|

시장보고서

상품코드

1940759

NOR 플래시 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)NOR Flash - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

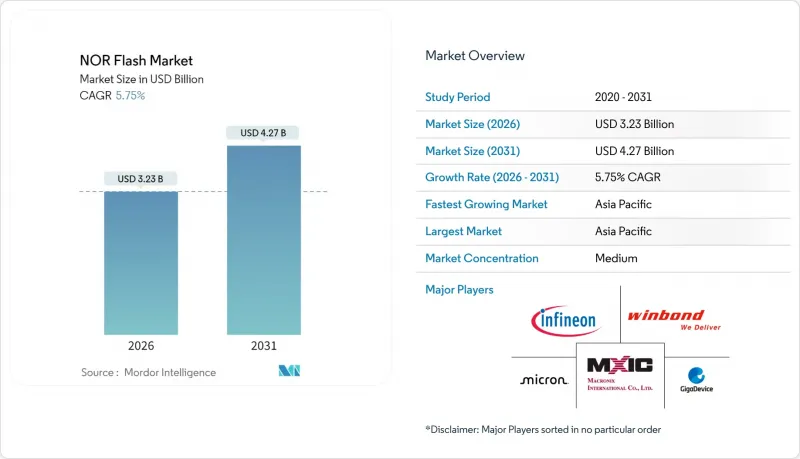

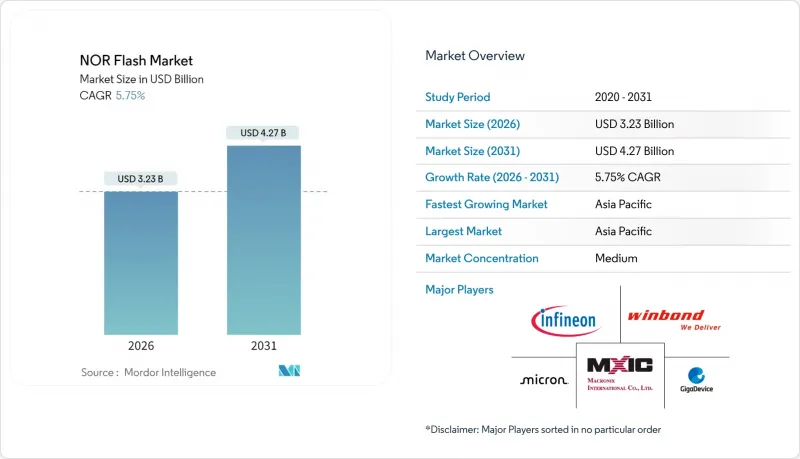

NOR 플래시 시장은 2025년에 30억 5,000만 달러로 평가되었고, 2026년 32억 3,000만 달러에서 2031년까지 42억 7,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 5.75%로 예상됩니다.

이러한 성장세는 첨단운전자보조시스템(ADAS)의 컨텐츠 증가, IoT 엣지 노드에서의 활용 확대, 산업 자동화에 대한 투자 재개를 반영하고 있습니다. 직렬 아키텍처가 주류가 된 이유는 적은 핀 수, 소형 실적, 에너지 효율, 공간 제약이 있는 제품에 적합하기 때문입니다. 인터페이스 업그레이드, 특히 쿼드 및 옥탈 SPI는 읽기 대역폭을 향상시켜 더 빠른 부팅과 더 풍부한 코드 실행을 가능하게 합니다. 각 제조업체들도 저전압 부품, 자동차 등급 기능 안전 인증, 신뢰성을 떨어뜨리지 않고 밀도를 높이는 초기 단계의 3D NOR 파일럿 등에 대응하고 있습니다.

세계 NOR 플래시 시장 동향 및 인사이트

펌웨어 집약적 ADAS 및 도메인 컨트롤러로 자동차 등급 NOR 수요 가속화

자동차 플랫폼은 분산형 전자 제어 장치에서 실시간 펌웨어를 중앙에서 관리하는 도메인/존 아키텍처로 전환하고 있습니다. NOR 플래시는 결정론적 읽기 대기시간과 즉각적인 부팅 실행을 실현하며, 이는 기능적 안전 목표를 뒷받침하는 특성입니다. ASIL-D 인증을 획득한 인피니언의 SEMPER 제품군은 통합 오류 검사 및 듀얼 뱅크 이중화가 코드 스토리지의 내결함성을 강화하는 방법을 보여줍니다. 레벨 2+ 및 레벨 3 기능이 대중화됨에 따라 512Mb-2Gb 직렬 부품에 대한 수요가 증가하고 있으며, 2030년까지 연평균 7.13%의 연평균 복합 성장률(CAGR)로 자동차 NOR 출하량을 증가시킬 것으로 예측됩니다.

전 세계 제조 현장에서 빠른 시동 IoT 에지 디바이스를 위한 쿼드/옥타 SPI 채택

쿼드 SPI는 이미 IoT 코드 스토리지 소켓의 절반 이상을 지원하고 있지만, 옥탈/xSPI는 지속적인 읽기 대역폭을 400MB/s까지 끌어올려 다운로드 시간을 절반으로 줄임으로써 새롭게 부상하고 있습니다. Synopsys의 보고서에 따르면, xSPI는 병렬 메모리에 비해 핀 수 오버헤드를 줄이고, PCB 배선을 용이하게 하며, 부품 비용을 절감할 수 있다고 합니다. GigaDevice의 GD25LX 시리즈는 펌웨어 로딩 시간을 80% 단축하여 엣지에서의 실시간 분석을 가능하게 합니다. 이러한 처리량의 이점은 산업 환경에서 보다 진보된 센서 융합 및 무선 업데이트(OTA) 기능을 실현하고 있습니다.

256Mb 이상의 NAND에 대한 비용 프리미엄이 고밀도 소비자 채택의 장벽이 되고 있습니다.

코드 크기가 256Mb를 초과하는 경우, 직렬 NAND와 eMMC는 비트당 단가가 2-5배 낮기 때문에 NOR을 대체하는 경향이 있습니다. 각 업체들은 기가 디바이스의 QSPI NAND와 같은 하이브리드 설계로 대응하고 있으며, NAND의 경제성으로 NOR 수준의 랜덤 읽기 성능을 구현하고 있습니다. 그러나 고밀도 소비자 장치에서는 NOR을 선택하기 전에 총 시스템 비용을 계속 평가할 것입니다.

부문 분석

시리얼 제품은 2025년 시장 점유율의 88.67%를 차지할 것으로 예상되며, 4-6핀 인터페이스, 소형 패키지, 조립의 용이성 등이 반영된 것으로 분석됩니다. 병렬 NOR은 헤드업 디스플레이나 페일 세이프 클러스터와 같이 진정한 랜덤 바이트 액세스가 필수적인 분야에서는 여전히 중요하지만, 마이크로컨트롤러와 FPGA 벤더들이 시리얼 코드 스토리지로 전환함에 따라 병렬 NOR의 존재감이 줄어들고 있습니다.

컴포넌트 공급업체는 시리얼 NOR에 사전 검증된 드라이버 스택을 번들로 제공하여 OEM 시장 출시 기간을 단축하고 있습니다. 새로운 3D NOR 프로토타입은 우선 시리얼 실적로 등장하여 이 아키텍처에 더 많은 밀도와 비용 측면에서 추진력을 제공할 것입니다. 이러한 상황에서 NOR 플래시 시장은 향후 10년간 시리얼 디바이스의 로드맵을 계속 지지할 것입니다.

쿼드 SPI는 2025년 매출의 40.72%를 차지하며 주류 마이크로컨트롤러를 뒷받침하고 있습니다. 도입 기반이 정점에 도달함에 따라 해당 부문의 CAGR은 완만해질 것이지만, 인스턴트 온 리눅스 및 AUTOSAR 이미지를 필요로 하는 워크로드를 위한 옥탈/xSPI는 7.15%의 성장률을 보일 것으로 예측됩니다. 옥탈은 JEDEC xSPI 프로토콜과도 호환되며, 밀도를 넘어 핀 호환성을 중요시하는 자동차 Tier 1 공급업체 및 산업용 시스템 통합사업자에서 NOR 플래시 시장 점유율을 확대할 수 있습니다.

옥탈/xSPI 지원 NOR 플래시 시장 규모는 2031년까지 크게 확대될 것으로 예측됩니다. 이전 버전과 호환되는 소프트웨어 후크를 통해 설계자는 보드 설계 변경 없이 단계적으로 대역폭을 업그레이드할 수 있어 쉽게 마이그레이션할 수 있습니다. 각 공급업체들은 인터페이스의 진화와 보안 및 기능 안전 옵션을 결합하여 프리미엄 소켓 시장을 공략하고 있습니다.

256Mb 이상의 장치는 고급 인포테인먼트 헤드 유닛 및 프로그래머블 로직 컨트롤러에 적합하여 2025년 19.94%의 시장 점유율을 차지할 것으로 예측됩니다. 반면, 64Mb 이하(32Mb 이상) 부품은 펌웨어를 많이 사용하는 IoT 노드에서 용량과 비용의 균형을 맞추기 위해 8.12%로 가장 빠르게 성장하고 있습니다.

고밀도화 로드맵은 적층 다이와 신흥 3D 레이아웃을 활용하여 평면 스케일링의 한계를 완화합니다. 그러나 엣지 디바이스의 코드 확장과 엄격한 부품 비용 제약이 충돌하는 32-64Mb 소켓 영역에서 가장 견조한 성장세를 보일 것으로 예측됩니다. 각 공급업체는 밀도 단계에 걸쳐 핀 호환이 가능한 업그레이드 경로를 제공함으로써 OEM 제조업체의 재설계 부담을 최소화합니다.

NOR 플래시 시장은 유형별(직렬, 병렬), 인터페이스별(SPI 싱글/듀얼 등), 밀도별(2Mb 이하 등), 전압별(3V 클래스 등), 최종사용자용도(소비자 가전 등), 공정 기술 노드(90nm 이상 등), 패키지 유형(WLCSP/CSP 등), 지역(북미 등)으로 구분됩니다.), 패키지 유형(WLCSP/CSP 등), 지역(북미 등)으로 구분됩니다. 시장 예측은 금액(USD) 및 수량(단위)으로 제공됩니다.

지역별 분석

아시아태평양은 2025년 NOR 플래시 시장 매출의 약 60.55%를 차지할 것으로 예상되며, 2031년까지 큰 폭으로 확대될 것으로 전망됩니다. 중국의 반도체 자급률 향상을 위한 노력으로 55nm 및 40nm 양산 라인에 많은 자본이 유입되어 지역 공급처가 국내 업체로 전환되고 있습니다. 대만은 지정학적 리스크에도 불구하고 외부 고객을 지원하면서 세계 웨이퍼 공급의 대부분을 담당하고 있습니다. 일본과 한국은 오랜 기간 구축된 팹을 통해 기여하고 있으며, 키옥시아의 신규 북상 팹2는 2025년 말부터 단계적으로 생산 능력을 추가할 것으로 예측됩니다.

북미는 자동차, 산업, 항공우주 설계에 특화된 프리미엄 시장입니다. CHIPS법에 근거한 정부 지원책으로 현지 웨이퍼 생산 개시 및 첨단 패키징 프로젝트를 촉진하고, 해외 파운드리로부터공급 다변화를 추진하고 있습니다. 마이크론은 자동차용 NOR 메모리 제품군을 확대하고 있으며, Li Auto의 크로스 도메인 컨트롤러는 중국 전기차에 미국산 메모리가 채택된 사례입니다.

유럽에서는 NOR의 기능 안전 특성과 일치하는 엄격한 신뢰성 및 추적성 기준이 유지되고 있습니다. 독일에 본사를 둔 인피니언은 Tier 1 자동차 제조업체 및 인더스트리 4.0 OEM을 위한 국내 공급망을 구축하고 있습니다. EU 정책 당국은 내결함성 반도체 생태계에 대한 자금 투입을 추진하고 있으며, 이는 아시아 파운드리에 대한 의존도를 낮추는 동시에 NOR 공급업체들 수요 전망을 강화할 수 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

LSH 26.03.10The NOR flash market was valued at USD 3.05 billion in 2025 and estimated to grow from USD 3.23 billion in 2026 to reach USD 4.27 billion by 2031, at a CAGR of 5.75% during the forecast period (2026-2031).

Growth momentum reflects rising content in advanced driver-assistance systems (ADAS), wider use in IoT edge nodes, and renewed investment in industrial automation. Serial architectures dominate because their low pin count, compact footprint, and energy efficiency align with space-constrained products. Interface upgrades-especially Quad and Octal SPI-are lifting read bandwidths, enabling faster boot and richer code execution. Manufacturers are also responding with lower-voltage parts, automotive-grade functional-safety certifications, and early 3D NOR pilots that raise density without sacrificing reliability.

Global NOR Flash Market Trends and Insights

Firmware-intensive ADAS and Domain Controllers Accelerating Automotive-grade NOR Demand

Automotive platforms are migrating from distributed electronic control units to domain and zone architectures that centralize real-time firmware. NOR Flash delivers deterministic read latency and instant-on execution, attributes that underpin functional safety targets. Infineon's SEMPER family, now ASIL-D certified, demonstrates how integrated error-checking and dual-bank redundancy strengthen code-storage resilience. As Level 2+ and Level 3 features proliferate, demand for 512 Mb-2 Gb serial parts is rising, propelling automotive NOR volumes at 7.13% CAGR through 2030.

Quad/Octal SPI Adoption for Fast-Boot IoT Edge Devices across Global Manufacturing Hubs

Quad SPI already powers more than half of IoT code-storage sockets, yet Octal/xSPI is emerging because it pushes sustained read bandwidths to 400 MB/s while halving download times. Synopsys reports that xSPI cuts pin-count overhead versus parallel memory, easing PCB routing and lowering BOM cost. GigaDevice's GD25LX series shows an 80% reduction in firmware load time, enabling real-time analytics at the edge. This throughput benefit is unlocking richer sensor-fusion and over-the-air update features in industrial settings.

Cost Premium over NAND Above 256 Mb Limiting High-Density Consumer Adoption

When code size grows beyond 256 Mb, Serial NAND or eMMC often displace NOR because they offer two to five times lower cost per bit. Vendors are countering with hybrid designs, such as GigaDevice's QSPI NAND-that deliver NOR-like random read at NAND economics. Nevertheless, high-density consumer devices will continue to evaluate total system cost before selecting NOR.

Other drivers and restraints analyzed in the detailed report include:

- Constellation-Scale LEO Satellites Requiring Radiation-Hardened NOR Flash Devices

- China's 55 nm and 40 nm Indigenous Process Push for NOR Self-Sufficiency

- Scaling Ceilings Beyond 45 nm Steering OEM Roadmaps Toward MRAM/ReRAM Substitutes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Serial products supplied 88.67% of the 2025 market share, reflecting their four-to-six-pin interface, smaller packages, and lower assembly complexity. Parallel NOR remains relevant where true random byte access is mandatory, such as heads-up displays and fail-safe clusters, but its footprint is narrowing as microcontroller and FPGA suppliers migrate to serial code storage.

Component vendors bundle Serial NOR with pre-verified driver stacks, accelerating time-to-market for OEMs. Emerging 3D NOR prototypes will debut first in serial footprints, giving the architecture another density and cost tailwind. In this context, the NOR Flash market continues to favor Serial device roadmaps through the decade.

Quad SPI delivered 40.72% revenue in 2025, underpinning mainstream microcontrollers. The segment's CAGR eases as installed bases peak, while Octal/xSPI climbs at 7.15% on workloads that need instant-on Linux or AUTOSAR images. Octal also aligns with JEDEC xSPI protocol, enabling NOR Flash market share gains among automotive Tier 1s and industrial SIs that value pin compatibility across densities.

The NOR Flash market size for Octal/xSPI parts is projected to jump significantly by 2031. Backward-compatible software hooks ease migration; hence, designers can phase-upgrade bandwidth without board redesign. Suppliers are merging interface advancements with security and functional-safety options to target premium sockets.

Devices with greater than 256 Mb captured 19.94% market share in 2025 due to their suitability for sophisticated infotainment head units and programmable logic controllers. Meanwhile, 64-Mb-and-less (greater than 32 Mb) parts grow fastest at 8.12% because they balance capacity and cost for firmware-rich IoT nodes.

Higher-density roadmaps leverage stacked-die or emerging 3D layouts to mitigate planar scaling ceilings. However, volume growth will remain strongest in 32-64 Mb sockets where code expansion in edge devices collides with tight bill-of-materials constraints. Vendors provide pin-compatible upgrade paths across density steps, minimizing redesign effort for OEMs.

NOR Flash Market is Segmented by Type (Serial, Parallel), Interface (SPI Single/Dual, and More), Density (2 Mb and Less, and More), Voltage (3V Class, and More), End-User Application (Consumer Electronics, and More), Process Technology Node (90 Nm and Older, and More), Packaging Type (WLCSP/CSP, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Asia Pacific controlled about 60.55% of the NOR Flash market revenue in 2025 and is projected to expand significantly by 2031. China's semiconductor self-sufficiency drive has drawn considerable capital toward 55 nm and 40 nm serial lines, shifting regional procurement toward domestic vendors. Taiwan continues to supply a significant portion of global wafers, anchoring external customers despite geopolitical risk. Japan and South Korea contribute through long-established fabs; Kioxia's new Kitakami Fab 2 will add incremental capacity starting late 2025.

North America represents a premium segment specialized in automotive, industrial, and aerospace designs. Government incentives under the CHIPS Act are catalyzing local wafer starts and advanced-packaging projects, diversifying supply away from overseas foundries. Micron is broadening its automotive NOR portfolio, with Li Auto's cross-domain controller an illustration of U.S. memory inside Chinese EVs.

Europe maintains strict reliability and traceability standards that align with NOR's functional-safety traits. Infineon's headquarters in Germany anchors a domestic supply chain serving Tier 1 automotive and Industry 4.0 OEMs. EU policymakers are channeling funds toward a resilient semiconductor ecosystem, which could ease the region's dependence on Asian foundries while strengthening demand visibility for NOR suppliers.

- Winbond Electronics Corporation

- Macronix International Co. Ltd.

- GigaDevice Semiconductor Inc.

- Infineon Technologies AG

- Micron Technology Inc.

- Integrated Silicon Solution Inc.

- Microchip Technology Inc.

- Renesas Electronics Corporation

- Elite Semiconductor Microelectronics Technology Inc.

- Wuhan XMC

- Puya Semiconductor (Shanghai) Co. Ltd.

- Samsung Semiconductor

- Alliance Memory

- Zbit Semiconductor

- YMTC - Xi'an Longsys

- Fudan Microelectronics Group Co. Ltd.

- AMIC Technology Corporation

- BOYA Microelectronics Co. Ltd.

- XTX Technology (Shenzhen) Limited

- Shenzhen Longsys Electronics Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Firmware-intensive ADAS and Domain Controllers Accelerating Automotive-grade NOR Demand

- 4.2.2 Quad/Octal SPI Adoption for Fast-Boot IoT Edge Devices across Global Manufacturing Hubs

- 4.2.3 Constellation-Scale LEO Satellites Requiring Radiation-Hardened NOR Flash Devices

- 4.2.4 China's 55 nm and 40 nm Indigenous Process Push for NOR Self-Sufficiency

- 4.2.5 Secure Boot and OTA Update Mandates in Industry 4.0 Factories

- 4.2.6 Low-Power 1.8 V Serial NOR for Wearable/Point-of-Care Healthcare Electronics

- 4.3 Market Restraints

- 4.3.1 Cost Premium over NAND Above 256 Mb Limiting High-Density Consumer Adoption

- 4.3.2 Scaling Ceilings Beyond 45 nm Steering OEM Roadmaps Toward MRAM/ReRAM Substitutes

- 4.3.3 Foundry Concentration in Taiwan Exposing Supply-Chain Disruption Risk

- 4.3.4 ASP Compression from Expanding Chinese Capacity Impacting Vendor Margins

- 4.4 Value / Supply-Chain Analysis

- 4.5 Macro Trend Impact Analysis

- 4.6 Regulatory and Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Pricing Analysis

- 4.9 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, VOLUME)

- 5.1 By Type (Value, Volume)

- 5.1.1 Serial NOR Flash

- 5.1.2 Parallel NOR Flash

- 5.2 By Interface (Value)

- 5.2.1 SPI Single / Dual

- 5.2.2 Quad SPI

- 5.2.3 Octal and xSPI

- 5.3 By Density (Value)

- 5.3.1 2 Megabit And Less NOR

- 5.3.2 4 Megabit And Less-NOR (greater than 2mb) NOR

- 5.3.3 8 Megabit And Less (greater than 4mb) NOR

- 5.3.4 16 Megabit And Less (greater than 8mb) NOR

- 5.3.5 32 Megabit And Less (greater than 16mb) NOR

- 5.3.6 64 Megabit And Less (greater than 32mb) NOR

- 5.3.7 128 Megabit and Less (greater than 64MB) NOR

- 5.3.8 256 Megabit and Less (greater than 128MB) NOR

- 5.3.9 Greater than 256 Megabit

- 5.4 By Voltage (Value)

- 5.4.1 3 V Class

- 5.4.2 1.8 V Class

- 5.4.3 Wide-Voltage (1.65 V - 3.6 V)

- 5.4.4 Others - 1.2V Class (and similar sub-1.8V) (2.5V, 5V, etc.)

- 5.5 By End-user Application (Value, Volume)

- 5.5.1 Consumer Electronics

- 5.5.2 Communication

- 5.5.3 Automotive

- 5.5.4 Industrial

- 5.5.5 Other Applications

- 5.6 By Process Technology Node (Value)

- 5.6.1 90 nm and Older

- 5.6.2 65 nm

- 5.6.3 55 nm (including 58 nm)

- 5.6.4 45 nm

- 5.6.5 28 nm and Below

- 5.7 By Packaging Type (Value)

- 5.7.1 WLCSP / CSP

- 5.7.2 QFN / SOIC

- 5.7.3 BGA / FBGA

- 5.7.4 Others

- 5.8 By Geography (Value, Volume)

- 5.8.1 North America

- 5.8.1.1 United States

- 5.8.1.2 Canada

- 5.8.1.3 Mexico

- 5.8.2 Europe

- 5.8.2.1 Germany

- 5.8.2.2 France

- 5.8.2.3 United Kingdom

- 5.8.2.4 Italy

- 5.8.2.5 Rest of Europe

- 5.8.3 Asia-Pacific

- 5.8.3.1 China

- 5.8.3.2 Japan

- 5.8.3.3 South Korea

- 5.8.3.4 Taiwan

- 5.8.3.5 India

- 5.8.3.6 South East Asia

- 5.8.3.7 Rest of Asia-Pacific

- 5.8.4 Rest of the World

- 5.8.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Winbond Electronics Corporation

- 6.4.2 Macronix International Co. Ltd.

- 6.4.3 GigaDevice Semiconductor Inc.

- 6.4.4 Infineon Technologies AG

- 6.4.5 Micron Technology Inc.

- 6.4.6 Integrated Silicon Solution Inc.

- 6.4.7 Microchip Technology Inc.

- 6.4.8 Renesas Electronics Corporation

- 6.4.9 Elite Semiconductor Microelectronics Technology Inc.

- 6.4.10 Wuhan XMC

- 6.4.11 Puya Semiconductor (Shanghai) Co. Ltd.

- 6.4.12 Samsung Semiconductor

- 6.4.13 Alliance Memory

- 6.4.14 Zbit Semiconductor

- 6.4.15 YMTC - Xi'an Longsys

- 6.4.16 Fudan Microelectronics Group Co. Ltd.

- 6.4.17 AMIC Technology Corporation

- 6.4.18 BOYA Microelectronics Co. Ltd.

- 6.4.19 XTX Technology (Shenzhen) Limited

- 6.4.20 Shenzhen Longsys Electronics Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet Need Analysis