|

시장보고서

상품코드

1934810

임상시험 공급 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Clinical Trial Supply - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

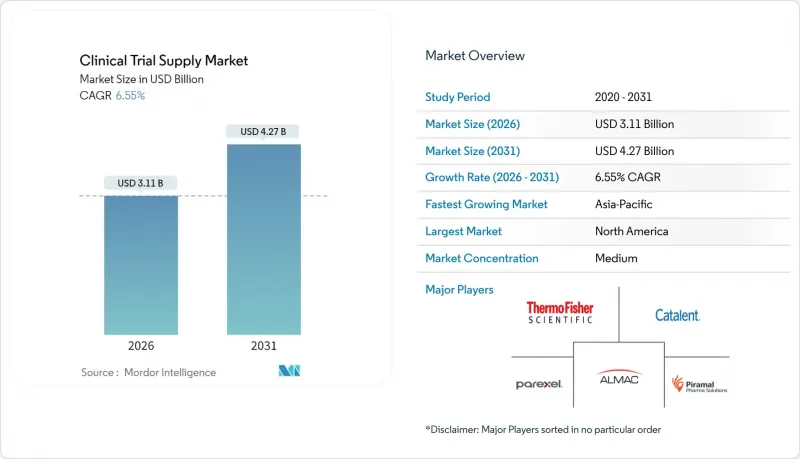

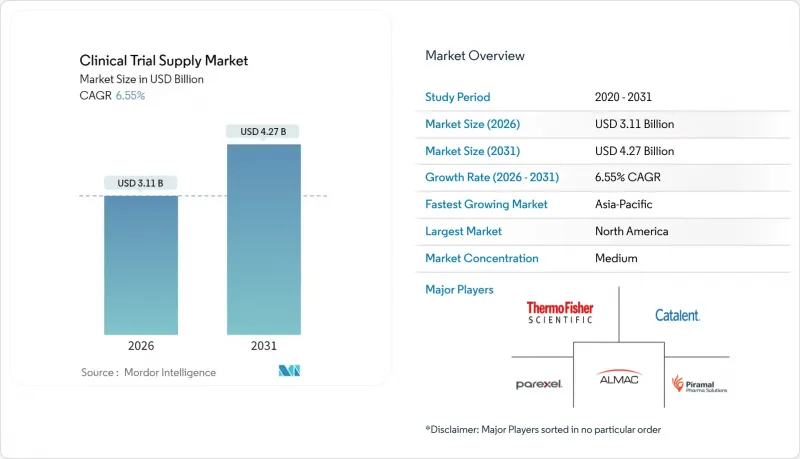

임상시험 공급 시장은 2025년에 29억 2,000만 달러로 평가되며, 2026년 31억 1,000만 달러에서 2031년까지 42억 7,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 6.55%로 예상됩니다.

분산형 임상시험(DCT)에 대한 규제 지원 강화, 바이오의약품 파이프라인의 급속한 증가, 실시간 온도 모니터링에 대한 수요 증가로 인해 스폰서들은 기술을 활용한 환자 중심 유통 모델로 전환하고 있습니다. 북미가 여전히 가장 큰 거점이지만, 아시아태평양의 빠른 성장은 채용 패턴의 변화, 더 깊은 연구자 네트워크, 국내 R&D에 대한 정부의 인센티브를 반영하고 있습니다. 복잡한 생물제제는 콜드체인 지출을 증가시키고 물류 전문가들이 초저온 기능을 추가하고 지속적인 운송 경로에 대한 가시성을 제공하는 IoT 센서에 투자하도록 유도하고 있습니다. 통합된 엔드투엔드 서비스 제공이 벤더 선택의 결정적인 요소로 떠오르면서 CRO(임상시험수탁기관)와 3PL(제3자 물류) 업체 간의 통합이 가속화되고 있습니다. 지속적인 의약품 부족, 관세 위험, 비교 대상 의약품의 비용 상승은 정적인 안전 재고 계산이 아닌 예측 분석에 기반한 강력한 다중 노드 공급망의 필요성을 강조하고 있습니다.

세계 임상시험 공급 시장 동향 및 인사이트

전 세계 임상시험 건수 증가

2023년 업계 주도의 임상시험 완료 건수는 전년 대비 10.7% 증가한 4,295건으로, 암 분야와 신흥 감염병 프로그램에 대한 스폰서들의 지속적인 의지를 보여주고 있습니다. 정밀의료 프로토콜의 급증으로 환자 코호트 세분화, 병행 시험 수 증가. 각 임상시험은 소량이지만 빈번한 임상시험용 의약품(IP) 수송을 필요로 합니다. 2024년 중반 현재 중국과 미국을 합친 가동 중인 등록 시험 건수는 32만 2,244건에 달하고, 국경을 넘는 물류 경로에 대한 부하가 얼마나 큰지 알 수 있습니다. 정부도 수요를 지원하고 있습니다. 미국 바이오의약첨단연구개발국(BARDA)은 엄격한 일정에 따라 공급이 필수적인 COVID-19 백신 임상 2b상 시험을 위해 새로운 자금을 투입했습니다. 이러한 움직임과 함께 임상시험용 의약품의 유통량은 지속적으로 증가하고 있으며, 지역적 병목현상을 피하기 위해 디지털 추적 시스템을 갖춘 확장 가능한 멀티노드 스토리지 네트워크 구축이 요구되고 있습니다.

전문 서비스 프로바이더에 대한 아웃소싱 증가

스폰서 기업의 CRO(의약품 개발 수탁기관) 및 물류 전문업체에 대한 의존도는 더욱 심화되고 있으며, 비 핵심적인 내부 기능을 폐지하는 움직임에 따라 CRO의 매출은 2029년까지 1,390억 달러에 달할 것으로 예측됩니다. IQVIA는 '데이터에서 유통까지' 통합 파트너로 자리매김하며 2023년 149억 8,000만 달러의 매출을 기록했습니다. 한편, 써모피셔 사이언티픽은 의약품 서비스 플랫폼에서 132억 9,000만 달러의 매출을 올리고 있습니다. 기능별 서비스 프로바이더(FSP) 모델은 풀서비스형 아웃소싱을 능가하는 성장률을 보이고 있으며, 스폰서 기업은 포장, 라벨링, 환자 직접 배송 등의 전문 인력 풀을 모듈 단위로 활용할 수 있습니다. 중국 CRO 업체인 우시 앱텍(WuXi AppTec)은 2024년 84억 4,000만 달러의 매출을 달성할 것으로 예상되며, 제조와 임상 물류 서비스를 결합한 아시아 지역의 경쟁이 치열해지고 있음을 보여줍니다. 이러한 변화로 인해 IRT 시스템과 제3자 물류 프로바이더(3PL) 간의 실시간 통합에 대한 수요가 증가하고 있으며, 분산된 사이트 네트워크에서 일정에 따라 환자에게 투약이 이루어지도록 하기 위해 IRT 시스템 간의 실시간 통합에 대한 요구가 증가하고 있습니다.

비교대조약과 물류비 상승

브랜드 생물학적 비교약은 일반적으로 환자 1주기당 1만 달러 이상의 가격대를 형성하고 있으며, 이러한 가격 수준은 중견 스폰서의 예산을 압박하고 공급망 기반에 대한 자본 배분을 저해합니다. 35시간 -60℃ 이하를 보장하는 극저온 포장 시스템은 상온 보관 옵션의 몇 배에 달하는 비용이 소요되어 환자 1인당 물류비용을 증가시키고 있습니다. 인플레이션 억제법 가격 규정의 시행은 수입원 축소 위험을 초래할 수 있으며, 스폰서가 고가 적응증에 대한 우선순위를 낮추게 될 수 있습니다. 이는 피험자 모집의 복잡성과 배송의 불확실성을 증가시킵니다. 자동화된 저스트 인 타임라인은 폐기물을 줄일 수 있지만, 초기 자본 집약도가 높고 소규모 바이오텍 기업에게는 자금 조달이 어렵습니다.

부문 분석

보관 및 유통 부문은 전 세계 보관 거점 및 검증된 창고에 대한 지속적인 수요로 인해 2025년 임상시험 공급 시장 점유율의 52.12%를 차지하며 가장 큰 매출을 기록할 것으로 예측됩니다. 그러나 공급망 관리 분야는 7.95%의 연평균 복합 성장률(CAGR)로 성장을 촉진할 것으로 예상되며, 임상시험 공급 오케스트레이션 서비스 시장 규모는 2031년까지 13억 3,000만 달러에 달할 것으로 전망됩니다. 스폰서 기업은 IRT 데이터, IoT 센서 피드, 레인별 위험 점수를 통합한 실시간 대시보드를 높이 평가하고 있으며, 환자에게 직접 전달할 때 위험을 줄이기 위해 노력하고 있습니다.

디지털 전환은 빠르게 진행되고 있습니다. 수백만 건의 거래를 처리할 수 있는 블록체인 기반 임상시험 관리 플랫폼은 현재 다국가 연구를 지원하는 기반이 되고 있으며, 대조 오류를 줄이고 변조 불가능한 감사 추적을 제공합니다. 프론티어 사이언티픽 솔루션즈(Frontier Scientific Solutions)의 노스캐롤라이나-아일랜드 간 15억 달러 규모의 게이트웨이 프로젝트는 실시간 온도 원격 측정 기능을 갖춘 보세 및 GDP 준수 운송 회랑의 추진을 구현하고 있습니다. 통합형 오케스트레이션이 확산됨에 따라 서비스 구성은 기존 스토리지에서 데이터베이스, 리스크 기반 공급망 설계로 전환될 것으로 예측됩니다.

임상 3상 시험은 대규모 환자 코호트와 장기 치료 주기를 포함하며, 2025년 지출의 48.85%를 차지합니다. 그러나 임상 1상 시험은 8.18%의 가장 빠른 CAGR을 나타낼 것으로 예상되며, 2031년까지 임상시험 공급 시장 규모를 5억 7,000만 달러까지 끌어올릴 것으로 전망됩니다. 사이클 타임이 단축되고 프로토콜이 복잡해짐에 따라 민첩한 소량 포장과 신속한 수출입 통관에 대한 수요가 증가하고 있습니다.

지난 5년간 임상 1상 시험의 피험자 등록 기간이 39% 연장되었고, 고비용의 약물 과잉을 피하기 위해 IRT(정보자원기술)를 통한 예측 정확도의 중요성이 커지고 있습니다. 미국 국립보건원(NIH)은 2025년 예산으로 25억 달러를 임상시험에 배정했으며, 그 중 상당 부분이 인간 대상의 첫 임상시험에 할당되어 있습니다. 세포 치료의 개념 증명이 증가함에 따라 물류는 더욱 복잡해지고 있습니다. 단일 환자 배치의 경우, 좁은 시간 내에 생산과 택배 수거를 동기화해야 하기 때문입니다.

지역별 분석

2025년에는 북미가 38.91%로 가장 큰 매출 점유율을 차지할 것으로 예측됩니다. 이는 미국내 18만 6,497건의 등록 시험과 분산형 임상시험(DCT)에 대한 FDA의 지원적 지침에 힘입은 결과입니다. 캐나다는 지역적 근접성과 비용 우위를 활용하여 초기 단계의 시험을 유치하고 있으며, 멕시코는 수입 허가 간소화를 통해 히스패닉계를 대상으로 한 다양성 목표에 있으며, 그 중요성이 커지고 있습니다. 지역 물류 인프라는 UPS의 16억 달러 규모의 Andlauer Healthcare Group 인수를 통해 미국과 캐나다 전역의 콜드체인 창고 네트워크를 확장하여 강화되었습니다.

아시아태평양은 7.62%의 가장 빠른 CAGR을 나타낼 것으로 예상되며, 이는 중국의 13만 5,747건의 등록 시험과 IND 심사를 60일 이내로 단축하는 정부의 신속 심사 절차가 반영된 결과입니다. 일본은 고가 전략과 엄격한 GCP 준수를 유지하며 고 복잡성 생물학 연구를 지원하고 있습니다. 인도의 비용 우위가 사이트 구축을 가속화하는 한편, 호주의 영어 규제 신청은 유럽 및 미국 스폰서의 첫 환자 등록 기간을 단축할 수 있습니다. DHL의 CRYOPDP 인수로 아시아태평양 15개국에서 바이오 샘플 당일 회수 서비스가 확대되어 지역내 엔드투엔드 서비스 제공 체제가 강화되었습니다.

유럽에서는 스폰서들이 저비용의 중동 및 동유럽(CEE) 사이트로 이동함에 따라 서유럽의 시험 건수가 21% 감소했으나, 균형 잡힌 사업 기반을 유지하고 있습니다. 영국의 EU 탈퇴(브렉시트)로 인해 영국향 신청의 규제 중복이 지속되고 있으며, 일부 종양학 프로그램이 독일이나 스페인으로 이전하는 움직임이 나타나고 있습니다. 유럽의 그린딜은 재사용 가능한 운송용기 도입과 탄소중립 노선 감사가 가속화되고 있습니다. Thermo Fisher의 새로운 네덜란드 초저온 허브는 세포치료제 임상시험을 위한 대륙별 운송 능력을 강화하여 유럽 스폰서들에게 대서양 횡단 수출에 대한 대안을 제공합니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

The clinical trial supply market was valued at USD 2.92 billion in 2025 and estimated to grow from USD 3.11 billion in 2026 to reach USD 4.27 billion by 2031, at a CAGR of 6.55% during the forecast period (2026-2031).

Rising regulatory support for decentralized clinical trials (DCTs), a rapid uptick in biologics pipelines, and heightened demand for real-time temperature monitoring are steering sponsors toward technology-enabled, patient-centric distribution models. North America remains the single largest hub, but Asia-Pacific's faster growth reflects shifting recruitment patterns, deeper investigator networks, and government incentives for domestic R&D. Complex biologics amplify cold-chain spending, prompting logistics specialists to add ultra-cold capacity and invest in IoT sensors that give continuous lane visibility. Consolidation among contract research organizations (CROs) and third-party logistics (3PL) providers is accelerating as integrated, end-to-end offerings become decisive in vendor selection. Persistent drug shortages, tariff risks, and comparator-drug cost inflation underline the need for resilient, multi-node supply chains built on predictive analytics rather than static safety-stock calculations.

Global Clinical Trial Supply Market Trends and Insights

Growth in Global Clinical-Trial Volume

Industry-sponsored trial completions climbed 10.7% year on year in 2023, totaling 4,295 studies and signaling sustained sponsor appetite for both oncology and emerging infectious-disease programs. A surge in precision-medicine protocols is fragmenting patient cohorts and multiplying the number of parallel studies that each require smaller yet more frequent investigational-product (IP) shipments. China and the United States together hosted 322,244 active registries by mid-2024, underscoring the load placed on cross-border logistics lanes. Governments are buttressing demand: the Biomedical Advanced Research and Development Authority (BARDA) directed new funding toward Phase 2b COVID-19 vaccine trials that must be supplied under stringent timelines. Collectively, these dynamics accelerate IP-volume growth and compel sponsors to deploy scalable, multi-node depot networks supported by digital tracking to avoid regional bottlenecks.

Rising Outsourcing to Specialized Service Providers

Sponsor reliance on CROs and logistics specialists continues to deepen; CRO revenue is projected to reach USD 139 billion by 2029 as sponsors disband non-core internal functions. IQVIA posted USD 14.98 billion in 2023 revenue by positioning itself as an integrated data-to-distribution partner, while Thermo Fisher Scientific earned USD 13.29 billion from its pharma services platform. Functional Service Provider (FSP) models are growing faster than full-service outsourcing, giving sponsors modular access to packaging, labeling, or direct-to-patient delivery talent pools. Chinese CRO heavyweight WuXi AppTec generated USD 8.44 billion in 2024, highlighting intensifying Asian competition built on combined manufacturing and clinical-logistics offerings. These shifts elevate demand for real-time integration between IRT systems and third-party logistics providers (3PLs) to secure on-schedule patient dosing across a dispersed site network.

Escalating Costs of Comparator Drugs and Logistics

Branded biologic comparators often trade above USD 10,000 per patient cycle, a pricing layer that squeezes mid-size sponsor budgets and redirects capital away from supply-chain infrastructure. Cryogenic packaging systems able to guarantee <=-60 °C for 35 hours cost several times more than ambient options, inflating per-patient logistics expense. Implementation of the Inflation Reduction Act's pricing provisions risks trimming revenue streams and could force sponsors to prioritize fewer, high-value indications, thereby raising recruitment complexities and shipment unpredictability. Automated just-in-time lines reduce wastage but carry steep upfront capital intensity that smaller biotech cohorts struggle to finance.

Other drivers and restraints analyzed in the detailed report include:

- Proliferation of Complex Biologics Requiring Cold-Chain Logistics

- Advances in Interactive Response-Technology Platforms

- Supply-Chain Disruptions from Geopolitical Instability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Storage & Distribution held the largest 2025 revenue, capturing 52.12% of the clinical trial supply market share due to the enduring need for global depots and validated warehousing. Supply Chain Management, however, is forecast to lead growth with a 7.95% CAGR, pushing the clinical trial supply market size for orchestration services to USD 1.33 billion by 2031. Sponsors increasingly value real-time dashboards that integrate IRT data, IoT sensor feeds, and lane-specific risk scores to de-risk direct-to-patient shipments.

Digital transformation is progressing fast. Blockchain-enabled clinical-trial management platforms capable of processing millions of transactions now underpin multi-country studies, reducing reconciliation errors and offering immutable audit trails. Frontier Scientific Solutions' USD 1.5 billion gateway project between North Carolina and Ireland exemplifies the push toward bonded, GDP-compliant corridors with real-time temperature telemetry. As integrated orchestration gains traction, the service mix will shift away from traditional storage toward data-driven, risk-based supply-chain design.

Phase III studies, covering expansive patient cohorts and long treatment cycles, accounted for 48.85% of 2025 spend. Yet Phase I is projected to log the fastest 8.18% CAGR, lifting its clinical trial supply market size to USD 0.57 billion by 2031. Shorter cycle times and higher protocol complexity push demand for agile, small-batch packaging and rapid import-export clearance.

Enrollment timelines in Phase I expanded 39% over the past five years, intensifying pressure on IRT-driven forecasting accuracy to avoid costly drug overage. Government backing strengthens momentum: the National Institutes of Health committed USD 2.5 billion to clinical trials in its 2025 appropriation, a substantial share earmarked for first-in-human studies. Rising cell-therapy proofs of concept further complicate logistics because single-patient batches require synchronized manufacturing and courier pick-up within narrow windows.

The Clinical Trial Supply Market Report is Segmented by Clinical Phase Type (Phase I, Phase II, and More), Product and Services (Manufacturing, and More), End-User (Pharmaceutical Companies, and More), Therapeutic Area (Oncology, CNS Disorders, Infectious Diseases, and More), Geography (North America, Europe, Asia-Pacific, The Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated the largest 38.91% revenue share in 2025, anchored by the United States' 186,497 registered studies and supportive FDA guidance on DCTs. Canada leverages proximity and cost advantages to attract early-phase studies, while Mexico gains relevance for Hispanic-focused diversity targets, helped by streamlined import licenses. Regional logistics infrastructure benefits from UPS's USD 1.6 billion deal to acquire Andlauer Healthcare Group, which augments cold-chain depots across the United States and Canada.

Asia-Pacific is projected to post the swiftest 7.62% CAGR, reflecting China's 135,747 registered trials and government fast-track pathways that trim IND review to as few as 60 days. Japan sustains premium pricing and stringent GCP compliance, supporting high-complexity biologic studies. India's cost differential fuels rapid site rollouts, while Australia's English-language regulatory filings shorten first-patient-in timelines for Western sponsors. DHL's acquisition of CRYOPDP widens same-day biospecimen pickup across 15 Asia-Pacific nations, bolstering regional end-to-end offerings.

Europe maintains a balanced footprint despite Western Europe's 21% drop in trial volume as sponsors pivot toward lower-cost Central and Eastern European (CEE) sites. Brexit continues to add regulatory duplication for UK submissions, nudging some oncology programs to relocate to Germany or Spain. The region's Green Deal accelerates uptake of reusable shippers and carbon-neutral lane audits. Thermo Fisher's new Dutch ultra-cold hub shores up continent-wide capacity for cell-therapy trials, giving European sponsors an alternative to trans-Atlantic exports.

- Thermo Fisher Scientific

- Catalent

- Parexel International

- Almac Group

- Marken (DHL Supply Chain)

- PCI Pharma Services

- World Courier

- Recipharm

- IQVIA

- Sharp Clinical

- Syneos Health

- ICON

- Biocair

- Yourway

- Patheon

- Piramal Group

- UDG Healthcare (Ashfield)

- Myonex

- Rubicon Research

- Clinigen

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth in Global Clinical Trial Volume

- 4.2.2 Rising Outsourcing to Specialized Service Providers

- 4.2.3 Proliferation of Complex Biologics Requiring Cold Chain Logistics

- 4.2.4 Advances in Interactive Response Technology Platforms

- 4.2.5 Increasing Regulatory Support for Patient-Centric Trial Designs

- 4.2.6 Emphasis on Sustainable Supply Chain Practices

- 4.3 Market Restraints

- 4.3.1 Escalating Costs of Comparator Drugs And Logistics

- 4.3.2 Supply Chain Disruptions from Geopolitical Instability

- 4.3.3 Shortage of Skilled Personnel in GMP Packaging and Labeling

- 4.3.4 Cybersecurity Vulnerabilities in Digital Supply Platforms

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Clinical Phase Type

- 5.1.1 Phase I

- 5.1.2 Phase II

- 5.1.3 Phase III

- 5.1.4 Phase IV / BA-BE / Other

- 5.2 By Product and Services

- 5.2.1 Manufacturing

- 5.2.2 Storage & Distribution

- 5.2.3 Supply Chain Management

- 5.3 By End-User

- 5.3.1 Pharmaceutical Companies

- 5.3.2 Biopharmaceutical / Biologics Firms

- 5.3.3 Medical-Device Sponsors

- 5.3.4 Contract Research Organizations (CROs)

- 5.4 By Therapeutic Area

- 5.4.1 Oncology

- 5.4.2 CNS Disorders

- 5.4.3 Infectious Diseases

- 5.4.4 Metabolic Disorders

- 5.4.5 Cardiovascular

- 5.4.6 Other Therapeutic Areas

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Thermo Fisher Scientific

- 6.3.2 Catalent

- 6.3.3 Parexel

- 6.3.4 Almac Group

- 6.3.5 Marken (DHL Supply Chain)

- 6.3.6 PCI Pharma Services

- 6.3.7 World Courier

- 6.3.8 Recipharm

- 6.3.9 IQVIA

- 6.3.10 Sharp Clinical

- 6.3.11 Syneos Health

- 6.3.12 ICON plc

- 6.3.13 Biocair

- 6.3.14 Yourway

- 6.3.15 Patheon

- 6.3.16 Piramal Pharma Solutions

- 6.3.17 UDG Healthcare (Ashfield)

- 6.3.18 Myonex

- 6.3.19 Rubicon Research

- 6.3.20 Clinigen

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment