|

시장보고서

상품코드

2035058

폴리부틸렌 테레프탈레이트(PBT) 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Polybutylene Terephthalate (PBT) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

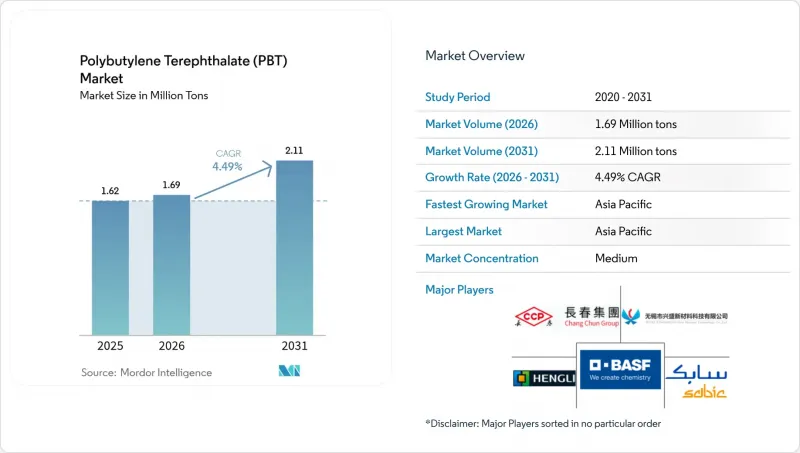

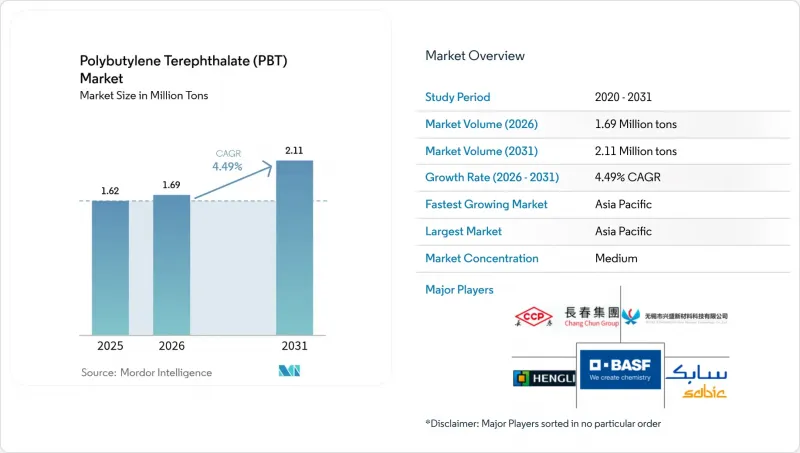

2026년 폴리부틸렌 테레프탈레이트(PBT) 시장 규모는 169만 톤으로 추정되며 2025년 162만 톤에서 확대해, 2031년에는 211만 톤에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 복합 성장률(CAGR) 4.49%를 나타낼 것으로 예측됩니다.

이러한 전망은 폴리부틸렌 테레프탈레이트가 치수 안정성, 내습성 및 다양한 첨가제 배합이 가능한 특성을 결합하여 엔지니어링 열가소성 수지 시장에서 시장 규모를 주도하고 있다는 것을 입증합니다. 이러한 모멘텀은(1) 세계 자동차 플랫폼의 적극적인 전동화 목표,(2) 공장 자동화에서 데이터 전송 속도의 기하급수적 증가,(3) 소비자 가전제품의 난연성 규제 강화,(4) 재생 엔지니어링 수지의 사용을 촉진하는 공공 정책적 인센티브 등 네 가지 거시적 요인의 시너지 효과에 기인합니다. 이 네 가지 요인이 결합하여 폴리부틸렌 테레프탈레이트(PBT) 시장의 중요성은 전통적인 엔진룸 내 응용 분야뿐만 아니라 고성능 배터리 팩, 고속 커넥터 및 정밀 산업용 기어 하우징으로 확대되고 있습니다. 제조업체들은 1,4-부탄디올 및 유리섬유 공급에 대한 수직계열화를 전략의 축으로 삼고 있으며, OEM 업체들은 물류 리스크를 줄이기 위해 현지에서의 확실한 컴파운딩을 중요시하고 있습니다. 이러한 추세로 인해 아시아태평양의 새로운 생산능력 증설에도 불구하고 지역 간 가격 차이는 좁게 유지되고 있습니다.

세계 폴리부틸렌 테레프탈레이트(PBT) 시장 동향과 인사이트

산업 자동화에서 고속 데이터 커넥터의 급속한 확산

산업 자동화 장비는 직렬 필드버스 아키텍처에서 멀티 기가비트 이더넷으로 전환하고 있으며, 이러한 전환으로 인해 공장 라인당 고주파 구리선 및 광섬유 인터페이스의 수가 두 배로 증가했습니다. 커넥터 하우징은 80°C에 가까운 연속적인 주변 온도에서 유전체 무결성을 보장하고, 기계유에 의한 오염을 견딜 수 있어야 하며, 반복적인 고온 및 저온 사이클을 견뎌내야 합니다. 유리섬유 강화 UL 94 V-0 폴리부틸렌 테레프탈레이트는 필요한 치수 안정성을 제공하고, 플러그 앤 플레이가 가능한 IP67 커넥터를 구현하여 기계 가동 중단 위험을 줄입니다. 일본과 독일의 기계 제조업체들은 IEC 61076의 상호 연결 규정을 준수하기 위해 무할로겐 PBT 하우징을 표준화하고 있으며, 이로 인해 폴리부틸렌 테레프탈레이트 시장은 차세대 로봇 하네스의 기본 재료로 자리 매김하고 있습니다. 예지보전용 센서가 모든 로봇의 관절에 도입되면서 수요 증가는 더욱 가속화되고 있으며, 각 관절에는 1만회 이상의 비틀림 사이클을 견딜 수 있고 미세한 균열이 발생하지 않는 소형 오버몰드 PBT 커넥터가 요구되고 있습니다.

EV 배터리 팩 부품에서 아시아에서 PA66에서 PBT로의 전환 가속화

중국, 한국, 베트남의 전기자동차 배터리 제조업체들은 현재 모듈 프레임, 냉각수 매니폴드, 전압 감지 커넥터에서 흡습성이 낮고, 전해액에 대한 내성이 우수하며, 125°C에서 급속 충전 시 치수 변화가 적다는 이유로 PA66보다 PBT를 지정하고 있습니다. 셀-투-팩 설계에서는 하우징이 고에너지 셀에 가까워지기 때문에 이러한 요구사항이 더욱 중요해집니다. 미국의 Tier 1 공급업체들도 이에 발맞추어 멕시코에서 배터리 부품 생산을 현지화함으로써 아시아 생산자들이 국내 가격 변동에 영향을 덜 받는 태평양 횡단 수요의 교량 역할을 하고 있습니다. 전기 이륜차의 단주기 플랫폼 혁신은 지속적인 배합 개선을 더욱 촉진하여 PBT를 보다 광범위한 모빌리티 분야에 정착시키고 있습니다.

바이오 유래 숙신산 공급과 연동된 1,4-부탄디올 가격의 변동성

폴리부틸렌 테레프탈레이트(PBT)의 중합은 안정적인 부탄디올 공급에 달려 있습니다. 바이오 유래의 제조 루트는 저탄소이지만 여전히 소수의 발효 공장에 집중되어 있어 원료인 설탕의 순도가 떨어지면 몇 주 동안 가동이 중단될 수 있으며, 현물 시장에서 급격한 가격 상승을 유발할 수 있습니다. 중국 PBT 업체들은 2024년 수익률을 지키기 위해 반응기 가동률을 낮추는 방식으로 대응했지만, EV용 사출성형 주문이 정점에 달한 바로 그 시기에 수지 공급이 타이트해져 수지 공급이 부족해졌습니다. 자체 생산 BDO가 없는 일반 가공업체는 납기 지연을 겪었고, 그 영향은 전자제품 생산 일정에까지 파급되었습니다. 중동의 석유화학 BDO 신규 생산능력은 2026년까지 가격 압력을 완화시킬 것으로 예상되지만, 당분간 가격 변동으로 인해 폴리부틸렌 테레프탈레이트 시장의 CAGR 전망치는 0.8% 하향 조정될 것으로 예측됩니다.

부문 분석

개질 등급 부문은 총 생산량의 68.15%를 차지하며 2031년까지 연평균 복합 성장률(CAGR) 4.87%를 나타낼 것으로 예측되어 폴리부틸렌 테레프탈레이트 시장에서 중심적인 위치를 차지할 것으로 예측됩니다. 유리 함량 30%에서는 인장탄성률이 10 GPa를 초과하고, HDT가 210°C에 가까워지며, 95°C의 냉각수 급증을 크리프 없이 견뎌야 하는 EV용 엔진룸 내 인버터 커버가 가능해집니다. 인계 난연제 배합은 0.4 mm 두께로 UL 94 V-0 표준을 달성하고 유동성 저하가 거의 없습니다. 이는 0.25초의 사이클 타임으로 캐비티 충진율을 향상시키고, 게이트 압력을 12MPa 낮춘 획기적인 성과입니다. 따라서, 개질 등급은 고밀도 기판 간 커넥터의 우선순위 재료로 확고히 자리매김하여 이 서브 클래스의 폴리부틸렌 테레프탈레이트 시장 규모를 확대하는 데 기여하고 있습니다.

미개질 PBT는 기계적 강도보다 광학적인 투명성이나 식품 접촉 시 순도가 우선시되는 분야에서 여전히 중요한 위치를 차지하고 있습니다. 의료용 주사기 플런저는 낮은 추출물을 활용하고 있으며, 적층조형용 필라멘트는 결정화 속도가 느리다는 특성을 활용하여 휨이 없는 시제품을 제작하고 있습니다. 그러나 OEM의 기술 사양이 엄격해짐에 따라 점유율은 점차 감소하고 있으며, 증가하는 수요는 개질 등급으로 이동하고 있습니다. 이에 따라 컴파운더들은 바이오 유래 숙신산 BDO를 배합하여 미개질 등급에 지속가능성이라는 매력을 부여함으로써 광범위한 폴리부틸렌 테레프탈레이트 시장 내에서 작지만 안정적인 틈새 시장을 강화하고 있습니다.

폴리부틸렌 테레프탈레이트(PBT) 시장 보고서는 제품 유형(비개질 PBT 및 개질 PBT), 최종 사용자 산업(자동차, 전기 및 전자, 산업 및 기계, 기타), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카) 별로 분류되어 있습니다. 시장 예측은 수량(톤) 및 금액(USD)으로 제공됩니다.

지역별 분석

아시아태평양은 소비량의 68.30%를 차지하고 있으며, 2031년까지 4.84%의 가장 높은 CAGR을 나타낼 것으로 예측됩니다. 이는 이 지역 내 단량체, 고분자 및 화합물 생산 능력의 독보적인 통합을 반영합니다. 충칭의 최근 확장은 생분해성 공중합체를 대상으로 포장 최종 시장을 개척하는 데 초점을 맞추었습니다. 이러한 규모는 비용 리더십을 보장하고, 전자 및 EV 공급망과의 근접성은 현지 인수를 보장하여 폴리부틸렌 테레프탈레이트 시장에서의 지역적 우위를 유지할 수 있습니다.

북미에서는 반도체 리쇼어링과 EV용 배터리의 현지 생산으로 공급라인이 단축되어 수요가 확대되고 있습니다. 생산업체들은 풍부한 셰일가스 유래의 제품별 원가 경쟁력 있는 원료로 활용하고 있으며, 미국 및 멕시코의 자동차 OEM 업체들이 커넥터 수요의 지속적인 확대를 주도하고 있습니다. 캐나다의 재생 소재 함유량에 대한 규제 압력으로 인해 화학적 재활용에 대한 투자가 진행되고 있으며, 2027년까지 북미 최초의 폐쇄형 PBT(폴리부틸렌 테레프탈레이트) 공급망이 구축될 가능성이 있습니다. 이를 통해 폴리부틸렌 테레프탈레이트 시장에서의 차별화를 더욱 강화할 수 있을 것입니다.

유럽에서 내연기관(ICE) 자동차의 회복세가 둔화되고 있는 가운데, 유럽은 여전히 바이오 원료 및 폐수지(PCR) 관련 기술 실증 장소로서 중요한 역할을 하고 있습니다. 유럽의 컴파운더들은 분자량을 유지하는 용매 기반 용해 재활용을 시범적으로 도입하고 있으며, 2028년까지 산업 폐기물의 30%를 회수하는 것을 목표로 하고 있습니다. 이러한 지속가능성에 대한 노력은 총 생산량 감소에도 불구하고 이 지역의 프리미엄급 제품 공급 점유율을 강화하는 데 기여하고 있습니다. 남미, 중동 및 아프리카 3개 지역은 신흥 자동차 조립 거점 및 통신 인프라 확대와 관련된 잠재력을 가지고 있어 향후 폴리부틸렌 테레프탈레이트(PBT) 시장 점유율 분포가 다양화될 가능성을 시사하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측(금액 및 수량)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

제8장 CEO을 위한 중요 전략적 과제 :

JHS 26.05.20Polybutylene Terephthalate market size in 2026 is estimated at 1.69 million tons, growing from 2025 value of 1.62 million tons with 2031 projections showing 2.11 million tons, growing at 4.49% CAGR over 2026-2031.

This baseline underscores the polybutylene terephthalate market size leadership in engineering thermoplastics that combine dimensional stability, moisture resistance, and the ability to accept a broad additive portfolio. Momentum stems from the convergence of four macro forces: (1) aggressive electrification targets in global vehicle platforms, (2) exponential growth in factory-automation data rates, (3) tightening flame-retardant regulations in consumer devices, and (4) public-policy incentives for recycled engineering-resin content. Together they expand the polybutylene terephthalate market's relevance beyond its legacy under-hood presence toward high-performance battery-pack, high-speed connector, and precision industrial gear housings. Producer strategies pivot around vertical integration into 1,4-butanediol and glass-fiber supply, while OEMs prize secure local compounding to de-risk logistics, a dynamic that keeps regional pricing spreads narrow despite fresh Asia-Pacific capacity.

Global Polybutylene Terephthalate (PBT) Market Trends and Insights

Rapid Adoption of High-Speed Data Connectors in Industrial Automation

Industrial-automation equipment is shifting from serial field-bus architectures to multi-gigabit deterministic Ethernet, a transition that multiplies the number of high-frequency copper and fiber-optic interfaces per factory line. Connector housings must guarantee dielectric integrity at continuous ambient temperatures near 80 °C, resist machine-oil contamination, and tolerate repetitive hot-cold cycles. Glass-fiber reinforced UL 94 V-0 polybutylene terephthalate delivers the requisite dimensional stability, enabling plug-and-play IP67 connectors that cut machine-downtime risk. Japanese and German machine builders standardize on halogen-free PBT housings to comply with IEC 61076 cross-mating rules, positioning the polybutylene terephthalate market as the default material in next-generation robotics harnesses. Volume growth further accelerates as predictive-maintenance sensors migrate into every robotic joint, each demanding miniature over-molded PBT connectors that survive 10,000+ torsion cycles without micro-cracks.

Asia's Accelerating Shift from PA66 to PBT in EV Battery-Pack Components

Electric-vehicle battery manufacturers in China, South Korea, and Vietnam now specify PBT over PA66 for module frames, coolant manifolds, and voltage-sensing connectors owing to lower moisture uptake, superior electrolyte resistance, and tighter dimensional change across 125 °C fast-charge excursions. Cell-to-pack designs amplify these requirements because housings sit closer to high-energy cells. . American Tier-1 suppliers follow suit as they localize battery-component production in Mexico, creating a trans-Pacific demand bridge that cushions Asian producers against domestic price swings. Short-cycle platform refreshes in electric two-wheelers further support recurring formulation upgrades, embedding PBT into a wider mobility universe.

Volatility of 1,4-Butanediol Prices Linked to Bio-Succinic Acid Supply

Polybutylene terephthalate polymerization hinges on stable butanediol supply. Bio-based routes, though lower-carbon, remain concentrated in a handful of fermentation plants that can shut down for weeks when feed-sugar purity drifts, creating sudden spot-market spikes. Chinese PBT producers responded in 2024 by trimming reactor rates to protect margins, easing resin availability just as EV injection-molding orders peaked. Merchant converters without captive BDO faced delivery delays that rippled into electronics production schedules. While new petrochemical BDO capacity in the Middle East will reduce price stress by 2026, interim volatility lops 0.8 percentage points off the polybutylene terephthalate market CAGR trajectory.

Other drivers and restraints analyzed in the detailed report include:

- Mainstream Auto Lightweighting and Metal-Replacement Trend

- Rising Demand for Halogen-Free FR Grades in Consumer Electronics

- Slower-Than-Expected European ICE Vehicle Production Recovery

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The modified-grade segment accounts for 68.15% of the overall volume and is on track for a 4.87% CAGR to 2031, underscoring its centrality to the polybutylene terephthalate market. At 30% glass loading, the tensile modulus climbs beyond 10 GPa while the HDT approaches 210 °C, enabling under-hood EV inverter covers that must withstand a 95 °C coolant surge without creep. Phosphorus-based flame-retardant formulations achieve a UL 94 V-0 rating at 0.4 mm with only marginal loss in flow, a breakthrough that enhances cavity-fill rates in 0.25 s cycle times and lowers gate pressures by 12 MPa. Modified grades, therefore, cement preferred-material status in high-density board-to-board connectors, fueling the polybutylene terephthalate market size for this subclass.

Unmodified PBT, retaining relevance where optical clarity or food-contact purity trumps mechanical strength. Medical syringe plungers exploit their low extractables, and additive-manufacturing filaments capitalize on their slow-crystallization window to build warp-free prototypes. Yet share slips incrementally as OEM engineering specifications escalate, channeling incremental demand into modified options. Compounders counter by blending bio-succinic BDO to grant unmodified grades sustainability appeal, reinforcing a modest but stable niche within the broader polybutylene terephthalate market.

The Polybutylene Terephthalate Market Report is Segmented by Product Type (Unmodified PBT and Modified PBT), End-User Industry (Automotive, Electrical and Electronics, Industrial and Machinery, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons) and Value (USD).

Geography Analysis

The Asia-Pacific region accounts for 68.30% of consumption and is forecast to record the fastest 4.84% CAGR through 2031, reflecting the unparalleled integration of monomer, polymer, and compound capacity within the region. The recent expansions in Chongqing are targeted at biodegradable copolymers that unlock packaging end-markets. Such scale secures cost leadership while proximity to electronics and EV supply chains guarantees local offtake, preserving regional dominance in the polybutylene terephthalate market.

Demand in North America is growing as semiconductor reshoring and EV-battery localization compact supply lines. Producers exploit abundant shale-gas derivatives for cost-competitive feedstock, and automotive OEMs in the United States and Mexico drive sustained connector demand. Canadian regulatory pressure for recycled content prompts chemical-recycling investments that may yield the continent's first closed-loop PBT stream by 2027, enhancing differentiation in the polybutylene terephthalate market.

Despite sluggish ICE vehicle recovery in Europe, the region remains a technology testbed for bio-based feedstock and post-consumer resin initiatives. Continental compounders pilot solvent-based dissolution recycling that retains molecular weight, aiming to recapture 30% of post-industrial waste by 2028. These sustainability advances bolster the region's premium-grade supply share, even as overall volume languishes. South America, the Middle-East and Africa, together, have potential tied to emerging automotive assembly hubs and expanding telecommunications infrastructure, hinting at future diversification of the polybutylene terephthalate market share distribution.

- BASF SE

- Celanese Corporation

- Chang Chun Group

- Evonik Industries AG

- Hengli Group Co. Ltd.

- Kolon Plastics Inc.

- LANXESS AG

- LG Chem Ltd.

- Mitsubishi Chemical Group Corporation

- Nan Ya Plastics Corporation

- Polyplastics Co. Ltd.

- SABIC

- Toray Industries Inc.

- Wuxi Xingsheng New Material Technology Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid adoption of high-speed data connectors in industrial automation

- 4.2.2 Asia's accelerating shift from PA66 to PBT in EV battery-pack components

- 4.2.3 Mainstream auto lightweighting and metal-replacement trend

- 4.2.4 Rising demand for halogen-free FR grades in consumer electronics

- 4.2.5 Government incentives for recycled engineering plastics content

- 4.3 Market Restraints

- 4.3.1 Volatility of 1,4-butanediol prices linked to bio-succinic acid supply

- 4.3.2 Slower-than-expected European ICE vehicle production recovery

- 4.3.3 Tight global glass-fiber supply impacting reinforced-PBT cost

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of Substitutes

- 4.6.4 Competitive Rivalry

- 4.6.5 Threat of New Entrants

- 4.7 End-use Sector Trends

- 4.7.1 Aerospace (Aerospace Component Production Revenue)

- 4.7.2 Automotive (Automobile Production)

- 4.7.3 Building and Construction (New Construction Floor Area)

- 4.7.4 Electrical and Electronics (Electrical and Electronics Production Revenue)

- 4.7.5 Packaging(Plastic Packaging Volume)

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Product Type

- 5.1.1 Unmodified PBT

- 5.1.2 Modified PBT

- 5.2 By End-User Industry

- 5.2.1 Automotive

- 5.2.2 Electrical and Electronics

- 5.2.3 Industrial and Machinery

- 5.2.4 Others

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 Australia

- 5.3.1.6 Malaysia

- 5.3.1.7 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 Canada

- 5.3.2.2 Mexico

- 5.3.2.3 United States

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 France

- 5.3.3.3 Italy

- 5.3.3.4 United Kingdom

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Nigeria

- 5.3.5.4 South Africa

- 5.3.5.5 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 BASF SE

- 6.4.2 Celanese Corporation

- 6.4.3 Chang Chun Group

- 6.4.4 Evonik Industries AG

- 6.4.5 Hengli Group Co. Ltd.

- 6.4.6 Kolon Plastics Inc.

- 6.4.7 LANXESS AG

- 6.4.8 LG Chem Ltd.

- 6.4.9 Mitsubishi Chemical Group Corporation

- 6.4.10 Nan Ya Plastics Corporation

- 6.4.11 Polyplastics Co. Ltd.

- 6.4.12 SABIC

- 6.4.13 Toray Industries Inc.

- 6.4.14 Wuxi Xingsheng New Material Technology Co.

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment