|

시장보고서

상품코드

1906256

포스포아미다이트 시장 : 점유율 분석, 업계 동향, 통계, 성장 예측(2026-2031년)Phosphoramidite - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

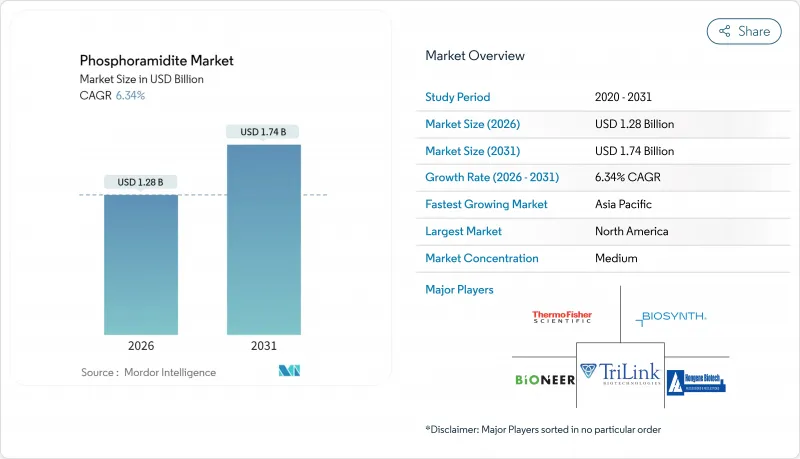

2026년 포스포아미다이트 시장 규모는 12억 8,000만 달러로 추정되며, 2025년 12억 달러에서 성장한 수치입니다.

2031년까지 17억 4,000만 달러에 달하고, 2026년부터 2031년에 걸쳐 CAGR 6.34%로 성장할 전망입니다.

치료용 올리고뉴클레오티드, 유전자 편집 기술의 진보, 합성 생물학의 규모 확대가 함께 견고한 수요의 기세를 지지하고 있습니다. 2024년 미국 식품의약국(FDA)이 승인한 2가지 약물인 이메테르스타트와 올레자르센이 이 약물 클래스의 효능을 입증하여 밸류체인 전체에서 생산 능력 증강을 촉구했습니다. 병렬로 수행된 높은 처리량 합성 기술에 대한 투자로 단위 비용이 저하되고 진단 및 연구 응용 분야에서의 가용성이 향상되었습니다. 유전체 의료에 대한 정부 보조금과 지리적으로 분산된 공급망 확보를 위한 업계의 노력이 함께 장기적인 소비 전망을 더욱 강화하고 있습니다.

세계 포스포아미다이트 시장 동향과 인사이트

핵산 치료제 파이프라인의 급속한 확장

2024년에 승인된 2가지 퍼스트 인 클래스 약물인 이메테르스타트와 올레잘센은 안티센스 및 GalNAc 결합 플랫폼의 임상적 효능을 확인하였으며, 현재 전 세계적으로 진행 중인 229건의 종양학 시험을 뒷받침했습니다. 같은 해 발행된 종합적인 FDA 지침은 약리학 및 안전성에 대한 요구사항을 간소화하고 개발 기간을 단축했습니다. 이러한 시너지 효과는 Kg 규모의 GMP 호환 포스포아미다이트를 필요로 하는 후기 개발 단계의 자산을 급증하고 있습니다. 각 후보 약물이 초기 단계부터 상업화에 이르는 과정에서 제조 규모가 그램 단위에서 수 톤 단위로 확대되므로 연간 수요가 두 배로 늘어납니다. 제약 포트폴리오가 희귀질환에서 일반적인 심대사 질환으로 전환함에 따라 환자 집단당 재료 수요는 더욱 팽창하고 수요 전망은 향후 10년간 지속될 전망입니다.

합성 생물학 플랫폼의 채택 가속

RNA 백신, 정밀효소, 바이오 베이스 화학제품에 견인되어 합성 생물학 분야 전체가 두 자릿수 성장을 이루고 있습니다. DNA 파운드리와 클라우드 기반 설계 도구는 엄청난 양의 포스포아미다이트를 소비하는 초고처리량 합성을 지원합니다. Codexis의 98% 커플링 효율 플랫폼과 같은 효소적 접근법은 불순물을 줄이고 기존의 화학적 방법을 보완합니다. 인공지능의 통합으로 구축 설계가 최적화되어 배열의 복잡성과 길이가 향상. 둘 다 배치 당 시약 사용량 증가로 이어집니다. 미국, 독일, 싱가포르의 새로운 바이오 파운드리의 설비 투자는 화학 합성 빌딩 블록에 대한 개발자의 확고한 신뢰를 뒷받침합니다.

GMP 등급 제조 시설의 고액 자본 요구 사항

아길렌트사가 2026년 조업 개시로 올리고뉴클레오티드 생산량을 두배로 하는 2025년의 발표가 나타내는 바와 같이, 신규 플랜트 확장 단체로 7억 2,500만 달러를 넘는 케이스가 있습니다. 건설의 복잡성은 반응기 군, 용매 회수 시스템, 클래스 C 클린 룸 및 검증 기간은 여러 해에 걸쳐 있습니다. 소규모 신규 진입기업은 동등한 자금조달에 어려움을 겪는 경우가 많아 그 결과 재무기반의 견고한 기존기업에 생산능력이 집중되고 있습니다. 회수기간의 장기화와 기술의 진부화 전망은 투자 리스크를 증폭시켜 수요 증가에도 불구하고 시장 진입을 억제하는 요인이 되고 있습니다.

부문 분석

2025년 시점에서 DNA 포스포아미다이트는 포스포아미다이트 시장 점유율의 51.85%를 차지하고, 안티센스 및 진단 프로브 합성에 있어서 핵심적인 역할에 의해 계속 시장을 견인하고 있습니다. LNA 하위 유형은 기반 규모야말로 작은 것, 생체내 안정성 요구의 높아짐을 받아, 8.21%의 연평균 복합 성장률(CAGR)로 다른 화학종을 웃도는 성장이 전망됩니다. DNA 기반 변이체용 포스포아미다이트 시장 규모는 수 Kg 규모의 종양학 및 심장병학 영역에서의 의약품 개발이 후기 임상시험 단계에 들어가면서 꾸준히 확대될 것으로 예측됩니다. 학술 분야의 지속적인 수요 외에도 새로운 CRISPR 가이드 RNA 워크플로우가 RNA 포스포아미다이트 수요를 지원하는 반면, 2'-O-메틸화 및 티오포스페이트와 같은 특수 수식은 높은 가격대의 틈새 시장을 형성하고 있습니다.

아실화 염기를 위한 1,3-디티안-2-일루메톡시카르보닐법으로 대표되는 다변형 전략의 진전은 병용 요법의 설계 가능성을 확대하고 있습니다. 다수의 생명 공학 기업들이 시험 중인 효소적 라이게이션 구축 방법은 특히 고도로 변형된 골격에서 화학적 DNA 아미도이트와 경쟁하는 것이 아니라 보완하는 것입니다.

2025년 제약 및 바이오테크놀러지 기업은 치료 파이프라인의 확대와 수직 통합형 제조에 대한 의욕을 배경으로 포스포아미다이트 시장의 56.74%를 차지했습니다. 그러나 아웃소싱의 동향은 CDMO(수탁개발제조기관) 및 CRO(수탁연구기관)를 뒷받침하고 있으며, 그 CAGR9.18%는 예측기간 내에서 가장 빠른 성장을 나타내고 있습니다. WuXi STA의 27개의 가동 올리고뉴클레오티드 라인과 TriLink의 CleanCap 라이선싱 모델은 활발한 서비스 수요를 뒷받침합니다. 학술기관은 일정한 기반 수요를 유지하고 있는 한편, 진단실험실에서는 규제 대상의 검사 키트용으로 고순도 로트의 주문이 증가하고 있습니다.

지역별 분석

북미는 2025년에 39.78%의 매출 점유율을 차지했고, 확립된 규제의 명확성, 대규모 개발 기업의 존재, 그리고 중요한 벤처 캐피탈의 유입에 지지를 받고 있습니다. 머크 KGaA에 의한 미주리 주 바이오컨쥬게이션 시설로의 7,600만 달러의 업그레이드는 이 지역에서 지속적인 자본 집약화를 보여줍니다. 미국은 또한 TriLink의 라이선싱 에코시스템을 통한 CleanCap 대응 mRNA 기술에서도 주도적인 입장에 있으며, 국내 혁신 클러스터를 강화하고 있습니다.

아시아태평양은 2031년까지 연평균 복합 성장률(CAGR) 7.29%에서 생산 비용이 낮고 선진 치료법에 대한 내부 수요 증가를 원동력으로 성장할 것으로 예측됩니다. 2024년 초부터 가동하고 있는 우시 STA의 169에이커(약 68만㎡)의 태흥시설은 국내 CDMO가 도달하고 있는 규모를 상징하고 있습니다. '중국+여러 국가' 조달을 촉구하는 정책 전환과 개정된 스파이 방지 규제가 함께 다국적 기업은 인도, 베트남, 태국에 공급원을 분산시켜 공급망의 지역 구조를 재구축하고 있습니다.

유럽은 선진적인 제조 기술과 엄격한 품질 기준으로 전략적 기반을 유지하고 있습니다. 바이오스프링사의 오펜바흐 RNA 메가파실리티는 2027년 완성을 예정하고 있으며, 세계 최대급의 핵산 전용 플랜트로서 고부가가치 바이오의약에 대한 지역적 대처를 뒷받침하고 있습니다. 유럽 제약 올리고뉴클레오티드 컨소시엄의 조화 작업과 함께, 이 지역은 제조 기술의 탁월성과 그린 케미스트리 도입에 있어서의 기준점이 계속되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 핵산 치료제 파이프라인의 급속한 확대

- 합성 생물학 플랫폼의 도입 가속

- 맞춤형 의료 및 진단법에 대한 수요의 확대

- 유전체 조사 이니셔티브에 대한 정부 자금

- 고처리량 올리고 합성(High-Throughput Oligo Synthesis) 기술 발전

- 안전한 바이오의약품 공급망에 대한 전략적 투자

- 시장 성장 억제요인

- GMP 등급 제조 시설에 대한 높은 자본 요건

- 원료의 순도에 관한 엄격한 규제 기준

- 용제 폐기물 처리에 관한 환경 문제

- 복잡한 올리고 화학 분야에서의 숙련 노동력 부족

- 규제 상황

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 유형별

- DNA 포스포아미다이트

- RNA 포스포아미다이트

- LNA 포스포아미다이트

- 2'-O-메틸화 RNA 포스포아미다이트

- 전문분야/개질 포스포아미다이트

- 최종 사용자별

- 제약 및 바이오테크놀러지 기업

- 학술기관 및 연구기관

- CDMO 및 CRO

- 진단 실험실

- 기타 최종 사용자

- 용도별

- 치료용 올리고뉴클레오타이드(Therapeutic Oligonucleotides)

- 진단약

- 유전자 및 세포 치료

- 합성 생물학 및 유전자 편집

- 조사 도구

- 순도 등급별

- 표준 조사 등급

- HPLC 등급

- GMP 등급

- 초고순도 등급

- 합성 방법별

- 고체상 화학 합성

- 효소적 DNA/RNA 합성

- 하이브리드 화학-효소법

- 생산규모별

- 연구/발견 규모(<1 mmol)

- 파일럿/임상 규모(1>100 mmol)

- 상업/GMP 제조 규모(1>100 mmol)

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Thermo Fisher Scientific Inc.

- Danaher Corp.(Integrated DNA Technologies)

- Merck KGaA(Sigma-Aldrich)

- Biosynth Ltd

- TriLink BioTechnologies

- Bioneer Corporation

- Hongene Biotech Corp.

- LGC Biosearch Technologies

- Glen Research

- Bachem AG

- Eurofins Genomics

- Synbio Technologies

- PolyOrg, Inc.

- Creative Biolabs, Inc.

- Lumiprobe Corp.

- QIAGEN NV

- Agilent Technologies Inc.

- Twist Bioscience

- BOC Sciences

- GenScript Biotech

제7장 시장 기회와 장래의 전망

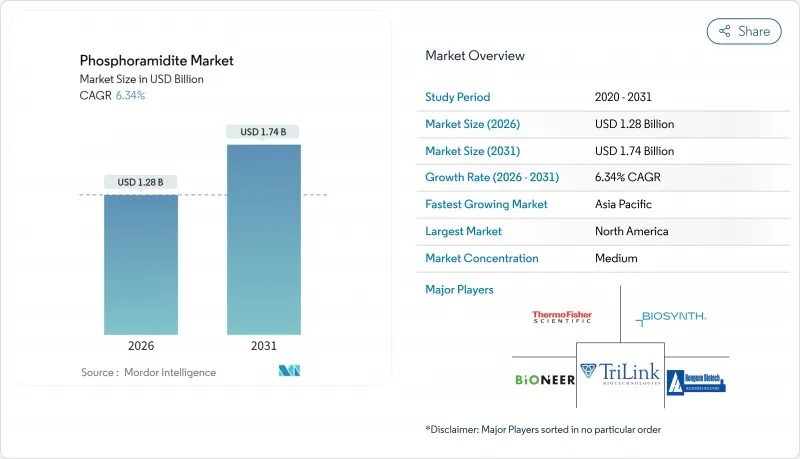

SHW 26.01.22Phosphoramidite market size in 2026 is estimated at USD 1.28 billion, growing from 2025 value of USD 1.20 billion with 2031 projections showing USD 1.74 billion, growing at 6.34% CAGR over 2026-2031.

Therapeutic oligonucleotides, gene-editing advances, and synthetic biology scale-up collectively underpin robust demand momentum. Two United States Food and Drug Administration approvals in 2024-imetelstat and olezarsen-validated the drug-class and triggered capacity additions across the value chain. Parallel investments in high-throughput synthesis technologies have lowered unit costs, improving accessibility for diagnostics and research applications. Government grants for genomic medicine along with industry initiatives to secure geographically diverse supply chains further reinforce long-term consumption prospects.

Global Phosphoramidite Market Trends and Insights

Rapid Expansion of Nucleic Acid Therapeutics Pipeline

Two first-in-class approvals in 2024, imetelstat and olezarsen, confirmed clinical efficacy for antisense and GalNAc-conjugated platforms and encouraged 229 oncology trials now active worldwide. Comprehensive FDA guidance issued the same year has streamlined pharmacology and safety expectations, shortening development timelines. The cumulative result is a rising pool of late-stage assets requiring kilogram-scale GMP phosphoramidites. Each candidate's progression from early stage to commercial launch multiplies annual demand because manufacturing campaigns scale from grams to multiple metric tons. As pharmaceutical portfolios pivot from rare disorders to prevalent cardiometabolic diseases the material requirement per patient cohort swells further, extending demand visibility into the next decade.

Accelerating Adoption of Synthetic Biology Platforms

The wider synthetic biology arena is expanding at double-digit rates, driven by RNA vaccines, precision enzymes, and bio-based chemicals. DNA foundries and cloud-based design tools support ultrahigh-throughput syntheses that consume vast volumes of phosphoramidites. Enzymatic approaches such as Codexis' 98% coupling-efficiency platform reduce impurities and complement established chemical methods without yet displacing them. Integration of artificial intelligence optimizes construct design, raising sequence complexity and length, both of which raise reagent usage per batch. Capital spending by new biofoundries in the United States, Germany, and Singapore evidences durable developer confidence in chemically synthesized building blocks.

High Capital Requirements for GMP-Grade Manufacturing Facilities

A single greenfield plant expansion can exceed USD 725 million, as confirmed by Agilent's 2025 announcement to double oligonucleotide output with operations commencing in 2026. Build-out complexity spans reactor suites, solvent recovery systems, and Class C cleanrooms, while validation timelines stretch to multiple years. Smaller entrants often struggle to marshal comparable funding, which concentrates capacity among financially robust incumbents. Extended payback periods and the prospect of technology obsolescence amplify investment risk, thereby tempering market entry despite rising demand.

Other drivers and restraints analyzed in the detailed report include:

- Growing Demand for Personalized Medicine and Diagnostics

- Government Funding for Genomic Research Initiatives

- Stringent Regulatory Standards for Raw Material Purity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

DNA phosphoramidites held 51.85% of the phosphoramidite market share in 2025 and continue anchoring the phosphoramidite market thanks to their central role in antisense and diagnostic probe synthesis. LNA subtypes, while representing a smaller base, are forecast to outpace other chemistries at an 8.21% CAGR amid rising in vivo stability needs. The phosphoramidite market size for DNA-based variants is projected to expand steadily as multi-kilogram oncology and cardiology drug campaigns enter late-stage trials. Continued academic demand plus new CRISPR guide-RNA workflows sustain RNA amidite volume, whereas specialty modifications such as 2'-O-methyl and thiophosphate commands premium pricing niches.

Advances in multi-modification strategies, exemplified by the 1,3-dithian-2-yl-methoxycarbonyl method for acylated bases, are broadening design possibilities for combination therapies. Enzymatic ligation-based construction methods trialed by several biotech firms complement, rather than compete with, chemical DNA amidites, particularly for highly modified backbones.

Pharmaceutical and biotechnology enterprises consumed 56.74% of the phosphoramidite market in 2025, driven by expanding therapeutic pipelines and vertically integrated manufacturing ambitions. Outsourcing trends nonetheless propel CDMOs and CROs, whose 9.18% CAGR marks the fastest uptake in the forecast horizon. WuXi STA's 27 operational oligonucleotide lines and TriLink's CleanCap licensing model attest to brisk service demand. Academic institutions preserve a meaningful baseline volume, while diagnostic labs increasingly order high-purity lots for regulated test kits.

The Phosphoramidite Market Report is Segmented by Type (DNA Phosphoramidites, and More), End-User (Pharmaceutical & Biotechnology Companies, and More), Application (Therapeutic Oligonucleotides, and More), Purity Grade (Standard Research Grade, and More), Synthesis Method (Solid-Phase Chemical Synthesis, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America posted 39.78% revenue share in 2025, underpinned by established regulatory clarity, large developer presence, and significant venture-capital flows. Merck KGaA's USD 76 million upgrade of its Missouri bioconjugation site illustrates sustained capital deepening within the region. The United States also leads in CleanCap-enabled mRNA technologies through TriLink's licensing ecosystem, reinforcing domestic innovation clusters.

Asia-Pacific is forecast to grow at 7.29% CAGR through 2031, propelled by lower production costs and rising internal demand for advanced therapies. WuXi STA's 169-acre Taixing facility, operational since early 2024, exemplifies the scale domestic CDMOs are reaching. Policy shifts encouraging "China-plus-many" sourcing, combined with updated anti-espionage regulations, are prompting multinational firms to diversify across India, Vietnam, and Thailand, reshaping supply-chain geography.

Europe maintains a strategic foothold through advanced manufacturing and rigorous quality norms. BioSpring's Offenbach RNA megafacility, on track for completion in 2027, will be among the world's largest dedicated nucleic-acid plants, underscoring regional commitment to high-value biologics. Coupled with the European Pharma Oligonucleotide Consortium's harmonization work, the continent remains a reference point for manufacturing excellence and green-chemistry adoption.

- Thermo Fisher Scientific

- Danaher Corp. (Integrated DNA Technologies)

- Merck

- Biosynth Ltd

- TriLink BioTechnologies

- Bioneer

- Hongene Biotech Corp.

- LGC Biosearch Technologies

- Glen Research

- Bachem AG

- Eurofins

- Synbio Technologies

- PolyOrg, Inc.

- Creative Biolabs, Inc.

- Lumiprobe Corp.

- QIAGEN

- Agilent Technologies

- Twist Bioscience

- BOC Sciences

- GenScript Biotech

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Expansion of Nucleic Acid Therapeutics Pipeline

- 4.2.2 Accelerating Adoption of Synthetic Biology Platforms

- 4.2.3 Growing Demand For Personalized Medicine and Diagnostics

- 4.2.4 Government Funding For Genomic Research Initiatives

- 4.2.5 Technological Advancements in High-Throughput Oligo Synthesis

- 4.2.6 Strategic Investments in Secure Biopharma Supply Chains

- 4.3 Market Restraints

- 4.3.1 High Capital Requirements for GMP-Grade Manufacturing Facilities

- 4.3.2 Stringent Regulatory Standards for Raw Material Purity

- 4.3.3 Environmental Concerns Over Solvent Waste Disposal

- 4.3.4 Limited Skilled Workforce For Complex Oligo Chemistry

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat Of New Entrants

- 4.5.2 Bargaining Power Of Buyers

- 4.5.3 Bargaining Power Of Suppliers

- 4.5.4 Threat Of Substitutes

- 4.5.5 Intensity Of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Type

- 5.1.1 DNA Phosphoramidites

- 5.1.2 RNA Phosphoramidites

- 5.1.3 LNA Phosphoramidites

- 5.1.4 2'-O-Methyl RNA Phosphoramidites

- 5.1.5 Specialty / Modified Phosphoramidites

- 5.2 By End-User

- 5.2.1 Pharmaceutical & Biotechnology Companies

- 5.2.2 Academic & Research Institutes

- 5.2.3 CDMOs & CROs

- 5.2.4 Diagnostic Laboratories

- 5.2.5 Other End-Users

- 5.3 By Application

- 5.3.1 Therapeutic Oligonucleotides

- 5.3.2 Diagnostics

- 5.3.3 Gene & Cell Therapy

- 5.3.4 Synthetic Biology & Gene Editing

- 5.3.5 Research Tools

- 5.4 By Purity Grade

- 5.4.1 Standard Research Grade

- 5.4.2 HPLC Grade

- 5.4.3 GMP Grade

- 5.4.4 Ultra-High Purity Grade

- 5.5 By Synthesis Method

- 5.5.1 Solid-Phase Chemical Synthesis

- 5.5.2 Enzymatic DNA/RNA Synthesis

- 5.5.3 Hybrid Chemical-Enzymatic

- 5.6 By Production Scale

- 5.6.1 Research / Discovery Scale (<1 mmol)

- 5.6.2 Pilot / Clinical Scale (1>100 mmol)

- 5.6.3 Commercial / GMP Manufacturing Scale (>100 mmol)

- 5.7 Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 Japan

- 5.7.3.3 India

- 5.7.3.4 Australia

- 5.7.3.5 South Korea

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 Middle East & Africa

- 5.7.4.1 GCC

- 5.7.4.2 South Africa

- 5.7.4.3 Rest of Middle East & Africa

- 5.7.5 South America

- 5.7.5.1 Brazil

- 5.7.5.2 Argentina

- 5.7.5.3 Rest of South America

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Thermo Fisher Scientific Inc.

- 6.3.2 Danaher Corp. (Integrated DNA Technologies)

- 6.3.3 Merck KGaA (Sigma-Aldrich)

- 6.3.4 Biosynth Ltd

- 6.3.5 TriLink BioTechnologies

- 6.3.6 Bioneer Corporation

- 6.3.7 Hongene Biotech Corp.

- 6.3.8 LGC Biosearch Technologies

- 6.3.9 Glen Research

- 6.3.10 Bachem AG

- 6.3.11 Eurofins Genomics

- 6.3.12 Synbio Technologies

- 6.3.13 PolyOrg, Inc.

- 6.3.14 Creative Biolabs, Inc.

- 6.3.15 Lumiprobe Corp.

- 6.3.16 QIAGEN N.V.

- 6.3.17 Agilent Technologies Inc.

- 6.3.18 Twist Bioscience

- 6.3.19 BOC Sciences

- 6.3.20 GenScript Biotech

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment