|

시장보고서

상품코드

1939637

슬리밍 에이드 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Slimming Aids - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

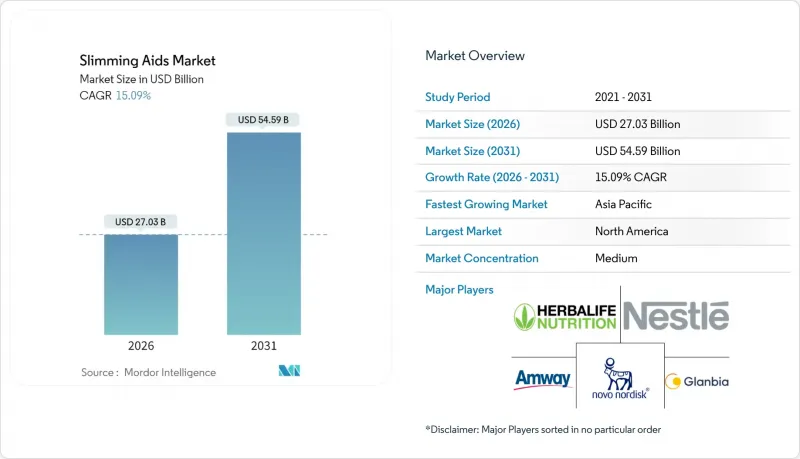

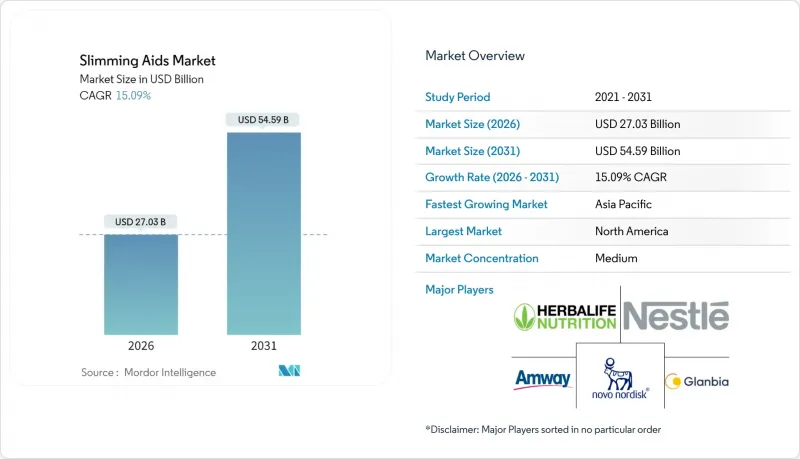

슬리밍 에이드 시장은 2025년에 234억 9,000만 달러로 평가되며, 2026년 270억 3,000만 달러에서 2031년까지 545억 9,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 15.09%로 예상됩니다.

두 자릿수 성장이 지속되는 배경에는 비만이 미용 문제에서 만성질환으로 자리매김한 점, 차세대 GLP-1 약물의 빠른 승인 주기, 신흥 국가의 가처분 소득 증가 등을 꼽을 수 있습니다. 세마글루타이드와 틸제파타이드의 강력한 심혈관계 결과 데이터는 보험 적용 범위를 확대하고, 원격의료 플랫폼은 처방 경로를 단축하고 복약 순응도를 향상시키고 있습니다. 동시에 피트니스 생태계는 웨어러블 및 커넥티드 기기를 통합하여 약물 치료와 경쟁하는 것이 아니라 보완하는 형태로 발전하고 있습니다. 식이요법 및 보충제 분야의 기존 기업이 주사 요법의 임상적 효과에 대응하기 위해 제품 포트폴리오를 재검토하면서 경쟁 압력이 심화되고 있습니다.

세계 슬리밍 보조제 시장 동향 및 인사이트

전 세계 비만 유병률 증가

성인 비만 - 2022년 8명 중 1명이 비만인 것으로 나타났습니다. 예측에 따르면 2050년까지 38억 명의 성인이 과체중 또는 비만이 될 것으로 예상되며, 이는 경기 사이클과 관계없이 지속되는 구조적 수요 요인을 강조하고 있습니다. 의료 시스템은 현재 비만을 장기적인 약물 치료가 필요한 만성질환으로 인식하고 있으며, 이로 인해 상환 경로가 확보되어 미용 목적의 사용자를 넘어 슬리밍 보조제 시장이 확대되고 있습니다. 2030년까지 연간 3조 달러로 추산되는 비용 부담은 초기 단계의 개입에 대한 정치적 긴급성을 만들어내고, 항비만 치료제의 추가 제도화를 촉진하고 있습니다. 이러한 역학적 배경은 케어 연속선상에 있는 혁신가 및 소매업체들에게 다년간의 가시성을 확보할 수 있는 기회를 제공합니다.

신흥 시장의 가처분소득 증가

아시아태평양의 구매력 증가는 프리미엄 체중 감량 솔루션에 대한 새로운 수요로 이어지고 있습니다. 인도 국내 체중 관리 시장은 2022년 172,000 루피(206억 달러) 규모이며, 2028년까지 315,000 루피(378억 달러)에 달할 것으로 예측됩니다. 중국 업체들은 저렴한 가격과 효능을 겸비한 GLP-1 바이오시밀러의 양산을 추진하고 있으며, 규제 당국의 승인 획득 후 수출 시장에서의 가격 인하가 예상됩니다. 도시화와 좌식 생활습관이 비만 발생률을 높이는 반면, 인도의 생산연동형 장려금 제도 등 정부 정책은 현지 생산비용을 낮추고 공급 안정성을 향상시키고 있습니다. 이러한 복합적인 요인으로 인해 기존에 저효능 한약에 의존하던 중산층 소비자층이 해방되어 정규 의료 분야로의 침투가 가속화되고 있습니다.

체중 감량 약물의 안전성 문제와 부작용

3개 대륙에서 위조 세마글루타이드가 경고된 사실은 고가 주사제의 병행수입 위험을 강조하고 있습니다. 췌장염, 갑상선 종양, 중증 저혈당증에 대한 블랙박스 경고는 여전히 처방 정보에서 중요한 위치를 차지하고 있습니다. 연구에 따르면 초기 제지방 체중 감소의 최대 30%는 근육으로, 임상의들은 장기적인 유지를 위해 저항 훈련과 단백질 보충을 권장하고 있습니다. Z세대의 회의적인 태도가 두드러져 57.5%가 약물 치료보다 생활습관 개선을 선호하고 있으며, 이러한 경향은 소셜미디어를 통해 확산되는 경험담으로 더욱 강화되고 있습니다. 이러한 인식은 도입 지연과 중단율 상승을 초래하여 단기적인 판매량 증가를 억제할 수 있습니다.

부문 분석

2025년 기준, 다이어트 보조제는 슬리밍 보조제 시장 점유율의 36.74%를 차지하며, 소매 유통에 대한 정착도와 규제 장벽이 낮다는 것을 보여줍니다. 그러나 소비자들이 GLP-1 요법과 운동을 결합한 종합적인 헬스케어법으로 전환함에 따라 이 부문의 CAGR은 기기 붐에 비해 뒤쳐지고 있습니다. 펠로톤의 커넥티드 러닝머신 사이클은 전년 대비 42%의 매출 성장을 기록하며 체중 감량을 돕는 고급 하드웨어에 대한 높은 수요를 보여주었습니다. 피트니스 기기 슬리밍 보조 시장 규모는 2031년까지 연평균 복합 성장률(CAGR) 15.48%로 확대될 것으로 예상되며, 웨어러블 기기 시장 전체가 포화상태인 가운데 새로운 수입원이 창출될 가능성을 시사하고 있습니다.

이눌린, 베르베린 등 임상적으로 효능이 확인된 유효 성분을 채택하여 의약품 수준의 효능을 표방하는 건강기능식품 브랜드가 있습니다. 스마트 체중계, 칼로리 관리 앱과의 크로스 프로모션을 통해 소비자 데이터를 수집하고, 개인별 맞춤 섭취량 제안을 통해 부가가치를 높이고 있습니다. 한편, 식사대용식은 분량 조절이 가능한 편의성으로 점유율을 유지하고 있지만, GLP-1 사용자들이 식욕억제 효과를 체감하면서 자사 제품과 경쟁에 직면하고 있습니다. 제조업체는 제지방 체중 감소를 상쇄하는 고단백질 배합으로 차별화를 꾀하고 판매량 감소를 억제하는 전략적 전환을 추진하고 있습니다.

천연 및 반합성 부문은 고유한 가치 제안으로 슬리밍 보조제 시장을 보완합니다. 허브 추출물, 식물 유래 성분, 유기 화합물로 구성된 자연주의 부문은 부작용을 최소화한 종합적인 체중 관리 솔루션을 원하는 소비자들에게 선호되고 있습니다. 이 카테고리의 제품에는 녹차 추출물, 가르시니아 캄보지아, 각종 식물 추출물 등이 자주 포함됩니다. 반합성 부문은 천연 성분과 합성 화합물을 결합하여 효과를 높이면서도 상대적으로 안전성을 유지하는 균형 잡힌 접근 방식을 제공하여 천연 제품과 합성 제품 사이의 간극을 메우고 있습니다. 이 부문은 체중 조절에 있으며, 천연 성분과 합성 성분의 장점을 모두 원하는 소비자들에게 특히 선호되고 있습니다.

세계 슬리밍 보조제 시장은 제품 유형(천연, 합성, 반합성), 복용 형태(정제, 캡슐, 분말, 시럽, 기타), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)으로 분류됩니다. 이 보고서에서는 위 부문 시장 규모(단위: 백만 달러)를 제공합니다.

지역별 분석

북미는 높은 비만 유병률과 GLP-1의 조기 도입으로 2025년 슬리밍 보조제 시장 매출의 41.87%를 차지할 것으로 예측됩니다. 미국에서는 강력한 심혈관 데이터에 따라 보험사의 항비만제에 대한 보험금 지급이 증가하고 있습니다. 한편, 캐나다의 단일 보험자 제도에서는 GLP-1 제제가 만성질환 치료 경로에 포함되어 있습니다. LillyDirect와 같은 소비자 직접 판매 모델은 2일 배송을 통해 유통을 효율화하고 복약 순응도를 높이고 있습니다.

아시아태평양은 CAGR 16.63%로 가장 빠르게 성장하고 있으며, 중산층 인구 증가와 적극적인 정부 정책으로 인해 가장 빠르게 성장하고 있습니다. 인도는 소득 증가와 높은 미충족 수요가 결합된 좋은 사례로, 2028년까지 슬리밍 보조제 시장 규모가 2배 이상 증가할 것으로 예측됩니다. 중국 바이오시밀러 업체들은 가격 압축과 판매량 확대를 추진할 것으로 보입니다.

유럽은 EMA(유럽의약품청)의 엄격한 모니터링을 통한 치료 안전성 검증으로 프리미엄 시장 지위를 유지하고 있습니다. 독일 건강보험 재단은 성과연동형 상환을 시범 도입하고 있으며, 영국은 브렉시트 이후 공급 물류에 대응하고 있습니다. 남미와 중동 및 아프리카은 점유율은 작지만, 의료 접근성 개선과 가격 압력 완화로 장기적인 성장 잠재력을 가지고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 지원(3개월)

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측(금액)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSA 26.03.06The Slimming aids market was valued at USD 23.49 billion in 2025 and estimated to grow from USD 27.03 billion in 2026 to reach USD 54.59 billion by 2031, at a CAGR of 15.09% during the forecast period (2026-2031).

Consistent double-digit growth reflects the repositioning of obesity from a cosmetic issue to a chronic disease, the rapid approval cycle for next-generation GLP-1 drugs, and rising disposable incomes in emerging economies. Strong cardiovascular outcome data for semaglutide and tirzepatide is broadening payer coverage, while telehealth platforms shorten the prescription pathway and lift adherence rates. At the same time, the fitness ecosystem is integrating wearables and connected equipment that complement pharmacotherapy rather than compete with it. Competitive pressure is intense as incumbents in meal plans and supplements overhaul their portfolios to counter the clinical efficacy of injectable therapies.

Global Slimming Aids Market Trends and Insights

Rising Global Obesity Prevalence

Adult obesity - 1 in 8 people lived with obesity in 2022. Forecasts indicate 3.80 billion adults could be overweight or obese by 2050, underscoring a structural demand driver that persists regardless of economic cycles. Healthcare systems now frame obesity as a chronic disease requiring long-term pharmacotherapy, which secures reimbursement pathways and expands the Slimming aids market beyond cosmetic users. The estimated USD 3 trillion annual cost burden projected for 2030 places political urgency on early-stage intervention, further institutionalizing anti-obesity therapeutics. This epidemiological backdrop cements multiyear visibility for innovators and retailers positioned across the continuum of care.

Growing Disposable Incomes in Emerging Markets

Rising purchasing power in Asia-Pacific translates into new demand for premium slimming solutions. India's domestic weight-management sector was INR 172,000 crore (USD 20.6 billion) in 2022 and is tracking toward INR 315,000 crore (USD 37.8 billion) by 2028. Chinese manufacturers are scaling GLP-1 biosimilars that promise affordability as well as efficacy, a move that will likely compress prices in export markets once regulatory clearances are secured. Urbanization and sedentary lifestyles raise obesity incidence, while government incentives such as India's Production Linked Incentive scheme lower local production costs and improve supply security. These combined factors unlock a sizable middle-class consumer base that previously relied on lower-efficacy herbal remedies, accelerating formal sector penetration.

Safety Concerns & Side-Effects of Weight-Loss Drugs

Warnings about counterfeit semaglutide in three continents underscore the parallel-trade risk for high-value injectables. Black-box cautions for pancreatitis, thyroid tumors and severe hypoglycemia remain prominent on prescribing information. Studies show up to 30% of initial lean-mass loss is muscle, prompting clinicians to recommend resistance training and protein supplementation for long-term maintenance. Gen Z skepticism is notable: 57.5% prefer lifestyle modification over medication, a sentiment amplified by viral social-media anecdotes. These perceptions may delay uptake or increase discontinuation rates, trimming near-term volume growth.

Other drivers and restraints analyzed in the detailed report include:

- Launch of Next-Gen GLP-1 Drugs

- Telehealth-Centred Prescription Models

- High Therapy Cost

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Dietary supplements captured 36.74% of the Slimming aids market share in 2025, underscoring the category's entrenched retail penetration and low regulatory hurdles. However, the segment's CAGR trails the equipment boom as consumers pivot toward holistic regimens that pair GLP-1 therapy with exercise. Connected treadmills and cycles posted 42% year-over-year revenue growth at Peloton, illustrating appetite for premium hardware that supports weight-loss accountability. The Slimming aids market size for fitness equipment is forecast to expand at 15.48% CAGR to 2031, suggesting incremental revenue pools even as the broader wearables category saturates.

Supplement brands respond with clinically-validated actives such as inulin and berberine, aiming to align efficacy narratives with pharmaceutical standards. Cross-promotion with smart scales and calorie-tracking apps furnishes consumer data that informs personalized dosages, enhancing perceived value. Meanwhile, meal replacements defend share via portion-controlled convenience but face cannibalization as GLP-1 users experience appetite suppression. Manufacturers differentiate through protein-dense formulations to offset lean-mass losses, a strategic pivot that tempers volume erosion.

The natural and semi-synthetic segments complement the slimming aids market with their unique value propositions. The natural segment, comprising herbal extracts, plant-based ingredients, and organic compounds, appeals to consumers seeking holistic weight management solutions with minimal side effects. Products in this category often include ingredients like green tea extracts, garcinia cambogia, and various botanical extracts. The semi-synthetic segment bridges the gap between natural and synthetic products, offering a balanced approach by combining natural ingredients with synthetic compounds to enhance efficacy while maintaining a relatively favorable safety profile. This segment particularly appeals to consumers who seek the benefits of both natural and synthetic ingredients in their weight management journey.

Global Slimming Aids Market is Segmented by Product Type (Natural, Synthetic, Semi-Synthetic), Mode of Consumption (Tablets, Capsules, Powder, Syrups, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East, and Africa, and South America). The Report Offers the Value (in USD Million) for the Above Segments.

Geography Analysis

North America generated 41.87% of Slimming aids market revenue in 2025 on the back of high obesity prevalence and early GLP-1 adoption. U.S. payers increasingly reimburse anti-obesity drugs following strong cardiovascular data, while Canadian single-payer systems integrate GLP-1s into chronic-disease pathways. Direct-to-consumer models, such as LillyDirect, streamline distribution and bolster adherence through two-day delivery.

Asia-Pacific is the fastest-growing region at 16.63% CAGR, propelled by expanding middle-class populations and proactive government policies. India exemplifies the convergence of rising income and high unmet medical need, with the Slimming aids market size projected to more than double by 2028. Chinese biosimilar entrants will likely compress prices and catalyze volume expansion.

Europe maintains a premium positioning with rigorous EMA oversight that validates therapeutic safety. German sickness funds pilot outcome-based reimbursements, while the U.K. navigates post-Brexit supply logistics. South America and the Middle East & Africa contribute smaller shares but hold long-run optionality as healthcare access improves and pricing pressure eases.

- Herbalife Ltd.

- WW International Inc.

- Novo Nordisk

- Eli Lilly and Company

- Simply Good Foods Co.

- GlaxoSmithKline

- Roche

- Amway Corp.

- Nestle S.A.

- Unilever PLC

- Peloton Interactive Inc.

- Johnson Health Tech Co. Ltd.

- Slimming World Group Ltd.

- GNC Holdings LLC

- FANCL Corp.

- Abbott Laboratories

- Bayer

- Nestle Health Science S.A.

- Abbott Nutrition Manufacturing Inc.

- Aurobindo Pharma Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising global obesity prevalence

- 4.2.2 Growing disposable incomes in emerging markets

- 4.2.3 Launch of next-gen GLP-1 drugs

- 4.2.4 Telehealth-centred prescription models

- 4.2.5 Corporate weight-management benefit schemes

- 4.2.6 Microbiome-targeted slimming products

- 4.3 Market Restraints

- 4.3.1 Safety concerns & side-effects of weight-loss drugs

- 4.3.2 High therapy cost

- 4.3.3 Social-media-driven fad-diet backlash

- 4.3.4 API supply bottlenecks for semaglutide family

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD Bn)

- 5.1 By Product Type

- 5.1.1 Dietary Supplements

- 5.1.2 Meal Replacements

- 5.1.3 Pharmeuticals (RX and OTC)

- 5.1.4 Fitness Equipment

- 5.2 By End User

- 5.2.1 Women

- 5.2.2 Men

- 5.2.3 Children & Adolescents

- 5.3 By source

- 5.3.1 Natural

- 5.3.2 synthetic

- 5.3.3 Semi-synthetic

- 5.4 By Distribution Channel

- 5.4.1 Online Retail

- 5.4.2 Pharmacies & Drug Stores

- 5.4.3 Hypermarkets / Supermarkets

- 5.4.4 Weight-Management Clinics

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 GCC

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)}

- 6.3.1 Herbalife Ltd.

- 6.3.2 WW International Inc.

- 6.3.3 Novo Nordisk A/S

- 6.3.4 Eli Lilly and Company

- 6.3.5 Simply Good Foods Co.

- 6.3.6 GlaxoSmithKline plc

- 6.3.7 Hoffmann-La Roche AG

- 6.3.8 Amway Corp.

- 6.3.9 Nestle S.A.

- 6.3.10 Unilever PLC

- 6.3.11 Peloton Interactive Inc.

- 6.3.12 Johnson Health Tech Co. Ltd.

- 6.3.13 Slimming World Group Ltd.

- 6.3.14 GNC Holdings LLC

- 6.3.15 FANCL Corp.

- 6.3.16 Abbott Laboratories

- 6.3.17 Bayer AG

- 6.3.18 Nestle Health Science S.A.

- 6.3.19 Abbott Nutrition Manufacturing Inc.

- 6.3.20 Aurobindo Pharma Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment