|

시장보고서

상품코드

1911811

유럽의 텀블 건조기 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Europe Tumble Dryers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

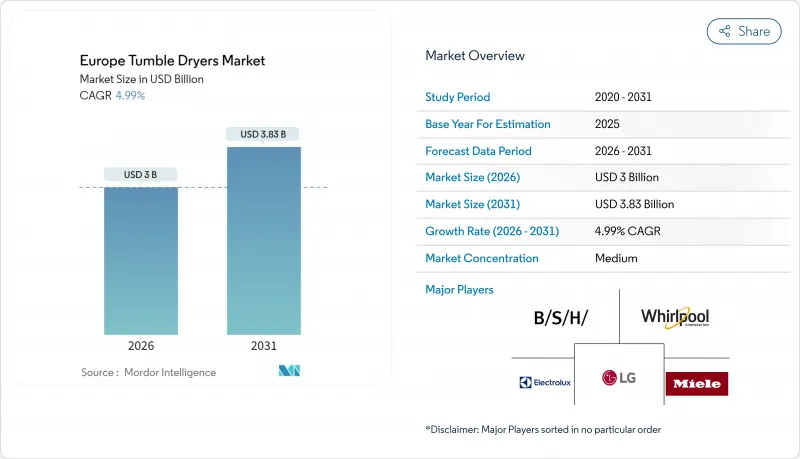

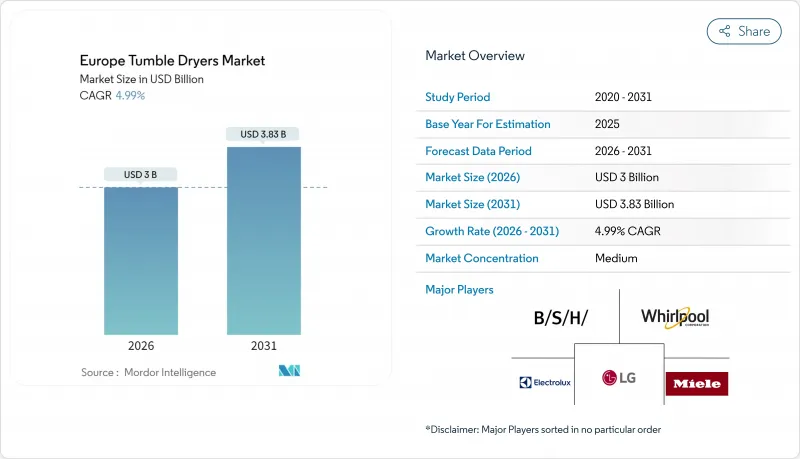

유럽의 텀블 건조기 시장은 2025년에 28억 6,000만 달러로 평가되었고, 2026년 30억 달러에서 2031년까지 38억 3,000만 달러에 이를 것으로 예측됩니다.

예측 기간(2026-2031년) CAGR은 4.99%로 성장이 전망됩니다.

절대적인 규모에서 유럽의 텀블 건조기 시장은 성숙한 교체 주도의 가전 카테고리에서 유럽 연합(EU)의 에코디자인 지침(2025년 7월부터 배기식 및 엔트리 레벨의 커패시터 유닛 금지)에 의한 기술 주도의 업그레이드 사이클로 이행하고 있습니다. 히트펌프 기술 혁신, 가정용 에너지 비용 상승, 그리고 팬데믹 이후의 지속가능성에 대한 주목과 맞물려, 거시경제의 변동이 계속되는 가운데도 건전한 수요의 기세를 지지하고 있습니다. 경쟁 전략은 현재 규제 준수, 프리미엄 포지셔닝, 신속한 제품 라인 쇄신에 초점을 맞추었습니다. 한편, 지역 격차는 현저하고, 독일이 보급률로 선두를 유지하는 한편, 스페인이 가장 급속한 증가율을 나타내고 있습니다. 동유럽 및 남유럽의 일부 지역에서의 높은 가격 감응도가 히트 펌프의 즉각 보급을 억제하는 반면, 지원적인 금융 방식 및 사회 주택용 일괄 조달 프로그램이 대상 고객층을 확대하고 있습니다. 동시에, 옴니채널 유통, 특히 온라인 마켓플레이스를 통한 판매는 고객 획득의 경제성을 재구성하고 소비자 직접 판매 능력을 가진 브랜드를 유리하게 만듭니다. R290 냉매와 관련된 공급망 마찰과 지속적인 방화 안전성 모니터링은 시장 운영 위험을 돋보이게 하지만, IoT 대응 모델과 유틸리티 사업자 수요 반응 파일럿 사업은 예측 기간 동안 성숙한 인접 수익원을 나타냅니다.

유럽의 텀블 건조기 시장 동향 및 인사이트

EU의 에너지 절약 규제가 히트 펌프 보급 가속

2025년 7월 시행의 에코디자인 규제로 제조업체는 유럽용 제품 라인에서 비히트펌프 기술을 제거할 수밖에 없으며, 유럽의 텀블 건조기 시장은 한꺼번에 단일 기술 경쟁으로 변모합니다. 이 규제만으로 2040년까지 15테라와트시(TWh)의 전력과 170만 톤(Mt)의 이산화탄소 환산량(CO2-eq)을 삭감해 소비자의 누적 절약액은 28억 달러에 달할 것으로 예측되고 있습니다. A 등급 평가는 현재 히트펌프 모델에만 적용되며, 배기식 또는 기본형 커패시터식 건조기는 실질적으로 적합하지 않은 상태로 추격되고 있습니다. 밀레 등의 프리미엄 브랜드는 조기에 대응해, 인피니티 케어 드럼과 울 전용 사이클을 탑재한 T2 노바 에디션을 발표했습니다. 에너지 효율을 넘은 섬유 보호 효과를 어필했습니다. BSH는 생산 체제를 히트 펌프식으로 재조정함으로써 이행기를 활용하여 규제 대응을 유지하면서 이익률을 유지하고 있습니다. 이 규제는 동시에 2단계 가격 체계를 도입하고, 프리미엄 제조업체는 가치를 유지할 수 있는 한편, 저가격 지향 기업은 엄격한 이익률 압력에 직면하고 있습니다. ISO 14001 지속가능성 인증을 기반으로 하는 적합성 감사가 조달의 전제조건이 되고 있으며, 대응이 지연된 기업의 경쟁 장벽이 더욱 높아지고 있습니다.

서유럽의 가처분 소득 증가 및 교체주기

거시환경 개선 및 억제된 인플레이션으로 자유재량 지출이 재활성화되고 있습니다. EU의 내구 소비재 판매는 2023년 2.90% 감소에서 2025년 2.80% 증가로 전환할 전망입니다. 평균 교환주기는 8-10년이며, 전기요금 상승으로 가구는 구매가격보다 라이프사이클 비용을 우선하게 되었습니다. 이로 인해 초기 비용이 2-3배 높음에도 불구하고 히트 펌프 솔루션이 선택되는 경향이 있습니다. 독일과 네덜란드에서는 캐쉬백 제도에 의한 보급 촉진이 진행되는 한편, 남유럽 시장에서는 가격 감응도가 높은 경향이 계속되고 있습니다. 유럽의 가전시장은 2027년까지 384억 8,000만 달러에서 424억 달러로 성장이 예상되고, 소비자가 에너지 절약성과 편리성을 요구하는 가운데 스마트 가전은 26%의 성장률을 기록할 전망입니다. 조사 데이터에 따르면 영국 응답자의 80%가 광열비를 우려하고 효율적인 건조기에 대한 투자 의욕의 높이로 이어지고 있습니다. 확립된 브랜드는 로열티의 이점을 활용하고 있으며, 세계 소비자의 35%가 브랜드 명성을 결정적인 요인으로 꼽고 있습니다. 전반적으로 소득 증가 및 교체 긴급성이 결합되어 유럽 텀블 건조기 시장의 CAGR에 1.2퍼센트 포인트의 바람을 불어넣었습니다.

히트펌프 모델의 초기 가격 프리미엄 높이

히트펌프식 건조기의 소매 가격은 1,000유로(1,090달러) 이상이 되는 경우가 많고, 배기식 모델의 300-400유로(327-436달러)와 비교해, 구입의 장벽이 높아지고 있습니다. 평생 에너지 절약은 500달러를 초과할 수 있지만 투자 회수 기간은 동유럽의 저소득 가구 채용을 방해하고 있습니다. 대출제도 및 정부의 보조금 제도가 일부를 보전하고 있지만, 규모의 경제에 의한 단가 저하까지는 보급이 진행되지 않습니다. 삼성과 LG는 AI 최적화 기능을 탑재한 엔트리 모델을 800유로(872달러) 미만으로 시판하고 있으며, 시장 전망을 쇄신할 가능성이 있습니다. 유럽의 기존 제조업체는 이익률을 지키거나 평균 판매 가격(ASP)을 희생하여 전환을 가속화할지 여부를 선택해야 하며, 두 가지 방법 모두 브랜드 가치와 설치 기반 경제성에 영향을 미칩니다. 단기적으로 가격 장벽은 유럽 건조기 시장의 CAGR을 약 1.4포인트 내리고 있습니다.

부문 분석

히트펌프식 모델은 2025년 시점에서 유럽 건조기 시장 규모의 35.44%를 차지하고, 2025년 중반에 시행되는 배기식 및 기본 커패시터 유닛의 규제 금지를 배경으로 13.10%의 연평균 복합 성장률(CAGR)로 확대 중입니다. 과거 주류였던 커패시터식 건조기는 2025년에 있어서도 유럽 시장 점유율의 50.92%를 차지했지만, 피할 수 없는 종말을 맞이하고 있으며, 수요는 규제 대응형 대체품으로 이행하고 있습니다. 프리미엄 포지셔닝은 70% 낮은 에너지 소비량과 의류 보호의 우위성에 의존하고 있어, 제조업체는 엔트리 레벨 SKU가 등장하는 가운데서도 가격을 유지하는 것이 가능해지고 있습니다. 삼성의 'Bespoke AI 세탁 콤보'는 대용량 설계와 머신러닝을 기반으로 사이클 최적화의 융합을 구현합니다. LG는 소비 전력을 570W로 줄인 완전 히트 펌프식 'Signature' 스택으로 대항하여 다양한 기술적 접근법을 보여줍니다. 예측 기간 동안 제품 차별화는 기계적 성능뿐만 아니라 연결성, 환경 인증, 애프터 서비스에 점점 의존하고 있습니다.

유럽의 텀블 건조기 시장에서는 영국에서 단독 주택의 외부 배기가 용이하기 때문에 역사적으로 인기가 있었던 배기식 설계의 단계적인 쇠퇴도 볼 수 있습니다. 집주인에 의한 개수나 건축 기준법의 변경에 의해 설치 형태는 밀폐 사이클식 커패시터 또는 히트 펌프 유닛으로 이행하고 있습니다. 제조업체는 이에 대응하고 BSH는 생산 라인을 고 이익률의 히트 펌프 제품군에 재배치하고 있습니다. 부품 공급자는 저항 히터의 단계적 폐지 및 R290 압축기의 생산 확대로 대응하고 있습니다. 규제 비 적합 재고의 절벽 상황을 겪고 소매 업체는 할인으로 인한 재고 처분을 진행하고 있으며 평균 판매 가격이 일시적으로 왜곡되었습니다. 그러나 2025년 이후 유럽 건조기 시장은 전 기종 히트펌프화로 전환하고 마진 보호를 위한 서비스 계약을 세트 판매함으로써 카테고리 수익은 회복될 전망입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- EU의 에너지 효율 규제가 히트 펌프 보급 가속

- 서유럽의 가처분 소득 증가 및 교체 사이클

- MDA 구입에 있어서 전자상거래 채널 성장

- 히트펌프식 건조기를 지정하는 사회 주택 개수 프로그램

- 호스피탈리티 업계의 ESG 목표가 고효율 설비로의 갱신 촉진

- 유틸리티 수요 반응 파일럿용 IoT 대응 건조기

- 시장 성장 억제요인

- 히트펌프 모델에 대한 고액의 초기 비용

- EU 주요 5개국에 있어서의 주택 부문 시장 포화 상태

- 화재 안전에 관한 리콜 사례가 소비자 신뢰 저하 초래

- R290 냉매 공급망에서의 변동성

- 밸류체인 및 공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 공급기업의 협상력

- 구매자의 협상력

- 대체품의 위협

- 경쟁의 격렬함

제5장 시장 규모 및 성장 예측

- 제품 유형별

- 히트 펌프식 텀블 건조기

- 커패시터식 텀블 건조기

- 배기식 텀블 건조기

- 최종 사용자별

- 주택

- 상업

- 유통 채널별

- 오프라인

- 온라인

- 국가별

- 영국

- 독일

- 프랑스

- 스페인

- 이탈리아

- 베네룩스

- 벨기에

- 네덜란드

- 룩셈부르크

- 북유럽 국가

- 덴마크

- 핀란드

- 아이슬란드

- 노르웨이

- 스웨덴

- 기타 유럽

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- BSH Hausgerate GmbH(Bosch/Siemens)

- Whirlpool Corp.

- Electrolux AB

- Miele & Cie. KG

- LG Electronics Inc.

- Samsung Electronics Co. Ltd.

- Candy Hoover Group(Haier Europe)

- Gorenje(Hisense Europe)

- Indesit

- Beko

- Hotpoint

- AEG

- Zanussi

- Teka Group

- Blomberg

- Asko Appliances

- Smeg SpA

- Vestel

- Sharp Corp.

- Grundig

제7장 시장 기회 및 장래 전망

AJY 26.01.30The European tumble dryer market was valued at USD 2.86 billion in 2025 and estimated to grow from USD 3.00 billion in 2026 to reach USD 3.83 billion by 2031, at a CAGR of 4.99% during the forecast period (2026-2031).

In absolute terms, the European tumble dryer market is evolving from a mature replacement-driven appliance category to a technology-led upgrade cycle triggered by the European Union's ecodesign mandate that bans vented and entry-level condenser units from July 2025. . Heat-pump innovation, the rising cost of household energy, and a post-pandemic focus on sustainability jointly underpin healthy demand momentum despite lingering macro volatility. Competitive strategies now hinge on regulatory compliance, premium positioning, and rapid portfolio renewal, while regional disparities remain pronounced as Germany maintains a lead in unit penetration but Spain posts the fastest incremental growth. Price sensitivity in Eastern and parts of Southern Europe tempers immediate heat-pump uptake, yet supportive financing schemes and bulk-procurement programs in social housing are widening the addressable base. Simultaneously, omnichannel distribution, especially via online marketplaces, is remolding customer acquisition economics and favoring brands with direct-to-consumer capabilities. Supply chain friction linked to R290 refrigerant and continued fire-safety scrutiny highlight the market's operational risks, but IoT-ready models and utility demand-response pilots represent adjacent revenue pools that will mature during the outlook period.

Europe Tumble Dryers Market Trends and Insights

EU Energy-Efficiency Mandates Accelerating Heat-Pump Adoption

The July 2025 ecodesign regulation compels manufacturers to eliminate non-heat-pump technology from their European portfolios, instantly transforming the Europe tumble dryer market into a single-technology contest. This rule alone is expected to save 15 TWh of electricity and 1.7 Mt CO2-equivalent by 2040, generating USD 2.8 billion in cumulative consumer savings. A-class ratings now appear exclusively on heat-pump models, effectively relegating vented or basic condenser dryers to non-compliant status. Premium brands such as Miele responded early, unveiling the T2 Nova Edition with InfinityCare drums and wool-specific cycles that showcase fabric-care benefits beyond raw energy efficiency. BSH capitalized on the transition by re-balancing production toward heat-pump units, thereby sustaining profit margins while meeting compliance. The regulation simultaneously introduces a two-tier pricing environment in which premium manufacturers can defend value, whereas value-oriented firms face intense margin pressure. Compliance audits based on ISO 14001 sustainability credentials are becoming procurement prerequisites, further raising competitive barriers for late adopters.

Rising Disposable Income & Replacement Cycles in Western Europe

Improved macro conditions and subdued inflation are rekindling discretionary spending, with EU consumer-durables sales swinging from a 2.90% decline in 2023 to a 2.80% upswing in 2025. Replacement cycles average 8-10 years, and rising electricity tariffs push households to prioritize life-cycle cost over sticker price, favoring heat-pump solutions despite a 2-3X upfront premium. Germany and the Netherlands reinforce adoption via cash-back schemes, while southern markets remain more price sensitive. The European household appliance market is projected to grow from USD 38.48 billion to USD 42.40 billion by 2027, with smart appliances experiencing 26% growth as consumers demand energy efficiency and convenience features. Survey data reveal 80% of UK respondents worried about utility bills, translating into a higher willingness to invest in efficient dryers. Established brands exploit loyalty advantages, as 35% of global consumers list brand reputation as a decisive factor. Altogether, income growth plus replacement urgency contribute a 1.2-percentage-point tailwind to the Europe tumble dryer market CAGR.

High Upfront Price Premium of Heat-Pump Models

Heat-pump dryers often retail for EUR 1,000 (USD 1,090) or more versus EUR 300-400 (USD 327-436) for vented alternatives, creating a steep affordability hurdle. Although lifetime energy savings can exceed USD 500, the payback horizon discourages adoption among lower-income households in Eastern Europe. Financing schemes and government rebates partially bridge the gap, but penetration lags until economies of scale lower unit costs. Samsung and LG are testing entry-level heat-pump SKUs with AI-driven optimization at sub-EUR 800 (USD 872) price points, potentially resetting market expectations. European incumbents must choose between defending margin or sacrificing ASP to accelerate conversion, with each approach influencing brand equity and installed-base economics. In the near term, price barriers shave roughly 1.4 percentage points off the CAGR of the Europe tumble dryer market.

Other drivers and restraints analyzed in the detailed report include:

- Growth of E-Commerce Channels for MDA Purchases

- Social-Housing Retrofit Programs Specifying Heat-Pump Dryers

- Market Saturation in Core EU-5 Residential Segment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Heat-pump models entered 2025 with a 35.44% contribution to the Europe tumble dryer market size and are advancing at a 13.10% CAGR, bolstered by the regulatory ban on vented and basic condenser units effective mid-2025. Condenser dryers, once dominant, still held 50.92% of Europe tumble dryer market share in 2025, yet they face an unavoidable sunset, funneling demand into compliant alternatives. Premium positioning hinges on 70% lower energy consumption and fabric-care advantages, allowing manufacturers to defend pricing even as entry-level SKUs emerge. Samsung's Bespoke AI Laundry Combo illustrates the convergence of large-capacity engineering and machine-learning-based cycle optimization. LG counters with a fully heat-pump Signature stack that reduces power draw to 570 W, demonstrating differing technological bets. Over the forecast horizon, product differentiation will increasingly rely on connectivity, environmental certifications, and after-sales services rather than core mechanical performance alone.

The Europe tumble dryer market also witnesses a gradual fadeout of vented designs, historically popular in the UK due to easy exterior venting in single-family homes. Landlord refurbishments and changing building codes shift those installations toward closed-cycle condensers or heat-pump units. Manufacturers retool factories accordingly, with BSH reallocating production lines to higher-margin heat-pump families. Component suppliers adapt by phasing out resistive heaters and scaling up R290 compressor output. The impending cliff on non-compliant stock encourages retailers to clear inventories through discounting, temporarily distorting average selling prices. Yet post-2025, category revenues rebound as the Europe tumble dryer market pivots to all-heat-pump portfolios linked with bundled service contracts that protect margins.

The Europe Tumble Dryer Market Report is Segmented by Product Type (Heat Pump Tumble Dryer, Condenser Tumble Dryer, Vented Tumble Dryer), End-User (Residential, Commercial), Distribution Channel (Offline, Online), and Geography (United Kingdom, Germany, France, Spain, Italy, BENELUX, NORDICS, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- BSH Hausgerate GmbH (Bosch/Siemens)

- Whirlpool Corp.

- Electrolux AB

- Miele & Cie. KG

- LG Electronics Inc.

- Samsung Electronics Co. Ltd.

- Candy Hoover Group (Haier Europe)

- Gorenje (Hisense Europe)

- Indesit

- Beko

- Hotpoint

- AEG

- Zanussi

- Teka Group

- Blomberg

- Asko Appliances

- Smeg S.p.A.

- Vestel

- Sharp Corp.

- Grundig

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EU energy-efficiency mandates accelerating heat-pump adoption

- 4.2.2 Rising disposable income & replacement cycles in Western Europe

- 4.2.3 Growth of e-commerce channels for MDA purchases

- 4.2.4 Social-housing retrofit programs specifying heat-pump dryers

- 4.2.5 Hospitality ESG targets driving high-efficiency fleet upgrades

- 4.2.6 IoT-ready dryers for utility demand-response pilots

- 4.3 Market Restraints

- 4.3.1 High upfront price premium of heat-pump models

- 4.3.2 Market saturation in core EU-5 residential segment

- 4.3.3 Fire-safety recall incidents denting consumer trust

- 4.3.4 R290 refrigerant supply-chain volatility

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Heat Pump Tumble Dryer

- 5.1.2 Condenser Tumble Dryer

- 5.1.3 Vented Tumble Dryer

- 5.2 By End-User

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.3 By Distribution Channel

- 5.3.1 Offline

- 5.3.2 Online

- 5.4 By Country

- 5.4.1 United Kingdom

- 5.4.2 Germany

- 5.4.3 France

- 5.4.4 Spain

- 5.4.5 Italy

- 5.4.6 BENELUX

- 5.4.6.1 Belgium

- 5.4.6.2 Netherlands

- 5.4.6.3 Luxembourg

- 5.4.7 NORDICS

- 5.4.7.1 Denmark

- 5.4.7.2 Finland

- 5.4.7.3 Iceland

- 5.4.7.4 Norway

- 5.4.7.5 Sweden

- 5.4.8 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 BSH Hausgerate GmbH (Bosch/Siemens)

- 6.4.2 Whirlpool Corp.

- 6.4.3 Electrolux AB

- 6.4.4 Miele & Cie. KG

- 6.4.5 LG Electronics Inc.

- 6.4.6 Samsung Electronics Co. Ltd.

- 6.4.7 Candy Hoover Group (Haier Europe)

- 6.4.8 Gorenje (Hisense Europe)

- 6.4.9 Indesit

- 6.4.10 Beko

- 6.4.11 Hotpoint

- 6.4.12 AEG

- 6.4.13 Zanussi

- 6.4.14 Teka Group

- 6.4.15 Blomberg

- 6.4.16 Asko Appliances

- 6.4.17 Smeg S.p.A.

- 6.4.18 Vestel

- 6.4.19 Sharp Corp.

- 6.4.20 Grundig

7 Market Opportunities & Future Outlook

- 7.1 Demand-response-ready heat-pump dryers integrated into home-energy-management systems

- 7.2 Subscription-based "laundry-appliance-as-a-service" models for urban micro-apartments