|

시장보고서

상품코드

2035004

운영 기술(OT) 보안 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Operational Technology (OT) Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

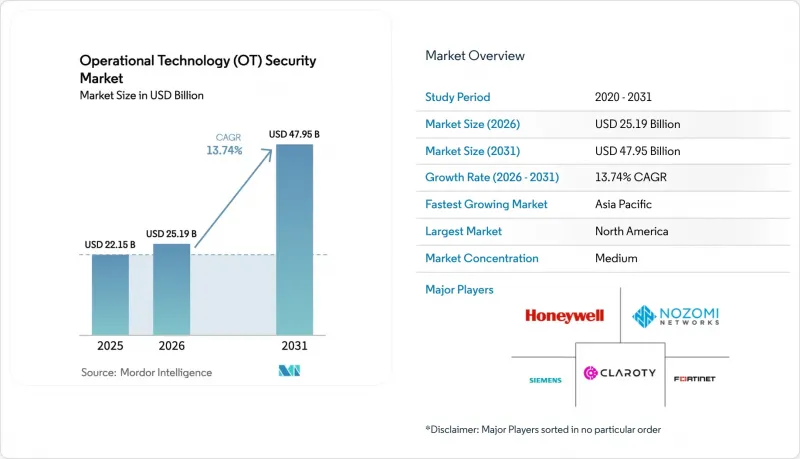

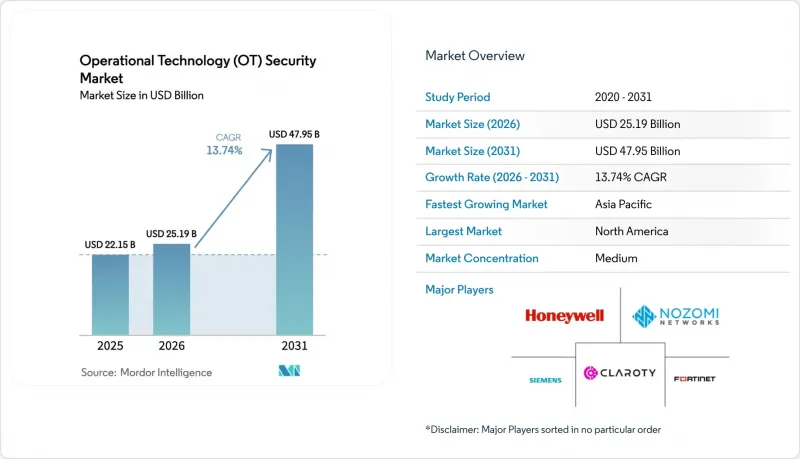

운영 기술(OT) 보안 시장 규모는 2025년 221억 5,000만 달러에서 2026년에는 251억 9,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 13.74%로 성장을 지속하여, 2031년까지 479억 5,000만 달러에 이를 것으로 예측됩니다.

중요 인프라의 광범위한 디지털화로 인해 과거에는 고립되어 있던 산업 제어 시스템이 인터넷상의 위협에 노출되어 다층적인 사이버 방어에 대한 긴급한 투자가 요구되고 있습니다. 2023년부터 2024년까지 보고된 산업 사이버 사고 중 제조업이 25.7%를 차지해 이 분야가 랜섬웨어, 와이퍼형 악성코드, 국가 지원 방해공작에 취약한 것으로 나타났습니다. 지정학적 긴장이 리스크를 증폭시켰습니다. 2024년, 국가와 연계된 그룹에 의한 에너지, 운송, 수자원 관련 자산에 대한 공격이 49% 증가했습니다. 규제 압력으로 인해 지출이 가속화되었습니다. 북미의 파이프라인 사업자들은 현재 사고 발생 후 12시간 이내에 CISA에 보고할 의무가 있으며, 이는 지속적인 모니터링 플랫폼의 도입을 촉진하고 있습니다. EU의 NIS2 지침이 공급망 전반에 걸쳐 '최첨단' 제어를 의무화함에 따라 플랫폼 통합이 가속화되고, 구매자가 개별 도구에서 통합 솔루션으로 전환하도록 유도하고 있습니다. 동시에 OT(Operational Technology)에 특화된 사이버 보안 인력의 부족으로 많은 사업자들이 AI 분석과 24시간 365일 사고 대응을 결합한 매니지드 감지 및 대응 서비스를 도입하고 있습니다.

세계 OT(Operational Technology) 보안 시장 동향 및 인사이트

중요 인프라에 대한 사이버 공격 급증

2025년 중반, 수도 유틸리티자가 400개의 무방비 웹 인터페이스를 공개한 것은 보안 대책이 적용되지 않은 산업 자산의 규모를 여실히 보여주고 있습니다. IOCONTROL과 같은 지능형 악성코드는 프로그래머블 로직 컨트롤러(PLC)를 표적으로 삼아 프로세스 변수를 은밀하게 조작할 수 있습니다. 규칙 기반 시스템에서는 이전에 보지 못한 행동을 인식하기 어려웠기 때문에 AI를 활용한 이상 징후 감지 툴의 도입이 진행되었습니다. 이번 공격은 가동 중단 외에도 연쇄적인 공급망 혼란을 일으켜 화학, 운송 등 관련 분야에도 영향을 미쳤습니다.

IT와 OT 네트워크의 융합으로 공격 대상 영역 확대

2024년, 제조업체의 80%가 기업의 IT 자원과 공장 네트워크를 통합한 후 보안 사고 증가를 경험했습니다. 클라우드 분석과 예지보전 워크로드는 생산성을 향상시켰지만, 동시에 인증 기능이 없는 레거시 프로토콜을 노출시켰습니다. IT와 OT의 전문성을 결합한 하이브리드 보안 운영 센터는 컨트롤러, 센서, 게이트웨이의 실시간 인벤토리를 유지하는 네트워크 세분화 및 자산 검색 엔진에 의해 지원되며, 전략적 필수 요건이 되었습니다.

OT 보안 플랫폼의 높은 도입 및 라이프사이클 비용

종합적인 OT 보안 프로그램에는 하드웨어 센서, 라이선스 비용, 다년간의 유지보수 계약 등 수백만 달러 규모의 지출이 필요합니다. 소규모 전력회사들은 도입 비용을 충당하기 위해 2억 5,000만 달러 규모의 '지방 및 지방 자치 단체를 위한 첨단 사이버 보안 보조금'에 의존했습니다. 맞춤형 통합과 장기간의 공장 인수 테스트는 총소유비용을 증가시키고, 과도기 동안 중요한 자산이 보호받지 못하는 단계적 배포를 촉진했습니다.

부문 분석

2025년에는 솔루션이 매출의 62.34%를 차지했습니다. 이는 자산 감지 엔진, 침입 감지 어플라이언스, 세분화 게이트웨이가 모든 OT 보안 시장 프로그램의 기반을 형성하고 있기 때문입니다. 그러나 사업자들이 사이버 인력 부족을 보완하기 위해 관리형 감지, 사고 대응, 컴플라이언스 감사에 의존함에 따라 서비스 부문은 2031년까지 연평균 복합 성장률(CAGR) 17.92%를 나타낼 것으로 예측됩니다. 현재 각 벤더들은 평균 감지 시간(MTD) 임계값을 보장하고, 24시간 SOC 모니터링을 지원하는 성과 기반 계약을 패키지로 제공합니다.

산업 기업들은 사이버 복원력을 자본 프로젝트가 아닌 운영상의 핵심성과지표(KPI)로 인식하는 경향이 강해지고 있습니다. 매니지드 OT SOC 서비스는 인력을 추가하지 않고도 확장 가능한 전문 지식을 제공하며, 전문 서비스 팀은 지멘스, ABB, 에머슨의 이기종 컨트롤러에 걸쳐 제로 트러스트 아키텍처를 맞춤화합니다. 이러한 변화는 플랫폼의 정착률을 높이는 요인으로 작용하고 있습니다. 왜냐하면 지속적인 서비스를 통해 벤더의 직원이 공장 내에 상주하게 되고, 기술 전환이 억제되어 OT 보안 시장에서의 지속적인 수익이 안정적이기 때문입니다.

초기 도입 단계에서는 지연에 대한 민감성 및 데이터 주권 관련 규제로 인해 On-Premise 구축이 주류를 이룰 것이며, 2025년에는 70.42%의 점유율을 차지할 것으로 예측됐습니다. 그러나 하이퍼스케일러들이 IEC 62443 및 ISO 27001 인증을 획득함에 따라 클라우드를 통한 분석 및 구성 관리는 CAGR 20.85%로 성장하고 있습니다. 중소 제조업체는 사용량에 따른 과금 모델을 활용하여 설비투자를 피하면서 고도화된 AI 위협 상관관계 분석 엔진을 활용하고 있습니다.

하이브리드 아키텍처가 주류가 되어 민감한 프로세스 변수는 플랜트 DMZ 내에 보관하고, 암호화된 텔레메트리 데이터는 장기적인 추세 분석, 위협 인텔리전스 강화, 포렌식 검색을 위해 클라우드 SOC로 전송되어 행동 지표로 활용되고 있습니다. 신뢰성이 높아짐에 따라 사업자들은 히스토리 백업, 펌웨어 리포지토리, 취약점 검색 워크로드를 클라우드로 이전하고 있으며, 이러한 추세는 SaaS 플랫폼으로 인한 OT(Operational Technology) 보안 시장 규모를 확대할 것으로 예측됩니다.

운영 기술(OT) 보안 시장은 구성요소(솔루션 및 서비스), 구축 형태(On-Premise 및 클라우드), 최종 사용자 산업(제조, 석유 및 가스, 전력, 운송 및 물류 등), 보안 계층(네트워크 모니터링 및 이상 징후 감지, 엔드포인트/장치 보안 등), 지역(북미, 남미, 유럽, 아시아태평양, 중동, 아프리카, 아시아태평양) 등으로 분류됩니다. 포인트/디바이스 보안 등), 지역(북미, 남미, 유럽, 아시아태평양, 중동/아프리카)으로 분류됩니다.

지역별 분석

북미는 파이프라인, 식품 가공업체 및 지방 수도국에 대한 대규모 공격으로 인해 핵심 인프라 방어에 대한 초당적 투자가 촉진된 결과, 2025년 매출의 38.15%를 차지하며 선두를 유지했습니다. TSA(Transportation Security Administration)의 지침에 따라 에너지 파이프라인 사업자는 SCADA 트래픽을 지속적으로 모니터링하고 12시간 이내에 이상 징후를 보고해야 합니다. 캐나다는 수력발전 댐을 위한 사이버 보안 프레임워크에 투자하고, 멕시코 자동차 산업 회랑에서는 SOC(보안운영센터) 아웃소싱 계약이 증가했습니다.

아시아태평양이 가장 높은 성장세를 보이며 2026년부터 2031년까지 운영 기술(OT) 보안 시장 규모가 연평균 19.75%의 성장률을 보일 것으로 예측됩니다. 중국은 5G 커넥티드 센서로 석유화학 및 철도 시스템을 현대화하고, 인도는 발전소 및 스마트시티 프로젝트에 대해 CERT-In에 사고 보고를 의무화했으며, 일본은 지정학적 혼란에 대비하여 원자력 발전소 제어 시스템을 강화했습니다. 아세안 국가들은 외국인 직접투자를 활용하여 프로젝트 초기 단계부터 IEC 62443 평가를 도입함으로써 기존 설비의 개보수에 따른 문제를 피할 수 있었습니다.

유럽에서는 NIS2 지침으로 인해 컴플라이언스 대상이 수천 개의 중견 산업 기업까지 확대되면서 꾸준한 모멘텀이 유지되고 있습니다. 독일은 Secure-by-Design(Secure-by-Design) PLC를 채택한 중소 기계 제조업체에 대한 국가 보조금을 지급하고, 영국 국가핵심인프라센터(CNIC)는 안전한 원격 액세스 게이트웨이 조달 체크리스트를 발표했으며, 이탈리아는 재생에너지 통합을 가속화하기 위해 재생에너지의 통합을 가속화하고, 안전한 인버터 텔레메트리를 요구했습니다. 동유럽의 전력회사들은 레거시 변전소 세분화를 우선순위에 두고 운영 기술(OT) 보안 시장의 지역적 수요를 증가시켰습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.05.20The operational technology security market size is expected to grow from USD 22.15 billion in 2025 to USD 25.19 billion in 2026 and is forecast to reach USD 47.95 billion by 2031 at 13.74% CAGR over 2026-2031.

Widespread digitalization of critical infrastructure exposed formerly isolated industrial control systems to internet-based threats, prompting urgent investment in layered cyber defense. Manufacturing accounted for 25.7% of reported industrial cyber incidents in 2023-2024, highlighting the sector's vulnerability to ransomware, wiper malware, and state-sponsored sabotage. Geopolitical tension compounded risk: state-aligned groups increased attacks on energy, transport, and water assets by 49% during 2024. Regulatory pressure accelerated spending; North American pipeline operators must now report incidents within 12 hours to CISA, driving uptake of continuous-monitoring platforms. Platform consolidation gained momentum because the EU NIS2 Directive requires "state-of-the-art" controls across supply chains, encouraging buyers to shift from point tools to integrated offerings. Simultaneously, the shortage of OT-specific cyber talent pushed many operators toward managed detection and response services that combine AI analytics with 24/7 incident handling.

Global Operational Technology (OT) Security Market Trends and Insights

Surge in Cyber-Attacks on Critical Infrastructure

Water utilities disclosed 400 exposed web interfaces in mid-2025, illustrating the scale of unsecured industrial assets. Sophisticated malware such as IOCONTROL targeted programmable logic controllers to enable covert manipulation of process variables. AI-driven anomaly-detection tools gained traction because rule-based systems struggled to recognize previously unseen behaviours. Beyond operational downtime, attacks produced cascading supply-chain disruption that affected adjacent sectors such as chemicals and transport.

Convergence of IT and OT Networks Expanding Attack Surface

Eighty percent of manufacturers experienced more security incidents after integrating enterprise IT resources with plant networks in 2024. Cloud analytics and predictive-maintenance workloads improved productivity but simultaneously exposed legacy protocols lacking authentication. Hybrid security operations centres that fuse IT and OT expertise became a strategic imperative, supported by network segmentation and asset-discovery engines that maintain real-time inventories of controllers, sensors, and gateways.

High Implementation and Lifecycle Cost of OT Security Platforms

Comprehensive OT security programs require multi-million-dollar outlays spanning hardware sensors, license fees, and multi-year maintenance contracts. Smaller electric utilities relied on the USD 250 million Rural and Municipal Advanced Cybersecurity Grant to offset adoption costs. Custom integration and prolonged factory-acceptance testing inflated the total cost of ownership, encouraging phased rollouts that can leave critical assets unprotected during transition.

Other drivers and restraints analyzed in the detailed report include:

- Stricter Global/Regional Regulations and Standards

- Rapid Industry 4.0 / IIoT Adoption in Process Industries

- Legacy System and Protocol Compatibility Limitations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions accounted for 62.34% revenue in 2025 because asset-discovery engines, intrusion-detection appliances, and segmentation gateways form the backbone of any operational technology security market program. However, services are rising at an 17.92% CAGR through 2031 as operators lean on managed detection, incident response, and compliance audits to offset the cyber-talent gap. Vendors now bundle outcome-based contracts that guarantee mean-time-to-detect thresholds and support around-the-clock SOC monitoring.

Industrial firms increasingly treat cyber resilience as an operational key-performance indicator rather than a capital project. Managed OT SOC offerings deliver scalable expertise without inflating headcount, while professional-services teams customize zero-trust architectures across heterogeneous controllers from Siemens, ABB, and Emerson. This shift underpins platform stickiness because continuous services embed vendor staff inside plants, discouraging technology swaps and stabilizing recurring revenue within the operational technology security market.

On-premises deployments dominated early rollouts due to latency sensitivities and data-sovereignty rules, capturing 70.42% share in 2025. Yet cloud-delivered analytics and configuration management are expanding at a 20.85% CAGR as hyperscalers achieve IEC 62443 and ISO 27001 certifications. Smaller manufacturers leverage consumption-based pricing to avoid capital expenditure while accessing advanced AI threat-correlation engines.

Hybrid architectures prevail, sensitive process variables remain inside the plant DMZ, whereas encrypted telemetry feeds behavioural indicators to cloud SOCs for long-term trending, threat-intelligence enrichment, and forensic search. As confidence grows, operators migrate historian backups, firmware repositories, and vulnerability-scanning workloads to the cloud, a trend expected to raise the operational technology security market size attributable to SaaS platforms.

Operational Technology (OT) Security Market is Segmented by Component (Solutions, and Services), Deployment Mode (On-Premise, and Cloud), End-User Industry (Manufacturing, Oil and Gas, Power Utilities, Transportation and Logistics, and More), Security Layer (Network Monitoring and Anomaly Detection, Endpoint/Device Security, and More), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa).

Geography Analysis

North America retained leadership with 38.15% of 2025 revenue after headline attacks on pipelines, food processors, and local water districts drove bipartisan investment in critical-infrastructure defense. TSA directives obligate energy-pipeline operators to continuously monitor SCADA traffic and report anomalies within 12 hours. Canada invested in cybersecurity frameworks for hydroelectric dams, while Mexican automotive corridors boosted SOC outsourcing agreements.

Asia-Pacific delivered the highest growth trajectory, with the operational technology security market size expanding at a 19.75% CAGR between 2026-2031. China modernized its petrochemical and rail systems with 5 G-connected sensors, India mandated CERT-In incident reporting for power plants and smart-city projects, and Japan reinforced its nuclear-plant control systems against geopolitical disruption. ASEAN countries leveraged foreign direct investment to incorporate IEC 62443 assessments from project inception, sidestepping legacy-retrofit challenges.

Europe maintained steady momentum as the NIS2 Directive widened compliance scope to thousands of medium-sized industrial firms. Germany established state subsidies for SME machine-builders adopting secure-by-design PLCs, the UK's Critical National Infrastructure Centre published procurement checklists for secure remote-access gateways, and Italy accelerated renewables integration, demanding secure inverter telemetry. Eastern European utilities prioritized the segmentation of legacy substations, lifting regional demand within the operational technology security market.

- Fortinet, Inc.

- Nozomi Networks Inc.

- Claroty Ltd.

- Honeywell International Inc.

- Siemens Aktiengesellschaft (Siemens AG)

- Schneider Electric SE

- Rockwell Automation, Inc.

- GE Vernova LLC

- Darktrace Holdings Limited

- Palo Alto Networks, Inc.

- Cisco Systems, Inc.

- International Business Machines Corporation

- Dragos, Inc.

- Tenable, Inc.

- Armis Security Ltd.

- Forescout Technologies, Inc.

- Check Point Software Technologies Ltd.

- Microsoft Corporation

- Waterfall Security Solutions Ltd.

- OPSWAT, Inc.

- Radiflow Ltd.

- Indegy Ltd. (now part of Tenable, Inc.)

- BAE Systems plc

- Tripwire, Inc.

- AO Kaspersky Lab

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in cyber-attacks on critical infrastructure

- 4.2.2 Convergence of IT and OT networks expanding attack surface

- 4.2.3 Stricter global/regional regulations and standards (e.g., NIS2, TSA SD02C)

- 4.2.4 Rapid Industry 4.0 / IIoT adoption in process industries

- 4.2.5 Insurance underwriting requirements linking premiums to OT-security posture

- 4.2.6 Emergence of plant-level zero-trust reference architectures

- 4.3 Market Restraints

- 4.3.1 High implementation and lifecycle cost of OT security platforms

- 4.3.2 Legacy system and protocol compatibility limitations

- 4.3.3 Budget deprioritisation at small / mid-size industrial sites

- 4.3.4 Shortage of OT-specific cyber-talent and field engineers

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape (IEC 62443, NIS2, TSA, CISA, ISA/IEC-99)

- 4.6 Technological Outlook (AI-driven anomaly detection, 5G campus networks, TSN)

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Macroeconomic Impact Assessment

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 On-Premises

- 5.2.2 Cloud

- 5.3 By End-User Industry

- 5.3.1 Manufacturing

- 5.3.2 Oil and Gas

- 5.3.3 Power Utilities

- 5.3.4 Transportation and Logistics

- 5.3.5 Chemicals and Pharma

- 5.3.6 Mining and Metals

- 5.4 By Security Layer

- 5.4.1 Network Monitoring and Anomaly Detection

- 5.4.2 Endpoint / Device Security

- 5.4.3 Identity and Access Management

- 5.4.4 Secure Remote Access and Segmentation Gateways

- 5.4.5 Governance, Risk and Compliance Platforms

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Nordics

- 5.5.3.7 Benelux

- 5.5.3.8 Russia

- 5.5.3.9 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 ASEAN

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 GCC

- 5.5.5.1.2 Turkey

- 5.5.5.1.3 Israel

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Analysis

- 6.2 Strategic Moves and Funding Landscape

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Fortinet, Inc.

- 6.4.2 Nozomi Networks Inc.

- 6.4.3 Claroty Ltd.

- 6.4.4 Honeywell International Inc.

- 6.4.5 Siemens Aktiengesellschaft (Siemens AG)

- 6.4.6 Schneider Electric SE

- 6.4.7 Rockwell Automation, Inc.

- 6.4.8 GE Vernova LLC

- 6.4.9 Darktrace Holdings Limited

- 6.4.10 Palo Alto Networks, Inc.

- 6.4.11 Cisco Systems, Inc.

- 6.4.12 International Business Machines Corporation

- 6.4.13 Dragos, Inc.

- 6.4.14 Tenable, Inc.

- 6.4.15 Armis Security Ltd.

- 6.4.16 Forescout Technologies, Inc.

- 6.4.17 Check Point Software Technologies Ltd.

- 6.4.18 Microsoft Corporation

- 6.4.19 Waterfall Security Solutions Ltd.

- 6.4.20 OPSWAT, Inc.

- 6.4.21 Radiflow Ltd.

- 6.4.22 Indegy Ltd. (now part of Tenable, Inc.)

- 6.4.23 BAE Systems plc

- 6.4.24 Tripwire, Inc.

- 6.4.25 AO Kaspersky Lab

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment