|

시장보고서

상품코드

1939745

아시아태평양의 계약 물류 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Asia-Pacific Contract Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

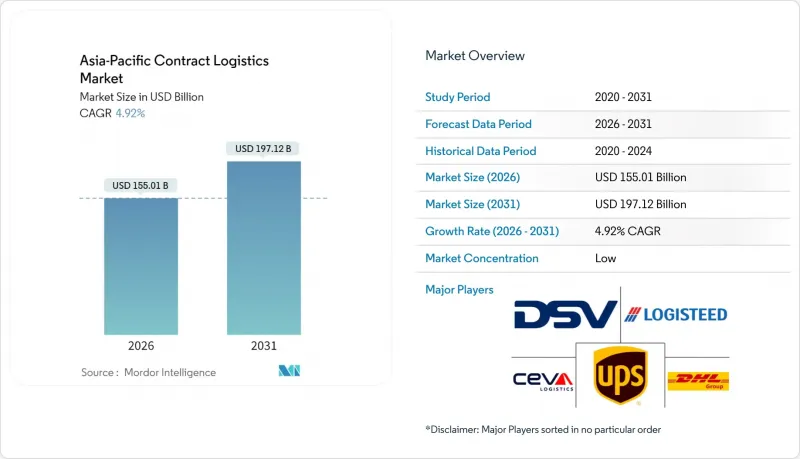

아시아태평양의 계약 물류 시장 규모는 2026년에 1,550억 1,000만 달러로 추정됩니다.

이는 2025년 1,477억 4,000만 달러에서 성장한 수치이며, 2031년에는 1,971억 2,000만 달러에 달할 것으로 예상됩니다. 2026년부터 2031년까지 연평균 성장률(CAGR)은 4.92%로 예측됩니다.

현재 아시아태평양의 계약 물류 시장 규모는 아시아태평양이 아웃소싱 가치사슬 관리의 세계 중심지로서의 역할을 반영하고 있으며, 예상 CAGR은 화주들이 풀필먼트 네트워크를 현대화하고 부가가치 서비스를 확대함에 따라 지속적인 성장세를 보일 것으로 예상하고 있습니다. 급속한 E-Commerce의 확대, 대규모 니어쇼어링 및 리쇼어링, 도로, 철도, 항만, 디지털 인프라에 대한 정부의 대규모 투자로 인해 제조업, 소매업, 의료 분야에서의 계약 물류 도입이 가속화되고 있습니다. 네트워크 설계, 자동화, 데이터 플랫폼을 통합한 장기적인 파트너십이 단기적인 거래형 계약을 대체하고 있으며, 이를 통해 공급업체는 인력 및 부동산이 부족한 환경에서도 강력한 공급 능력을 제공할 수 있습니다. 혼잡한 남중국해 항로의 해상 보험료 상승과 온도 관리가 필요한 운송 경로의 지속적인 콜드체인 병목현상은 복잡성을 증가시키지만, 엄격한 품질 관리와 국경 간 규정 준수를 실현할 수 있는 공급자에게는 수익성이 높은 틈새 시장을 창출하고 있습니다.

아시아태평양의 계약 물류 시장 동향과 인사이트

아시아태평양의 폭발적인 이커머스 활성화

디지털 커머스의 성장은 아시아태평양의 계약 물류 시장에서 풀필먼트 경제를 재정의하고 있습니다. 온라인 판매 속도는 브랜드에 옴니채널 재고 배분, 마이크로 풀필먼트 거점, 전용 리버스 물류 루프를 채택하도록 강요하고 있으며, 이는 대부분의 사내 네트워크가 감당할 수 없는 수준입니다. 인도네시아와 베트남의 경우, 연간 온라인 판매 성장률이 오프라인 매장 성장률을 훨씬 상회하고 있어, 창고 개발자들은 피킹 및 포장 자동화를 위한 메자닌 층과 고급 식료품용 온도 관리 셀을 추가해야 하는 상황에 처해 있습니다. 지역별로 반품률이 15-30%에 달하는 경우가 많으며, 계약 물류 제공업체는 현재 재생 라인, 재포장 스테이션, 실시간 시각화 대시보드를 통합 제안에 포함시켜 대응하고 있습니다.

공급망 니어쇼어링/리쇼어링('중국+1' 전략)

다국적 기업들은 지정학적 위험 분산과 총착륙 비용 절감을 위해 부품 조달과 최종 조립을 동남아시아나 인도로 재배치하고 있습니다. 베트남 북부 경제권이나 인도네시아 바탄 공단 등 새로운 생산 거점에서는 원자재 반입 전처리, 저스트 인 시퀀스 생산 라인 공급, 수출 화물의 집적화가 요구되고 있으며, 기존 제공업체는 여러 국가를 아우르는 컨트롤 타워에서 이를 제공할 수 있습니다. 듀얼 소싱 전략은 중국 내외의 공장을 넘나드는 가시성을 요구하며, 화주는 운송 계획, 마일스톤 관리, 공급업체 관리 재고를 물류 전문업체에 위탁하는 경향이 있습니다. 인도의 생산연계형 인센티브 제도, 인도네시아의 옴니버스법 등 정부 정책으로 공장 이전이 가속화되고 새로운 물류회랑이 성숙해짐에 따라 아시아태평양의 계약 물류 시장은 중기적으로 성장할 것으로 보입니다.

주요 거점의 부동산 및 인건비 상승

2024년 싱가포르, 홍콩, 도쿄에서는 토지 공급의 제약과 데이터센터 사업자의 경쟁적 수요로 인해 프라임급 창고 임대료가 급등했습니다. 동시에 호주와 한국에서는 지게차 운전자와 피킹 작업자의 기본 임금이 두 자릿수 상승하여 대량 처리 업무의 수익률을 압박하고 있습니다. 계약 물류 사업자들은 상품 운반 로봇, 자동 팔레타이저, 에너지 절약형 공조 시스템 등을 통해 이러한 압력을 완화하고 있지만, 이러한 장비 업데이트에는 많은 자본 지출과 장기간의 회수 기간이 필요합니다. 이러한 경제 상황은 조호르바루, 치바 등 저비용 위성도시를 거점으로 하는 허브 앤 스포크 네트워크를 촉진하고 있지만, 대도시 지역의 라스트 마일 마감시간은 여전히 문제이며, 서비스 수준 계약이 엄격해지고 단기적인 요금 인상이 제한되고 있습니다.

부문 분석

아시아태평양의 계약 물류 시장에서 운송 부문은 2025년 매출의 62.55%를 차지할 것으로 예상됩니다. 이는 중국의 촘촘한 도로 교통망과 인도네시아의 광활한 국내 해상 항로망을 기반으로 하고 있습니다. 공급자는 분절된 지역 조건에서 비용과 속도의 균형을 맞추기 위해 장거리 트럭 운송, 철도 셔틀, 근해 피더 항로를 연계하여 운영하고 있습니다. 한편, 부가가치 서비스는 제조업체들이 지역 유통센터 내 지연 배송 대응, 키트 조립, 간이 조립 능력을 요구함에 따라 2031년까지 4.03%의 가장 높은 CAGR을 기록할 것으로 예측됩니다. 가전제품의 표시 규제가 복잡해지는 가운데, 계약 물류 사업자는 현지에 인쇄-부착 라인 설치를 추진. 한편, 패션 브랜드는 창고 내 봉제 셀을 활용하여 사이즈 조정을 빠르게함으로써 판매율을 높이고 있습니다. 이러한 변화로 인해 수익률이 확대되고, 변동이 심한 간선 운임에 대한 의존도가 낮아졌습니다. 아시아태평양의 계약 물류 시장 규모는 고부가가치 분야에서 구조적 확장을 강화하고 있습니다.

창고 및 유통 업무는 여전히 핵심이며, EC 소포 물량 및 옴니채널 재고 전략과 연동하여 확대되고 있습니다. 고밀도 셔틀 시스템은 도심 매립형 부지의 설치 면적을 줄이고, 항만 인근의 교차 도킹 레이아웃은 온도 관리가 필요한 농산물의 체류 시간을 단축시킵니다. 선진 사업자들은 창고 관리 시스템과 실시간 운송 가시성 플랫폼을 연동하여 예측 도착 시간대 파악 및 예외 알림을 통해 고객 경험을 개선하고 있습니다. 항공화물 포워딩의 취급량도 마찬가지로 증가하고 있으며, 고부가가치 소량화물 및 생물학적 제제를 위한 직접 주입 모델은 출발지부터 최종 배송지까지 멀티모달 관리가 요구되어 아시아태평양의 계약 물류 시장 전체의 성장을 뒷받침하고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

제8장 부록

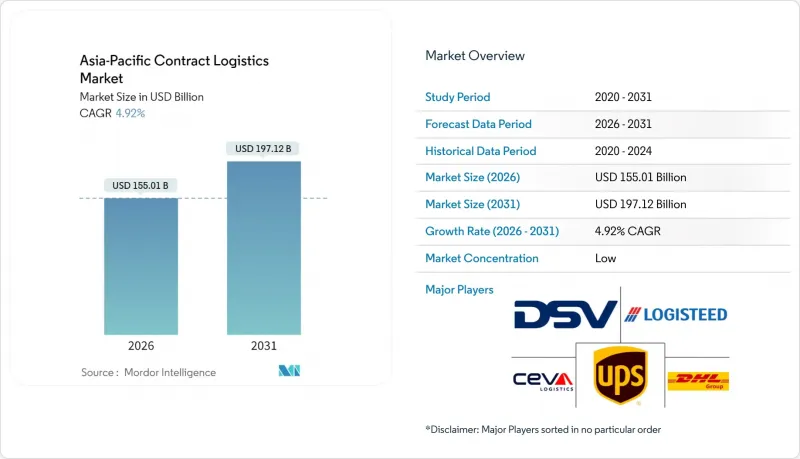

KSM 26.03.09Asia-Pacific Contract Logistics Market size in 2026 is estimated at USD 155.01 billion, growing from 2025 value of USD 147.74 billion with 2031 projections showing USD 197.12 billion, growing at 4.92% CAGR over 2026-2031.

The current Asia-Pacific Contract Logistics market size reflects the region's role as the global center for outsourced supply-chain management, and the forecast CAGR points to sustained momentum as shippers modernize fulfillment networks and extend value-added services. Rapid e-commerce expansion, large-scale near- and re-shoring, and government mega-investments in road, rail, port, and digital infrastructure are accelerating contract-logistics adoption across manufacturing, retail, and healthcare sectors. Long-term partnerships that align network design, automation, and data platforms continue to replace short-term, transactional arrangements, allowing providers to deliver resilient capacity in tight labor and real-estate environments. Rising marine-insurance premiums on congested South-China-Sea routes and persistent cold-chain bottlenecks in temperature-sensitive corridors add complexity, but they also create high-margin niches that reward providers capable of rigorous quality control and cross-border compliance.

Asia-Pacific Contract Logistics Market Trends and Insights

Explosive E-commerce Penetration Across Asia-Pacific

Digital commerce growth is redefining fulfillment economics across the Asia-Pacific Contract Logistics market. Online sales velocity is forcing brands to adopt omnichannel inventory allocation, micro-fulfillment nodes, and dedicated reverse-logistics loops that most in-house networks cannot match. Indonesia and Vietnam record annual online-sales expansion far above brick-and-mortar growth, pushing warehouse developers to add mezzanine floors for pick-and-pack automation and temperature-controlled cells for premium groceries. Regional return rates often reach 15-30%, demanding refurbishment lines, re-boxing stations, and real-time visibility dashboards that contract-logistics providers now bundle into integrated propositions.

Near-/Re-shoring of Supply Chains ("China+1")

Multinational corporations are reallocating component sourcing and final assembly to Southeast Asia and India to diversify geopolitical risk and lower total landed cost. New production clusters in Vietnam's Northern Economic Zone and Indonesia's Batang Industrial Park demand inbound raw-material staging, just-in-sequence line feeding, and export consolidation that established providers can deliver from multi-country control towers. Dual-sourcing strategies require visibility across Chinese and non-Chinese plants, prompting shippers to hand over transport planning, milestone monitoring, and supplier-managed inventory to logistics specialists. Government programs such as India's Production-Linked Incentive scheme and Indonesia's Omnibus Law further accelerate factory relocations, locking in mid-term growth for the Asia-Pacific Contract Logistics market as new corridors mature.

Soaring Real-estate & Labor Costs in Tier-1 Hubs

Prime-grade warehouse rents rose sharply across Singapore, Hong Kong, and Tokyo in 2024, driven by constrained land supply and competing demand from data-center operators. Simultaneously, base wages for forklift drivers and order-pickers climbed in double digits in Australia and South Korea, eroding profit margins for high-volume operations. Contract-logistics providers mitigate these pressures through goods-to-person robotics, automated palletizers, and energy-efficient HVAC systems, but such upgrades require heavy capital outlays and lengthier payback periods. The economics encourage hub-and-spoke networks anchored in lower-cost satellite cities such as Johor Bahru and Chiba, yet last-mile cut-off times in megacities remain challenging, tightening service-level agreements and limiting rate increases in the near term.

Other drivers and restraints analyzed in the detailed report include:

- Government Mega-spend on Logistics Infrastructure

- Outsourcing Focus of Manufacturers & Retailers

- Fragmented Standards & Permits Across Asia-Pacific Nations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The transportation slice of the Asia-Pacific Contract Logistics market generated 62.55% of revenue in 2025, anchored by dense road fleets in China and sprawling domestic maritime lanes in Indonesia. Providers orchestrate synchronized long-haul trucking, rail shuttles, and short-sea feeder loops to balance cost and speed across fragmented geography. Meanwhile, value-added services are expected to post the strongest 4.03% CAGR to 2031 as manufacturers seek postponement, kitting, and light-assembly capabilities inside regional distribution centers. Growing label-compliance complexity in consumer electronics pushes contract operators to install on-site print-and-apply lines, while fashion brands use in-warehouse sewing cells for rapid size adjustments that elevate sell-through rates. The shift broadens margins and reduces reliance on volatile linehaul rates, reinforcing the structural expansion of the Asia-Pacific Contract Logistics market size within higher-value niches.

Warehouse-and-distribution operations remain central, scaling with e-commerce parcel volumes and omni-inventory strategies. High-density shuttle systems reduce footprint in urban infill sites, whereas cross-docking layouts near seaports cut dwell time for temperature-sensitive produce. Progressive operators couple warehouse-management systems with real-time transport-visibility platforms, unlocking predictive arrival windows and exception alerts that sharpen customer experience. Airfreight forwarding volumes climb in parallel as direct-injection models for high-value parcels and biologics require multi-modal control from origin to doorstep, buttressing growth across the Asia-Pacific Contract Logistics market.

The Asia-Pacific Contract Logistics Market Report is Segmented by Service Type (Transportation, Warehousing & Distribution, and Value-Added Services), Contract Duration (1-3 Years and Above 3 Years), End-User Industry (Manufacturing & Automotive, , Retail & E-Commerce, Healthcare & Pharmaceuticals, Chemicals, and More), Country (China, India, Japan, Australia, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Deutsche Post DHL Group

- DSV

- CEVA Logistics

- UPS Supply Chain Solutions

- Logisteed Ltd

- CJ Logistics

- Nippon Express Co. Ltd

- Toll Group

- Yusen Logistics Co. Ltd

- Kuehne + Nagel

- Kerry Logistics Network Ltd

- Hellmann Worldwide Logistics

- Rhenus Logistics

- Geodis

- GAC

- Silk Contract Logistics

- Linc Group

- Rohlig Logistics

- Allcargo Logistics Ltd

- Broekman Logistics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosive e-commerce penetration across Asia-Pacific

- 4.2.2 Near-/re-shoring of supply chains ("China+1")

- 4.2.3 Government mega-spend on logistics infrastructure

- 4.2.4 Outsourcing focus of manufacturers & retailers

- 4.2.5 EV battery gigafactories' in-plant logistics demand

- 4.2.6 Digital customs platforms speeding cross-border flows

- 4.3 Market Restraints

- 4.3.1 Soaring real-estate & labour costs in tier-1 hubs

- 4.3.2 Fragmented standards & permits across Asia-Pacific nations

- 4.3.3 Cold-chain capacity bottlenecks for biologics

- 4.3.4 Rising marine-insurance premiums in South-China-Sea lanes

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook (Automation, AI, IoT, WMS)

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Threat of Substitutes

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Bargaining Power of Suppliers

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Government Initiatives & SEZ Landscape

- 4.9 Transport Corridors (Maritime, Rail, Road)

- 4.10 Insights on E-commerce (Domestic & Cross-Border)

- 4.11 Insights on Reverse Logistics

- 4.12 COVID-19 & Geo-Political Events Impact Review

5 Market Size & Growth Forecasts

- 5.1 By Service Type

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Rail

- 5.1.1.3 Air

- 5.1.1.4 Sea

- 5.1.2 Warehousing & Distribution

- 5.1.3 Value-added Services (Assembly, Labelling, Kitting)

- 5.1.1 Transportation

- 5.2 By Contract Duration

- 5.2.1 1 - 3 Years

- 5.2.2 Above 3 years

- 5.3 By End-user Industry

- 5.3.1 Manufacturing & Automotive

- 5.3.2 Food & Beverage

- 5.3.3 Retail & E-commerce

- 5.3.4 Healthcare & Pharmaceuticals

- 5.3.5 Chemicals

- 5.3.6 Other Industries

- 5.4 By Country

- 5.4.1 China

- 5.4.2 India

- 5.4.3 Japan

- 5.4.4 South Korea

- 5.4.5 Australia

- 5.4.6 Singapore

- 5.4.7 Malaysia

- 5.4.8 Indonesia

- 5.4.9 Thailand

- 5.4.10 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration Analysis

- 6.2 Strategic Moves (M&A, JVs, Automation Cap-ex)

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Deutsche Post DHL Group

- 6.4.2 DSV

- 6.4.3 CEVA Logistics

- 6.4.4 UPS Supply Chain Solutions

- 6.4.5 Logisteed Ltd

- 6.4.6 CJ Logistics

- 6.4.7 Nippon Express Co. Ltd

- 6.4.8 Toll Group

- 6.4.9 Yusen Logistics Co. Ltd

- 6.4.10 Kuehne + Nagel

- 6.4.11 Kerry Logistics Network Ltd

- 6.4.12 Hellmann Worldwide Logistics

- 6.4.13 Rhenus Logistics

- 6.4.14 Geodis

- 6.4.15 GAC

- 6.4.16 Silk Contract Logistics

- 6.4.17 Linc Group

- 6.4.18 Rohlig Logistics

- 6.4.19 Allcargo Logistics Ltd

- 6.4.20 Broekman Logistics

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

8 Appendix

- 8.1 GDP Distribution by Activity & Region

- 8.2 Capital-Flow Insights

- 8.3 External Trade Statistics