|

시장보고서

상품코드

2035067

산업용 가스 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Industrial Gas - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

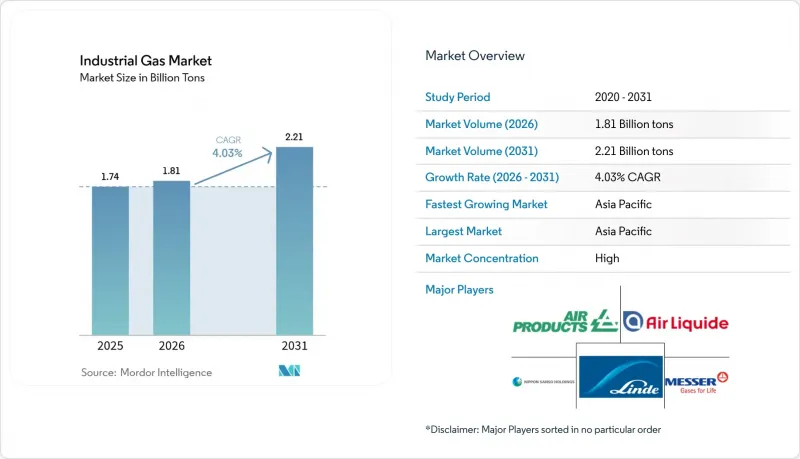

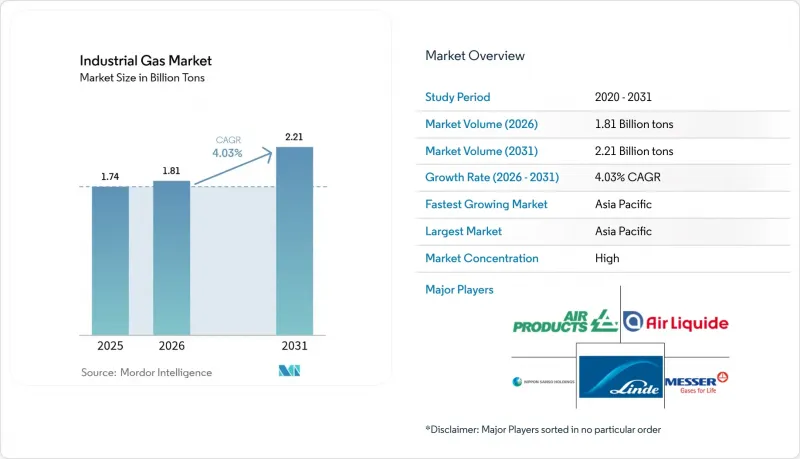

산업용 가스 시장 규모는 2025년 17억 4,000만 톤에서 2026년에는 18억 1,000만 톤으로 확대되어 2026년부터 2031년까지 CAGR 4.03%로 성장을 지속하여, 2031년까지 22억 1,000만 톤에 이를 것으로 예측됩니다.

철강, 반도체, 화학업체들의 견조한 수요가 이러한 성장을 뒷받침하고 있으며, 그린 수소, 고순도 산소, 식품용 이산화탄소를 둘러싼 제품 혁신으로 양적 확대보다 가치 창출이 앞서고 있습니다. 생산자들은 물류 리스크를 줄이기 위해 현장 공급 모델을 강화하고 있으며, 대규모 에너지 소비 기업들은 전력 비용을 고정하는 수십 년간공급 계약을 체결하고 있습니다. 반도체 제조의 지역적 분산화로 인해 고순도 질소 및 아르곤 수요는 미국과 유럽으로 이동하고 있지만, 아시아는 여전히 총 공급량에서 선도적인 위치를 유지하고 있습니다. 동시에 헬륨 회수 프로젝트, 탄소 포집 사업 및 소형 공기 분리 장치는 기존 기업과 인프라 투자자 모두로부터 새로운 자본을 유치하고 있습니다.

세계 산업용 가스 시장 동향 및 인사이트

신흥국의 급속한 산업화

아시아 전역, 특히 중국과 인도의 견조한 제조업 성장으로 산소와 질소 등 범용 가스의 기저부하 수요가 증가하고 있습니다. 서인도만 하더라도 제철소, 석유화학 클러스터, 비료단지가 밀집되어 있으며, 이들이 함께 지역 기반의 공기분리 능력을 뒷받침하고 있습니다. 지역 당국은 'Make in India' 우대 정책을 추진하고 있으며, 고순도 질소 및 아르곤을 사용하는 전자제품 조립, 태양전지 생산, 전기자동차 공급망에 대한 투자를 장려하고 있습니다. 지하철에서 신규 정유시설에 이르는 병행 인프라 프로젝트는 패키지 배송과 마이크로 벌크 배송에 적합한 분산형 수요 거점을 확대되고 있습니다. 미국 에너지정보국(EIA)은 2050년까지 아시아의 천연가스 소비량이 3배로 증가할 것으로 예측하고 있으며, 그 중 80%가 산업용으로 공급될 것으로 예상하고 있습니다. 이는 공정 가스 수요의 규모를 나타내는 지표가 됩니다.

그린수소 추진으로 현장 전기분해 계약 체결 주도

탈탄소화 목표에 따라 저탄소 수소의 도입이 가속화되고 있으며, 화학, 철강 및 중량물 운송 사업자들은 장기 공급 계약을 체결하고 있습니다. 에어프로덕츠는 ACWA Power 및 NEOM과 협력하여 사우디에 85억 달러 규모의 재생가능 에너지를 이용한 전해 플랜트를 개발하고 있으며, 연간 65만 톤의 그린 암모니아 원료를 공급할 예정입니다. 유럽연합(EU), 호주, 미국에서도 유사한 계약에 따른 프로젝트가 건설 중이며, 계획 생산량은 총 110만 톤을 초과할 것으로 예측됩니다. 이들 프로젝트는 질소(불활성화를 위한), 산소(제품별) 등 관련 가스 수요를 늘리고, 트럭 운송에 따른 배출가스 및 전력 손실을 줄이기 위해 온사이트 발전을 최적공급모델로 강화하고 있습니다.

북미으로 확대되는 헬륨 공급 및 보안 플랫폼

세계 헬륨 수급이 타이트해지면서 MRI 장비 가동, 반도체 제조, 항공우주 분야의 불활성화 처리에 영향을 미치고 있습니다. 텍사스에 위치한 전략적 저장시설인 '클리프사이드 헬륨 시스템'은 현재도 관리인의 관리 하에 있으며, 중요 사용자에 대한 최소한공급은 유지되고 있습니다. 퀀텀 테크놀로지(Quantum Technology Corp.)는 캐나다 서부에 40년 만에 새로운 헬륨 정제소를 가동하여 작지만 중요한 지역적 공급의 이중화를 확보했습니다. 그럼에도 불구하고, 2024년 하반기에는 헬륨 가격이 급등하여 조달 예산에 압력을 가하고, 최종 사용자가 회수, 정제 및 재활용 스키드에 대한 투자를 촉진하고 있습니다. 이러한 가격 변동은 신규 팹(제조공장)의 신중한 설비투자 계획의 배경이 되고 있으며, 단기적으로 전체 소비량 증가를 억제하는 요인으로 작용하고 있습니다.

부문 분석

산소는 2025년 산업용 가스 시장 규모에서 31.65%의 압도적인 점유율을 유지하고 있으며, 철강업체들의 DRI 용광로 전환과 병원의 고 유량 인공호흡기 도입 확대에 따라 전체 수요량 증가를 상회하는 성장세를 이어갈 것으로 보입니다. 2024년 린데와 에어리퀴드는 의료용 산소 전용 진공 압력 스윙 흡착기를 20개 이상 가동하여 팬데믹 이후 기준 수요를 반영했습니다. 이와 병행하여 나고야대학의 조사에서는 더 낮은 에너지 소비로 산소와 아르곤을 분리할 수 있는 흡착 및 용해 막이 입증되어 향후 초순수 응용 분야에서 비용 절감의 가능성을 보여주었습니다.

질소 수요는 반도체 불활성화, 레이저 절단, 고급 식품 라인의 가스 대체 포장에 의해 주도되고 있습니다. 이 부문은 금속 가공 공장용 실린더, 전자제품 클린룸용 액화 질소, 냉장 창고 허브의 온사이트 발생기 등 균형 잡힌 공급 형태 조합의 이점을 누리고 있습니다. 이산화탄소 공급량은 2024년 에탄올 공장의 원료 공급 중단으로 인해 감소했습니다. 그러나 양조장의 자체 회수 덕분에 음료 제조업체는 심각한 공급 부족을 피할 수 있었습니다.

'산업용 가스 시장 보고서'는 제품 유형(질소, 산소, 이산화탄소 등), 공급 형태(패키지/용기, 벌크 액체 등), 최종 사용자 산업(화학 가공/정제, 전자/반도체 등), 지역(아시아태평양, 북미, 유럽, 유럽, 남미, 중동/아프리카)별로 분류되어 있습니다. 시장 예측은 수량(톤) 기준으로 제시되어 있습니다.

지역별 분석

2025년 아시아는 석유화학, 철강, 전자산업 집적지가 주도하여 산업용 가스 시장 규모에서 42.55%의 압도적인 점유율을 차지했습니다. 중국의 통합 제철 능력과 인도의 탄탄한 인프라 투자가 결합되어 지난해 하루 600톤 이상의 새로운 공기분리장치(ASU) 증설을 지원했습니다. 각 지역 정부는 산업용 가스 유통을 넷제로 로드맵과 일치시키기 위해 탄소회수 시범사업과 그린수소 수출회랑을 추진하고 있습니다. 경쟁 환경에서는 세계 유수의 기업들과 현지 기업들이 합작 투자를 통해 세계 수준의 엔지니어링 표준을 유지하면서 생산의 현지화를 추진하고 있습니다.

북미는 멕시코만 연안의 정유시설에 공급하는 성숙한 파이프라인망과 중서부 및 북동부 지역을 커버하는 유연한 일반 액화가스 수송망이 특징이며, 시장에서 큰 거래량을 보이고 있습니다. 미국 정유사의 수소 구매량은 2012년부터 2022년까지 29% 증가했으며, 자체 소유 개질 설비에서 외부 조달로 단계적으로 전환하고 있는 것으로 나타났습니다. 청정 에너지 프로젝트에 대한 지속적인 인플레이션 억제책은 저탄소 암모니아, 지속 가능한 항공 연료 및 CO2 격리 사업을 촉진하고 있으며, 모두 전용 산업용 가스를 필요로 합니다. 캐나다는 틈새 헬륨 거점으로 부상하고 있으며, 오랫동안 미국 토지관리청(BLM) 저장 시스템이 지배해 온 시장에 중복성을 더하고 있습니다.

유럽은 여전히 부가가치의 중심지이며, 그린 수소 회랑과 식품 등급 탄소 포집에 주력하고 있습니다. 에어리퀴드, 린데 등의 기업들은 해운 및 장거리 트럭 운송의 탈탄소화를 지원하기 위해 재생에너지 구매 계약과 양성자 교환막형 전해질 장치를 연계하고 있습니다. F가스 규제와 메탄 배출 기준의 강화로 인해 냉동기기 제조업체들은 자연 냉매로 전환해야 하는 상황에 처해 있으며, 이로 인해 이 지역의 가스 포트폴리오가 더욱 다양해지고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.05.20The Industrial Gas Market size is expected to grow from 1.74 billion tons in 2025 to 1.81 billion tons in 2026 and is forecast to reach 2.21 billion tons by 2031 at 4.03% CAGR over 2026-2031.

Healthy demand from steel, semiconductor, and chemical producers underpins this growth, while product innovation around green-hydrogen, high-purity oxygen, and food-grade carbon dioxide keeps value creation ahead of volume expansion. Producers are reinforcing on-site supply models to reduce logistics exposure, and large energy users are signing multi-decade supply contracts that lock in power costs. Regionalization of semiconductor fabrication is shifting high-purity nitrogen and argon flows toward the United States and Europe, even as Asia retains overall volume leadership. At the same time, helium recovery projects, carbon capture ventures, and small-footprint air-separation units are attracting fresh capital from both incumbents and infrastructure investors.

Global Industrial Gas Market Trends and Insights

Rapid Industrialization in Emerging Economies

Robust manufacturing expansion across Asia, especially in China and India, is lifting base-load demand for volume gases such as oxygen and nitrogen. Western India alone houses a large concentration of steel mills, petrochemical clusters, and fertilizer complexes that collectively anchor localized air-separation capacity. Regional authorities are pressing ahead with Make-in-India incentives, encouraging investment in electronics assembly, solar-cell production, and electric-vehicle supply chains that use high-purity nitrogen and argon. Parallel infrastructure projects-from metro rail to greenfield refineries-are extending distributed demand pockets that favor packaged and microbulk deliveries. The U.S. Energy Information Administration projects Asian natural-gas consumption will triple by 2050, with 80% channelled into industry, a proxy for the scale of process-gas requirements.

Green-Hydrogen Push Driving On-Site Electrolysis Contracts

Decarbonization targets are accelerating the adoption of low-carbon hydrogen, prompting chemical, steel, and heavy-transport operators to lock in long-term supply agreements. In partnership with ACWA Power and NEOM, Air Products is developing a USD 8.5 billion renewable-powered electrolysis plant in Saudi Arabia that will supply 650,000 t/y of green ammonia feedstock. Similar contracts across the European Union, Australia, and the United States are under construction, collectively exceeding 1.1 million t/y of planned output. These projects boost demand for associated gases such as nitrogen (for inerting) and oxygen (as a by-product), and they reinforce on-site generation as the preferred delivery model, reducing trucking emissions and power losses.

Helium Supply-Security Platforms Expanding in North America

Tight global helium balances continue to disrupt MRI equipment uptime, semiconductor fabrication, and aerospace inerting. The Cliffside Helium System in Texas, a strategic storage complex, remains under receivership yet sustains a minimum allocation for critical users. Quantum Technology Corp. started Western Canada's first new helium refinery in four decades, adding small but important regional redundancy. Nonetheless, helium prices rose sharply in late 2024, pressuring procurement budgets and encouraging end-users to invest in recovery, purification, and recycling skids. This volatility underpins cautious CAPEX planning for greenfield fabs and acts as a near-term drag on overall consumption growth.

Other drivers and restraints analyzed in the detailed report include:

- Oxygen Uptake from Low-Carbon DRI Steel Plants

- CO2 Capture & Re-Use Projects in EU Breweries & Soda Plants

- High Capital Investment and Operational Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Oxygen retained a commanding 31.65% share of the industrial gases market size in 2025 and continues to outpace overall volume growth as steelmakers migrate to DRI furnaces and hospitals expand high-flow ventilator capacity. During 2024, Linde and Air Liquide commissioned more than 20 vacuum pressure swing adsorption units dedicated to medical oxygen, reflecting post-pandemic baseline demand. In parallel, research at Nagoya University demonstrated an adsorptive-dissolution membrane capable of separating oxygen from argon at lower energy intensity, pointing toward future cost savings in ultra-high-purity applications.

Nitrogen is driven by semiconductor inerting, laser-cutting, and modified-atmosphere packaging for premium food lines. The segment benefits from a balanced mix of delivery modes: packaged cylinders for metal-fabrication shops, merchant liquid for electronics clean rooms, and on-site generators at cold-storage hubs. Carbon dioxide volume slipped in 2024 because of feedstock disruptions at ethanol plants; however, in-house capture at breweries cushioned beverage producers against outright shortages.

The Industrial Gases Market Report is Segmented by Product Type (Nitrogen, Oxygen, Carbon Dioxide, and More), Mode of Supply (Packaged/Cylinder, Merchant Bulk Liquid, and More), End-User Industry (Chemical Processing and Refining, Electronics and Semiconductor, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (tons).

Geography Analysis

Asia accounted for a dominant 42.55% share of the industrial gases market size in 2025, driven by strong petrochemical, ferrous metallurgy, and electronics clusters. China's integrated steel capacity and India's robust infrastructure spending jointly supported more than 600 t/d of new ASU capacity additions last year. Regional governments are promoting carbon capture pilots and green-hydrogen export corridors, aligning industrial gas flows with net-zero roadmaps. The competitive terrain features joint ventures between global majors and domestic firms that localize production while retaining world-scale engineering standards.

North America, characterized by mature pipelines supplying Gulf Coast refineries and adaptable merchant-liquid networks serving the Midwest and Northeast, demonstrates significant volume in the market. Purchases of hydrogen by U.S. refiners rose 29% between 2012 and 2022, illustrating a gradual shift from captive reformers to outsourced supply. Ongoing inflation-reduction incentives for clean-energy projects are catalyzing low-carbon ammonia, sustainable aviation fuel, and CO2 sequestration ventures, each requiring dedicated industrial gas inputs. Canada is emerging as a niche helium hub, adding redundancy to a market long dominated by the U.S. Bureau of Land Management's storage system.

Europe remains a value-added epicenter, focusing on green-hydrogen corridors and food-grade carbon capture. Air Liquide, Linde, and others are synchronizing renewable power purchase agreements with proton-exchange membrane electrolyzers to support maritime shipping and long-haul trucking decarbonization. Stricter F-gas regulation and methane thresholds are nudging refrigeration OEMs toward natural refrigerants, further diversifying gas portfolios in the region.

- Air Liquide

- Air Products and Chemicals Inc.

- Air Water Inc.

- Asia Technical Gas Co Pte Ltd.

- BASF SE

- Bhuruka Gases Ltd.

- Ellenbarrie Industrial Gases Limited

- Gasco

- Goyal MG gases pvt.ltd

- Gruppo SIAD

- Gulf Cryo

- Iwatani Corporation

- Linde plc

- Messer SE & Co. KGaA

- Nippon Sanso Holdings Corporation

- Oxair

- PT Samator Indo Gas Tbk

- Resonac Holdings Corporation

- Sapio Group

- SOL Group

- Southern Industrial Gas Sdn Bhd

- Yingde Gas Shanghai

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Industrialization in Emerging Economies

- 4.2.2 Green-Hydrogen Push Driving On-Site Electrolysis Contracts in EU and Australia

- 4.2.3 Oxygen Uptake from Low-Carbon DRI Steel Plants in US and MENA

- 4.2.4 CO2 Capture and Re-Use Projects in EU Breweries and Soda Plants

- 4.2.5 Helium Supply-Security Platforms Expanding in North America

- 4.3 Market Restraints

- 4.3.1 High Capital Investment and Operational Costs

- 4.3.2 Stringent Safety and Environmental Regulations

- 4.3.3 Volatility in Raw Material and Energy Prices

- 4.4 Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Nitrogen

- 5.1.2 Oxygen

- 5.1.3 Carbon Dioxide

- 5.1.4 Hydrogen

- 5.1.5 Helium

- 5.1.6 Argon

- 5.1.7 Ammonia

- 5.1.8 Methane

- 5.1.9 Propane

- 5.1.10 Butane

- 5.1.11 Other Product Types

- 5.2 By Mode of Supply

- 5.2.1 Packaged/Cylinder

- 5.2.2 Merchant Bulk Liquid

- 5.2.3 On-Site (Tonnage) Generation

- 5.3 By End-user Industry

- 5.3.1 Chemical Processing and Refining

- 5.3.2 Electronics and Semiconductor

- 5.3.3 Food and Beverage Processing

- 5.3.4 Oil and Gas

- 5.3.5 Metal Production and Fabrication

- 5.3.6 Medical and Pharmaceutical

- 5.3.7 Automotive and Transportation

- 5.3.8 Energy and Power Generation

- 5.3.9 Other Industries (Aerospce and water and waste Water Treatment)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN

- 5.4.1.6 Australia

- 5.4.1.7 New Zealand

- 5.4.1.8 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Nordics

- 5.4.3.6 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Turkey

- 5.4.5.4 South Africa

- 5.4.5.5 Nigeria

- 5.4.5.6 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Air Liquide

- 6.4.2 Air Products and Chemicals Inc.

- 6.4.3 Air Water Inc.

- 6.4.4 Asia Technical Gas Co Pte Ltd.

- 6.4.5 BASF SE

- 6.4.6 Bhuruka Gases Ltd.

- 6.4.7 Ellenbarrie Industrial Gases Limited

- 6.4.8 Gasco

- 6.4.9 Goyal MG gases pvt.ltd

- 6.4.10 Gruppo SIAD

- 6.4.11 Gulf Cryo

- 6.4.12 Iwatani Corporation

- 6.4.13 Linde plc

- 6.4.14 Messer SE & Co. KGaA

- 6.4.15 Nippon Sanso Holdings Corporation

- 6.4.16 Oxair

- 6.4.17 PT Samator Indo Gas Tbk

- 6.4.18 Resonac Holdings Corporation

- 6.4.19 Sapio Group

- 6.4.20 SOL Group

- 6.4.21 Southern Industrial Gas Sdn Bhd

- 6.4.22 Yingde Gas Shanghai

7 Market Opportunities and Future Outlook

- 7.1 Growing Demand for Low-Carbon Gases in the Coming Years

- 7.2 White-space and Unmet-Need Assessment