|

시장보고서

상품코드

2034976

제품 수명주기 관리(PLM) 소프트웨어 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Product Lifecycle Management (PLM) Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

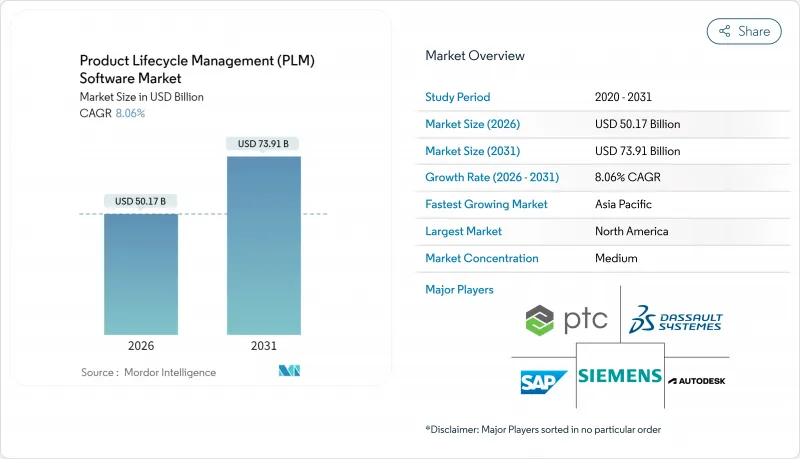

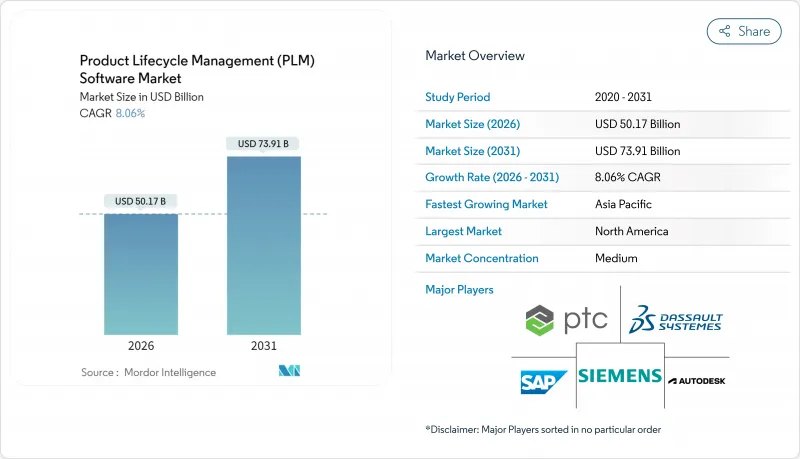

제품 수명주기 관리(PLM) 소프트웨어 시장 규모는 2026년에 501억 7,000만 달러에 이르고, 2031년까지 739억 1,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 8.06%를 기록할 전망입니다.

이러한 성장 궤적은 클라우드 도입의 급속한 확대, 엔지니어링 툴체인에 생성형 AI 코파일럿의 도입, 자동차, 항공우주, 전자, 생명과학 제조 분야에서 엔드투엔드 디지털 추적성에 대한 규제 요건이 강화됨에 따라 뒷받침되고 있습니다. Tier 1 제조업체들은 탄력적인 컴퓨팅이 시뮬레이션 병목현상을 해소하고, 실시간 협업으로 검토 주기를 크게 단축할 수 있다는 점에서 SaaS 플랫폼으로 전환하고 있습니다. 기존 벤더들은 인수 및 플랫폼 확장을 통해 시뮬레이션, 품질, 지속가능성 기능을 통합하기 위해 적극적으로 움직이고 있지만, 오픈소스 대체 솔루션은 특히 비용에 민감한 지역에서 가격 압박을 가하고 있습니다. 사이버 보안에 대한 우려는 여전히 남아있지만, FedRAMP, ISO 27001, SOC 2 Type II에 대한 지속적인 인증 획득으로 규제 대상 산업의 주저함이 완화되고 있습니다. 초기 투자 부담으로 인해 주춤했던 중견기업들은 이제 마이크로 구독 번들을 통해 최고 수준의 PLM 워크플로우에 대한 접근을 민주화하는 마이크로 구독 번들을 활용하고 있습니다.

세계 제품 수명주기 관리(PLM) 소프트웨어 시장 동향 및 인사이트

주요 제조업계의 클라우드 퍼스트 도입

클라우드 네이티브 PLM 아키텍처는 자체 데이터센터에 대한 의존도를 줄이고, 전 세계 검토 주기를 단축합니다. 지멘스는 2025년 4분기 클라우드의 연간 경상수익(ARR)이 소프트웨어 ARR 총액 53억 유로(56억 7,000만 달러)의 49%에 달했다고 발표하며, SaaS로의 전환 속도를 실감케 했습니다. PTC는 Windchill+SaaS 도입이 가속화됨에 따라 2026년 ARR 성장률이 7-9%를 나타낼 것으로 전망하고 있습니다. 온디맨드 컴퓨팅을 통해 하드웨어의 과도한 프로비저닝 없이 제너레이티브 디자인 워크로드를 확장할 수 있고, 공급업체에 대한 실시간 액세스를 통해 설계 변경 지시(ECO) 지연을 크게 줄일 수 있기 때문에 클라우드 도입이 확대되고 있습니다.

엔드-투-엔드 디지털 스레드에 대한 수요 증가

요구사항, CAD, 시뮬레이션, 제조 지침, 현장 데이터를 연결하는 지속적인 디지털 스레드를 통해 폐쇄 루프 피드백이 가능합니다. NIST는 2024년 프레임워크를 발표하고 PLM, ERP, MES의 데이터를 통합하기 위해 STEP AP242 및 관련 스키마 채택을 권장했습니다. 딜로이트와 지멘스는 항공우주 및 자동차 산업 고객을 위해 이러한 프레임워크를 실용화하기 위해 '디지털 스레드 및 디지털 트윈 얼라이언스(Digital Thread and Digital Twin Alliance)'를 결성했습니다. 초기 도입 기업들은 폐기물을 줄이고, 설계 반복을 가속화하며, 규제 당국의 상세한 실물 추적 가능성에 대한 감사 대응력을 향상시켰습니다고 보고하고 있습니다.

레거시 CAD와 최신 PLM 간의 상호운용성 격차 해소

CATIA, NX, SolidWorks, Creo에 걸친 하이브리드 CAD 환경은 클라우드 리포지토리로 전환할 때 데이터 변환 오류가 발생합니다. ITI의 조사에 따르면, 전환 작업의 30-40%는 여전히 수동 수정이 필요하며, 이는 프로젝트의 공사 기간을 연장시키고 있습니다. 지멘스가 2025년 1월 알테아를 인수한 것은 HyperWorks 시뮬레이션과 Teamcenter를 보다 긴밀하게 통합하기 위한 것이지만, STEP과 같은 중립적인 포맷의 채택 상황은 여전히 불균등합니다.

부문 분석

2025년에는 On-Premise 도입이 매출의 56.66%를 차지할 것으로 예상됐으며, 이는 관리되는 기술 데이터와 레거시 계약이 여전히 많은 프로그램의 기반이 되고 있음을 보여줍니다. PLM 소프트웨어 시장의 클라우드 부문은 시뮬레이션 부하 증가를 흡수하고 세계 설계 검토를 지원하는 탄력적 컴퓨팅에 힘입어 2031년까지 연평균 복합 성장률(CAGR) 10.96%를 나타낼 것으로 예측됩니다. 클라우드 도입 PLM 소프트웨어 시장 규모는 2026년 217억 5,000만 달러에서 2031년 366억 1,000만 달러로 확대될 것으로 예상되며, SaaS로의 비가역적 전환이 강조되고 있습니다. 지멘스는 2025년 말 기준 클라우드 ARR이 소프트웨어 구독의 49%를 차지했다고 지적하며, Tier 1 제조업체들 사이에서 클라우드 ARR이 주류로 받아들여지고 있음을 확인했습니다.

하이브리드 토폴로지는 현실적인 타협안으로 떠오르고 있습니다. 민감한 지적재산권(IP)은 방화벽 안에 두고, 공급업체 포털, 디지털 트윈 분석, 고성능 시뮬레이션은 클라우드로 이동합니다. 오토데스크는 중견 제조업체들이 종량제 라이선스를 채택함에 따라 Fusion 360이 2025년도에 제조 부문의 매출을 15-16% 증가시킨 것으로 평가했습니다. 방위 및 제약 산업에서 On-Premise 도입이 계속될 것으로 예상되지만, 클라우드 벤더들이 FedRAMP 및 ISO 27001 인증을 획득함에 따라 SaaS로의 성장세는 계속될 것이며, 제품 수명주기 관리(PLM) 소프트웨어 시장 전체에서 지원 및 업그레이드의 경제성을 재구축할 것입니다.

협업 PDM은 버전 관리, 변경 거버넌스, BOM 계층 구조 관리에서 핵심적인 역할을 수행한 덕분에 2025년 48.26%의 매출 점유율을 유지했습니다. 그러나 디지털 제조 및 MES-PLM 통합은 CAGR 9.32%의 성장세를 보이며 빠르게 성장하고 있는 분야입니다. 디지털 제조 솔루션으로 인한 제품 수명주기 관리(PLM) 소프트웨어 시장 규모는 2026년 81억 3,000만 달러에서 2031년 127억 5,000만 달러로 확대될 것으로 예측됩니다. 지멘스는 Opcenter MES를 Teamcenter에 통합하여 설계 변경을 현장 일정에 반영함으로써 오래된 작업지시서로 인한 낭비를 줄였습니다. 로크웰 오토메이션도 FactoryTalk와 PTC Windchill을 연동하여 유사한 시너지를 실현했습니다.

현재 클라우드 마이크로서비스로 제공되는 시뮬레이션 및 분석 애드온은 통합 제품군의 매력을 높여주는 역할을 하고 있습니다. Ansys는 Windchill 및 Teamcenter와 연동되는 클라우드 네이티브 솔버를 도입하여 멀티피직스 검증을 몇 주에서 며칠로 단축했습니다. 자동차 섀시 설계에는 여전히 MCAD의 통합이 필요하지만, 펌웨어와 하드웨어가 함께 진화해야 하는 전자 분야에서는 용도 수명주기 관리(ALM)가 강화되고 있습니다. PDM, MES, 시뮬레이션을 하나의 계약으로 묶어 제공하는 벤더는 고객 유지율을 높이고 전체 PLM 소프트웨어 시장에서 플랫폼의 경쟁 우위를 강화하고 있습니다.

지역별 분석

북미는 2025년에도 35.28%의 매출 점유율을 유지하며 자동차, 항공우주, 산업기계 분야의 탄탄한 PLM 인프라가 견인차 역할을 할 것으로 예측됩니다. 이 지역의 PLM 소프트웨어 시장 점유율은 견조한 디지털 전환 예산과 새로운 사이버 보안 표준에 대한 빠른 대응을 반영하고 있습니다. 미국 제조업체들은 클라우드 R&D 비용에 대한 세액공제를 활용하여 SaaS로의 전환을 원활하게 진행하고 있습니다. 캐나다의 항공우주 클러스터에서는 민관 컨소시엄을 활용하여 PLM과 현장의 센서 데이터를 통합하는 디지털 트윈 파일럿 프로젝트를 추진하고 있습니다.

아시아태평양은 여전히 가장 빠르게 성장하는 지역으로 2031년까지 연평균 복합 성장률(CAGR) 10.44%를 나타낼 것으로 예측됩니다. 중국의 '14차 5개년 계획'에서는 외국산 엔지니어링 툴에 대한 의존도를 낮추기 위해 국내 PLM 도입에 대해 적극적으로 보조금을 지급하고 있습니다. 인도의 디지털 제조 미션은 국내 OEM과 세계 Tier 1 공급업체 모두 SaaS 기반 PLM을 통해 설계 데이터와 생산 데이터를 통합할 것을 촉구하고 있습니다. 베트남과 태국의 아세안 전자 허브에서는 PLM 도입과 5G 공장 네트워크를 결합하여 대량 생산을 위한 PCB 설계 반복을 용이하게 하고 있습니다.

유럽에서는 독일, 프랑스, 영국을 중심으로 상당한 수요가 예상됩니다. CSRD(Corporate Sustainability Reporting Directive)에 따른 환경 보고 의무화로 인해 PLM 제품군 전체에 수명주기 평가(LCA) 플러그인이 도입되고 있으며, 자동차 및 항공우주 분야의 주요 제조업체들은 수소 추진 시스템 및 도심 항공 모빌리티(UAM) 프로그램을 관리하기 위해 시스템을 업그레이드하고 있습니다. 동유럽의 수탁 제조업체는 EU의 밸류체인에 진입하고 고객의 감사 요구 사항을 준수하기 위해 경량 PLM을 채택하고 있습니다.

남미, 중동, 아프리카는 아직 개발 중이지만 미래가 기대되는 시장입니다. 브라질의 플렉스 연료 자동차 제조업체는 에탄올과 가솔린의 변형 설계를 위해 PLM을 도입하고 있습니다. 사우디아라비아의 '비전 2030'은 PLM이 모듈식 설비 구축을 총괄하는 디지털 산업 회랑에 자금을 지원하고 있습니다. 아프리카의 통신장비 재생업체는 예비 부품의 물류를 최적화하기 위해 클라우드 PLM 도입을 고려하고 있습니다. 절대적인 매출은 뒤쳐져 있지만, 신규 투자 증가로 인해 제품 수명주기 관리(PLM) 소프트웨어 시장 전체에서 두 자릿수 성장이 기대되는 분야가 생겨나고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.05.20The Product Lifecycle Management (PLM) Software Market size reached USD 50.17 billion in 2026 and is projected to advance to USD 73.91 billion by 2031, reflecting an 8.06% CAGR during 2026-2031.

This trajectory is underpinned by fast-rising cloud adoption, the infusion of generative-AI copilots into engineering toolchains, and mounting regulatory demands for end-to-end digital traceability in automotive, aerospace, electronics, and life-sciences manufacturing. Tier-1 manufacturers are shifting toward SaaS platforms as elastic compute reduces simulation bottlenecks and real-time collaboration slashes review cycles. Incumbent vendors have moved aggressively to embed simulation, quality, and sustainability capabilities through acquisitions and platform extensions, while open-source alternatives apply price pressure, especially in cost-sensitive regions. Cyber-security concerns remain, yet continuous certification against FedRAMP, ISO 27001, and SOC 2 Type II is easing hesitancy among regulated industries. Mid-market firms, long held back by upfront capital outlays, now tap micro-subscription bundles that democratize access to best-of-breed PLM workflows.

Global Product Lifecycle Management (PLM) Software Market Trends and Insights

Cloud-First Adoption Among Tier-1 Manufacturers

Cloud-native PLM architectures reduce reliance on proprietary data centers and shorten global review loops. Siemens reported that cloud annual recurring revenue reached 49% of its EUR 5.3 billion (USD 5.67 billion) software ARR in fiscal Q4 2025, illustrating the velocity of SaaS migrations. PTC forecasts 7-9% ARR growth for 2026 as Windchill+ SaaS deployments accelerate. Elevated cloud uptake stems from on-demand compute that scales generative-design workloads without hardware over-provisioning, while real-time access for suppliers slashes engineering change-order latency.

Growing Need for End-to-End Digital Thread

A continuous digital thread links requirements, CAD, simulation, manufacturing instructions, and field data, enabling closed-loop feedback. NIST published a 2024 framework urging adoption of STEP AP242 and related schemas to knit PLM, ERP, and MES data together. Deloitte and Siemens formed the Digital Thread and Twin Alliance to operationalize such frameworks for aerospace and automotive clients. Early adopters report lower scrap, faster design iterations, and audit readiness as regulators request granular as-built traceability.

Persistent Interoperability Gaps Between Legacy CAD and Modern PLM

Hybrid CAD estates spanning CATIA, NX, SolidWorks, and Creo introduce data-translation errors when ported into cloud repositories. ITI documented that 30-40% of migrations still need manual remediation, inflating project timelines. Siemens' acquisition of Altair in January 2025 targets tighter integration of HyperWorks simulation with Teamcenter, yet neutral formats such as STEP remain unevenly adopted.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Push for Product Traceability and Sustainability Reporting

- Generative-AI Copilots Trimming Engineering Change-Order Cycles

- Cyber-Security and IP Leakage Concerns in Multi-Tenant SaaS

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

On-premise installations accounted for 56.66% revenue in 2025, a reminder that controlled technical data and legacy contracts still anchor many programs. The cloud segment of the PLM software market is growing at 10.96% CAGR to 2031, propelled by elastic compute that absorbs simulation spikes and supports global design reviews. The PLM software market size for cloud deployments is set to expand from USD 21.75 billion in 2026 to USD 36.61 billion in 2031, underscoring an irreversible shift toward SaaS. Siemens noted that cloud ARR equaled 49% of its software subscriptions by late 2025, confirming mainstream acceptance among Tier-1 manufacturers.

Hybrid topologies have emerged as a pragmatic compromise. Sensitive IP remains behind firewalls while supplier portals, digital twin analytics, and high-performance simulation burst to the cloud. Autodesk credits Fusion 360 for 15-16% manufacturing revenue growth in fiscal 2025 as mid-market fabricators adopted pay-as-you-go licensing. On-premise deployments will persist in defense and pharma, yet as cloud vendors attain FedRAMP and ISO 27001, growth will keep tilting to SaaS, reshaping support and upgrade economics across the Product Lifecycle Management (PLM) Software market.

Collaborative PDM maintained 48.26% revenue share in 2025 thanks to its core role in version control, change governance, and BOM hierarchy management. However, digital manufacturing and MES-PLM integration is the breakout segment, advancing at 9.32% CAGR. The Product Lifecycle Management (PLM) Software market size attributable to digital manufacturing solutions is anticipated to climb from USD 8.13 billion in 2026 to USD 12.75 billion in 2031. Siemens knitted Opcenter MES into Teamcenter to propagate engineering changes to shop-floor schedules, trimming scrap tied to outdated work instruction. Rockwell Automation achieved similar synergy by aligning FactoryTalk with PTC Windchill.

Simulation and analysis add-ons, now often delivered as cloud micro-services, reinforce the pull of integrated suites. Ansys introduced cloud-native solvers that handshake with Windchill and Teamcenter, compressing multi-physics validation from weeks to days. MCAD integration remains necessary for automotive chassis engineering, while application lifecycle management strengthens in electronics where firmware and hardware must co-evolve. Vendors bundling PDM, MES, and simulation under one contract gain stickiness, fortifying platform moats across the PLM software market.

The Product Lifecycle Management (PLM) Software Market Report is Segmented by Deployment Type (On-Premise, and Cloud), Solution Type (Collaborative PDM / CPDM, MCAD Integration PLM, and More), Organization Size (Large Enterprises, and Small and Medium Enterprises (SMEs)), End-User Industry (Automotive and Transportation, Aerospace and Defense, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America maintained 35.28% revenue share in 2025, spearheaded by entrenched PLM infrastructures in automotive, aerospace, and industrial machinery. The PLM software market share of the region reflects robust digital transformation budgets and early compliance with emerging cyber-security norms. U.S. manufacturers leverage tax credits for cloud R&D spending, smoothing SaaS transitions. Canadian aerospace clusters tap public-private consortia to pilot digital twins that integrate PLM with field sensor data.

Asia Pacific remains the fastest-growing region, posting a 10.44% CAGR through 2031. China's 14th Five-Year Plan actively subsidizes domestic PLM deployment to cut reliance on foreign engineering tools. India's digital manufacturing mission is pushing both domestic OEMs and global tier-one suppliers to unify design and production data via SaaS PLM. ASEAN electronics hubs in Vietnam and Thailand pair PLM rollouts with 5G factory networks, facilitating high-volume PCB design iterations.

Europe contributes sizable demand, centered in Germany, France, and the United Kingdom. CSRD-driven environmental reporting is prompting lifecycle-assessment plug-ins across PLM suites, while automotive and aerospace primes upgrade to manage hydrogen propulsion and urban air-mobility programs. Eastern Europe's contract manufacturers join EU value chains, adopting lightweight PLM to comply with customer audit requirements.

South America, the Middle East, and Africa remain nascent yet promising. Brazil's flex-fuel vehicle producers deploy PLM to juggle ethanol and gasoline variant engineering. Saudi Arabia's Vision 2030 funds digital industrial corridors where PLM orchestrates modular equipment builds. African telecom equipment refurbishers evaluate cloud PLM to optimize spare-parts logistics. Although absolute revenue lags, rising green-field investments yield double-digit growth pockets across the Product Lifecycle Management (PLM) Software Market.

- Siemens AG

- Dassault Systems SE

- PTC Inc.

- SAP SE

- Autodesk Inc.

- Oracle Corporation

- IBM Corporation

- ANSYS Inc.

- Aras Corporation

- Arena (SaaS by PTC)

- Infor Inc.

- Hexagon AB

- Bentley Systems Inc.

- Altair Engineering Inc.

- Propel Software

- IFS AB

- HCLTech xLMCloud

- Accenture Industry X

- OpenBOM

- Propulsion-PLM

- Centric Software

- CONTACT Software

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-first Adoption among Tier-1 Manufacturers

- 4.2.2 Growing Need for End-to-End Digital Thread

- 4.2.3 Regulatory Push for Product Traceability and Sustainability Reporting

- 4.2.4 Generative-AI Copilots Trimming Engineering Change-Order Cycles

- 4.2.5 Micro-subscription PLM Bundles for SMB Value Chains

- 4.2.6 Low-Code PLM Platforms Democratising Custom Workflows (UNDER-REPORTED)

- 4.3 Market Restraints

- 4.3.1 Persistent Interoperability Gaps between Legacy CAD and Modern PLM

- 4.3.2 Cyber-security and IP Leakage Concerns in Multi-tenant SaaS

- 4.3.3 Growing Open-Source Digital-Twin Stacks Cannibalising Paid Licences

- 4.3.4 Trade-Policy-Driven Chip Export Controls Disrupting PLM Upgrade Cycles (UNDER-REPORTED)

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Type

- 5.1.1 On-Premise

- 5.1.2 Cloud

- 5.2 By Solution Type

- 5.2.1 Collaborative PDM / cPDM

- 5.2.2 MCAD Integration PLM

- 5.2.3 Simulation and Analysis

- 5.2.4 Digital Manufacturing and MES-PLM

- 5.2.5 ALM / SLM

- 5.3 By Organisation Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By End-user Industry

- 5.4.1 Automotive and Transportation

- 5.4.2 Aerospace and Defence

- 5.4.3 Electronics and High-Tech

- 5.4.4 Industrial Machinery and Heavy Equipment

- 5.4.5 Architecture, Engineering and Construction

- 5.4.6 Life Sciences and Medical Devices

- 5.4.7 Consumer Packaged Goods / Retail

- 5.4.8 Other End-user Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia and New Zealand

- 5.5.3.6 Rest of Asia Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, Recent Developments)

- 6.4.1 Siemens AG

- 6.4.2 Dassault Systems SE

- 6.4.3 PTC Inc.

- 6.4.4 SAP SE

- 6.4.5 Autodesk Inc.

- 6.4.6 Oracle Corporation

- 6.4.7 IBM Corporation

- 6.4.8 ANSYS Inc.

- 6.4.9 Aras Corporation

- 6.4.10 Arena (SaaS by PTC)

- 6.4.11 Infor Inc.

- 6.4.12 Hexagon AB

- 6.4.13 Bentley Systems Inc.

- 6.4.14 Altair Engineering Inc.

- 6.4.15 Propel Software

- 6.4.16 IFS AB

- 6.4.17 HCLTech xLMCloud

- 6.4.18 Accenture Industry X

- 6.4.19 OpenBOM

- 6.4.20 Propulsion-PLM

- 6.4.21 Centric Software

- 6.4.22 CONTACT Software

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment