|

시장보고서

상품코드

1907224

매니지드 서비스 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Managed Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

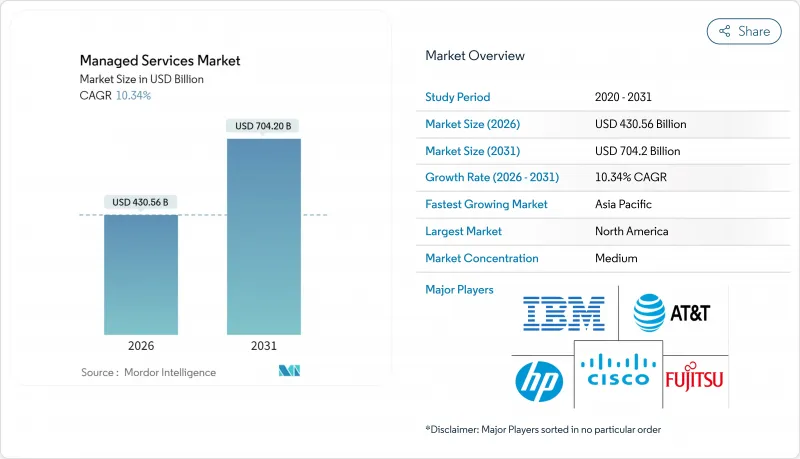

2026년 매니지드 서비스 시장 규모는 4,305억 6,000만 달러로 추정되며, 2025년 3,902억 1,000만 달러에서 성장했으며, 2031년에는 7,042억 달러에 이를 것으로 예상됩니다.

2026년부터 2031년까지의 연평균 성장률(CAGR)은 10.34%를 나타낼 전망입니다.

이 강력한 성장은 하이브리드 클라우드의 복잡성, 증가하는 사이버 위협, 지속적인 예산 모니터링에 직면하는 기업이 IT 운영을 외부 위탁하는 방향으로 전환하고 있음을 반영합니다. 클라우드 중심의 딜리버리 모델, AI의 광범위한 도입, 규제 압력에 의해 제공업체의 서비스 제공 형태가 재구축되는 한편, 경쟁상의 차별화는 지능적인 자동화와 수직적인 전문지식에 의존하게 되었습니다. 전략적 아웃소싱은 순수한 비용 절감에서 디지털 혁신의 핵심 기둥으로 이동하여 보안 운영 센터, 멀티클라우드 오케스트레이션 도구 및 에지 관리 플랫폼에 대한 공급자 투자를 가속화하고 있습니다. M&A 활동은 규모의 중요성을 보여주며, 공급자는 기술적 격차를 없애고 지리적 범위를 확대하기 위한 비유기적 성장을 추구하고 있습니다.

세계의 매니지드 서비스 시장 동향과 인사이트

하이브리드 클라우드의 복잡화는 매니지드 서비스의 도입을 촉진

하이브리드 클라우드 아키텍처는 On-Premise, 프라이빗 클라우드 및 여러 퍼블릭 클라우드를 결합하여 운영 복잡성이 증가하고 사내 팀이 대응에 어려움을 겪고 있습니다. Microsoft의 EU 데이터 경계와 같은 규제 이니셔티브는 데이터의 로컬 처리를 요구하고 컴플라이언스, 이식성 및 통합된 보안 정책을 보장할 수 있는 공급자로의 마이그레이션을 기업에 촉구합니다. 분산 환경에서 원활한 워크로드 이식성과 실시간 정책 적용은 매니지드 인프라 및 보안 서비스에 대한 장기적인 수요를 확고히 합니다.

비용 최적화 압력으로 아웃소싱 결정 가속화

지속적인 이익률 압박으로 인해 고정 IT 간접비는 매니지드 서비스를 통해 변동비 항목으로 전환되고 있습니다. 액센추어가 미국 공군과 체결한 16억 달러 규모의 'Cloud One' 계약과 같은 대규모 혁신 사례는 기업이 아웃소싱을 단순한 전술적 수단이 아니라 전략적 요소로 파악하고 있음을 보여줍니다. 공급자는 자동화 기술, AI 도구 및 공인 인력 풀을 패키징하여 구매 기업이 선행 투자를 피하면서 신기술에 액세스할 수 있도록 합니다.

데이터 주권 규제가 서비스 제공 모델을 제약

현지처리를 의무화하는 규제에 의해 프로바이더는 각 관할 구역에서 인프라를 중복해 구축하지 않으면 안 되고, 규모의 경제성이 저하되어, 세계의 서비스 제공이 복잡화하고 있습니다. Microsoft의 "EU 데이터 경계"는 여러 지역에 걸친 고객을 수용하기 위해 공급자가 흡수해야 하는 추가 자본 비용과 운영 오버헤드를 보여줍니다.

부문 분석

2025년 시점에서 클라우드 도입은 매니지드 서비스 시장의 52.35%를 차지했고 하이브리드 클라우드가 2031년까지 연평균 복합 성장률(CAGR) 11.92%를 유지하는 가운데 그 리드를 확대하고 있습니다. 온디맨드에서 리소스를 시작하고 데이터 규제를 준수하며 에지 워크로드를 통합할 수 있는 이유가 기업이 On-Premise 모델에서 마이그레이션하는 이유입니다. Accenture의 Cloud One 참여와 같은 하이퍼스케일러와의 제휴는 공동 혁신이 여러 해 동안 대규모 계약을 가능하게 하는 좋은 예입니다.

매니지드 서비스 시장은 클라우드 도입을 통해 공급자가 인프라 공유, 패치 자동화, AI 구동 비용 최적화의 대규모 배포를 실현할 수 있다는 점에서 혜택을 누리고 있습니다. 데이터 민감한 영역에서는 프라이빗 클라우드가 여전히 중요하며, 쉽게 리팩토링할 수 없는 레거시 워크로드를 위해 On-Premise 서비스가 계속됩니다. 멀티클라우드 오케스트레이션과 FinOps 보고서를 습득한 공급업체가 새로운 지출을 얻는 최상의 입장에 있습니다.

2025년 시점에서 매니지드 인프라 서비스는 수익의 38.40%를 차지했고 이종 환경의 운용 유지라는 기반적 요구를 반영했습니다. 그러나 성장을 견인하는 것은 매니지드 보안 서비스로 11.72%의 연평균 복합 성장률(CAGR)을 나타내며 랜섬웨어와 컴플라이언스 위반 벌금에 대한 경영진 수준의 우려를 반영하고 있습니다. AI를 활용한 위협 사냥, 제로 트러스트 도입, 자동화된 인시던트 봉쇄가 시장의 승자를 결정합니다.

시큐리티 제공 분야의 매니지드 서비스 시장 규모는 사이버 보험 회사가 인수 기준을 엄격화함에 따라 가속될 것으로 예측됩니다. 공급업체는 SOC-as-a-Service를 컴플라이언스 보고 및 테이블 탑 연습과 결합하여 높은 이익률의 지속적인 수익을 창출합니다. 네트워크 및 통신 서비스는 5G 배포의 혜택을 누리며 데이터센터를 위한 에너지 관리 제품은 지속가능성 요구 사항을 추진하고 있습니다.

매니지드 서비스 시장은 도입 형태(On-Premise, 클라우드), 서비스 유형(매니지드 데이터센터, 매니지드 보안, 매니지드 통신 등), 기업 규모(중소기업, 대기업), 최종 사용자 업종(은행, 금융서비스 및 보험(BFSI), IT 및 통신, 제조 등), 지역별로 세분화됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

지역별 분석

북미는 2025년 32.40%의 수익 점유율을 유지했습니다. 이것은 조기 클라우드 마이그레이션, 사이버 규제, 높은 IT 지출에 의해 지원됩니다. 미국 공군 클라우드 원과 같은 연방 프로그램은 대규모 관리 서비스 계약의 가시성을 높이고 있습니다. BFSI(은행 및 금융 및 보험) 및 의료 분야의 고객이 계속 수요를 지지해, 프로바이더는 이 지역을 AI 및 엣지 파일럿의 전개 거점으로서 활용하고 있습니다.

아시아태평양은 2031년까지 연평균 복합 성장률(CAGR) 11.28%로 가장 빠르게 성장하는 지역입니다. 중국의 제조업 고도화, 인도의 디지털 공공 인프라 추진, 일본의 노후화 플랜트 근대화가 레거시와 클라우드 워크로드를 교차할 수 있는 프로바이더에의 지출을 촉진하고 있습니다. 하이퍼스케일러는 주권 클라우드 요구사항을 충족시키기 위해 현지 MSP와 협력하여 ASEAN 정부는 판매 사이클을 단축하는 클라우드 우선 정책을 채택하고 있습니다.

유럽에서는 GDPR(EU 개인정보보호규정)(일반 데이터 보호 규칙), 디지털 업무 탄력성 법 및 지속가능성 규제가 컴플라이언스의 복잡성을 높이는 동안 꾸준한 확대를 볼 수 있습니다. 독일은 인더스트리 4.0의 매니지드 서비스를 추진하고 영국은 브렉짓 후 금융규제에서 MSP에 의존하고 프랑스는 소블린 클라우드의 틀을 중시하고 있습니다. 공급자는 환경 목표 달성을 위해 지역에 근거한 데이터센터와 녹색 에너지 조달을 통해 차별화를 도모하고 있습니다. 중동 및 아프리카는 여전히 개발 도상이지만, 스마트 시티와 전자 정부 프로젝트로 빠르게 성장하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 지원(3개월간)

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 하이브리드 클라우드 운영 모델로의 전환

- 기업 IT 예산의 비용 최적화 압력

- 사이버 위협 증가와 컴플라이언스 요건 강화

- 엣지 컴퓨팅의 전개에는 원격 관리 서비스가 요구

- 24시간 365일 체제의 매니지드 검지·대응 서비스에 있어서 사이버 보험의 필요조건

- 지속가능성과 그린IT규제가 추진하는 매니지드 전력·냉각서비스

- 시장 성장 억제요인

- 지속적인 데이터 주권과 프라이버시 규제

- 다중 벤더 통합과 레거시 상호 운용성의 과제

- 벤더 록인의 위험과 장기 MSP 계약에 따른 높은 해지 비용

- MSP내의 인재 부족이 서비스 품질의 확장성을 제한

- 공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 시장의 거시 경제적 요인의 평가

제5장 시장 규모와 성장 예측

- 배포별

- On-Premise

- 클라우드

- 퍼블릭 클라우드

- 프라이빗 클라우드

- 하이브리드 클라우드

- 서비스 유형별

- 매니지드 데이터센터

- 매니지드 보안

- 매니지드 통신

- 매니지드 네트워크

- 매니지드 인프라

- 매니지드 모빌리티

- 기타

- 기업 규모별

- 중소기업

- 대기업

- 최종 사용자별 업계

- BFSI

- IT 및 통신

- 헬스케어 및 생명과학

- 제조업

- 소매업 및 전자상거래

- 정부 및 공공 부문

- 에너지 및 유틸리티

- 미디어 및 엔터테인먼트

- 기타(교육기관, 비영리단체)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 동남아시아

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 이집트

- 기타 아프리카

- 중동

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- IBM Corporation

- Cisco Systems Inc.

- Fujitsu Ltd

- ATandT Inc.

- Hewlett Packard Enterprise(HPE)

- Microsoft Corporation

- Verizon Communications Inc.

- Dell Technologies Inc.

- Nokia Corporation

- Deutsche Telekom AG(T-Systems)

- Rackspace Technology Inc.

- Tata Consultancy Services Ltd

- Wipro Ltd

- Accenture plc

- Capgemini SE

- HCL Technologies Ltd

- Cognizant Technology Solutions

- NTT Data Corp.

- DXC Technology Co.

- Lumen Technologies Inc.

- Orange Business Services

제7장 시장 기회와 향후 전망

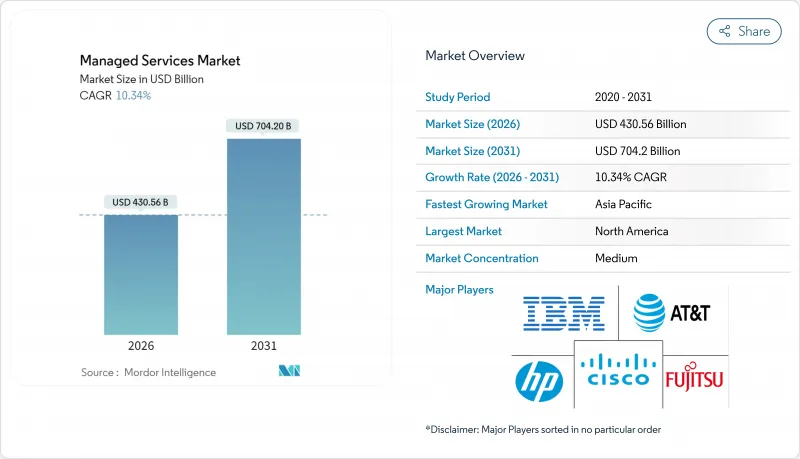

KTH 26.01.20Managed services market size in 2026 is estimated at USD 430.56 billion, growing from 2025 value of USD 390.21 billion with 2031 projections showing USD 704.2 billion, growing at 10.34% CAGR over 2026-2031.

The strong growth reflects enterprises' pivot toward outsourced IT operations as they juggle hybrid-cloud complexity, rising cyber threats, and ongoing budget scrutiny. Cloud-centric delivery models, wider AI adoption, and regulatory pressures are reshaping provider offerings, while competitive differentiation now hinges on intelligent automation and vertical expertise. Strategic outsourcing has shifted from pure cost reduction to a core pillar of digital transformation, accelerating provider investments in security operations centers, multi-cloud orchestration tools, and edge management platforms. M&A activity underscores the appeal of scale, with providers pursuing inorganic growth to fill technology gaps and expand geographic reach.

Global Managed Services Market Trends and Insights

Hybrid-cloud complexity drives managed services adoption

Hybrid-cloud architectures combine on-premises, private, and multiple public clouds, elevating operational complexity that internal teams struggle to master. Regulatory initiatives such as the Microsoft EU Data Boundary require localized data handling, pushing enterprises toward providers that can guarantee compliance, portability, and unified security policies.Seamless workload portability and real-time policy enforcement across distributed environments cement long-term demand for managed infrastructure and security offerings.

Cost optimization pressures accelerate outsourcing decisions

Persistent margin pressure turns fixed IT overhead into a variable line item through managed services. Large transformation deals such as Accenture's USD 1.6 billion Cloud One contract with the U.S. Air Force illustrate how enterprises view outsourcing as strategic, not merely tactical. Providers bundle automation, AI tooling, and certified talent pools, allowing buyers to avoid up-front capital outlays while still accessing emerging capabilities.

Data-sovereignty regulations constrain service delivery models

Mandates requiring localized processing force providers to duplicate infrastructure in each jurisdiction, reducing economies of scale and complicating global delivery. Microsoft's EU Data Boundary illustrates the additional capital and operational overhead that providers must absorb to serve multi-region clients.

Other drivers and restraints analyzed in the detailed report include:

- Cybersecurity threat evolution demands specialized response capabilities

- Edge computing expansion creates remote management requirements

- Vendor lock-in concerns limit long-term commitments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud deployment held 52.35% share of the managed services market in 2025 and is widening its lead as hybrid cloud posts a 11.92% CAGR through 2031. The ability to spin up resources on demand, comply with data regulations, and integrate edge workloads explains why enterprises migrate from on-premises models. Hyperscaler alliances, like Accenture's engagement on Cloud One, show how co-innovation can unlock large multiyear deals.

The managed services market benefits as cloud deployment allows providers to pool infrastructure, automate patches, and roll out AI-driven cost-optimization at scale. Private cloud remains relevant for data-sensitive sectors, while on-premises services persist for legacy workloads that cannot be refactored easily. Providers that master multi-cloud orchestration and FinOps reporting are best positioned to capture new spend.

Managed infrastructure services owned 38.40% revenue in 2025, reflecting the baseline need to keep heterogeneous estates running. Yet managed security services lead growth with an 11.72% CAGR, mirroring board-level concern over ransomware and compliance fines. AI-enabled threat hunting, zero-trust rollouts, and automated incident containment set market winners apart.

The managed services market size for security offerings is expected to accelerate as cyber-insurance carriers tighten underwriting criteria. Providers are bundling SOC-as-a-service with compliance reporting and tabletop exercises, creating high-margin recurring revenue. Network and communication services gain from 5G roll-outs, while data-center energy management products ride sustainability mandates.

Managed Services Market is Segmented by Deployment (On-Premises, Cloud), Service Type (Managed Data Center, Managed Security, Managed Communications, and More), Enterprise Size (Small and Medium Enterprises, Large Enterprises), End-User Vertical (BFSI, IT and Telecommunication, Manufacturing, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 32.40% revenue share in 2025, buoyed by early cloud migration, cyber regulations, and high IT spend. Federal programs such as the U.S. Air Force Cloud One create visibility for large managed services contracts. BFSI and healthcare customers continue to anchor demand, and providers use the region as a launchpad for AI and edge pilots.

Asia-Pacific is the fastest-growing region at 11.28% CAGR to 2031. China's manufacturing upgrades, India's digital-public-infrastructure push, and Japan's aging plant modernization funnel spend toward providers capable of bridging legacy and cloud workloads. Hyperscalers team with local MSPs to address sovereign-cloud requirements, while ASEAN governments adopt cloud-first mandates that shorten sales cycles.

Europe shows steady expansion as GDPR, Digital Operational Resilience Act, and sustainability rules heighten compliance complexity. Germany drives Industry 4.0 managed services, the United Kingdom leans on MSPs for post-Brexit financial regulation, and France emphasizes sovereign-cloud frameworks. Providers differentiate through localized data centers and green-energy sourcing to meet environmental targets. The Middle East and Africa remain nascent but grow quickly on smart-city and e-government projects.

- IBM Corporation

- Cisco Systems Inc.

- Fujitsu Ltd

- ATandT Inc.

- Hewlett Packard Enterprise (HPE)

- Microsoft Corporation

- Verizon Communications Inc.

- Dell Technologies Inc.

- Nokia Corporation

- Deutsche Telekom AG (T-Systems)

- Rackspace Technology Inc.

- Tata Consultancy Services Ltd

- Wipro Ltd

- Accenture plc

- Capgemini SE

- HCL Technologies Ltd

- Cognizant Technology Solutions

- NTT Data Corp.

- DXC Technology Co.

- Lumen Technologies Inc.

- Orange Business Services

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift to hybrid-cloud operating models

- 4.2.2 Cost-optimization pressure on enterprise IT budgets

- 4.2.3 Rising cyber-threat volume and compliance mandates

- 4.2.4 Edge-computing roll-outs demanding remote managed services

- 4.2.5 Cyber-insurance prerequisites for 24/7 managed detection and response

- 4.2.6 Sustainability and green-IT regulations driving managed power/cooling

- 4.3 Market Restraints

- 4.3.1 Persistent data-sovereignty and privacy regulations

- 4.3.2 Multi-vendor integration and legacy interoperability challenges

- 4.3.3 Vendor lock-in risk and high exit costs of long-term MSP contracts

- 4.3.4 Talent shortages within MSPs limiting service-quality scalability

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Assesment of Macroeconomic Factors on the market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment

- 5.1.1 On-premise

- 5.1.2 Cloud

- 5.1.2.1 Public Cloud

- 5.1.2.2 Private Cloud

- 5.1.2.3 Hybrid Cloud

- 5.2 By Service Type

- 5.2.1 Managed Data Center

- 5.2.2 Managed Security

- 5.2.3 Managed Communications

- 5.2.4 Managed Network

- 5.2.5 Managed Infrastructure

- 5.2.6 Managed Mobility

- 5.2.7 Others

- 5.3 By Enterprise Size

- 5.3.1 Small and Medium Enterprises (SMEs)

- 5.3.2 Large Enterprises

- 5.4 By End-user Vertical

- 5.4.1 BFSI

- 5.4.2 IT and Telecommunication

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Manufacturing

- 5.4.5 Retail and E-commerce

- 5.4.6 Government and Public Sector

- 5.4.7 Energy and Utilities

- 5.4.8 Media and Entertainment

- 5.4.9 Others (Education, Non-Profit)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Southeast Asia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 Cisco Systems Inc.

- 6.4.3 Fujitsu Ltd

- 6.4.4 ATandT Inc.

- 6.4.5 Hewlett Packard Enterprise (HPE)

- 6.4.6 Microsoft Corporation

- 6.4.7 Verizon Communications Inc.

- 6.4.8 Dell Technologies Inc.

- 6.4.9 Nokia Corporation

- 6.4.10 Deutsche Telekom AG (T-Systems)

- 6.4.11 Rackspace Technology Inc.

- 6.4.12 Tata Consultancy Services Ltd

- 6.4.13 Wipro Ltd

- 6.4.14 Accenture plc

- 6.4.15 Capgemini SE

- 6.4.16 HCL Technologies Ltd

- 6.4.17 Cognizant Technology Solutions

- 6.4.18 NTT Data Corp.

- 6.4.19 DXC Technology Co.

- 6.4.20 Lumen Technologies Inc.

- 6.4.21 Orange Business Services

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment