|

시장보고서

상품코드

1940802

미국의 POS 단말기 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)United States (US) Point Of Sale (POS) Terminals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

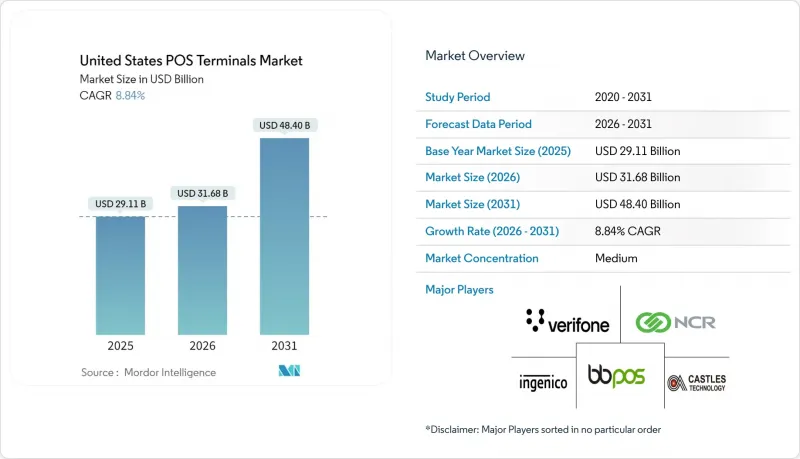

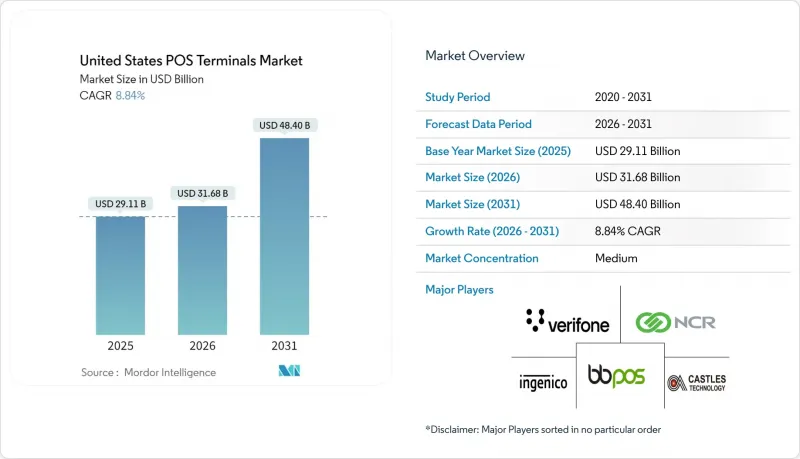

미국의 POS 단말기 시장은 2025년 291억 1,000만 달러에서 2026년에는 316억 8,000만 달러로 성장하여 2026년부터 2031년까지 CAGR 8.84%를 기록하며 2031년에는 484억 달러에 달할 것으로 예측됩니다.

이러한 성장은 EMV 및 NFC 업그레이드 가속화, 비접촉식 결제의 보급 확대, 소규모 사업자의 클라우드 기반 모바일 POS 솔루션으로의 전환에 의해 주도되고 있습니다. PCI DSS 4.0 의무화를 포함한 규제 요인이 하드웨어 업데이트 주기를 촉진하는 한편, FedNow를 비롯한 실시간 결제 인프라가 결제에 대한 기대치를 재구성하고 있습니다. 프로세서 수수료의 압축으로 인해 독립형 하드웨어의 수익률이 줄어들면서 벤더 통합에 대한 압박이 커지고 있습니다. 또한, 소매업체들은 반통합 아키텍처와 임베디드 금융 애플리케이션을 지원하는 안드로이드 스마트 단말기를 선호하고 있으며, PCI 적용 범위를 벗어나지 않고도 통합된 상거래 분석을 실현하고 있습니다.

미국(US) POS(Point of Sale) 단말기 시장 동향 및 인사이트

EMV 및 NFC 단말기의 빠른 업데이트 주기

EMVCo의 기록에 따르면, 2024년 미국 내 비접촉식 거래는 87% 증가하여 탭 결제가 전체 카드 제시 거래의 34%를 차지했습니다. 비 EMV 지원 하드웨어에 대한 책임 전가는 부정사용의 위험을 증가시키고, 가맹점이 NFC 지원 단말기로 업데이트하도록 유도하고 있습니다. 비접촉식 결제는 칩 삽입 방식보다 53% 더 빠르며, 대기시간 단축과 카트 이탈 방지로 이어집니다. 경쟁 압력으로 인해 도입이 늦어졌던 중소기업들도 2027년 계약 갱신 전에 단말기를 갱신해야 하는 상황입니다.

중소기업의 클라우드형 mPOS 솔루션으로의 이행

미국 연방준비제도이사회 조사에 따르면, 미국 중소기업의 67%가 결제 시스템 내 통합 재고 관리 및 분석 기능을 우선순위로 꼽았습니다. 태블릿형 mPOS는 초기 하드웨어 비용을 절감하고, 기존 리스 계약에 비해 월별 처리 수수료를 23% 절감할 수 있습니다. Stripe과 Square의 임베디드 금융 서비스는 도입 장벽을 더욱 낮추고, 연결 환경만 있으면 어디서든 팝업 소매업체가 결제를 받을 수 있도록 지원하고 있습니다.

POS 단말기에 대한 사이버 공격의 고도화

FS-ISAC의 추적 조사에 따르면, 2024년에는 POS를 타겟으로 한 악성코드 변종이 34% 증가했으며, NFC 채널과 안드로이드의 취약점을 악용하는 사례도 확인되었습니다. 이로 인해 소매업체는 엔드포인트 감지 및 암호화 통신에 대한 예산을 책정해야 하며, 전체 POS 시스템 비용이 15-25% 상승하고 있습니다. 소규모 사업자들은 복잡성을 우려해 업그레이드를 미루거나, 리스크가 높은 환경에서는 현금 결제만 하는 경우가 증가하고 있습니다.

부문 분석

비접촉식 결제 솔루션은 미국 POS 단말기 시장에서 가장 빠르게 성장하는 분야로 CAGR 10.37%로 성장하고 있습니다. 그러나 접촉식 리더기는 2025년 기준 미국 POS 단말기 시장에서 여전히 68.15%의 점유율을 차지하고 있습니다. 마스터카드의 조사에 따르면, 비접촉식 결제는 이미 전 세계 대면 거래의 73%를 차지하고 있으며, 미국에서의 이용률은 전년 대비 87% 증가했습니다. 연방준비제도이사회(FRB)의 데이터에 따르면, 처리 속도 향상과 위생상의 이점으로 인해 비접촉식 결제를 선호하는 소비자가 2023년 23%에서 2024년 41%로 증가했다고 합니다.

가맹점에서는 고액 거래나 고령층을 대상으로 칩 & PIN 결제를 계속 지원하면서 기존 기반을 활용하면서 NFC를 단계적으로 도입하고 있습니다. 애플페이와 구글페이가 35세 미만 스마트폰 소유자의 67%에게 보급되고 있는 가운데, 듀얼 인터페이스 단말기는 변화하는 결제 습관에 대응하고 있습니다. 접촉식 및 비접촉식 결제를 원활하게 제공할 수 있는 벤더는 2031년까지 미국 POS 단말기 시장의 확대분을 확보할 수 있을 것으로 예상됩니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.10The United States Point Of Sale Terminals market is expected to grow from USD 29.11 billion in 2025 to USD 31.68 billion in 2026 and is forecast to reach USD 48.4 billion by 2031 at 8.84% CAGR over 2026-2031.

This growth is driven by accelerated EMV and NFC upgrades, rising contactless adoption, and the migration of small merchants to cloud-based mobile POS solutions. Regulatory triggers, including PCI DSS 4.0 mandates, are prompting hardware refresh cycles, while FedNow and other real-time rails are reshaping settlement expectations. Processor fee compression is intensifying vendor consolidation pressures as margins on standalone hardware narrow. Merchants also favor Android smart terminals that support semi-integrated architectures and embedded finance applications, enabling unified commerce analytics without breaching PCI scope.

United States (US) Point Of Sale (POS) Terminals Market Trends and Insights

Rapid EMV and NFC Terminal Upgrade Cycle

EMVCo recorded an 87% rise in U.S. contactless transactions during 2024, with tap-to-pay now accounting for 34% of all card-present activity. Liability shifts on non-EMV hardware elevate fraud risk, pushing merchants toward NFC-ready replacements. Contactless processing is 53% faster than chip insert, cutting wait times and limiting basket abandonment. Competitive pressure now compels even late-adopting small businesses to refresh terminals ahead of 2027 contract renewals.

SME Shift to Cloud-Based mPOS Solutions

Federal Reserve polling shows 67% of U.S. small firms prioritize integrated inventory and analytics within payment systems. Tablet-based mPOS reduces upfront hardware costs and lowers monthly processing fees by 23% versus legacy leases. Embedded finance bundles from Stripe and Square further compress adoption friction, helping pop-up retailers accept payments wherever connectivity exists.

Intensifying Cyber-Attack Sophistication on POS End-Points

FS-ISAC tracked a 34% rise in POS-targeted malware variants during 2024, including exploits on NFC channels and Android vulnerabilities. Merchants now budget for endpoint detection and encrypted communications that raise overall POS system costs 15-25%. Smaller operators, deterred by added complexity, postpone upgrades or revert to cash-only in high-risk settings.

Other drivers and restraints analyzed in the detailed report include:

- Retailer Demand for Unified Commerce Analytics

- PCI-DSS 4.0 Compliance Driving Hardware Refresh

- Inflation-Driven Cap-Ex Deferrals by Small Merchants

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Contactless solutions constitute the fastest-moving slice of the US POS terminals market at a 10.37% CAGR, although contact-based readers still held a 68.15% US POS terminals market share in 2025. Mastercard found tap-to-pay already represents 73% of face-to-face transactions globally, and U.S. usage climbed 87% year over year. Federal Reserve data shows consumer preference for contactless rose to 41% in 2024 from 23% in 2023, sustained by quicker throughput and hygiene benefits.

Merchants continue to support chip-and-PIN for large-ticket sales and older consumer cohorts, leveraging the installed base while gradually layering in NFC. Dual-interface devices accommodate evolving wallet habits as Apple Pay and Google Pay reach 67% penetration among under-35 smartphone owners. Vendors able to furnish seamless contact and contactless acceptance stand to capture the incremental US POS terminals market size expansion through 2031.

The United States Point of Sale Terminals Market Report is Segmented by Mode of Payment Acceptance (Contact-Based and Contactless), POS Type (Fixed Point-Of-Sale Systems, Mobile/Portable Point-Of-Sale Systems), End-User Industry (Retail, Hospitality, Healthcare, Transportation and Logistics, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Verifone Systems Inc.

- Ingenico Inc.

- PAX Technology Limited

- Toshiba Global Commerce Solutions, Inc.

- NCR Corporation

- Diebold Nixdorf Incorporated

- Castles Technology Co., Ltd.

- BBPOS Limited

- Newland Payment Technology Co., Ltd.

- UIC Payworld Inc.

- Equinox Payments, LLC

- Clover Network, LLC

- Square Inc. (Block Inc.)

- Toast, Inc.

- Lightspeed Commerce Inc.

- Posiflex Technology, Inc.

- Epson America, Inc.

- Elo Touch Solutions, Inc.

- HP Inc. (Retail Solutions)

- Zebra Technologies Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors

- 4.3 Market Drivers

- 4.3.1 Rapid EMV and NFC Terminal Upgrade Cycle

- 4.3.2 SME Shift to Cloud-Based mPOS Solutions

- 4.3.3 Retailer Demand for Unified Commerce Analytics

- 4.3.4 PCI-DSS 4.0 Compliance Driving Hardware Refresh

- 4.3.5 Surge in Real-Time Payment and Wallet Acceptance at POS

- 4.3.6 Embedded-Finance ISVs Bundling Terminals with SaaS

- 4.4 Market Restraints

- 4.4.1 Intensifying Cyber-attack Sophistication on POS End-points

- 4.4.2 Inflation-Driven Cap-Ex Deferrals by Small Merchants

- 4.4.3 Processor and Gateway Fee Compression Squeezing Hardware Margins

- 4.4.4 Rural Connectivity Gaps Limiting Wireless POS Performance

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Intensity of Competitive Rivalry

- 4.8.5 Threat of Substitutes

- 4.9 Assessment of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Mode of Payment Acceptance

- 5.1.1 Contact-based

- 5.1.2 Contactless

- 5.2 By POS Type

- 5.2.1 Fixed Point-of-Sale Systems

- 5.2.2 Mobile / Portable Point-of-Sale Systems

- 5.3 By End-User Industry

- 5.3.1 Retail

- 5.3.2 Hospitality

- 5.3.3 Healthcare

- 5.3.4 Transportation and Logistics

- 5.3.5 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Verifone Systems Inc.

- 6.4.2 Ingenico Inc.

- 6.4.3 PAX Technology Limited

- 6.4.4 Toshiba Global Commerce Solutions, Inc.

- 6.4.5 NCR Corporation

- 6.4.6 Diebold Nixdorf Incorporated

- 6.4.7 Castles Technology Co., Ltd.

- 6.4.8 BBPOS Limited

- 6.4.9 Newland Payment Technology Co., Ltd.

- 6.4.10 UIC Payworld Inc.

- 6.4.11 Equinox Payments, LLC

- 6.4.12 Clover Network, LLC

- 6.4.13 Square Inc. (Block Inc.)

- 6.4.14 Toast, Inc.

- 6.4.15 Lightspeed Commerce Inc.

- 6.4.16 Posiflex Technology, Inc.

- 6.4.17 Epson America, Inc.

- 6.4.18 Elo Touch Solutions, Inc.

- 6.4.19 HP Inc. (Retail Solutions)

- 6.4.20 Zebra Technologies Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment