|

시장보고서

상품코드

1940679

디지털 화물 운송 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Digital Freight Forwarding - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

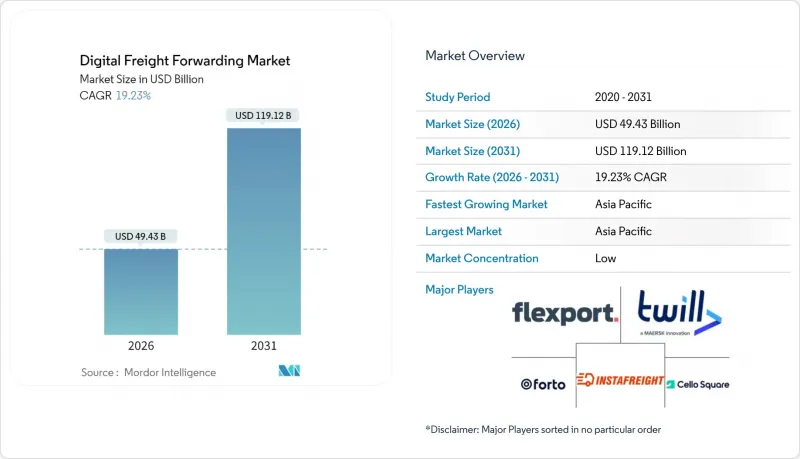

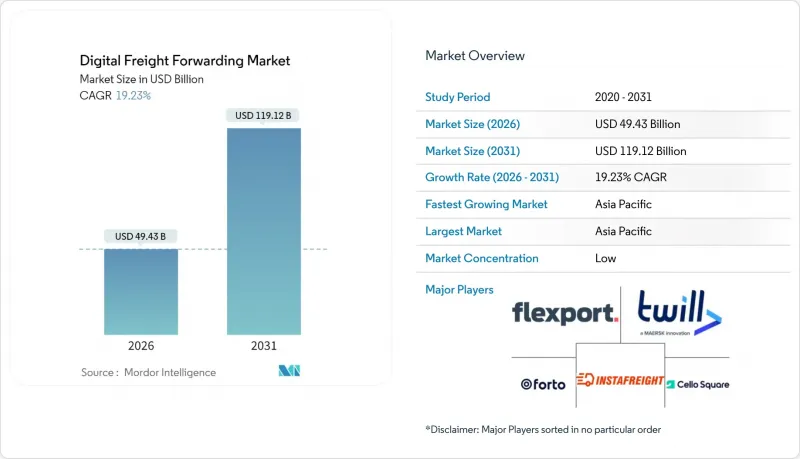

디지털 화물 운송 시장 규모는 2025년 414억 6,000만 달러에서 2026년에는 494억 3,000만 달러에 이를 것으로 추정됩니다.

2031년에는 1,191억 2,000만 달러에 달할 것으로 예상되며, 2026-2031년 연평균 복합 성장률(CAGR) 19.23%로 성장할 것으로 전망됩니다.

급속한 국경 간 전자상거래의 확산, 종이 없는 무역에 대한 규제 요건, API 지원 통신사 연결의 확대가 결합되어 성장을 가속하고 있으며, 화주들은 아날로그 예약 프로세스에서 벗어나고 있습니다. 운임 검색, 예약, 통관, 실시간 가시성을 통합한 통합형 클라우드 네이티브 플랫폼은 이제 세계 무역 조정의 기반을 형성하고 있습니다. 아시아태평양은 수출 제조업 집적지로서의 강점과 정부 주도의 중소기업 디지털화 프로그램을 통해 선도적 지위를 유지하고 있습니다. 반면 북미와 유럽은 운송사 API의 조기 표준화와 엄격한 데이터 정확도 규제를 통해 규모를 확대하고 있습니다. 경쟁의 역학관계는 DSV와 쉥커의 통합과 같은 수직적 통합과 레인 단위의 동적 가격 책정에 AI를 활용하는 순수 기술 기반 신규 시장 진출기업을 중심으로 전개되고 있습니다. 그 결과, 수작업에 의한 중개업자의 수익률은 구조적으로 압축되고, 화주의 전환 비용을 높이는 부가가치 디지털 서비스에 대한 지속적인 투자가 진행되고 있습니다.

세계 디지털 화물 운송 시장 동향과 인사이트

크로스보더 EC의 급성장

국경 간 소매 거래는 2027년까지 8조 달러를 넘어설 것으로 예상되며, 동남아시아 판매자가 도매업체를 거치지 않고 유럽과 미국 소비자에게 직접 도달할 수 있기 때문에 CAGR 9%를 유지할 것으로 예측됩니다. 화주들은 통관, 관세 계산, 라스트 마일 추적을 하나의 인터페이스로 통합할 것을 점점 더 많이 요구하고 있습니다. 디지털 화물 운송 시장 플랫폼은 유럽위원회의 ICS2 프로그램에서 요구하는 수입 요약 신고서를 자동화하여 수작업으로 인한 서류작업을 없애고 국경 통과 지연을 줄입니다. 옴니채널 소매업체들은 현재 단일 추적 ID로 팔레트 단위의 B2B 운송과 소포 단위의 B2C 배송을 관리할 수 있는 화물 툴을 기대하고 있습니다. 자동화된 컴플라이언스 기능과 여러 운송업체를 지원하는 소포 라우팅 기능을 통합한 플랫폼 사업자는 스프레드시트나 이메일에 의존하는 중개업체에 비해 경쟁 우위를 점하고 있습니다.

클라우드 기반 화물 플랫폼 도입 확대

On-Premise 운송 관리 시스템은 최신 운송업체 API와 연동하거나 여러 운송 모드에 대한 1분 미만의 가시성을 제공하지 못하기 때문에 71%의 도입 사례가 클라우드 모델로 전환되고 있습니다. 중견 화주들은 기존 소프트웨어가 요구하는 막대한 설비투자와는 달리 출하량에 따라 확장 가능한 구독 가격 체계를 채택하고 있습니다. GDPR(EU 개인정보보호규정) 준수를 위해 구축된 데이터 현지화 모듈은 벤더가 지역 내 호스팅 및 동의 거버넌스를 제공함으로써 유럽 내 도입을 가속화하고, 규제 대상 산업에서 디지털 화물 운송 시장의 꾸준한 침투를 촉진하고 있습니다. 주요 ERP 제품군에 대한 사전 구축된 커넥터는 IT 부담을 최소화하고 중소기업의 진입장벽을 더욱 낮춥니다.

데이터 표준의 파편화

철도, 트럭, 해상, 항공 각 사업자가 호환되지 않는 EDI 및 API 사양을 채택하고 있기 때문에 물류 데이터 세트는 여전히 사일로화되어 있습니다. 화주는 여전히 여러 통합을 조정해야 하며, 이는 엔드투엔드 자동화를 방해하고 IT 예산을 확대하는 요인으로 작용하고 있습니다. 블록체인 파일럿 프로젝트는 투명성의 가능성을 보여주고 있지만, 통일된 데이터 사전의 부재로 인해 규모 확대에 어려움을 겪고 있습니다. 정부는 자율적 프레임워크를 추진하고 있지만, 연결성과 자원이 제한된 신흥 지역에서는 채택이 늦어지고 있습니다. 전 세계적인 합의가 없는 상황에서 디지털 화물 운송 시장은 계속 확대되고 있지만, 고비용의 회피 수단이 수반되는 상황입니다.

부문 분석

운송 관리는 2025년 매출의 58.45%를 차지할 것으로 예상되며, 화주가 디지털 화물 운송 시장에 진입하는 첫 번째 단계로서의 역할을 강조하고 있습니다. 자동화된 차선 단위의 경로 설정과 실시간 요금 검색은 즉각적인 투자수익률(ROI)을 창출하며, 비용에 민감한 중소기업의 도입을 촉진하고 있습니다. AI를 통한 적재량 조정은 트럭의 주행거리당 수익을 향상시키고, 빈 차량으로 인한 귀가 운송을 줄입니다. 한편, 해상운송의 전자선하증권(eB/L)은 화물의 신속한 인도를 가능하게 합니다.

통관부터 공급망 금융에 이르는 부가가치 서비스는 13.85%의 연평균 복합 성장률(CAGR)로 가장 빠르게 성장하는 부문입니다. 이러한 서비스는 재무 및 컴플라이언스 업무를 플랫폼에 통합하여 고객 정착을 촉진합니다. 옴니채널 소매가 입고화물과 풀필먼트 센터 간의 긴밀한 연계를 필요로 하는 가운데, 창고 관리 시스템과의 통합의 중요성이 커지고 있습니다. 이러한 인접 영역의 확장을 통해 플랫폼은 화주 지출의 더 큰 점유율을 확보할 수 있으며, 단순한 요금 비교를 통한 상품화로부터 자신을 보호할 수 있습니다.

소매 및 전자상거래 분야는 D2C 브랜드 수출 확대와 플래시 세일 배송에 대한 수요 증가로 인해 2025년 35.42%의 점유율을 차지할 것으로 예측됩니다. 의류 및 가전제품 화주들은 디지털 포워딩 플랫폼이 제공하는 엔드투엔드 가시성을 높이 평가했습니다.

의료 및 제약 분야는 2031년까지 연평균 복합 성장률(CAGR) 10.95%를 유지할 것으로 예상되는 고성장 부문입니다. 온도 관리 화물 모니터링, 시리얼 레벨의 추적성, 엄격한 감사 추적을 위해서는 전문적인 디지털 워크플로우가 필요합니다. DHL이 의료 네트워크에 22억 달러를 투자하는 등 의약품 컴플라이언스에 대한 벤더들의 관심이 가속화되고 있으며, 2-8℃의 운송 경로 무결성을 보장할 수 있는 플랫폼이 차별화 요소로 작용하고 있습니다.

지역별 분석

아시아태평양은 2025년 매출의 39.55%를 차지하며 19.42%의 연평균 복합 성장률(CAGR)로 확대될 것으로 예측됩니다. 이는 제조업의 수출이 지배적이라는 점과 중소기업의 디지털화를 지원하는 공공정책이 뒷받침하고 있다는 점을 반영합니다. 인도의 특송 물류 부문은 고속도로와 공항 정비로 인한 화물 흐름의 가속화를 배경으로 연간 10-12% 성장을 목표로 하고 있습니다. 아시아태평양 무역원활화 보고서에 따르면, 디지털 문서화 개혁으로 평균 무역비용이 11% 절감될 것으로 추산되어 도입의 근거를 강화했습니다.

북미의 경우, 잘 구축된 전자상거래 생태계와 트럭 운송 및 소량 배송 사업자 간 API 표준화의 선행 단계가 장점으로 작용하고 있습니다. 연방해사위원회의 데이터 정확도 프로그램은 표준화된 이벤트 코드를 촉진하고 플랫폼 간 상호 운용성을 지원합니다. 캐나다와 멕시코는 USMCA(미국-멕시코-캐나다 협정)에 따른 니어쇼어링(near-shoring)의 기세를 타고 자동화된 통관 모듈과 이중 언어 인터페이스에 대한 수요가 증가하고 있습니다.

유럽에서는 eFTI와 ICS2에 의한 페이퍼리스화 의무화가 진행되어 화주들은 디지털화를 강요받고 있습니다. 독일에서는 DSV와 쉥커의 합병으로 10억 유로(11억 달러)의 디지털 강화 예산이 투입되었고, 북유럽 국가에서는 플랫폼 도입과 녹색 물류 목표가 연계되어 있습니다. 영국의 브렉시트 이후 통관 프로토콜은 컴플라이언스 자동화의 필요성을 높이고, 화물 운송을 통합 서비스 제공업체로 유도하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측(금액, 10억 달러)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

LSH 26.03.10Digital Freight Forwarding Market size in 2026 is estimated at USD 49.43 billion, growing from 2025 value of USD 41.46 billion with 2031 projections showing USD 119.12 billion, growing at 19.23% CAGR over 2026-2031.

Rapid cross-border e-commerce adoption, regulatory mandates for paperless trade, and the spread of API-enabled carrier connectivity collectively propel growth as shippers pivot away from analog booking processes. Integrated, cloud-native platforms that fuse rate discovery, booking, customs, and real-time visibility now form the backbone of global trade orchestration. Asia-Pacific retains leadership because of deep export manufacturing hubs and government-backed SME digitization programs, while North America and Europe scale through early carrier API standardization and strict data accuracy rules. Competitive dynamics center on vertical integrations like the DSV-Schenker combination and on pure-play technology entrants harnessing AI for lane-level dynamic pricing. The result is structural margin compression for manual intermediaries and sustained investment in value-added digital services that raise switching costs for shippers.

Global Digital Freight Forwarding Market Trends and Insights

Rapid Growth of Cross-Border E-commerce

Cross-border retail transactions are forecast to surpass USD 8 trillion by 2027, maintaining a 9% CAGR as Southeast Asian sellers reach Western consumers without wholesalers. Shippers increasingly demand unified customs clearance, duty calculation, and last-mile traceability in one interface. Digital freight forwarding market platforms automate entry summary declarations required under the European Commission's ICS2 program, eliminating manual paperwork and cutting border clearance delays. Omnichannel retailers now expect freight tools that manage pallet-level B2B moves alongside parcel-level B2C deliveries under a single tracking ID. Platform operators that embed automated compliance and multi-carrier parcel routing gain competitive advantage over intermediaries reliant on spreadsheets or email.

Rising Adoption of Cloud-Based Freight Platforms

Cloud models account for 71% of deployments because on-premise Transportation Management Systems cannot connect to modern carrier APIs or provide sub-minute visibility across modes. Mid-market shippers embrace subscription pricing that scales with shipment volumes, in contrast to the heavy capex demanded by legacy software. Data-localization modules built for GDPR compliance accelerate European uptake as vendors offer in-region hosting and consent governance, positioning the digital freight forwarding market for steady penetration in regulated verticals. Pre-built connectors into leading ERP suites minimize IT effort, further lowering barriers for SMEs.

Data-Standards Fragmentation

Logistics data sets remain siloed because rail, truck, ocean, and air parties adopt incompatible EDI and API specifications. Shippers must still juggle multiple integrations, hurting end-to-end automation and enlarging IT budgets. Blockchain pilots demonstrate transparency potential yet stall at scale for lack of unified data dictionaries. Governments push voluntary frameworks, but adoption lags in emerging regions where connectivity and resources are limited. Without global consensus, digital freight forwarding market expansion continues, albeit with costly workarounds.

Other drivers and restraints analyzed in the detailed report include:

- API-Enabled Carrier Connectivity

- AI-Driven Dynamic-Pricing Marketplaces

- Cyber-Security & Privacy Risks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation Management contributed 58.45% of 2025 revenue, underscoring its role as the first stop for shippers entering the digital freight forwarding market. Automated lane-level routing and live rate discovery generate immediate ROI, encouraging adoption even among cost-conscious SMEs. AI load-balancing elevates truck revenue per mile and trims empty backhauls, while electronic Bills of Lading in ocean freight hasten cargo releases.

Value-added Services, from customs clearance to supply-chain financing, is the fastest-growing slice, advancing at a 13.85% CAGR. These offerings stick customers to platforms by embedding financial and compliance workflows. Warehouse Management integration gains importance as omnichannel retail requires tight coordination between inbound freight and fulfillment centers. The expansion of these adjacencies positions platforms to capture a larger share of shipper spend and insulate against pure rate-comparison commoditization.

Retail & E-commerce dominated demand at 35.42% in 2025, propelled by direct-to-consumer brand exports and flash-sale delivery promises. Shippers of apparel and consumer electronics prize the end-to-end visibility that digital freight forwarding market platforms deliver.

Healthcare & Pharma is the breakout segment, on track for an 10.95% CAGR through 2031. Temperature-controlled cargo monitoring, serial-level traceability, and stringent audit trails demand specialized digital workflows. Investments such as DHL's USD 2.2 billion spend on healthcare networks amplify vendor focus on pharma compliance, differentiating platforms able to guarantee 2-8°C lane integrity.

The Digital Freight Forwarding Market Report is Segmented by Function (Transportation Management, Warehouse Management, Value-Added Services), End-Users (Retail & E-Commerce, and More), Deployment Mode (Cloud, On-Premise), Firm Type (SMEs, Large Enterprises and Government Entities), and Geography (North America, South America, Asia-Pacific, Europe, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific holds 39.55% of 2025 revenue and is set to expand at a 19.42% CAGR, reflecting dominant manufacturing exports and supportive public policy that subsidizes SME digitization. India's express logistics sector targets 10-12% annual growth with highway and airport upgrades quickening freight flows. The Asia-Pacific Trade Facilitation Report pegs average trade-cost cuts at 11% from digital documentation reforms, reinforcing adoption logic.

North America benefits from entrenched e-commerce ecosystems and early-stage API uniformity across truckload and parcel carriers. Federal Maritime Commission data-accuracy programs stimulate standardized event codes, aiding platform interoperability. Canada and Mexico ride USMCA nearshoring momentum, raising demand for automated border-clearance modules and bilingual interfaces.

Europe pushes paperless mandates via eFTI and ICS2, compelling shippers to digitize or lose market access. Germany gains from the DSV-Schenker merger's EUR 1 billion (USD 1.10 billion) digital enhancement budget, while Nordic countries pair platform adoption with green-logistics goals. Post-Brexit customs protocols in the United Kingdom intensify need for compliance automation, steering freight toward integrated service providers.

- Flexport

- Twill (Maersk)

- Forto

- Cello Square

- InstaFreight

- Transporteca

- Kontainers

- Kuehne + Nagel International AG (KN Freight Net)

- Turvo

- iContainers

- DHL Group

- DSV (Shipa Freight / myDSV)

- Sennder

- Cargo.one

- CEVA Logistics

- Shypple

- Zencargo

- Cubic

- Boxnbiz

- Freightwalla

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid growth of cross-border e-commerce

- 4.2.2 Rising adoption of cloud-based freight platforms

- 4.2.3 API-enabled carrier connectivity

- 4.2.4 AI-driven dynamic-pricing marketplaces

- 4.2.5 EU eFTI regulation mandating digital documents

- 4.2.6 Satellite-IoT route-optimisation tools

- 4.3 Market Restraints

- 4.3.1 Data-standards fragmentation

- 4.3.2 Cyber-security and privacy risks

- 4.3.3 Digital-skills talent gap

- 4.3.4 Carrier direct-booking margin squeeze

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Investment Scenario Analysis

- 4.8 Value-Proposition Benchmarking of E-Platforms

- 4.9 Impact of Global Disruptions on Trade Flows

- 4.10 Porter's Five Forces

- 4.10.1 Bargaining Power of Suppliers

- 4.10.2 Bargaining Power of Buyers

- 4.10.3 Threat of New Entrants

- 4.10.4 Threat of Substitutes

- 4.10.5 Competitive Rivalry Intensity

5 Market Size and Growth Forecasts (Value, USD Bn)

- 5.1 By Function

- 5.1.1 Transportation Management

- 5.1.1.1 Land

- 5.1.1.2 Sea

- 5.1.1.3 Air

- 5.1.2 Warehouse Management

- 5.1.3 Value-added Services

- 5.1.1 Transportation Management

- 5.2 By End-users

- 5.2.1 Retail and E-commerce

- 5.2.2 Manufacturing

- 5.2.3 Healthcare and Pharma

- 5.2.4 Automotive

- 5.2.5 Others

- 5.3 By Deployment Mode

- 5.3.1 Cloud

- 5.3.2 On-premise

- 5.4 By Firm Type

- 5.4.1 SMEs

- 5.4.2 Large Enterprises and Government Entities

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Peru

- 5.5.2.3 Chile

- 5.5.2.4 Argentina

- 5.5.2.5 Rest of South America

- 5.5.3 Asia-Pacific

- 5.5.3.1 India

- 5.5.3.2 China

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.5.3.7 Rest of Asia-Pacific

- 5.5.4 Europe

- 5.5.4.1 United Kingdom

- 5.5.4.2 Germany

- 5.5.4.3 France

- 5.5.4.4 Spain

- 5.5.4.5 Italy

- 5.5.4.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.5.4.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.5.4.8 Rest of Europe

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab of Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle East And Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, ... Recent Developments)

- 6.4.1 Flexport

- 6.4.2 Twill (Maersk)

- 6.4.3 Forto

- 6.4.4 Cello Square

- 6.4.5 InstaFreight

- 6.4.6 Transporteca

- 6.4.7 Kontainers

- 6.4.8 Kuehne + Nagel International AG (KN Freight Net)

- 6.4.9 Turvo

- 6.4.10 iContainers

- 6.4.11 DHL Group

- 6.4.12 DSV (Shipa Freight / myDSV)

- 6.4.13 Sennder

- 6.4.14 Cargo.one

- 6.4.15 CEVA Logistics

- 6.4.16 Shypple

- 6.4.17 Zencargo

- 6.4.18 Cubic

- 6.4.19 Boxnbiz

- 6.4.20 Freightwalla

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment