|

시장보고서

상품코드

1906257

전동 공구 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Power Tools - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

전동 공구 시장은 2025년 769억 6,000만 달러에서 2026년에는 821억 6,000만 달러로 성장하고 2026년부터 2031년에 걸쳐 CAGR 6.76%로 성장을 지속하여 2031년까지 1,139억 2,000만 달러에 이를 전망입니다.

인프라 정비 계획의 확대, 급속한 도시화, 무선 기술로의 전환이 공급망이 정상화되는 중에서도 수요를 뒷받침하고 있습니다. 무선화는 작업 현장의 생산성을 재정의하고 있으며 주요 도시의 배출 규제 강화가 공기압식 및 가솔린식 유닛에서 배터리 구동 플랫폼으로의 전환을 가속화하고 있습니다. 신흥경제국의 DIY 참여율 상승과 전자상거래에 대한 접근 확대가 소비자 기반을 넓히고 아시아와 유럽에서 스마트 제조 장려책이 고정밀도 공구 시스템에 대한 현장 투자를 촉진하고 있습니다. 경쟁의 치열성은 여전히 중간 규모이며, 주요 기업은 차별화된 배터리 생태계를 통해 점유율을 보호하는 반면, 중국의 신규 진입기업은 현지 생산과 적극적인 가격 설정을 활용하고 있습니다.

세계의 전동 공구 시장의 동향 및 인사이트

고출력 밀도를 실현하는 리튬 이온 배터리 플랫폼으로의 전환

배터리 셀 기술은 매년 연간 5-7%의 에너지 밀도 향상을 달성하고 있으며, 시공업자에게는 유선 공구와 동급의 가동 시간과 무선의 기동성이라는 이점을 제공하고 있습니다. DEWALT의 탭리스 셀 구조는 출력을 50% 향상시키면서 경량화를 실현해, 지붕 시공 및 전기 공사 기술자들이 토크 손실 없이 더 가벼운 배터리 팩을 휴대할 수 있도록 합니다.

북미 및 유럽에서의 건설 기계 전동화

미국 및 캐나다 건설 관리자의 66%가 배출량 규제와 라이프사이클 비용 절감을 이유로 2년 이내에 완전 전동화 현장이 실현될 것으로 전망하고 있습니다. 유럽 지자체도 같은 목표를 추구하고 있으며, 볼보 등 OEM 제조업체는 2030년까지 완전 전동 라인업을 선언했습니다. 이동식 급속 충전기의 보급에 의해 범위에 대한 불안도 줄어들고 있습니다. 도시 프로젝트에서는 배터리식 또는 유선 전동 공구의 사용이 증가하고 있어 공기압 및 유압식 공구 부문에 압력을 가하는 한편, 송전망이 정비되지 않은 격오지에서는 엔진 구동 유닛의 틈새 시장이 남아 있습니다. 전체 전동 플릿을 도입한 건설업자는 최대 60%의 CO2 저감과 30%의 납기 단축을 보고하고 있어 투자 회수의 유효성을 뒷받침하고 있습니다.

리튬 코발트 가격의 변동으로 무선 제품의 부품 원가 상승

미국의 관세조치로 중국제 리튬이온전지의 종합관세율은 2025년에 58%까지 인상되었으며 OEM의 이익률과 소매가격에 압력을 가하고 있습니다. 배터리 부품은 고출력 무선 공구 비용의 30-40%를 차지하고 있으며, 스팟 가격의 상승으로 제조업체는 공급 확보와 가격 안정화를 위해 호주와 아프리카에서의 대체 조달 계약의 협상을 요구받고 있습니다.

부문 분석

전동 공구 시장에서 전동식은 2025년 매출의 63.02%를 차지했습니다. 무선 하위 부문은 리튬 이온 팩의 성능이 유선 제품의 성능에 가까워짐에 따라 2031년까지 연평균 복합 성장률(CAGR) 7.24%로 확대될 전망입니다. 공기압식 공구는 기존의 압축공기 시스템이 존재하는 분야에서 지위를 유지하고, 유압식 공구는 교량 장력 조정 등 초고토크가 필요한 틈새 시장에 대응하고 있습니다. 엔진 구동식 장비는 도시 지역의 소음 규제 및 배출 가스 규제로 인해 오프그리드 건설 현장 및 임업 작업으로 제한됩니다. 다중 브랜드의 배터리 통합을 통한 소유 비용 절감과 충전 인프라 간소화로 무선 솔루션의 전동 공구 시장 내 규모가 급증할 것으로 전망됩니다. 그러나 원재료 가격의 변동과 개발도상지역에서의 급속 충전의 보급 제한에 따라 가격을 중시하는 사용자층에서는 유선 유닛에 대한 수요가 유지됩니다.

인체공학적 설계의 향상, 브러쉬리스 구동, 펌웨어 업데이트가 현재는 프리미엄 무선 제품의 차별화 요인이 되고 있습니다. 보쉬의 '프로페셔널 18V 시스템'과 마키타의 'LXT 교체식 배터리 팩'은 에코시스템의 일관성이 고객 충성도를 보장하는 방법을 제시합니다. 플릿 관리자는 케이블이 없는 작업 현장에 의한 다운타임의 단축과 안전성의 향상을 평가하면서 이러한 이행을 뒷받침하고 있습니다.

2025년 전동 공구 시장에서 드릴 및 체결 공구는 매출의 31.88%를 차지하였으며 건설 현장과 조립 라인에서의 보급도를 반영하고 있습니다. 임팩트 드라이버 및 렌치는 자동차 및 항공우주 분야에서 체결 사양의 엄격화(정확한 토크 관리 및 추적성을 위한 데이터 수집이 요구됨)에 의해 CAGR 7.78%로 성장을 지속하고 있습니다. 절단 및 절삭 공구는 견조하게 유지되고 있으며, 보쉬가 도입한 초경 칩 블레이드는 바이메탈제에 비해 20배의 수명을 실현하여 대량 생산을 실시하는 목공 장인에게 인기를 얻고 있습니다.

HAVS 대책 규제에 의해 잭해머의 재설계가 진행되었으며 보쉬의 무선 GSH 18V-5는 8.5J의 충격 에너지와 진동 저감을 위한 가변 속도 제어를 양립시키고 있습니다. 히트건과 무선 접착 공구 등 신흥 부문은 내장 및 전자기기 수리 분야에서 수요를 확대하여 기존 건설업을 넘어 시장을 개척하고 있습니다. 가격 경쟁이 격화하는 가운데, 프리미엄 브러쉬리스 제품군이 종합적으로 기여하여 일류 브랜드의 전동 공구 시장 내 점유율 유지를 뒷받침하고 있습니다.

지역별 분석

아시아태평양은 2025년 전동 공구 시장에서 세계 매출의 39.55%를 차지하였으며 7.61%의 연평균 복합 성장률(CAGR)이 전망되고 있습니다. 이는 중국의 고도화 계획에 근거한 25%의 설비 투자 증가와 국내외 OEM 제조업체를 끌어들이는 인도의 '메이크 인 인디아' 정책에 뒷받침되고 있습니다. 지역에 근거한 배터리 팩 생산과 가처분 소득 증가가 무선 제품의 보급을 촉진하는 한편, 성숙하면서도 혁신을 중시하는 일본 시장에서는 프리미엄 브러쉬리스 모델에 의한 제품 차별화를 도모하고 있습니다.

북미는 전동 공구 시장에서 기술적으로 선진적이면서 성장 속도가 완만한 지역입니다. 미국 렌탈협회(ARA)는 2024년 설비 렌탈 수익이 773억 달러에 달한 것으로 발표했으며 이는 지속적인 수요 기반의 견조함을 뒷받침하고 있습니다. 그러나 중국제 배터리에 대한 관세가 조달 비용을 밀어 올려 멕시코에서의 니어 쇼어링을 촉진하고 있습니다. 이 나라에서는 공구 수입이 두 자릿수로 성장하여 관세 회피를 위한 공급망의 재구축이 진행되고 있습니다.

유럽의 전동 공구 시장은 지역에 따라 다른 동향을 보여줍니다. 서유럽 시장에서는 렌탈 채널 포화와 엄격한 HAVS 규제가 과제가 되는 반면, 동유럽은 EU 자금과 새로운 제조 능력의 혜택을 받고 있습니다. EU의 81억 유로 규모의 IPCEI 이니셔티브는 스마트 공장 투자를 촉진하고 연결형 정밀 공구에 대한 수요를 창출하고 있습니다. 환경 규제 대응의 압력에 의해 전동 모델이 우위가 되고 주요 OEM 제조업체는 저진동 인증이나 재사용 가능한 포장으로 차별화를 도모하고 있습니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- 북미 및 유럽에서의 건설 기계 플릿 전동화

- 아시아에서의 전자상거래의 침투로 DIY 문화 확대 촉진

- 자동차의 경량화로 고정밀도가 요구되고 브러쉬리스 공구의 도입 촉진

- 스마트 제조에 대한 정부 인센티브(예 : 중국 제조 2025, EU의 IPCEI)

- 고출력 밀도를 실현하는 무선 공구를 실현하는 리튬 이온 전지 플랫폼으로의 이행

- 건설업자 간에서의 모듈식 및 구독형 툴 온디맨드 프로그램의 급증

- 억제요인

- 리튬 및 코발트 가격의 변동으로 무선 공구의 부품 원가 상승

- 서유럽에서의 성숙 렌탈 채널의 포화 상태

- 수완 진동 증후군(HAVS)에 관한 규제상의 우려로 중기 해체 공구의 도입 제한

- 신흥 시장에서 위조품 공급이 단편화되어 브랜드 프리미엄 훼손

- 가치 및 공급망 분석

- 규제 및 업계 정책 전망

- 기술 전망

- 업계의 매력도 - Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 유통 채널 분석

제5장 시장 규모 및 성장 예측

- 동작 모드별

- 전기

- 무선

- 유선

- 공기압

- 유압

- 엔진 구동식

- 전기

- 제품별

- 굴착 및 체결 공구

- 절삭 및 절단 공구

- 연삭 및 연마 공구

- 제거 공구(썬더 등)

- 해체 공구(브레이커, 잭해머)

- 임팩트 드라이버 및 렌치

- 네일러 및 스테이플러

- 기타(히트건, 접착건, 믹서, 특수 공구)

- 최종 사용자별

- 건설 및 인프라

- 자동차

- 항공우주 및 방위

- 에너지 및 발전

- 조선, 선박, 철도

- 제조업(전자기기, 금속 가공, 목공 등)

- 주택 및 DIY

- 기타(유틸리티, 광업 등)

- 판매 채널별

- 오프라인

- 직접 산업용 및 유통업체용

- 양판점 및 철물점

- 온라인

- 전자상거래 마켓플레이스

- 자사 운영 디지털 스토어

- 오프라인

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 페루

- 기타 남미

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 베네룩스(벨기에, 네덜란드, 룩셈부르크)

- 북유럽 국가(덴마크, 핀란드, 아이슬란드, 노르웨이, 스웨덴)

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- ASEAN(인도네시아, 태국, 필리핀, 말레이시아, 베트남)

- 기타 아시아태평양

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 카타르

- 쿠웨이트

- 튀르키예

- 이집트

- 남아프리카

- 나이지리아

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 움직임(M&A, 제휴, 제품 발매)

- 시장 점유율 분석

- 기업 프로파일

- Stanley Black & Decker Inc.

- Robert Bosch GmbH

- Techtronic Industries Co. Ltd.

- Makita Corporation

- Hilti Corporation

- Atlas Copco AB

- Ingersoll Rand Inc.

- Snap-on Incorporated

- Apex Tool Group

- Emerson Electric Co.

- Husqvarna AB

- Honeywell International Inc.

- KYOCERA Corporation

- Festool GmbH

- Cummins Inc.(Tool segment)

- Hitachi Koki(HiKOKI)

- Illinois Tool Works(ITW)

- Ridgid(Emerson)

- Baier Power Tools

- Positec Tool Corporation

- Panasonic Life Solutions

- CEMBRE SpA

- CSUN Power Tools*

제7장 시장 기회 및 미래 전망

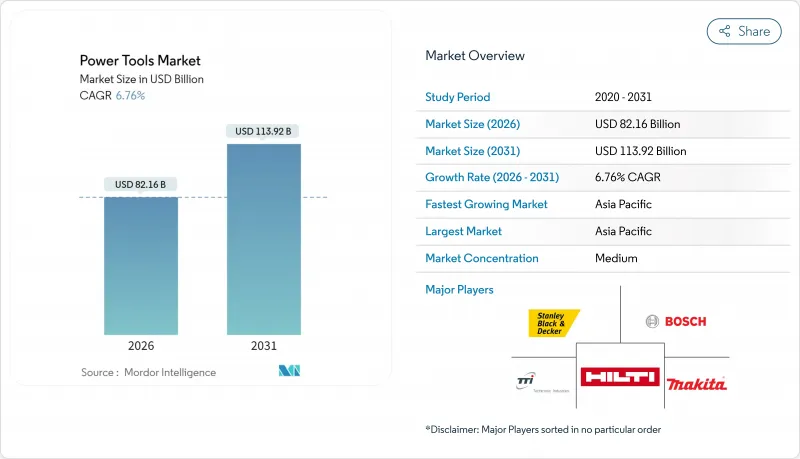

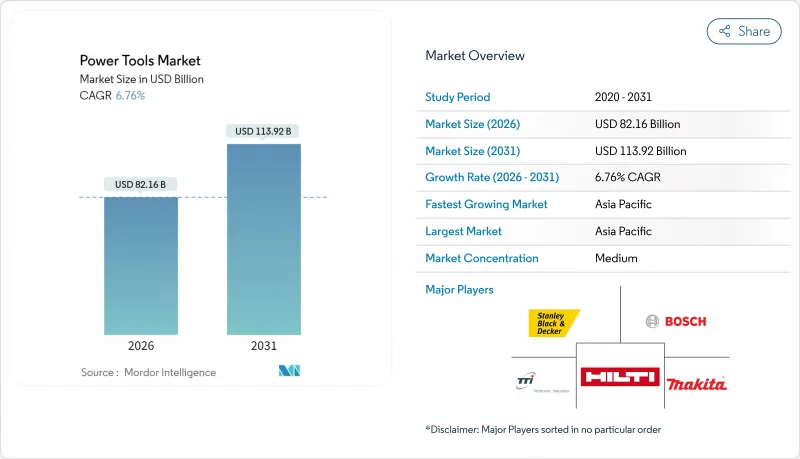

CSM 26.01.21The Power Tools market is expected to grow from USD 76.96 billion in 2025 to USD 82.16 billion in 2026 and is forecast to reach USD 113.92 billion by 2031 at 6.76% CAGR over 2026-2031.

Expanding infrastructure programs, rapid urbanization, and the shift toward cordless technologies sustain demand even as supply chains normalize. Cordless electrification is redefining job-site productivity, while stricter emissions rules in major cities accelerate the replacement of pneumatic and gas-powered units with battery platforms. Rising DIY participation and e-commerce access in emerging economies widen the consumer base, and smart manufacturing incentives in Asia and Europe stimulate factory-floor investments in high-precision, connected tool systems. Competitive intensity remains moderate; leaders safeguard their share through differentiated battery ecosystems, whereas new Chinese entrants leverage localized production and aggressive pricing.

Global Power Tools Market Trends and Insights

Shift to Lithium-ion Battery Platforms Enabling Higher Power Density Cordless Tools

Cell chemistries continue to raise energy density by 5-7% annually, giving contractors similar runtime to corded equivalents with the benefit of untethered mobility. DEWALT's tabless cell architecture boosts power 50% while shedding weight, allowing roofers and electricians to carry lighter packs without sacrificing torque.

Electrification of Construction Equipment Fleet in North America & Europe

Sixty-six percent of construction managers in the United States and Canada now expect fully electric jobsites within two years, citing emissions caps and lower lifetime running costs. European municipalities pursue similar goals; OEMs such as Volvo pledge all-electric line-ups by 2030 while mobile fast-charging rollouts shrink range anxiety. Urban projects increasingly specify battery or corded-electric tools, pressuring pneumatic and hydraulic segments yet leaving a niche for engine-driven units on remote sites lacking grid access. Contractors adopting all-electric fleets report up to 60% CO2 savings and 30% shorter project timelines, reinforcing the payback narrative.

Volatility in Lithium & Cobalt Prices Inflating Cordless BOM Cost

US tariffs have lifted the composite duty on Chinese lithium-ion batteries to 58% in 2025, pressuring OEM margins and retail prices. Battery inputs account for 30-40% of high-power cordless tool cost; spikes in spot prices force manufacturers to negotiate alternate offtake deals in Australia and Africa to secure supply and smooth pricing.

Other drivers and restraints analyzed in the detailed report include:

- Government Incentives for Smart Manufacturing

- DIY Culture Expansion Fueled by E-commerce Penetration in Asia

- Saturation of Mature Rental Channels in Western Europe

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Electric formats captured 63.02% of 2025 revenue in the power tool market, with cordless sub-segments expanding at 7.24% CAGR through 2031 as lithium-ion packs approach corded performance parity. Pneumatic tools retain footholds where compressed-air systems already exist, and hydraulic devices address ultra-high-torque niches such as bridge tensioning. Engine-driven equipment is relegated to off-grid construction and forestry operations due to urban noise and emissions limits. The power tools market size for cordless solutions is projected to widen sharply as multi-brand battery alliances cut ownership costs and simplify charging infrastructure. However, raw-material pricing swings and limited fast-charging availability in developing regions keep corded units relevant for price-sensitive users.

Enhanced ergonomics, brushless drives, and firmware updates now differentiate premium cordless products. Bosch's Professional 18V System and Makita's LXT interchangeable packs highlight how ecosystem consistency locks in customer loyalty. Fleet managers appreciate the reduced downtime and safety gains derived from cable-free worksites, reinforcing the transition.

Drilling and fastening tools accounted for 31.88% of 2025 revenue in the power tool market, reflecting their ubiquity across construction and assembly lines. Impact drivers and wrenches register an 7.78% CAGR thanks to automotive and aerospace tightening specifications that require exact torque and data capture for traceability. Sawing and cutting remain resilient; carbide-tipped blades introduced by Bosch offer 20x life versus bi-metal alternatives, appealing to high-volume carpenters.

Regulations targeting HAVS prompt redesigns in demolition hammers; Bosch's cordless GSH 18V-5 balances 8.5 J impact energy with adaptive speed control to mitigate vibration exposure. Emerging categories such as heat guns and cordless glue tools gain traction in decor and electronics rework, expanding the addressable universe beyond traditional construction trades. Collectively, premium brushless offerings underpin power tools market share retention for tier-one brands despite price competition.

The Power Tools Market is Segmented by Mode of Operation (Electric, and Others), by Product (Drilling & Fastening Tools, and Others), by End-User (Construction & Infrastructure, and Others), by Sales Channel (Offline and Online), and by Region (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 39.55% of 2025 global revenue in the power tool market and is poised for a 7.61% CAGR, anchored by China's 25% capital-investment hike under its upgrading plan and India's Make in India incentives that draw both domestic and foreign OEMs. Localized battery pack production and rising disposable incomes spur cordless adoption, while Japan's mature yet innovation-centric market relies on premium brushless models to differentiate offerings.

North America constitutes a technologically advanced yet slower-growing region in the power tools market. The American Rental Association expects equipment rental revenue to climb to USD 77.3 billion in 2024, reinforcing a substantial recurring demand base. Nevertheless, tariffs on Chinese batteries inflate procurement costs, motivating near-shoring in Mexico, where tool imports surge double digits and supply chains reconfigure to sidestep duties.

Europe shows divergent trajectories in the power tools market: Western markets see rental channel saturation and strict HAVS regulation, whereas Eastern Europe benefits from EU funding and fresh manufacturing capacity. The EU's EUR 8.1 billion IPCEI initiative stimulates smart-factory investments, generating demand for connected precision tools. Environmental compliance pressure favors electric models, and leading OEMs differentiate through low-vibration certifications and recyclable packaging.

- Stanley Black & Decker Inc.

- Robert Bosch GmbH

- Techtronic Industries Co. Ltd.

- Makita Corporation

- Hilti Corporation

- Atlas Copco AB

- Ingersoll Rand Inc.

- Snap-on Incorporated

- Apex Tool Group

- Emerson Electric Co.

- Husqvarna AB

- Honeywell International Inc.

- KYOCERA Corporation

- Festool GmbH

- Cummins Inc. (Tool segment)

- Hitachi Koki (HiKOKI)

- Illinois Tool Works (ITW)

- Ridgid (Emerson)

- Baier Power Tools

- Positec Tool Corporation

- Panasonic Life Solutions

- CEMBRE S.p.A.

- CSUN Power Tools*

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Electrification of Construction Equipment Fleet in North America & Europe

- 4.2.2 DIY Culture Expansion Fueled by E-commerce Penetration in Asia

- 4.2.3 Automotive Light-weighting Demands Higher Precision, Driving Brushless Tools Adoption

- 4.2.4 Government Incentives for Smart Manufacturing (e.g., Made-in-China 2025, EU IPCEI)

- 4.2.5 Shift to Lithium-ion Battery Platforms Enabling Higher Power Density Cordless Tools

- 4.2.6 Surge in Modular, Subscription-based Tool-on-Demand Programs Among Contractors

- 4.3 Market Restraints

- 4.3.1 Volatility in Lithium & Cobalt Prices Inflating Cordless Tool BOM Cost

- 4.3.2 Saturation of Mature Rental Channels in Western Europe

- 4.3.3 Regulatory Noise Around Hand-Arm Vibration Syndrome (HAVS) Limiting Heavy Demolition Tool Uptake

- 4.3.4 Fragmented Counterfeit Supply in Emerging Markets Undercutting Brand Premiums

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory & Industry Policies Outlook

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Distribution Channel Analysis

5 Market Size & Growth Forecasts (Value, In USD Billion)

- 5.1 By Mode of Operation

- 5.1.1 Electric

- 5.1.1.1 Cordless

- 5.1.1.2 Corded

- 5.1.2 Pneumatic

- 5.1.3 Hydraulic

- 5.1.4 Engine-Driven

- 5.1.1 Electric

- 5.2 By Product

- 5.2.1 Drilling & Fastening Tools

- 5.2.2 Sawing & Cutting Tools

- 5.2.3 Grinding & Polishing Tools

- 5.2.4 Material Removal Tools (sanders, etc.)

- 5.2.5 Demolition Tools (Breakers, Jackhammers)

- 5.2.6 Impact Drivers & Wrenches

- 5.2.7 Nailers & Staplers

- 5.2.8 Others (heat guns, glue guns, mixers, speciality tools)

- 5.3 By End-user

- 5.3.1 Construction & Infrastructure

- 5.3.2 Automotive

- 5.3.3 Aerospace & Defense

- 5.3.4 Energy & Power Generation

- 5.3.5 Shipbuilding, Marine & Railways

- 5.3.6 Manufacturing (Electronics, Metalworking, Wood Work, etc.)

- 5.3.7 Residential / DIY

- 5.3.8 Others (Utilities, Mining, etc.)

- 5.4 By Sales Channel

- 5.4.1 Offline

- 5.4.1.1 Direct Industrial/ Distributor

- 5.4.1.2 Mass Retail / Home Centers

- 5.4.2 Online

- 5.4.2.1 E-commerce Marketplaces

- 5.4.2.2 Brand-Owned Digital Stores

- 5.4.1 Offline

- 5.5 By Region

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Peru

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.5.3.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam)

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Qatar

- 5.5.5.4 Kuwait

- 5.5.5.5 Turkey

- 5.5.5.6 Egypt

- 5.5.5.7 South Africa

- 5.5.5.8 Nigeria

- 5.5.5.9 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, Product Launches)

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)}

- 6.4.1 Stanley Black & Decker Inc.

- 6.4.2 Robert Bosch GmbH

- 6.4.3 Techtronic Industries Co. Ltd.

- 6.4.4 Makita Corporation

- 6.4.5 Hilti Corporation

- 6.4.6 Atlas Copco AB

- 6.4.7 Ingersoll Rand Inc.

- 6.4.8 Snap-on Incorporated

- 6.4.9 Apex Tool Group

- 6.4.10 Emerson Electric Co.

- 6.4.11 Husqvarna AB

- 6.4.12 Honeywell International Inc.

- 6.4.13 KYOCERA Corporation

- 6.4.14 Festool GmbH

- 6.4.15 Cummins Inc. (Tool segment)

- 6.4.16 Hitachi Koki (HiKOKI)

- 6.4.17 Illinois Tool Works (ITW)

- 6.4.18 Ridgid (Emerson)

- 6.4.19 Baier Power Tools

- 6.4.20 Positec Tool Corporation

- 6.4.21 Panasonic Life Solutions

- 6.4.22 CEMBRE S.p.A.

- 6.4.23 CSUN Power Tools*

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment