 기여합니다. 북유럽 국가에서는 환경 기준이 통합되어 재활용 가능한 알루미늄 함유율이 70%를 초과하는 사다리에는 조달 포인트가 부여되고 있습니다. 한편 중동 및 아프리카에서는 산업 다각화 계획에 따른 초기 단계의 성장을 볼 수 있지만 물류상의 과제가 시장 침투를 방해하고 있습니다. 라틴아메리카에서는 상품 사이클에 따른 도입이 진행되고 브라질에서의 농업 사업의 확대가 그레인 엘리베이터의 유지 보수용 유리 섬유제 사다리의 계절적인 수입 증가를 지원하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 주택 개수 및 DIY 문화의 확대

- 건설 현장에서의 안전 규제 강화

- 신흥 경제국의 인프라 투자 확대

- 전자상거래 창고 네트워크 확대

- 고전압 설비 보수에 있어서의 GFRP제 사다리의 도입

- 렌탈 플릿에서 IoT를 활용한 사용 상황 분석

- 시장 성장 억제요인

- 원재료 가격의 변동성

- 사다리 관련 부상으로 인한 대안 제시

- 신규 판매를 잠식하는 렌탈 모델

- 드론/고소 작업차(MEWP)에 의한 점검 업무의 대체

- 업계 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 시장의 최신 동향과 혁신에 관한 인사이트

- 업계의 최근 동향(신제품 출시, 전략적 이니셔티브, 투자, 제휴, 합작 사업, 사업 확대, M&A 등)에 대한 인사이트

제5장 시장 규모와 성장 예측

- 제품 유형별

- 스텝 사다리

- 연장 사다리

- 플랫폼 사다리

- 접이식 사다리

- 텔레스코픽 사다리

- 특수/커스텀 사다리

- 재료별

- 알루미늄

- 유리 섬유

- 철강

- 목재

- 플라스틱/복합재료

- 최종 사용자 업계별

- 주택/DIY

- 건설

- 산업제조

- 유틸리티 및 통신

- 상업 및 기관용

- 운송 및 물류

- 유통 채널별

- 오프라인(홈 센터, 공업용 도매업체)

- 온라인(전자상거래 플랫폼, 소비자 직접 판매)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 페루

- 칠레

- 아르헨티나

- 기타 남미

- 유럽

- 영국

- 독일

- 프랑스

- 스페인

- 이탈리아

- 베네룩스

- 북유럽 국가

- 기타 유럽

- 아시아태평양

- 인도

- 중국

- 일본

- 호주

- 한국

- 동남아시아

- 기타 아시아태평양

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

- 나이지리아

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- WernerCo

- Louisville Ladder Inc.

- Little Giant Ladders(Wing Enterprises)

- Zarges GmbH

- Hailo Werk

- Altrex BV

- KRAUSE-Werk GmbH

- Youngman Group(Werner UK)

- Gorilla Ladders(Tricam)

- Tubesca-Comabi

- Telesteps AB

- Featherlite Ladders

- FACAL

- Hymer-Leichtmetallbau

- ABRU(Werner)

- Shanghai Ruiju Tools

- Zhejiang Yongkang Chuangxin

- Jinma Ladder

- Alinco Inc.

- Hermans

제7장 시장 기회와 장래의 전망

SHW 26.01.22The Ladder market is expected to grow from USD 2.31 billion in 2025 to USD 2.43 billion in 2026 and is forecast to reach USD 3.14 billion by 2031 at 5.25% CAGR over 2026-2031.

Moderate growth reflects a maturing product category that continues to benefit from residential renovation, infrastructure outlays supported by the U.S. Infrastructure Investment and Jobs Act, and ongoing equipment renewal by professional trades. ConstructConnect projects 8.5% growth in total U.S. construction spending in 2025, a trend that underpins new and replacement ladder demand across commercial and institutional job sites. Aluminum remains the leading material owing to weight-to-strength advantages, while fiberglass leads unit growth as utilities adopt non-conductive products for high-voltage maintenance. E-commerce logistics expansion sustains sales of compact telescopic configurations sought by warehouse operators, and safety regulations on fixed access systems stimulate replacement purchases well before OSHA's 2036 compliance deadline. Competitive intensity stays moderate because regional brands counterbalance large multinationals through specialized catalog depth and localized distribution.

Global Ladder Market Trends and Insights

Rising Residential Renovation and DIY Culture

Homeowners in the United States prioritized remodeling as the median selling price reached USD 420,400 in November 2024, encouraging upgrades rather than relocations. Millennials entering peak ownership years prefer doing projects themselves, helped by online tutorials and wider access to pro-grade tools through big-box retailers. Social media visibility increases peer-to-peer skill sharing that boosts ladder purchases for interior painting, ceiling fan replacement, and attic access. Remote and hybrid work has heightened demand for home office conversions, pushing step ladders and multipurpose articulating designs into routine household toolkits. Distributors report that portable ladders under 20 lb are replacing heavier legacy units as consumers favor convenience and storage efficiency. The effect on the ladders market is a steady baseline of unit demand, even when new-build housing slows.

Heightened Safety Regulations in Construction

OSHA's revised Walking and Working Surfaces rule requires all new fixed ladders over 24 ft to include a fall-arrest system, phasing out cages by 2036. Contractors are accelerating replacement programs to avoid bulk retrofits later, spurring sales of cage-free vertical systems with integrated cable sleeves. European EN 131 Professional vs. Non-Professional classifications further segment the ladders industry by performance level and test loads, encouraging premium SKUs. Large builders such as Turner Construction enforce "ladders last" policies that mandate written permission for portable ladder use, shifting certain tasks to platform models with guardrails. Insurers now link workers' compensation premiums to documented ladder safety training and equipment age, nudging employers to refresh fleets sooner. Manufacturers able to certify products across OSHA, ANSI, and EN standards enjoy a competitive edge that aligns with global contractors' multi-region operations.

Volatility in Raw-Material Prices

London Metal Exchange aluminum cash prices climbed 12% year-over-year through Q2 2025, mirroring energy cost inflation that tightens smelter margins. Ladder producers consuming mill-finish coil are often locked into quarterly contracts, so spot surges translate to immediate gross-margin compression. Steel tube inputs used in platform railings and extension stiles face similar volatility as geopolitical events reshape global trade flows. Currency swings in emerging markets worsen purchasing-power unpredictability for import-reliant assemblers. Producers pass some costs to distributors, but excessive hikes dampen demand in price-sensitive residential channels. To hedge exposure, multinationals pursue lightweight structural polymers; however, certifying new materials under ANSI A14 protocols can take 18 months, slowing market uptake.

Other drivers and restraints analyzed in the detailed report include:

- Growing Infrastructure Spending in Emerging Economies

- Expansion of E-commerce Warehouse Networks

- Ladder-Related Injuries Prompting Alternatives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Step ladders generated the largest slice of the ladder market size at USD 0.79 billion in 2025, equal to 34.02% of global revenue. Their popularity in painting, decor, and light-duty trade tasks rests on inherent stability from four-leg contact and wide tread depth. The design also adapts easily to fiberglass construction, letting utilities meet dielectric requirements without sacrificing portability. Despite that dominance, telescopic ladders are on course for a 6.21% CAGR as compact living and mobile workforces seek collapsible tools that fit in vans or closets.

Safety upgrades underpin telescopic momentum. Werner's April 2025 launch introduced single-button retraction that prevents finger pinches, alongside visual lock indicators to certify proper extension. These features mitigate the EN 131-6 compliance gaps that previously tarnished the category. Contractors appreciate telescopic reach on job-site punch-lists where time penalties for moving bulky extension ladders add cost. Product evolution signals that multifunctional, space-saving formats will continue to gain share even as traditional step designs hold ground in household settings. Manufacturers leveraging patented rung-to-stile joints and automatic-locking couplers command premium pricing and foster brand loyalty across pro user communities.

Aluminum contributed 42.10% to the ladder market share in 2025, reflecting its optimal strength-to-weight ratio that supports widespread adoption across residential and commercial settings. Its corrosion resistance and recyclability align with sustainability guidelines in corporate procurement. Conversely, fiberglass, though heavier, is projected to log the fastest 6.78% CAGR, a pace attributed to electric utility field work where dielectric safety is non-negotiable.

Utility crews working on energized lines require non-conductive ladders certified to 30 kV ratings. Glass-fiber reinforced polymer (GFRP) laminates provide that protection while resisting UV degradation better than painted aluminum. Field studies show that replacing wood pole steps with 10 ft fiberglass variants cuts line-truck payload weight by 14%, letting fleets meet state axle limits and lower fuel costs. Telecommunications technicians rotating 5G antennas on rooftops similarly specify fiberglass to avoid RF arc hazards. Supply chain data indicates that fiberglass orders comprise almost 28% of material volume growth in Asia-Pacific, suggesting a global normalization of insulated ladder specifications.

The Ladder Market Report is Segmented by Product Type (Step Ladders, Extension Ladders, Platform Ladders, and More), Material (Aluminum, Fiberglass, Steel, and More, End-User Industry (Residential/DIY, Construction, Industrial Manufacturing, Utilities & Telecom, and More)), Distribution Channel (Offline, Online), and Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led with 31.85% of global revenue in 2025 after residential renovation surged and OSHA's forthcoming 2036 compliance deadline spurred early replacement of fixed cages with cable-based fall-arrest systems. U.S. single-family remodeling outlays rose 3.5% year-over-year, sustaining demand for aluminum stepladders and fiberglass podium units. Canadian utilities accelerated network-hardening programs that specify 28 ft insulated extensions, while Mexican maquiladora expansions drove industrial platform orders. Construction forecasts of 8.5% growth for 2025, cement expectations of steady ladder procurement across commercial interiors and civil infrastructure.

Asia-Pacific is the fastest-growing region, tracking a 5.62% CAGR to 2031 as public infrastructure pipelines ramp up. India's planned USD 1.45 trillion outlay through FY 2029 increases reliance on portable access equipment for bridge girder inspection and metro rail electrification. China's transition to mechanized job-site workflows keeps basic ladder demand resilient because finishing trades still require lightweight solutions for ceiling work, even where aerial lifts proliferate. Australia and Japan sustain orders by modernizing port facilities and replacing aging transmission lines with higher-capacity circuits. Southeast Asian growth markets such as Indonesia open opportunities for mid-tier brands that can localize assembly to avoid import duties.

Europe maintains a mature yet stable profile. Renovation stimulus programs in Germany and France prioritize energy-efficient retrofits that necessitate frequent attic access and facade repairs, translating to consistent ladder sales. EN 131's Professional category compels contractors to upgrade to thicker stiles and reinforced rungs, benefits that raise average selling prices. Nordic countries integrate environmental criteria, awarding procurement points for ladders with recyclable aluminum content above 70%. Meanwhile, the Middle East and Africa show early-stage growth tied to industrial diversification plans, though logistical hurdles constrain full market penetration. Latin American adoption follows commodity cycles, with Brazilian agribusiness expansions supporting seasonal spikes in fiberglass ladder imports for grain elevator maintenance.

- WernerCo

- Louisville Ladder Inc.

- Little Giant Ladders (Wing Enterprises)

- Zarges GmbH

- Hailo Werk

- Altrex B.V.

- KRAUSE-Werk GmbH

- Youngman Group (Werner UK)

- Gorilla Ladders (Tricam)

- Tubesca-Comabi

- Telesteps AB

- Featherlite Ladders

- FACAL

- Hymer-Leichtmetallbau

- ABRU (Werner)

- Shanghai Ruiju Tools

- Zhejiang Yongkang Chuangxin

- Jinma Ladder

- Alinco Inc.

- Hermans

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising residential renovation & DIY culture

- 4.2.2 Heightened safety regulations in construction

- 4.2.3 Growing infrastructure spending in emerging economies

- 4.2.4 Expansion of e-commerce warehouse networks

- 4.2.5 Adoption of GFRP ladders in high-voltage maintenance

- 4.2.6 IoT-enabled usage analytics in rental fleets

- 4.3 Market Restraints

- 4.3.1 Volatility in raw-material prices

- 4.3.2 Ladder-related injuries prompting alternatives

- 4.3.3 Rental model cannibalizing new sales

- 4.3.4 Drone/MEWP substitution for inspection tasks

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Industry

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Step Ladders

- 5.1.2 Extension Ladders

- 5.1.3 Platform Ladders

- 5.1.4 Folding Ladders

- 5.1.5 Telescopic Ladders

- 5.1.6 Specialty/Custom Ladders

- 5.2 By Material

- 5.2.1 Aluminum

- 5.2.2 Fiberglass

- 5.2.3 Steel

- 5.2.4 Wood

- 5.2.5 Plastic/Composite

- 5.3 By End-User Industry

- 5.3.1 Residential / DIY

- 5.3.2 Construction

- 5.3.3 Industrial Manufacturing

- 5.3.4 Utilities & Telecom

- 5.3.5 Commercial & Institutional

- 5.3.6 Transportation & Logistics

- 5.4 By Distribution Channel

- 5.4.1 Offline (Home-Improvement Stores, Industrial Distributors)

- 5.4.2 Online (E-commerce Platforms, Direct-to-Consumer)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Peru

- 5.5.2.3 Chile

- 5.5.2.4 Argentina

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 BENELUX

- 5.5.3.7 NORDICS

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 India

- 5.5.4.2 China

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 South-East Asia

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East & Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle East & Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 WernerCo

- 6.4.2 Louisville Ladder Inc.

- 6.4.3 Little Giant Ladders (Wing Enterprises)

- 6.4.4 Zarges GmbH

- 6.4.5 Hailo Werk

- 6.4.6 Altrex B.V.

- 6.4.7 KRAUSE-Werk GmbH

- 6.4.8 Youngman Group (Werner UK)

- 6.4.9 Gorilla Ladders (Tricam)

- 6.4.10 Tubesca-Comabi

- 6.4.11 Telesteps AB

- 6.4.12 Featherlite Ladders

- 6.4.13 FACAL

- 6.4.14 Hymer-Leichtmetallbau

- 6.4.15 ABRU (Werner)

- 6.4.16 Shanghai Ruiju Tools

- 6.4.17 Zhejiang Yongkang Chuangxin

- 6.4.18 Jinma Ladder

- 6.4.19 Alinco Inc.

- 6.4.20 Hermans

7 Market Opportunities & Future Outlook

- 7.1 Multi-Functional and Space-Saving Ladder Solutions

- 7.2 Rising DIY Culture Boosting Household Ladder Demand