|

시장보고서

상품코드

2035042

수정 발진기 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Crystal Oscillator - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

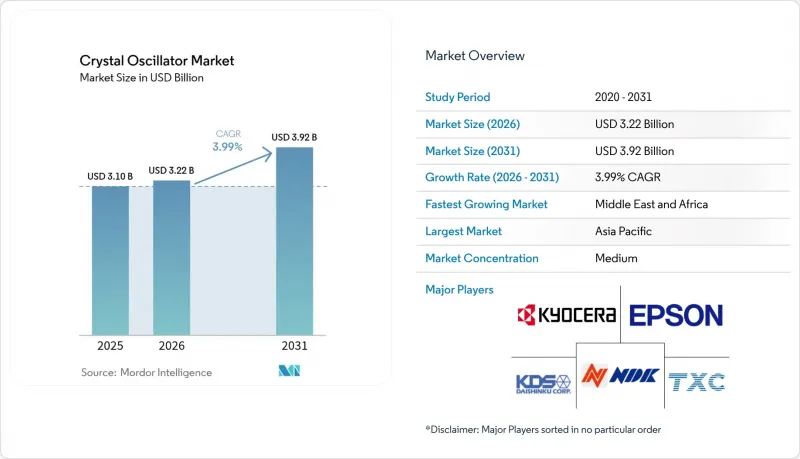

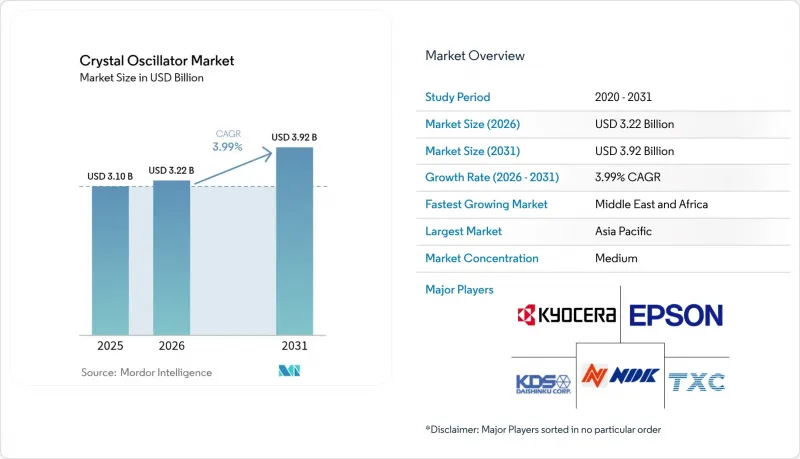

2026년 수정 발진기 시장 규모는 32억 2,000만 달러로 추정되며 2025년 31억 달러에서 확대해, 2031년에는 39억 2,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 복합 성장률(CAGR) 3.99%를 나타낼 것으로 예측됩니다.

5G 기지국, 자동차 레이더 및 정밀 산업 네트워크에서 이 기술의 확고한 역할로 인해 부품의 수명 주기가 단축되고 있음에도 불구하고 수요는 유지되고 있습니다. 5G 시분할 이중화(TDD) 셀이나 GHz 대역의 레이더 어레이와 같이 타이밍 정확도가 간섭 및 데이터 무결성 위험을 줄일 수 있는 분야에서는 채택이 가속화되고 있습니다. 저궤도(LEO) 위성에서 부피가 큰 루비듐 기준기에서 소형 오븐 제어 수정 발진기(OCXO)로의 전환이 진행되어 대상 시장 기반이 확대되고 있습니다. 웨어러블 기기 및 IoT 노드용 저전력 설계로 인해 수정 발진기 시장의 적용 범위는 1마이크로암페어 단위의 전력 소비가 중요한 에너지 수확 환경으로 확대되고 있습니다. 한편, 합성석영을 둘러싼 공급망 취약성과 RoHS 규제 대응 강화는 여전히 지속적인 역풍으로 작용하고 있습니다.

세계 수정 발진기 시장 동향 및 인사이트

초안정 TCXO를 필요로 하는 5G RRH 및 스몰셀 도입 급증

5G 네트워크에서는 업링크와 다운링크의 간섭을 방지하기 위해 1.5µs 이내의 주파수 및 위상 정합이 요구됩니다. 원격 무선 헤드(RRH)에는 현재 ±50ppb의 TCXO가 내장되어 있으며, GNSS가 스푸핑되었을 때 정밀 시간 프로토콜(PTP) 홀드오버에 의존하기 때문에 타이밍은 단순한 비용 항목에서 서비스 품질(QoS)의 안전장치로 격상되었습니다. 네트워크 사업자는 열충격에 강한 엡손의 SC 컷 수정 진동자를 지정하고, 스몰셀 공급업체는 GNSS를 사용할 수 없는 실내 사이트를 위해 기판 수준의 OCXO 백업을 통합하고 있습니다.

차량용 레이더와 ADAS의 보급이GHz 대역 OCXO 수요를 견인합니다.

77-79GHz 대역의 레이더로의 전환으로 센티미터 단위의 해상도가 가능하지만, 고스트 타겟을 피하기 위해서는 100 fs 미만의 지터를 가진 OCXO가 필요합니다. 8개 이상의 레이더 모듈을 장착한 차량은 레벨 3의 자율주행을 실현하기 위해 센서 데이터를 융합하는 코히런트 타이밍에 의존하고 있습니다. 스카이웍스의 클록 제너레이터 Si5332는 이러한 요구사항을 충족시키기 위해 ISO26262 준수 및 위상 배열 동기화 기능을 제공합니다. 장치는 AEC-Q200을 통과하고 -40°C에서 125°C의 온도 범위에서 작동해야 하기 때문에 진입장벽이 높아져 경쟁은 자동차 분야에서 풍부한 실적을 보유한 기업으로 한정되어 있습니다.

MEMS 클럭 제너레이터의 평균판매가격(ASP) 하락이 저가형 수정 발진기(XO) 시장을 잠식하고 있습니다.

SiTime의 클록 SoC는 PLL, 발진기 및 스펙트럼 확산 기능을 통합하여 기판 면적을 50% 줄이고, OEM이 여러 SPXO를 생략할 수 있도록 합니다. 수정 발진기는 여전히 MEMS의 절반의 전류로 0.18ps의 지터를 달성하지만, 유연한 주파수 메뉴와 SKU 수의 감소는 비용에 민감한 구매자를 끌어들이고 있습니다. MEMS 생산량이 증가함에 따라 범용 SPXO의 평균 판매 가격은 하락 압력을 받고 있으며, 이에 따라 수정 발진기 공급업체들은 프리미엄 OCXO 및 자동차용 제품 라인에 더욱 집중하고 있습니다.

부문 분석

2025년 TCXO 카테고리는 수정 발진기 시장의 35.78%를 차지했습니다. 이는 엄격한 예산 범위 내에서 ±100ppb의 안정성을 중시하는 통신 장비에 힘입은 결과입니다. 지속적인 소형화를 통해 ±1ppm의 성능 저하 없이 2.0×1.6 mm의 패키지 크기를 실현했습니다. 그러나 ppm 이하 수준의 홀드오버를 요구하는 LEO 위성 및 5G 엣지 서버에 힘입어 OCXO 하위 부문은 2031년까지 연평균 복합 성장률(CAGR) 4.18%로 성장을 주도할 것으로 예측됩니다. 이러한 추세에 따라 OCXO는 정밀 인프라 투자에서 수정 발진기 시장 점유율이 확대될 것으로 예측됩니다.

OCXO는 이중 오븐 설계, 복합 크리스탈 컷팅 및 디지털 온도 보상 기능을 활용하여 엡손의 OG7050CAN 시리즈에서 예열 시 전력 소비를 56% 줄였습니다. 단순 패키지형 수정 발진기(PCO)는 비용 중심의 소비재를 계속 지원하고 있으며, VCXO는 온디맨드 방식으로 주파수를 재조정해야 하는 TSN(Time Sensitive Networking) 게이트웨이에서 채택이 확대되고 있습니다. MEMS 기반 XO는 높은 BOM 비용에도 불구하고 위상 노이즈보다 실장 면적이 우선시되는 설계 프로젝트에 채택되고 있습니다. FCXO와 SAW 디바이스는 여전히 틈새 시장이며, 테스트 장비와 mm파 링크용으로 활용되고 있습니다.

2025년에는 표면 실장 패키지가 매출의 68.05%를 차지했으며, 스마트폰 및 IoT 기판의 집적도 향상에 따라 확대되고 있습니다. 자동 실장은 조립 시간을 단축하고 설계자가 PCB의 양면에 부품을 배치할 수 있게 함으로써 수정 발진기 시장에서 칩 레벨 통합으로의 전환을 가속화하고 있습니다. 스루홀 실장의 점유율은 철도 신호 모듈이나 발사체 로켓의 아비오닉스 등 진동이나 온도 구배로 인해 솔더 조인트의 강도가 위협받는 경우에 한정되어 있습니다.

기존의 국방 및 우주 프로그램에서는 현장 수리 및 기밀성을 보장하기 위해 스루홀 캔이 지정되어 있습니다. 라콘의 우주용 인증 HC45 패키지는 10년간의 에이징에서 ±0.1ppm 미만의 정확도를 유지하며, QML-V의 선별 기준을 충족합니다. 한편, 표면 실장형 로드맵 디바이스는 민수용 생산 라인에서 사용할 수 있도록 시간당 1,000 사이클의 리플로우 프로파일 테스트를 거쳤습니다. 이러한 양극화로 인해 두 가지 방식 모두 여전히 중요하지만, 전체 수정 발진기 시장에서는 픽앤플레이스에 적합한 외형을 채택한 제품에 대한 수요가 더욱 증가하고 있습니다.

지역별 분석

2025년 아시아태평양은 수정 발진기 시장 매출의 47.15%를 차지했으며, 일본의 합성 수정 오토클레이브와 중국의 PCB 실장 규모가 그 견인차 역할을 했습니다. 중국의 휴대폰 생산 부진으로 일본의 생산량은 감소했습니다. 2024년 부품 출하량은 전년 대비 25% 감소했지만, 8인치 웨이퍼 슬라이싱 능력에서 이 지역의 생산 능력은 여전히 다른 지역을 압도하고 있습니다. 중국의 국산 5G 무선기 보급은 여전히 SPXO의 대량 구매를 견인하고 있으며, 휴대폰 시장의 침체로부터 제조업체를 보호하고 있습니다. 한국과 대만은 중공정 웨이퍼 가공을 전문으로 하고 있으며, 지역 내 폐쇄형 루프 공급을 통해 발진기 1개당 물류비용을 절감하고 있습니다.

북미는 MEMS 기반 및 군용 OCXO에서 프리미엄 점유율을 차지하고 있습니다. SiTime의 실리콘 밸리 팹리스 모델은 TSMC의 MEMS 라인을 활용하고 있으며, Microchip의 뉴햄프셔에 위치한 크리스탈 공장은 Vectron 브랜드의 항공우주용 크리스탈 발진기를 생산하고 있습니다. 국방 예산과 데이터센터 업그레이드에서 가격보다 성능이 우선시되기 때문에 이 지역의 수정 발진기 시장의 평균 판매 가격 상승을 뒷받침하고 있습니다.

유럽에서는 공급망 리스크 헤지 전략에 집중하고 있습니다. QuartzCom의 스위스산 웨이퍼와 독일 R&D 클러스터가 일본 집중 리스크를 줄이고 있습니다. EU의 RoHS 규제 기한으로 인해 무연 제품 재인증이 가속화되어 현지 테스트 하우스에 서비스 수익을 가져다주고 있습니다. 중동 및 아프리카는 CAGR 5.49%로 가장 빠르게 성장하고 있으며, 2030년까지 50개의 디자인 하우스가 설립될 사우디아라비아의 2억 6,600만 달러 규모의 반도체 허브가 그 견인차 역할을 하고 있습니다. 리야드 및 두바이의 스마트 시티 구축으로 IoT 게이트웨이 및 5G 스몰셀의 고정밀 타이밍에 대한 지역적 수요가 더욱 확대되어 수정 발진기 시장의 발자취를 넓힐 것입니다. 남미는 여전히 소폭 성장에 머물러 있지만, 주로 브라질과 콜롬비아의 통신사 업그레이드가 주도하고 있습니다. 그러나 물류 거리와 업스트림 공급의 제한이 성장을 저해하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.05.20The crystal oscillator market size in 2026 is estimated at USD 3.22 billion, growing from 2025 value of USD 3.10 billion with 2031 projections showing USD 3.92 billion, growing at 3.99% CAGR over 2026-2031.

The technology's entrenched role in 5G base stations, automotive radar, and precision industrial networks sustains demand even as component lifecycles shorten. Adoption accelerates wherever timing precision mitigates interference or data-integrity risks, such as 5G Time Division Duplex cells and GHz-level radar arrays. Migrations away from bulky rubidium standards toward compact Oven-Controlled Crystal Oscillators (OCXOs) in Low Earth Orbit satellites broaden the addressable base. Power-efficient designs for wearable and IoT nodes are expanding the reach of the crystal oscillator market into energy-harvesting environments where every microampere matters. Meanwhile, supply-chain fragility around synthetic quartz and tightening RoHS compliance remain persistent headwinds.

Global Crystal Oscillator Market Trends and Insights

Surge in 5G RRH and Small-Cell Deployments Requiring Ultra-Stable TCXOs

5G networks demand frequency and phase alignment within 1.5 µs to prevent uplink-downlink interference. Remote Radio Heads now embed +-50 ppb TCXOs and rely on Precision Time Protocol holdover when GNSS is spoofed, elevating timing from a cost line item to a quality-of-service safeguard. Network operators specify SC-cut crystal units from Epson that survive thermal shock, while small-cell vendors integrate board-level OCXO backups for indoor sites where GNSS is unavailable.

Automotive Radar and ADAS Uptake Driving GHz-Level OCXO Demand

The shift to 77-79 GHz radar enables centimeter-scale resolution but necessitates OCXOs with sub-100 fs jitter to avoid ghost targets. Vehicles hosting eight or more radar modules depend on coherent timing to fuse sensor data for Level-3 autonomy. Skyworks' Si5332 clock generator delivers ISO26262 compliance and phased-array synchronization to meet this requirement. Entry barriers rise because devices must pass AEC-Q200 and function from -40 °C to 125 °C, limiting competition to firms with deep automotive pedigrees.

MEMS Clock-Generator ASP Erosion Cannibalising Low-End Quartz XOs

SiTime's Clock-SoC integrates PLLs, resonators, and spread-spectrum functions, shrinking board area by 50% and letting OEMs drop multiple SPXOs. Although quartz still delivers 0.18 ps jitter at half the current of MEMS, the flexible frequency menu and reduced SKU count entice cost-sensitive buyers. Average selling prices on commodity SPXOs face down-pressure as MEMS volume grows, prompting quartz suppliers to double down on premium OCXO and automotive lines.

Other drivers and restraints analyzed in the detailed report include:

- Migration from Rubidium to High-Stability OCXOs in Space-Constrained LEO Satellites

- Rapid Proliferation of Wearable/IoT Nodes Mandating Miniature SPXOs and MEMS-XO Hybrids

- Supply-Chain Fragility of Synthetic Quartz Wafers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The TCXO category held a 35.78% slice of the crystal oscillator market in 2025, supported by telecom equipment that values +-100 ppb stability within tight budgets. Continuous miniaturization now reaches 2.0 X 1.6 mm packages without sacrificing +-1 ppm performance. However, the OCXO subsegment leads growth at 4.18% CAGR to 2031, fueled by LEO satellites and 5G edge servers demanding sub-ppm holdover. These trends position OCXOs to capture a larger share of the crystal oscillator market size for precision infrastructure spending.

OCXOs leverage double-oven designs, composite crystal cuts, and digital temperature compensation to slash warm-up power by 56% in Epson's OG7050CAN series. Simple Packaged Crystal Oscillators keep cost-driven consumer goods ticking, while VCXOs gain in Time-Sensitive Networking gateways that must retune frequency on demand. MEMS-based XOs command design wins where footprint trumps phase noise, despite higher BOM cost. FCXOs and SAW devices remain niche, serving test equipment and mm-wave links.

Surface-mount packages owned 68.05% revenue in 2025 and expand alongside smartphone and IoT board densities. Automated placement trims assembly minutes and frees designers to stack components on both PCB sides, reinforcing the crystal oscillator market's shift toward chip-level integration. The through-hole share persists only where vibration or thermal gradients threaten solder-joint integrity, such as rail-signaling modules or launch-vehicle avionics.

Legacy defense and space programs specify through-hole cans for field repairs and hermeticity. Rakon's space-qualified HC45 package offers 10-year aging below +-0.1 ppm, meeting QML-V screening levels. Meanwhile, surface-mount roadmap devices test 1,000-cycle-per-hour reflow profiles to endure consumer production lines. The dichotomy ensures both schemes stay relevant, although volume tilts further toward pick-and-place friendly outlines across the wider crystal oscillator market.

The Crystal Oscillator Market Report is Segmented by Crystal Type (Temperature-Compensated (TCXO), Oven-Controlled (OCXO), Voltage-Controlled (VCXO), and More), Mounting Scheme (Surface-Mount, and Thru-Hole), Crystal Cut (AT-Cut, BT-Cut, SC-Cut, and More), End-User Industry (Consumer Electronics, Telecom and Networking, Aerospace and Defense, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific held 47.15% of crystal oscillator market revenue in 2025, anchored by Japan's synthetic quartz autoclaves and China's PCB assembly scale. Japanese volumes dipped on weak Chinese handset output, with parts shipments down 25% year-on-year in 2024, yet regional capacity remained unrivaled for 8-inch wafer slicing. China's push for indigenous 5G radios still drives bulk SPXO purchases, cushioning producers against handset softness. South Korea and Taiwan specialize in midstream wafer processing, enabling regional closed-loop supply that lowers logistics cost per oscillator.

North America commands premium share in MEMS-based and military-grade OCXOs. SiTime's Silicon Valley fabless model co-opts TSMC MEMS lines, while Microchip's New Hampshire crystal plant supports Vectron-labelled aerospace cans. Defense budgets and datacenter upgrades prioritize performance over price, thus supporting higher average selling prices within the regional crystal oscillator market.

Europe concentrates on supply-chain hedge strategies. QuartzCom's Swiss wafers and Germany's R&D clusters mitigate Japan concentration risk. EU RoHS deadlines accelerate lead-free requalifications, creating services revenue for local test houses. Middle East and Africa advance fastest at 5.49% CAGR, spearheaded by Saudi Arabia's USD 266 million semiconductor hub forming 50 design houses by 2030. Smart-city rollouts in Riyadh and Dubai further expand regional demand for precise timing in IoT gateways and 5G small cells, broadening the crystal oscillator market footprint. South America remains modest, driven mainly by carrier upgrades in Brazil and Colombia, but logistic distances and limited upstream supply temper growth.

- Seiko Epson Corporation

- Kyocera Corporation

- Nihon Dempa Kogyo (NDK) Co. Ltd

- Daishinku Corp.

- TXC Corporation

- SiTime Corporation

- Rakon Ltd

- Vectron International (Microchip)

- Siward Crystal Technology Co. Ltd

- Hosonic Electronic Co. Ltd

- Fox Electronics

- CTS Corporation

- Abracon LLC

- ECS Inc.

- Micro Crystal AG

- Jauch Quartz GmbH

- Statek Corporation

- River Eletec Corporation

- Mercury Electronic Ind Co. Ltd

- Raltron Electronics Corporation

- Aker Technology Co. Ltd

- NEL Frequency Controls Inc.

- WTL Frequency Products Co. Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in 5G RRH and Small-Cell Deployments Requiring Ultra-Stable TCXOs

- 4.2.2 Automotive Radar and ADAS Uptake Driving GHz-level OCXO Demand

- 4.2.3 Migration from Rubidium to High-Stability OCXOs in Space-Constrained LEO Satellites

- 4.2.4 Rapid Proliferation of Wearable/IoT Nodes Mandating Miniature SPXOs and MEMS-XO Hybrids

- 4.2.5 Factory-Floor Digitalisation (Industry 4.0) Elevating VCXO Use in Time-Sensitive Networking

- 4.2.6 Military Conversion to Software-Defined Radios Boosting SC-Cut OCXO Procurement

- 4.3 Market Restraints

- 4.3.1 MEMS Clock-Generator ASP Erosion Cannibalising Low-End Quartz XOs

- 4.3.2 Supply-Chain Fragility of Synthetic Quartz Wafers (Japan-Centric)

- 4.3.3 High-Temperature Drift Limiting XO Adoption in SiC-Based Powertrains

- 4.3.4 Stringent EU RoHS Lead-Free Solder Windows Raising Requalification Cost

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Trends on the Crystal Oscillator Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Crystal Type

- 5.1.1 Temperature-Compensated (TCXO)

- 5.1.2 Oven-Controlled (OCXO)

- 5.1.3 Voltage-Controlled (VCXO)

- 5.1.4 Simple Packaged (SPXO)

- 5.1.5 Frequency-Controlled (FCXO)

- 5.1.6 MEMS-Based Crystal Oscillators

- 5.1.7 Other Crystal Types

- 5.2 By Mounting Scheme

- 5.2.1 Surface-Mount

- 5.2.2 Thru-Hole

- 5.3 By Crystal Cut

- 5.3.1 AT-Cut

- 5.3.2 BT-Cut

- 5.3.3 SC-Cut

- 5.3.4 Others (IT-CUT, FC-Cut)

- 5.4 By End-user Industry

- 5.4.1 Consumer Electronics

- 5.4.2 Telecom and Networking

- 5.4.3 Automotive

- 5.4.4 Aerospace and Defense

- 5.4.5 Industrial Automation

- 5.4.6 Medical and Healthcare

- 5.4.7 Research and Measurement

- 5.4.8 Other Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Nordics

- 5.5.2.5 Rest of Europe

- 5.5.3 South America

- 5.5.3.1 Brazil

- 5.5.3.2 Rest of South America

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South-East Asia

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Gulf Cooperation Council Countries

- 5.5.5.1.2 Turkey

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Seiko Epson Corporation

- 6.4.2 Kyocera Corporation

- 6.4.3 Nihon Dempa Kogyo (NDK) Co. Ltd

- 6.4.4 Daishinku Corp.

- 6.4.5 TXC Corporation

- 6.4.6 SiTime Corporation

- 6.4.7 Rakon Ltd

- 6.4.8 Vectron International (Microchip)

- 6.4.9 Siward Crystal Technology Co. Ltd

- 6.4.10 Hosonic Electronic Co. Ltd

- 6.4.11 Fox Electronics

- 6.4.12 CTS Corporation

- 6.4.13 Abracon LLC

- 6.4.14 ECS Inc.

- 6.4.15 Micro Crystal AG

- 6.4.16 Jauch Quartz GmbH

- 6.4.17 Statek Corporation

- 6.4.18 River Eletec Corporation

- 6.4.19 Mercury Electronic Ind Co. Ltd

- 6.4.20 Raltron Electronics Corporation

- 6.4.21 Aker Technology Co. Ltd

- 6.4.22 NEL Frequency Controls Inc.

- 6.4.23 WTL Frequency Products Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment