|

시장보고서

상품코드

1934738

타이어 재료 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Tire Material - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

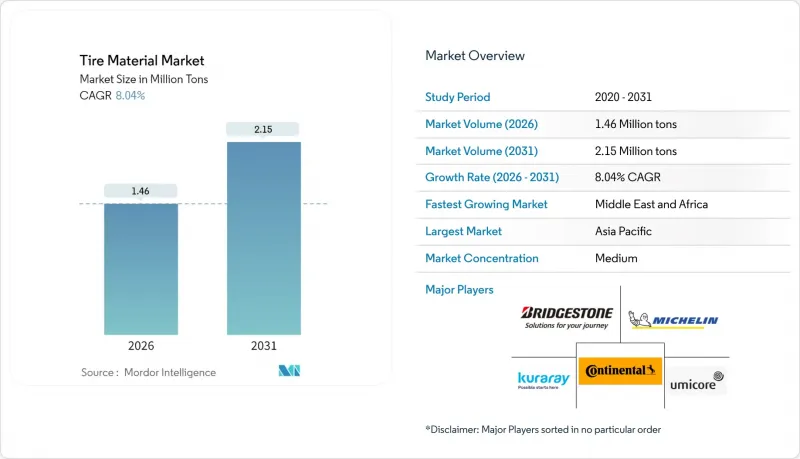

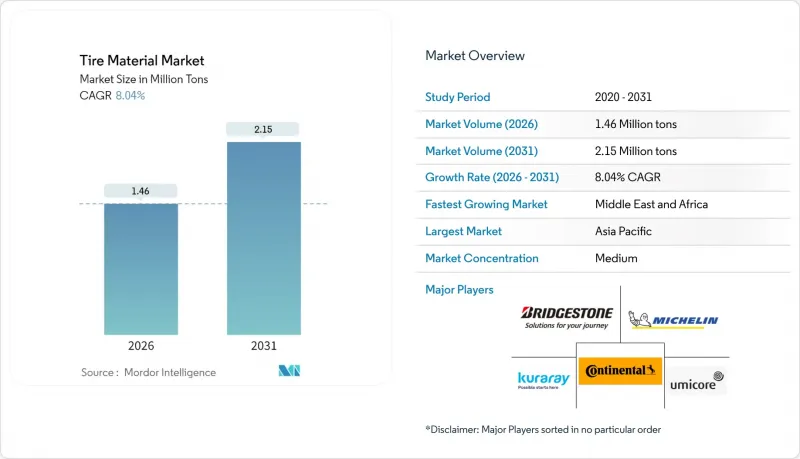

2026년 타이어 재료 시장 규모는 146만 톤으로 추정되며, 2025년 135만 톤으로부터 성장하며, 2031년에는 215만 톤에 달할 것으로 예측됩니다.

2026-2031년 연평균 복합 성장률(CAGR) 8.04%로 확대될 것으로 예측됩니다.

전기자동차 배터리 팩으로 인한 차량 중량 증가, 유로 7 표준의 엄격한 타이어 마모 한계치, E-Commerce를 위한 차량 교체 주기의 가속화로 인해 합성 엘라스토머와 고실리카 충전 시스템에 대한 수요가 증가하고 있습니다. 통합 타이어 제조업체는 재생 카본블랙과 바이오 실리카에 대한 투자를 진행하고 있으며, 이는 공급망의 안정성이 현물 가격 고려 사항을 능가하고 있음을 보여줍니다. 아시아태평양이 세계 생산량을 주도하는 가운데, 중동의 국가 주도의 다각화 프로그램은 새로운 생산 능력을 창출하고 지역 무역 흐름을 재편할 것으로 예측됩니다. 주요 리스크 요인으로는 유가 변동성, PFAS 규제 동향, OEM 재고 조정 지속 등을 들 수 있으며, 이러한 요인들이 복합적으로 작용하여 계획기간 단축을 초래하고 순환형 원재료의 가치를 높이고 있습니다.

세계 타이어 소재 시장 동향과 인사이트

전기자동차(EV) 및 하이브리드차 생산의 세계 확대

2023년 전기 트럭 판매량은 전년 대비 35% 증가한 5만 4,000대에 달하고, 처음으로 전기버스 판매량을 넘어섰습니다. 300-500kg의 배터리 팩은 타이어 접지면에 추가 하중을 가하여 기존 컴파운드의 수명을 절반으로 줄입니다. 타이어 제조업체들은 현재 액체 파르네센 고무와 같은 합성 블렌드를 테스트하여 발열 증가 없이 낮은 구름 저항 목표를 달성하기 위해 노력하고 있습니다. 국제고무연구그룹(IRSG)은 천연고무 수요가 2030년까지 1,690만 톤에 달할 것으로 예측하고 있지만, EV 플랫폼은 판매량 증가와 기존 엘라스토머의 비율을 분리하고 있습니다. 공급업체인 Kuraray와 JSR은 솔루션 S-SBR과 동등한 성능을 가지면서도 탄소강도가 낮은 바이오폴리머의 상용화를 빠르게 진행하고 있으며, 타이어 소재 시장이 특수 엘라스토머로 전환하고 있는 이유를 지원하고 있습니다.

OEM(Original Equipment Manufacturer)의 낮은 구름 저항 화합물로의 전환

2026년 중반에 시행되는 유로7 규제는 승용차 타이어 마모를 7mg/km, 소형 상용차는 11mg/km로 제한하므로 고카본블랙 배합의 사용이 제한됩니다. OEM(Original Equipment Manufacturer)들은 현재 습식 그립 성능 목표를 달성하면서 회전 저항을 최대 20%까지 감소시키는 실리카-실란계 배합을 지정하고 있습니다. 바이오 에탄올에서 추출한 에보닉의 ULTRASIL 9100 GR은 표면적 요구 사항을 손상시키지 않고 CO2 배출량을 60% 감소시킵니다. PPG의 AGILON 실리카는 유사한 견인 효과를 실현하면서 혼합 에너지 감소에 중점을 두고 있으며, 유럽의 전력 비용 상승에 따라 우선순위가 높아지고 있습니다. 북미 트럭 OEM 업체들은 여전히 80℃ 이상의 고온에 견딜 수 있는 카본블랙이 풍부한 배합을 선호하고 있으며, 이는 필러 수요를 분산시켜 공급업체가 이중 생산라인을 유지해야만 하는 상황을 초래합니다.

유가 및 카본블랙 가격 변동

유럽의 카본블랙 가격은 러시아로부터의 수입금지 조치로 인해 2024년 6월 18% 상승했습니다. 이로 인해 타이어 제조업체들은 튀르키예와 이집트에서 고가의 원료를 조달할 수밖에 없었습니다. FCC 타르 등 원료는 브렌트유 가격을 3개월 정도 늦게 따라가기 때문에 유가 상승이 계약 재협상을 상회할 경우 마진 압축이 발생합니다. 캐봇의 2024년 4분기 보강재 판매량은 가격 불확실성으로 인해 고객이 재고 보충을 늦추면서 7% 감소했습니다. 천연고무 선물도 변동이 심해, 2025년 3월에는 태국과 인도네시아의 생산량 증가로 인해 전주 대비 2.1% 하락했습니다. 이로 인해 타이어 제조업체들은 60-90일 분량의 안전재고를 보유할 수 밖에 없어 운전자금이 묶여 있는 상황입니다.

부문 분석

엘라스토머는 2025년 타이어 소재 시장 규모의 42.88%를 차지할 것으로 예상되며, 2031년까지 연평균 5.43%의 연평균 복합 성장률(CAGR)로 확대될 것으로 예상되며, EV 응용 분야에서 합성 블렌드가 순수 천연 고무를 대체할 것으로 예측됩니다. 천연고무는 우수한 인열강도로 인해 승용차 타이어의 주류를 이루고 있지만, 낮은 구름저항 규제 강화로 인해 용액 S-SBR, 폴리부타디엔, 바이오 액상 파르네센 고무로의 전환이 가속화되고 있습니다. Kuraray는 미쉐린의 파일럿 프로그램에서 수명주기 CO2 배출량 30% 감소, 구름 저항 10% 감소를 보고했으며, 이는 프리미엄 OEM 사양이 새로운 폴리머를 어떻게 평가하고 있는지를 보여줍니다. 전체 컴파운드의 약 1/3을 차지하는 보강 충전재의 경우, Euro 7의 마모 한계 규제로 인해 고실리카 배합이 요구됨에 따라 실리카의 점유율이 상승하고 있습니다. 에보닉과 PPG의 바이오에탄올 기반 실리카 등급은 카본블랙과의 역사적 비용 차이를 좁히고 있으며, 이러한 변화는 타이어 소재 시장에서 공급업체 기반의 다양화를 촉진하고 있습니다.

경량 가소제는 방향족 함량에 대한 REACH 규제 강화로 인해 처리된 증류물 추출물과 톨루엔 오일 유도체로 전환이 진행되고 있습니다. 이는 복합재료 비용을 1kg당 0.10-0.15달러 증가시키지만, 환경 부하를 줄이는데 기여하고 있습니다. 나노 산화아연 등급은 중금속 함량을 40% 감소시켜 재활용을 용이하게 합니다. 반면, 베카르의 스크랩 함량이 50%인 강선은 컴파운드의 CO2 배출량을 절반으로 줄입니다. 이러한 점진적인 발전으로 OEM(Original Equipment Manufacturer)가 제조부터 폐기까지 지속가능성 지표를 추구함에 따라 재료 공급업체는 프리미엄 가격 책정 위치를 확보할 수 있게 되었습니다.

타이어 재료 시장 보고서는 재료 유형(엘라스토머, 보강 충진재, 가소제, 화학물질, 금속 보강재, 섬유 보강재), 차종(승용차, 소형 상용차, 대형 트럭, 버스), 지역(아시아태평양, 북미, 유럽, 유럽, 남미, 중동 및 아프리카) 별로 분류됩니다. 시장 예측은 톤 단위로 제공됩니다.

지역별 분석

2025년 아시아태평양은 타이어 재료 시장 점유율의 52.05%를 차지했습니다. 이는 중국의 소형차 생산량이 3,050만대로 세계 천연고무 공급량의 62%를 차지하고 있는 배경에 기인합니다. 사이론, 린롱 등 중국 타이어 제조업체들은 2024년 70% 이상의 순이익 성장을 보고하고 국내외에서 생산 능력을 확장하고 있으며, 업스트림 소재에 대한 지속적인 수요를 보여주고 있습니다. 일본의 브리지스톤, 스미토모 고무, 요코하마 고무는 2025년도에 총 설비투자를 10.6% 증액하여 고부가가치 EV 부품과 해외 공장에 자금을 투입하고 있습니다. 동남아시아의 비용 우위와 천연고무에 대한 접근성은 신규 진입을 촉진하는 한편, EU의 타이어 라벨 기준은 현지 제조업체들이 낮은 구름 저항 배합을 채택하여 고급 충전재에 대한 수출 수요를 창출하고 있습니다.

중동 및 아프리카은 가장 빠르게 성장하는 지역으로 사우디와 UAE가 산업 다각화 전략을 펼치면서 2031년까지 연평균 복합 성장률(CAGR) 5.82%를 보일 것으로 예측됩니다. 5억 5,000만 달러 규모의 피렐리 PIF 공장과 이집트의 18억 달러 규모의 생산능력 계획 등으로 자급자족형 클러스터 구축이 약속되어 있으며, 현지에서의 카본블랙, 실리카, 합성고무 공급이 필요합니다. 유럽과 북미는 규제 압력으로 인해 바이오 실리카 및 재생 카본블랙의 채택이 가속화되고 엄격한 추적성 표준이 도입됨에 따라 혁신의 중심지 역할을 하고 있습니다. 이러한 교훈은 나중에 신흥 시장에도 파급됩니다. 남미의 성장률은 3-4%이며, 환율 변동과 생산능력 확대 둔화로 인해 성장률이 억제되고 있습니다. 그러나 브라질은 7,000만대의 자동차 보유대수라는 탄탄한 애프터마켓 기반이 있으며, 특수 필러에 대한 수입 수요가 여전히 존재합니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

The tire material market size in 2026 is estimated at 1.46 million tons, growing from 2025 value of 1.35 million tons with 2031 projections showing 2.15 million tons, growing at 8.04% CAGR over 2026-2031.

Higher vehicle weight from electric-vehicle battery packs, tighter Euro 7 tire-abrasion limits, and accelerated replacement cycles in e-commerce fleets are shifting demand toward synthetic elastomers and high-silica filler systems. Integrated tire makers are investing in recovered carbon black and bio-based silica, signaling that supply-chain security now outweighs spot-price considerations. The Asia-Pacific region dominates the global volume, while sovereign diversification programs in the Middle East are unlocking greenfield capacity that will reshape regional trade flows. Headline risks center on crude oil volatility, pending PFAS restrictions, and lingering OEM inventory destocking that together shorten planning horizons and elevate the value of circular feedstocks.

Global Tire Material Market Trends and Insights

Global Ramp-Up of EV and Hybrid Vehicle Production

Electric trucks sold 54,000 units in 2023, 35% higher than in 2022, marking the first time the category outpaced electric buses. Battery packs weighing 300-500 kg place additional load on tire contact patches, cutting traditional compound life in half. Tire makers now test synthetic blends, such as liquid farnesene rubber, to meet lower rolling-resistance targets without increasing heat buildup. The International Rubber Study Group expects natural-rubber demand to hit 16.9 million tons by 2030, yet EV platforms are decoupling volume growth from historical elastomer ratios. Suppliers Kuraray and JSR are racing to commercialize bio-based polymers that match the performance of solution S-SBR at a lower carbon intensity, reinforcing why the tire material market is shifting toward specialty elastomers.

OEM Shift Toward Low Rolling Resistance Compounds

Euro 7 rules, effective mid-2026, cap tire abrasion at 7 mg/km for passenger cars and 11 mg/km for light commercial vehicles, which limits the use of high-carbon-black compounds OEMs now specify silica-silane systems that cut rolling resistance by up to 20% while meeting wet-grip targets. Evonik's ULTRASIL 9100 GR, produced from bio-ethanol, delivers a 60% CO2 reduction without compromising surface-area requirements. PPG's AGILON silica attains similar traction benefits but emphasizes lower mixing energy, a priority as European electricity costs rise. North American truck OEMs still prefer carbon-black-rich recipes that resist heat above 80 °C, fragmenting filler demand and obliging suppliers to maintain dual production lines.

Volatile Crude Oil and Carbon-Black Pricing

European carbon-black prices rose 18% in June 2024, following the ban on imports from Russia, which forced tire makers to source higher-priced material from Turkey and Egypt. Feedstocks, such as FCC tar, track Brent crude with a three-month lag, resulting in margin compression when oil rallies outpace contract renegotiations. Cabot's Q4 2024 reinforcement volumes fell 7% as customers delayed restocking amid price uncertainty. Natural-rubber futures also remain volatile, dropping 2.1% week-over-week in March 2025 as Thai and Indonesian output expanded, prompting tire makers to hold 60-90 days of safety stock, which ties up working capital.

Other drivers and restraints analyzed in the detailed report include:

- Surge in E-Commerce Activities and Replacement Tire Miles

- Re-Industrialization of Southeast Asia Creating New Local Tire Plants

- Looming EU PFAS Ban Limiting Fluorinated Additives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Elastomers accounted for 42.88% of the tire material market size in 2025 and will expand at a 5.43% CAGR through 2031 as synthetic blends displace pure natural rubber in EV applications. Natural rubber still dominates passenger tires due to its superior tear strength, yet low-rolling-resistance mandates are accelerating the switch to solution S-SBR, polybutadiene, and bio-based liquid farnesene rubber. Kuraray reports lifecycle CO2 cuts of 30% and a 10% reduction in rolling resistance in Michelin pilot programs, illustrating how premium OEM specifications reward novel polymers. Reinforcing fillers, which occupy approximately one-third of the total compound volume, are witnessing a rise in silica's share as Euro 7 abrasion limits force higher-silica tread recipes. Bio-ethanol silica grades from Evonik and PPG are closing the historical cost gap with carbon black, a shift that further diversifies supplier bases within the tire material market.

Lightweight plasticizers face stricter REACH limits on aromatic content, prompting a shift toward treated distillate extracts and tall-oil derivatives, even though they add USD 0.10-0.15 per kilogram to compound cost. Nano-zinc-oxide grades cut heavy-metal loading by 40%, easing recycling, while Bekaert steel cord with 50% scrap content lowers compound CO2 by half. These incremental advances position material suppliers for premium pricing as OEMs chase cradle-to-grave sustainability metrics.

The Tire Material Market Report is Segmented by Material Type (Elastomers, Reinforcing Fillers, Plasticizers, Chemicals, Metal Reinforcements, and Textile Reinforcements), Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Trucks, Buses), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific held 52.05% of the tire material market share in 2025, underpinned by China's 30.5-million-unit light-vehicle output and the region's 62% share of global natural-rubber supply. Chinese tire makers, such as Sailun and Linglong, reported net profit growth exceeding 70% in 2024 and are expanding capacity both domestically and internationally, indicating sustained demand for upstream materials. Japan's Bridgestone, Sumitomo, and Yokohama raised their combined capital expenditure by 10.6% for FY 2025, directing funds toward high-value EV components and overseas plants. Southeast Asia's cost advantage and access to raw rubber encourage new entrants, while EU-aligned tire labeling standards prompt local producers to adopt low-rolling-resistance recipes, creating export-ready demand for advanced fillers.

The Middle East and Africa region is the fastest-growing geography, registering a 5.82% CAGR through 2031, as Saudi Arabia and the UAE deploy industrial diversification strategies. Projects such as the USD 550 million Pirelli-PIF plant and Egypt's USD 1.8 billion capacity pipeline promise to build a self-sufficient cluster that will need local carbon black, silica, and synthetic rubber supply. Europe and North America remain innovation hubs because regulatory pressure accelerates the adoption of bio-based silica, recovered carbon black, and stringent traceability standards, lessons that later cascade to emerging markets. South America's growth is at 3-4%, tempered by currency volatility and slower capacity additions; however, Brazil's 70 million vehicle parc offers a resilient aftermarket base that still imports specialty fillers.

- Bekaert

- Birla Carbon

- Bridgestone Corporation

- Cabot Corporation

- Continental AG

- Evonik

- Exxon Mobil Corporation

- JSR Corporation

- Kuraray Co., Ltd.

- LANXESS

- Linglong Tire

- Michelin

- Orion

- Sailun Group Co., Ltd.

- Sumitomo Rubber Industries, Ltd.

- Umicore

- Zhongce Rubber Group Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Global ramp-up of EV and hybrid vehicle production

- 4.2.2 OEM shift toward low-rolling-resistance compounds

- 4.2.3 Surge in e-commerce activities and the corresponding rise in replacement tire miles

- 4.2.4 Re-industrialisation of Southeast Asia creating new local tire plants

- 4.2.5 Cold-in-place recycling enabling circular feedstocks

- 4.3 Market Restraints

- 4.3.1 Volatile crude-oil and carbon-black pricing

- 4.3.2 OEM inventory destocking in 2024-25

- 4.3.3 Looming EU PFAS ban limiting fluorinated additives

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Material Type

- 5.1.1 Elastomers

- 5.1.1.1 Natural Rubber

- 5.1.1.2 Synthetic Rubber

- 5.1.2 Reinforcing Fillers

- 5.1.2.1 Carbon Black

- 5.1.2.2 Silica

- 5.1.3 Plasticizers

- 5.1.3.1 Paraffinic Oil

- 5.1.3.2 Naphthenic Oil

- 5.1.3.3 Aromatic Oil

- 5.1.4 Chemicals

- 5.1.4.1 Sulfur

- 5.1.4.2 Zinc Oxide

- 5.1.4.3 Stearic Acid

- 5.1.5 Metal Reinforcements

- 5.1.5.1 Steel Cord

- 5.1.5.2 Bead Wire

- 5.1.6 Textile Reinforcements

- 5.1.6.1 Nylon

- 5.1.6.2 Polyester

- 5.1.6.3 Others

- 5.1.1 Elastomers

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Light Commercial Vehicles (LCV)

- 5.2.3 Heavy Trucks

- 5.2.4 Buses

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Turkey

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Bekaert

- 6.4.2 Birla Carbon

- 6.4.3 Bridgestone Corporation

- 6.4.4 Cabot Corporation

- 6.4.5 Continental AG

- 6.4.6 Evonik

- 6.4.7 Exxon Mobil Corporation

- 6.4.8 JSR Corporation

- 6.4.9 Kuraray Co., Ltd.

- 6.4.10 LANXESS

- 6.4.11 Linglong Tire

- 6.4.12 Michelin

- 6.4.13 Orion

- 6.4.14 Sailun Group Co., Ltd.

- 6.4.15 Sumitomo Rubber Industries, Ltd.

- 6.4.16 Umicore

- 6.4.17 Zhongce Rubber Group Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment