|

시장보고서

상품코드

1911389

필리핀의 시설 관리(FM) 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Philippines Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

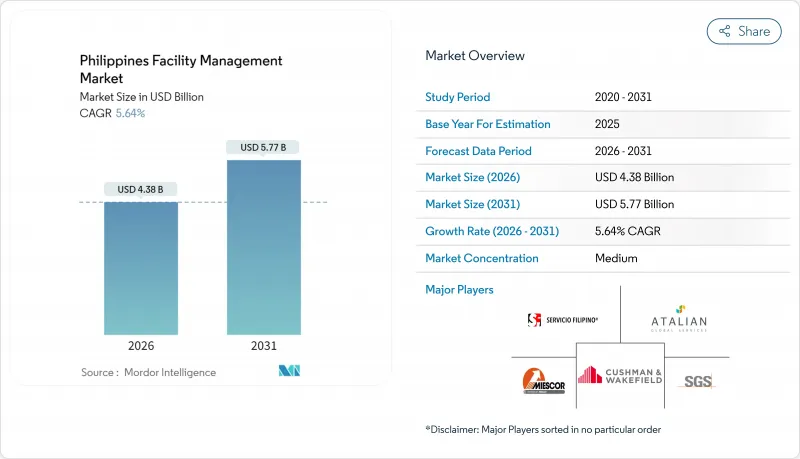

필리핀의 시설 관리(FM) 시장은 2025년의 41억 5,000만 달러에서 2026년에는 43억 8,000만 달러로 성장하고 2026-2031년에 걸쳐 CAGR 5.64%로 성장을 지속하여, 2031년까지 57억 7,000만 달러에 달할 전망입니다.

3,700건 이상의 유틸리티 계획에 대한 자본 지출 증가, 380억 달러 규모의 비즈니스 프로세스 아웃소싱(BPO) 부문로부터의 왕성한 사무실 수요, 2026년부터의 지속가능성 보고 의무화가 함께 필리핀 제도 전역에서 아웃소싱과 기술을 활용한 빌딩 서비스에 대한 지출을 높이고 있습니다. 노후화된 교통망, 에너지 자산, 상업 빌딩에는 지속적인 기계, 전기 및 배관 공사가 필요하기 때문에 하드 서비스가 현재 매출의 대부분을 차지하고 있습니다. 그러나 기업의 위생환경과 생산성의 관련성을 기업이 인식함에 따라 소프트 서비스의 수요도 확대되고 있습니다. 다국적 기업 고객이 하드, 소프트, 디지털 솔루션을 통합한 계약을 요구하는 가운데, 산업 재편의 압력이 높아지고 있습니다. 지역별 수요에도 변화가 나타나고 있으며, 세부, 다바오, 클라크에서는 투자 성장률이 가장 높고, 서비스 제공업체는 현지 서비스 거점의 구축을 요구받고 있습니다.

필리핀의 시설 관리 시장의 동향 및 인사이트

인프라 개발이 수요를 견인

"Build Better More"시책에 의한 유틸리티 부문과 2,190억 페소의 바탄-카비테 교량, 1,875억 페소의 파나이섬, 기마라스섬, 네그로스섬 교량 등이 필리핀의 시설 관리 시장의 규모 확대에 기여하고 있습니다. 2022년 이후에 1,200km의 도로와 같은 수의 교량이 완성됨으로써 교량 데크의 점검, 터널 환기 설비의 유지 관리, 도로를 따르는 자산 관리의 필요성이 더욱 높아지고 있습니다. 60억 페소 규모의 PGH 암 센터와 여러 지역 병원과 같은 의료시설의 건설에 의해 대상이 되는 기반에 전문적인 임상 환경이 더해졌습니다. 따라서 계약자는 지역 도시에서 서비스를 신속하게 동원할 수 있으며 단일 컨세션 내에서 다양한 자산을 관리할 수 있는 공급업체가 필요합니다. 이러한 복합 용도 회랑은 교통, 소매, 주택 요소를 조합하고 있기 때문에 하드, 소프트, 에너지 효율화를 통합한 패키지를 제공하는 서비스 제공업체가 입찰에서 우위성을 획득하고 있습니다.

기술 통합이 서비스 제공을 변화

IoT 지원 플랫폼은 필리핀의 시설 관리 시장 전반에 걸쳐 서비스 범위를 재구성하고 있습니다. 마닐라 도심의 사무실에서 도입이 진행되는 Milesight사의 AI 탑재 재실 감지 센서 등에 의해 예측 보전 스케줄이나 공간 최적화 전략에 활용되는 실시간 이용 데이터가 제공되고 있습니다. PLDT 엔터프라이즈의 스마트 IoT 제품군은 유틸리티 미터와 엘리베이터 제어를 통합 대시보드에 연결하여 대응 시간을 단축하고 에너지 비용을 절감합니다. 과학기술부가 가금류 시설에서 실시한 470만 페소 규모의 ChicIoT 파일럿 사업은 센서 기반 모니터링이 산업 및 농업 비즈니스 시설로도 확대되고 있음을 보여줍니다. 세부, 바콜로드, 일로일로, 다바오의 100개 정부 기관을 대상으로 하는 500만 달러 규모의 스마트 시티 프로그램은 통합 플랫폼이 현재 어느 정도 규모로 조달할 수 있는지를 입증합니다. 시설 관리 시스템 내에 분석 엔진을 통합하여 경보를 정량화할 수 있는 절약 효과로 변환할 수 있는 공급자는 보다 장기적인 계약 기간을 확보하고 있습니다.

노동력 부족이 시장 성장 제약

건설노동자 부족이 약 30만명으로 추정되는 것 외에도 수도권에서의 임금 상승으로 시설기술자와 현장감독자의 급여 기대치가 인상되었습니다. 직업훈련학교 졸업생에 대한 해외 파견 경쟁도 국내 노동력의 추가적인 감소를 초래하고 있습니다. 일로코스 지방과 세부에서는 전기기사와 공조설비 전문가를 확보하기 위해 고용주가 임금 수준의 인상을 개시하고 있으며 이는 고정가격계약으로 운영하는 서비스 계약업체의 이익률을 압박하고 있습니다. 따라서 공급자는 장학금 제도와 기술자의 생산성을 극대화하는 디지털 작업 지시 플랫폼에 대한 투자가 필수적입니다.

부문 분석

2025년 하드 서비스는 필리핀의 시설 관리 시장에서 63.12%의 점유율을 차지하였고 이는 열대 태풍 다발 지역에서의 기계, 전기 및 배관과 방화 설비에 대한 유지 관리의 중요성을 반영하고 있습니다. 교통 회랑의 지속적인 업그레이드와 1990년대 건축 오피스 타워의 개보수에는 24시간 체제의 자산 관리 프로그램이 요구됩니다. 더불어 예측 분석을 통한 다운타임 단축이 진행되고 있습니다. 마닐라 도심의 IoT 대응 냉각 장치는 효율 저하가 발생하기 전에 기술자에게 경고하여 시설당 에너지 소비량을 8-10% 줄이고 있습니다. 소프트 서비스 부문은 2031년까지 연평균 복합 성장률(CAGR) 6.71%의 급성장이 예상됩니다. 이는 입주자가 청소 및 경비 컨시어지 서비스를 종업원 정착율이나 브랜드 평가의 중요한 요소로 파악하는 경향이 강해지고 있기 때문입니다. 팬데믹 후 실내 공기질 모니터링에 관한 정부 규정도 청소 팀의 업무 범위를 확대하고 있습니다.

재실 감지 센서와 방문자 관리 앱을 도입하는 빌딩이 늘어나면서 하드 서비스와 소프트 서비스의 경계가 모호해지고 있습니다. 예를 들어 공간 예약 데이터를 활용하여 청소 팀은 통행량이 많은 지역에 집중할 수 있으며 HVAC 설정도 통행량에 따라 실시간으로 조정됩니다. 이 융합을 통해 공급업체는 두 영역을 통합한 제안 패키지를 제공하고, 이 구성이 필리핀의 시설 관리 시장에서 점유율을 확대할 것으로 예측됩니다.

필리핀의 시설 관리 시장 보고서는 유형별(사내 시설 관리 및 외부 위탁 시설 관리(단일 FM, 패키지 FM, 통합 FM)), 제공 형태별(하드 FM 및 소프트 FM), 최종 사용자 산업별(상업, 기관, 공공 및 인프라, 공업, 기타)로 분류되어 있습니다. 시장 규모와 예측은 위의 모든 부문에 대해 금액(달러)으로 제공됩니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 현재 가동률

- 주요 FM 사업자의 수익률

- 노동력 지표 - 노동참가율

- 서비스 유형별 시설 관리 시장의 점유율(%)

- 하드 서비스별 시설 관리 시장의 점유율(%)

- 소프트 서비스별 시설 관리 시장의 점유율(%)

- 주요 도시권에서의 도시화와 인구 증가

- 필리핀 인프라 정비 계획의 부문별 투자 우선순위

- 노동기준과 안전기준에 특화된 규제요인

- 촉진요인

- 인프라 정비가 수요를 촉진

- 기술 통합에 의한 서비스 제공의 변화

- 지속 가능한 시설 관리를 통한 경쟁 우위 강화

- 아웃소싱 동향 증가

- BPO 부문에서 통합형 FM 계약에 대한 수요 증가

- 정부의 그린빌딩 의무화가 FM 업무 범위 확대를 촉진

- 억제요인

- 노동력 부족이 시장 성장을 제약

- 규제 준수에 의한 업무 복잡성의 증대

- 가격 경쟁을 초래하는 높은 비용 감응도

- 분산된 공급 기반에 의한 서비스 표준화 부족

- 밸류체인 분석

- PESTEL 분석

- 신규 참가자를 위한 규제 및 법적 틀

- 거시경제지표가 FM 수요에 미치는 영향

- Porter's Five Forces 분석

- 공급자의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 투자 및 자금 조달 분석

제5장 시장 규모 및 성장 예측

- 서비스 유형별

- 하드 서비스

- 자산 관리

- MEP 및 HVAC 서비스

- 소방 설비 및 안전 대책

- 기타 하드 FM 서비스

- 소프트 서비스

- 사무실 지원 및 보안

- 청소 서비스

- 케이터링 서비스

- 기타 소프트 FM 서비스

- 하드 서비스

- 제공 형태별

- 자사 관리

- 외부 위탁

- 단일 FM

- 패키지 FM

- 통합 FM

- 최종 사용자 산업별

- 상업시설(IT 및 통신, 소매 및 창고, 기타)

- 호스피탈리티(호텔, 음식점, 대규모 레스토랑)

- 공공 및 공공 인프라(정부 기관, 교육 기관, 수송)

- 의료(공공 및 민간 시설)

- 산업 공정(제조업, 에너지, 광업)

- 기타 최종 사용자 산업(공동주택, 엔터테인먼트, 스포츠 레저)

제6장 경쟁 구도

- 시장 집중도

- 전략적 전개 및 파트너십

- 시장 점유율 분석

- 기업 프로파일

- CBRE Philippines

- Servicio Filipino Inc.

- Meralco Industrial Engineering Services Corporation

- SGS Philippines Inc.

- Santos Knight Frank Inc.(Knight Frank LLP)

- Century Properties Management Inc.

- Mansion Maintenance Co. Inc.

- Kontrac Facilities Management Services Inc.

- Jones Lang LaSalle Inc.

- Artelia Group

- WeCare Facility Management Services Inc.

- Hydron Corporation

- Atalian Global Services Philippines Inc.

- Kabraso

- CPMGI

- Cushman & Wakefield Debenham Tie Leung Limited

제7장 시장 기회 및 미래 전망

CSM 26.02.04The Philippines facility management market is expected to grow from USD 4.15 billion in 2025 to USD 4.38 billion in 2026 and is forecast to reach USD 5.77 billion by 2031 at 5.64% CAGR over 2026-2031.

Rising capital expenditure on more than 3,700 public-works schemes, buoyant office demand from the USD 38 billion business-process-outsourcing (BPO) sector and mandatory sustainability reporting from 2026 are combining to lift spending on outsourced and technology-enabled building services across the archipelago. Hard services dominate present revenue because ageing transport links, energy assets and commercial towers require continuous mechanical, electrical and plumbing work, yet soft services are gaining traction as employers link workplace hygiene with productivity. Consolidation pressures are intensifying as multinational customers ask for integrated contracts that blend hard, soft and digital solutions. Regional demand is shifting: Cebu, Davao and Clark are registering the fastest investment growth and forcing service providers to build local delivery hubs.

Philippines Facility Management Market Trends and Insights

Infrastructure development fueling demand

Public works under the Build Better More portfolio, including the PHP 219 billion Bataan-Cavite Interlink Bridge and PHP 187.5 billion Panay-Guimaras-Negros crossings, are broadening the footprint of the Philippines facility management market. Completion of 1,200 km of roads and an equal number of bridges since 2022 has intensified the need for bridge-deck inspections, tunnel ventilation upkeep and roadside asset management. Healthcare builds such as the PHP 6 billion PGH Cancer Center and several regional hospitals add specialist clinical environments to the addressable base. Contractors therefore require suppliers able to mobilise quickly in provincial locations and manage multiform assets within single concessions. As these mixed-use corridors combine transport, retail and residential elements, service providers that offer integrated hard, soft and energy-efficiency packages are gaining bid advantages.

Technology integration transforming service delivery

IoT-enabled platforms are reshaping service scopes throughout the Philippines facility management market. Deployments of AI-powered occupancy sensors, such as Milesight's roll-out in Metro Manila offices, are providing live utilisation data that feeds predictive maintenance schedules and space optimisation strategies. PLDT Enterprise's Smart IoT suite is linking utilities meters and lift controls to unified dashboards, cutting response times and lowering energy bills. The Department of Science and Technology's PHP 4.7 million ChicIoT pilot in poultry facilities shows that sensor-based monitoring is also moving into industrial and agri-business estates. A USD 5 million smart-city programme across 100 government units in Cebu, Bacolod, Iloilo and Davao is demonstrating the scale at which integrated platforms can now be procured. Providers that can embed analytics engines within building-management systems and translate alerts into quantifiable savings are securing longer contract tenures.

Labor shortages constraining market growth

An estimated deficit of 300,000 construction workers, coupled with wage hikes in the National Capital Region, is pushing up salary expectations for facility technicians and site supervisors. Competition from overseas placements for Technical and Vocational Education Training graduates is further thinning the local labour pool. Employers in Ilocos and Cebu have started raising pay scales to secure electricians and HVAC specialists, eroding margins for service contractors that operate fixed-price agreements. Providers must therefore invest in scholarship schemes and digital work-order platforms that maximise technician productivity.

Other drivers and restraints analyzed in the detailed report include:

- Sustainable facility management bolstering competitive advantage

- Outsourcing trend gaining momentum

- Regulatory compliance increasing operational complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hard services accounted for 63.12% of the Philippines facility management market share in 2025, reflecting the criticality of mechanical, electrical, plumbing and fire-safety upkeep in a tropical, typhoon-prone environment. Ongoing rehabilitation of transport corridors and the refurbishing of 1990s-era office towers require round-the-clock asset management programmes. In parallel, predictive analytics is reducing downtime: IoT-enabled chillers in Metro Manila now alert engineers before efficiency drifts occur, lowering energy draw by 8-10% per site. Soft services are on a faster 6.71% CAGR route to 2031 because occupants increasingly view cleaning, security and concierge support as levers for employee retention and brand reputation. Government mandates on indoor-air-quality monitoring post-pandemic are also broadening the duty scope of janitorial teams.

As more buildings embed occupancy sensors and visitor-management apps, distinctions between hard and soft services are blurring. For example, space-booking data enables housekeeping crews to focus on high-traffic zones, while HVAC set-points are adjusted in real time based on footfall. This convergence is prompting suppliers to package both domains into single integrated proposals, a configuration expected to command a rising share of the Philippines facility management market.

The Philippine Facility Management Market Report is Segmented by Type (In-House Facility Management and Outsourced Facility Management (single FM, Bundled FM, and Integrated FM)), Offering Type (Hard FM and Soft FM), and End-User Industry (Commercial, Institutional, Public/Infrastructure, Industrial, and More). The Market Size and Forecasts are Provided in Terms of Value in (USD) for all the Above Segments.

List of Companies Covered in this Report:

- CBRE Philippines

- Servicio Filipino Inc.

- Meralco Industrial Engineering Services Corporation

- SGS Philippines Inc.

- Santos Knight Frank Inc. (Knight Frank LLP)

- Century Properties Management Inc.

- Mansion Maintenance Co. Inc.

- Kontrac Facilities Management Services Inc.

- Jones Lang LaSalle Inc.

- Artelia Group

- WeCare Facility Management Services Inc.

- Hydron Corporation

- Atalian Global Services Philippines Inc.

- Kabraso

- CPMGI

- Cushman & Wakefield Debenham Tie Leung Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.1.1 Current Occupancy Rates

- 4.1.2 Profitability Rates of Major FM Players

- 4.1.3 Workforce Indicators - Labor Participation

- 4.1.4 Facility Management Market Share (%), by Service Type

- 4.1.5 Facility Management Market Share (%), by Hard Services

- 4.1.6 Facility Management Market Share (%), by Soft Services

- 4.1.7 Urbanization and Population Growth in Major Metros

- 4.1.8 Sector Investment Priorities in Philippines's Infrastructure Pipeline

- 4.1.9 Regulatory Drivers Specific to Labour and Safety Standards

- 4.2 Market Drivers

- 4.2.1 Infrastructure Development Fueling Demand

- 4.2.2 Technology Integration Transforming Service Delivery

- 4.2.3 Sustainable Facility Management Bolstering Competitive Advantage

- 4.2.4 Outsourcing Trend Gaining Momentum

- 4.2.5 Rising Demand for Integrated FM Contracts in BPO Sector

- 4.2.6 Government Green Building Mandates Driving FM Scope Expansion

- 4.3 Market Restraints

- 4.3.1 Labor Shortages Constraining Market Growth

- 4.3.2 Regulatory Compliance Increasing Operational Complexity

- 4.3.3 High Cost Sensitivity Leading to Price-based Competition

- 4.3.4 Fragmented Supplier Base Diluting Service Standardization

- 4.4 Value Chain Analysis

- 4.5 PESTEL Analysis

- 4.6 Regulatory and Legislative Framework for Market Entrants

- 4.7 Impact of Macroeconomic Indicators on FM Demand

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Services

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Investment and Funding Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Hard Services

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard FM Services

- 5.1.2 Soft Services

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Soft FM Services

- 5.1.1 Hard Services

- 5.2 By Offering Type

- 5.2.1 In-house

- 5.2.2 Outsourced

- 5.2.2.1 Single FM

- 5.2.2.2 Bundled FM

- 5.2.2.3 Integrated FM

- 5.3 By End-user Industry

- 5.3.1 Commercial (IT and Telecom, Retail and Warehouses, etc.)

- 5.3.2 Hospitality (Hotels, Eateries, Large-scale Restaurants)

- 5.3.3 Institutional and Public Infrastructure (Govt, Education, Transportation)

- 5.3.4 Healthcare (Public and Private Facilities)

- 5.3.5 Industrial and Process (Manufacturing, Energy, Mining)

- 5.3.6 Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Partnerships

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 CBRE Philippines

- 6.4.2 Servicio Filipino Inc.

- 6.4.3 Meralco Industrial Engineering Services Corporation

- 6.4.4 SGS Philippines Inc.

- 6.4.5 Santos Knight Frank Inc. (Knight Frank LLP)

- 6.4.6 Century Properties Management Inc.

- 6.4.7 Mansion Maintenance Co. Inc.

- 6.4.8 Kontrac Facilities Management Services Inc.

- 6.4.9 Jones Lang LaSalle Inc.

- 6.4.10 Artelia Group

- 6.4.11 WeCare Facility Management Services Inc.

- 6.4.12 Hydron Corporation

- 6.4.13 Atalian Global Services Philippines Inc.

- 6.4.14 Kabraso

- 6.4.15 CPMGI

- 6.4.16 Cushman & Wakefield Debenham Tie Leung Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Technology-led Integrated FM (IoT, BMS, AI-based Predictive Maintenance)

- 7.3 ESG-compliant FM Solutions Demand

- 7.4 Future Service-Model Shifts (Outcome-based Contracts)