|

시장보고서

상품코드

1934889

항공기용 열교환기 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Aircraft Heat Exchanger - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

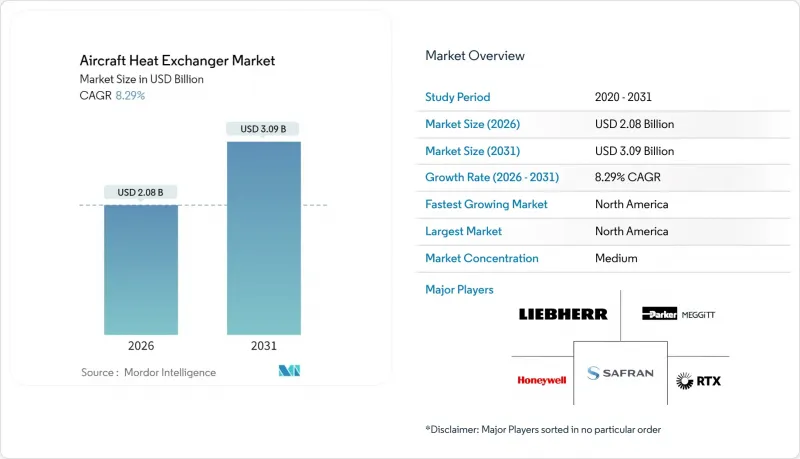

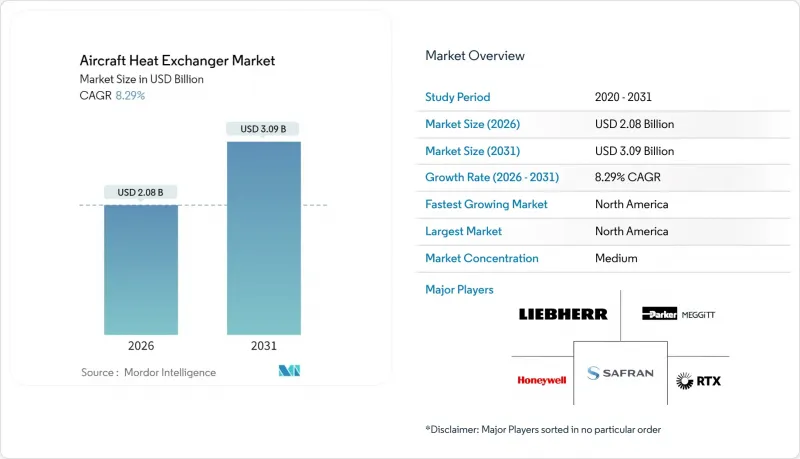

항공기용 열교환기 시장 규모는 2026년에는 20억 8,000만 달러로 추정되고 있으며, 2025년 19억 2,000만 달러에서 성장이 전망됩니다.

2031년까지의 예측에서는 30억 9,000만 달러에 달하며, 2026-2031년에 CAGR 8.29%로 확대할 전망입니다.

항공기 열교환기 시장은 기체 현대화 프로그램, 기내 공기질 규제 강화, 수소전기 및 하이브리드 추진 시스템으로의 전환으로 확대되고 있습니다. 동시에 항공사가 자산의 수명주기를 연장함에 따라 애프터마켓용 개조가 점점 더 중요해지고 있습니다. 플랫 튜브 구조는 높은 열효율과 컴팩트한 형상을 겸비하고 있으며, 무게에 민감한 단통로 제트기에 필수적이며, 채택을 촉진하고 있습니다. 엔진 시스템이 가장 큰 매출 기반을 유지하는 반면, 환경제어시스템(ECS)은 항공사가 승객의 편안함을 우선시하는 추세로 인해 가장 빠른 성장세를 보이고 있습니다. 북미는 항공우주 제조 거점이 밀집되어 있고, 국방 조달이 가속화되고 있으며, 시장 규모와 성장률에서 선도적인 위치를 차지하고 있습니다.

세계 항공기 열교환기 시장 동향 및 전망

협동체 및 리저널 제트기 생산 확대

보잉사가 2043년까지 예상하는 44,000대의 납품 기종 중 단통로 제트기가 4분의 3 이상을 차지합니다. 이로 인해 조립 라인은 계속 가동되고 있으며, 소형 열 관리 부품에 대한 수요가 증가하고 있습니다. 열교환기 공급업체는 생산 라인의 중단을 피하기 위해 생산 초기 단계에서 수년간의 블록 주문을 확보합니다. 이는 최근 물류 병목현상으로 인해 강조된 교훈입니다. 특히 플랫 튜브 코어는 높은 표면적 대 부피비가 공간 제약이 있는 나셀과 슬림라인 날개에 적합하므로 가장 큰 이점을 가지고 있습니다. 자동 진공 브레이징과 같은 첨단 제조 기술에 대한 병행 투자는 항공우주 등급의 공차를 유지하면서 생산량 증가를 지원합니다. 전반적으로 단일 통로 제트기 생산량 증가는 항공기용 열교환기 시장의 예상 CAGR을 2.1% 끌어올릴 것으로 예측됩니다.

기내 공기질 개선을 위한 전 기종 대상 ECS 개조 프로그램

팬데믹 이후 승객의 기대와 진화하는 대기질 규제로 인해 항공사들은 신규 항공기 도입을 기다리기보다 환경 제어 시스템 개조를 추진하고 있습니다. 60개 이상의 항공사가 채택하고 있는 CTT Systems의 가습 키트는 실제 운항에서 입증된 실적을 보유하고 있습니다. 개조는 일반적으로 야간 정비 점검에 통합되어 즉각적인 운영 투자 회수를 가져옵니다. 항공사들이 '웰빙' 객실의 수익화를 추진하면서 모듈식 열교환기 카트리지에 대한 관심이 높아지고 있습니다. ECS의 혁신은 습도 제어를 넘어 미립자 물질의 여과와 능동적인 기내 온도 구역 설정으로 확장되고 있으며, 이 두 가지 모두 추가적인 열 부하 분산이 필요합니다. 이러한 개조 캠페인은 항공기 열교환기 시장의 장기적인 성장에 1.8% 포인트의 기여를 할 것으로 예측됩니다.

니켈 및 알루미늄 투입 비용 변동

원자재 비용은 열교환기 비용의 최대 3분의 2를 차지하므로 관세 변동이나 상품 가격 변동을 흡수하기 어렵습니다. 2025년 3월 특정 금속에 25%의 관세가 부활함에 따라 미국내 항공우주산업의 투입비용이 상승하고 있습니다. 공급업체들은 여러 공급처 확보, 선물계약을 통한 헤지, 대체 합금 인증 대응에 대응하고 있지만, 이익률 압박은 지속되어 항공기용 열교환기 시장의 CAGR을 1.4% 낮추고 있습니다.

부문 분석

평관 설계는 우수한 표면적 이용률과 낮은 압력 손실로 엔진 및 기체 날개 부근에 콤팩트하게 설치할 수 있으며, 2025년 항공기용 열교환기 시장 점유율 64.42%를 차지할 것으로 예측됩니다. 수요는 단통로 기계 생산량에 비례하여 확대되고 있으며, 적층제조 기술을 통해 엔지니어는 튜브 형상을 최적화하여 최대 15%의 경량화를 실현할 수 있습니다. 이에 따라 연평균 8.80%의 연평균 복합 성장률(CAGR)이 예상되며, 플랫 튜브 유닛은 2031년까지 20억 5,000만 달러 규모에 도달하여 예측 기간 중 항공기용 열교환기 시장 규모의 대부분을 차지할 것으로 예측됩니다.

플레이트 핀 구조는 초고온 또는 고압 환경, 특히 경량화보다 견고성을 우선시하는 군용 플랫폼에서 여전히 필수적입니다. 실리콘 카바이드 및 흑연 폼핀 기술의 발전으로 내열 온도 범위가 1,300℃까지 확장되어 차세대 터빈 코어의 새로운 응용 분야를 개발하고 있습니다. 인증 요건이 완화됨에 따라 플레이트 핀 장비는 성장률은 낮아지지만 안정적인 출하량을 유지하며 전체 항공기용 열교환기 시장에서 틈새 시장으로서의 중요성을 유지할 것으로 예측됩니다.

고정익 프로그램은 2025년 매출의 69.72%를 차지했으며, 주로 민간 수송기와 전술 군용 제트기가 주도했습니다. 특히 연료 효율이 높은 협폭기용 수주 잔고가 크게 쌓이면서 8.97%의 연평균 복합 성장률(CAGR)을 견인했습니다. 이에 따라 2031년까지 고정익 플랫폼이 항공기용 열교환기 시장 규모의 근간을 이룰 것으로 전망됩니다. 동시에 차세대 전투기에는 고출력 항공전자 및 지향성 에너지 무기를 탑재하기 위해 냉각 용량을 두 배로 늘려야 합니다.

회전익 및 틸트로터 항공기는 유지보수 수요로 인한 안정적인 수요를 제공하지만, 무인항공기(UAV)는 가장 빠른 단위 확장을 보이고 있습니다. 방위 부대의 체류 시간이 40시간 이상으로 연장됨에 따라 경량 열교환기는 미션 크리티컬한 존재가 될 것입니다. 화물 운송 및 감시용 상용 드론도 보급되고 있지만, 도심항공모빌리티(UAM) 기단이 금세기 후반에 확대되기 전까지는 그 절대적인 매출 기여도는 여전히 미미할 것으로 보입니다.

지역별 분석

북미는 설계, 생산 및 유지보수 활동에서 타의 추종을 불허하는 규모를 자랑하며, 공급업체는 개발 비용을 민간 및 군사 프로그램에 분산하여 상각할 수 있습니다. 차세대 전투기 및 무인시스템에 대한 정부 계약이 장기적인 수요를 창출하는 반면, 민간 OEM(Original Equipment Manufacturer)는 중요한 열교환 코어를 조달하기 위해 국내 주조소 및 적층제조국에 의존하고 있습니다. 관세로 인한 금속 비용 급등으로 단기적인 비용 압박이 가중되고 있지만, 공급망 현지화 정책이 이러한 역풍을 일부 상쇄하고 있습니다.

유럽은 에어버스의 와이드바디 항공기 수주잔고와 지속가능한 항공 기술 분야의 리더십을 활용하고 있습니다. 리프헬 에어버스사의 전기식 ECS(전기식 환경제어시스템) 등 공동연구를 통해 유럽 공급업체들은 블리드리스 구조에서 선점 우위를 점하고 있습니다. 사프란과 HAL(인도 항공기 제작사) 또는 에어 리퀴드(Air Liquide)와의 제휴는 단조 부품 및 수소 기술 전문 지식에 대한 접근성을 확대하여 미국에 비해 상대적으로 낮은 방위비 지출에도 불구하고 견고한 중기적 성장을 지원하고 있습니다.

아시아태평양의 성장은 기체 증강과 현지화 정책에 기인합니다. 인도의 MRO 사업자는 공장 용량을 확장하고 열교환기 정비가 필요한 GTF 및 LEAP 엔진의 오버홀 작업을 수주하고 있습니다. 중국 OEM 업체들은 국산 엔진 프로그램을 지원하기 위해 초합금 가공 기술에 투자하여 유럽과 미국 공급망에 대한 의존도를 점차 줄여나가고 있습니다. 평균 판매가격은 유럽과 미국 시장보다 낮지만, 물량 확대가 8.9% 이상의 지역 매출 성장을 촉진하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

Aircraft heat exchanger market size in 2026 is estimated at USD 2.08 billion, growing from 2025 value of USD 1.92 billion with 2031 projections showing USD 3.09 billion, growing at 8.29% CAGR over 2026-2031.

Fleet modernization programs, stricter cabin-air quality regulations, and a shift toward hydrogen-electric and hybrid propulsion are expanding the aircraft heat exchanger market. At the same time, aftermarket retrofits are gaining prominence as airlines extend the life cycles of their assets. The flat-tube architecture facilitates adoption because it pairs high thermal efficiency with compact form factors, which are essential for weight-sensitive single-aisle jets. Engine systems maintain the largest revenue base, yet environmental control systems (ECS) show the fastest growth as carriers prioritize passenger well-being. North America dominates in terms of value and growth due to its dense aerospace manufacturing base and accelerating defense procurement.

Global Aircraft Heat Exchanger Market Trends and Insights

Ramp-up in narrowbody and regional jet production

Single-aisle jets comprise over three-quarters of the 44,000 aircraft deliveries Boeing foresees by 2043, keeping assembly lines busy and lifting demand for compact thermal-management components. Heat exchanger suppliers secure multiyear block orders early in production to avoid line stoppages, a lesson underscored by recent logistics bottlenecks. Flat-tube cores benefit most because their high surface-area-to-volume ratio suits space-constrained nacelles and slimline wings. Parallel investment in advanced manufacturing, such as automated vacuum brazing, supports higher output without compromising aerospace-grade tolerances. Overall, rising single-aisle throughput adds 2.1 percentage points to the forecast CAGR for the aircraft heat exchanger market.

Fleet-wide ECS retrofit programs for cabin air quality

Post-pandemic passenger expectations and evolving air-quality mandates spur carriers to retrofit environmental control systems rather than wait for new aircraft slots. CTT Systems' humidification kits, used by more than 60 airlines, demonstrate real-world traction. Retrofits typically integrate into overnight maintenance checks, generating immediate operational payback and increasing interest in modular heat-exchanger cartridges as airlines monetize "well-being" cabins. ECS innovation extends beyond humidity control to particulate filtration and active cabin-temperature zoning, each requiring additional heat load dissipation. These retrofit campaigns add 1.8 percentage points to long-term growth for the aircraft heat exchanger market.

Nickel and aluminium input-cost volatility

Raw materials account for up to two-thirds of the heat exchanger's cost, making it challenging to absorb tariff swings and commodity price fluctuations. The 25% tariff restored on certain metals in March 2025 elevates aerospace input prices in the US. Suppliers respond by dual-sourcing, hedging futures contracts, and qualifying alternative alloys; yet, margin pressure persists, trimming 1.4 percentage points off the aircraft heat exchanger market's CAGR.

Other drivers and restraints analyzed in the detailed report include:

- Shift to high-temperature ceramic HX materials

- Hydrogen-electric propulsion waste-heat recovery

- Qualification bottlenecks for new HX designs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Flat tube designs captured 64.42% of the aircraft heat exchanger market share in 2025, thanks to their superior surface area utilization and low pressure drop, which enables compact installations near engines and aircraft wings. Demand scales with single-aisle production, while additive manufacturing allows engineers to refine tube geometry, resulting in a mass reduction of up to 15%. The resulting 8.80% CAGR positions flat-tube units to reach USD 2.05 billion by 2031, accounting for most of the aircraft heat exchanger market size during the forecast period.

Plate-fin configurations remain indispensable for ultra-high-temperature or high-pressure environments, particularly on military platforms prioritizing robustness over minimal weight. Advances in silicon-carbide and graphite-foam fins extend their service window to 1,300 °C, opening new applications in next-generation turbine cores. As qualification hurdles are cleared, plate-fin devices are expected to maintain steady volumes, albeit at lower growth rates, retaining niche relevance in the broader aircraft heat exchanger market.

Fixed-wing programs accounted for 69.72% of 2025 revenue, primarily driven by commercial transports and tactical military jets. Substantial order backlogs, especially for fuel-efficient narrowbody models, propel a 8.97% CAGR, keeping fixed-wing platforms the anchor of the aircraft heat exchanger market size through 2031. Concurrently, next-generation fighters require a doubling of cooling capacity to support high-power avionics and directed-energy payloads.

Rotorcraft and tiltrotors provide steady, maintenance-driven demand, yet unmanned aerial vehicles (UAVs) show the fastest unit expansion. As defence forces extend loiter times beyond 40 hours, lightweight exchangers become mission-critical. Commercial drones for cargo and surveillance are also gaining traction; however, their absolute revenue contribution remains modest until urban air mobility (UAM) fleets scale up later in the decade.

The Aircraft Heat Exchanger Market Report is Segmented by Type (Plate-Fin and Flat Tube), Platform (Fixed-Wing Aircraft, Rotary-Wing Aircraft, and More), Application (Environmental Control Systems, Engine Systems, Electronic Pod Cooling, and Hydraulic Cooling), Vendor (OEM and Aftermarket), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America enjoys unmatched scale in design, production, and sustainment activities, allowing suppliers to amortise development spending across civil and military programs. Government contracts for next-generation fighters and unmanned systems generate long-cycle demand, while commercial OEMs rely on domestic foundries and additive manufacturing bureaus for critical heat-transfer cores. Tariff-driven metal cost spikes raise near-term cost pressure, yet supply-chain localization initiatives partly offset this headwind.

Europe leverages Airbus's widebody backlog and leadership in sustainable aviation technology. Collaborative research, such as Liebherr-Airbus' electrical ECS, gives European suppliers an early mover advantage in bleed-less architectures. Partnerships between Safran and HAL, or Air Liquide, widen access to forged parts and hydrogen expertise, supporting robust mid-term growth despite comparatively lower defense outlays than those of the US.

Asia-Pacific region's rise stems from fleet expansion and localization policies. Indian MRO providers scale shop capacity, attracting GTF and LEAP engine overhauls that demand exchanger servicing. Chinese OEMs are investing in superalloy processing to support their indigenous engine programs, thereby gradually reducing their reliance on Western supply chains. While average selling prices are lower than in Western markets, volume expansion continues to drive regional revenue growth above 8.9%.

- Safran SA

- TAT Technologies Ltd.

- Honeywell International Inc.

- Parker-Hannifin Corporation

- Triumph Group, Inc.

- Wall Colmonoy Corporation

- Boyd Corporation

- THERMOVAC Aerospace Pvt. Ltd.

- AMETEK, Inc.

- RTX Corporation

- Unison Industries, LLC

- Intergalactic (General Electric Company)

- Sumitomo Precision Products Co., Ltd.

- Morpheus Designs

- Turbotec Products, Inc.

- Liebherr Group

- JAMCO Corporation

- Parfuse Corporation

- Signia Aerospace

- Sintavia, LLC

- Airmark Components

- Conflux Technology Pty Ltd.

- AddUp SAS

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Ramp-up in narrowbody and regional jet production

- 4.2.2 Fleet-wide ECS retrofit programs for cabin air-quality

- 4.2.3 Shift to high-temperature ceramic HX materials

- 4.2.4 Hydrogen-electric propulsion waste-heat recovery

- 4.2.5 Additive-manufactured micro-channel cores

- 4.2.6 Defense UAV endurance-extension initiatives

- 4.3 Market Restraints

- 4.3.1 Nickel and aluminum input-cost volatility

- 4.3.2 Qualification bottlenecks for new HX designs

- 4.3.3 Supply-chain consolidation raising OEM dependency

- 4.3.4 Weight-penalties versus integrated thermal-management

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Plate-Fin

- 5.1.2 Flat Tube

- 5.2 By Platform

- 5.2.1 Fixed-Wing Aircraft

- 5.2.2 Rotary-Wing Aircraft

- 5.2.3 Unmanned Aerial Vehicles

- 5.3 By Application

- 5.3.1 Environmental Control Systems

- 5.3.2 Engine Systems (Oil/Fuel/Air)

- 5.3.3 Electronic Pod Cooling

- 5.3.4 Hydraulic Cooling

- 5.4 By Vendor

- 5.4.1 Original Equipment Manufacturer (OEM)

- 5.4.2 Aftermarket

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 France

- 5.5.2.3 Germany

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Safran SA

- 6.4.2 TAT Technologies Ltd.

- 6.4.3 Honeywell International Inc.

- 6.4.4 Parker-Hannifin Corporation

- 6.4.5 Triumph Group, Inc.

- 6.4.6 Wall Colmonoy Corporation

- 6.4.7 Boyd Corporation

- 6.4.8 THERMOVAC Aerospace Pvt. Ltd.

- 6.4.9 AMETEK, Inc.

- 6.4.10 RTX Corporation

- 6.4.11 Unison Industries, LLC

- 6.4.12 Intergalactic (General Electric Company)

- 6.4.13 Sumitomo Precision Products Co., Ltd.

- 6.4.14 Morpheus Designs

- 6.4.15 Turbotec Products, Inc.

- 6.4.16 Liebherr Group

- 6.4.17 JAMCO Corporation

- 6.4.18 Parfuse Corporation

- 6.4.19 Signia Aerospace

- 6.4.20 Sintavia, LLC

- 6.4.21 Airmark Components

- 6.4.22 Conflux Technology Pty Ltd.

- 6.4.23 AddUp SAS

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment