|

시장보고서

상품코드

2035113

로봇 잔디깎기기계 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Robotic Lawn Mower - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

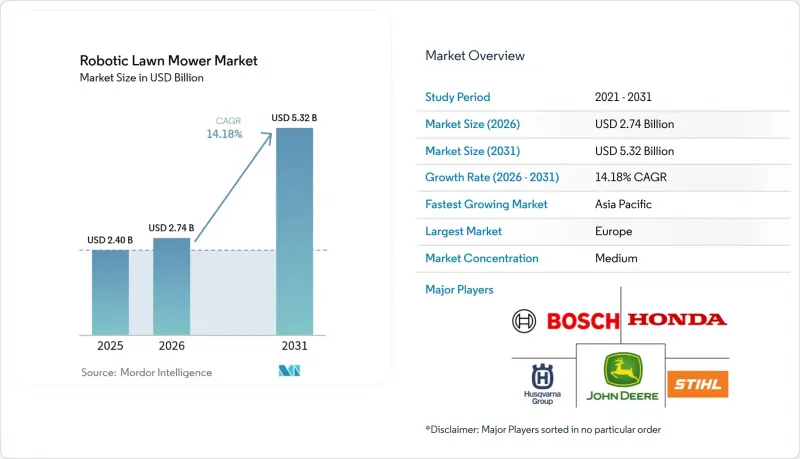

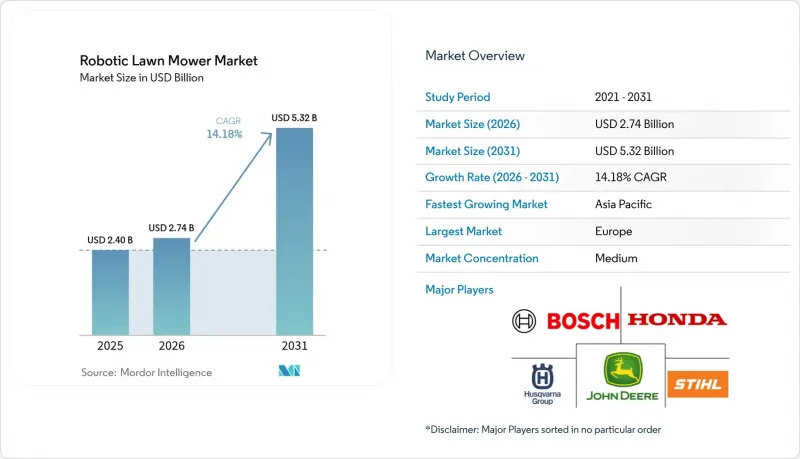

로봇 잔디깎기기계 시장 규모는 2025년 24억 달러에서 2026년에는 27억 4,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 14.18%로 성장을 지속하여, 2031년에는 53억 2,000만 달러에 이를 것으로 예측됩니다.

이러한 성장을 견인하고 있는 것은 배터리로 구동되는 자율 잔디깎기기계 시스템의 보급 확대입니다. 시장 확대는 조경 산업의 인력 부족, 환경 규제 강화, 충전 기술 향상, 경계선 설치가 필요 없는 첨단 시각 기반 내비게이션 시스템 등에 의해 뒷받침되고 있습니다. 제조업체들은 구독 서비스나 기존 장비에 대한 원격 소프트웨어 업데이트를 통해 수익원을 강화하고 있습니다. 소매업체들이 수익성이 높은 스마트홈 기기에 집중하는 것은 시장에 긍정적인 영향을 미치고 있으며, 주택 소유주들 사이에서 자동 잔디깎기기계 서비스 이용이 점점 더 증가하고 있습니다. 상업 부문, 특히 스포츠 시설 관리자와 시설 유지관리 업체들은 인력 부족에 대응하고 넓은 면적의 잔디를 균일하게 관리하기 위해 로봇 잔디깎기기계에 대한 투자를 늘리고 있습니다.

세계 로봇 잔디깎기기계 시장 동향 및 인사이트

주택용 잔디 관리 아웃소싱 증가

주거용 잔디 관리 시장에서는 여가 시간을 우선시하는 맞벌이 가구와 육체노동을 선호하지 않는 고령화 인구 증가를 배경으로 자가 관리보다 전문업체에 의뢰하는 것을 선호하는 경향이 강해지고 있습니다. 조경업체들은 인력 증원 없이 서비스 일정을 유지하기 위해 로봇 잔디깎기기계를 도입해 만성적인 인력난을 해결하고 있습니다. 이 자동화를 통해 작업자는 조경 설계 및 하드스케이프와 같은 수익성 높은 서비스에 집중할 수 있습니다. 로봇 잔디깎기기계는 야간에도 작동하기 때문에 노선당 서비스 제공 횟수를 늘리면서 인력 부족의 영향을 받지 않고 균일한 잔디 높이를 확보할 수 있습니다. 빈번하고 정밀한 예초는 잔디의 건강 상태를 개선하고 비료 사용량을 줄여 서비스 제공업체의 투자 대비 효과를 높입니다. 이러한 잔디 관리의 외주화 추세는 단독주택이 주류를 이루고 가구 소득 수준이 전문 서비스 이용료를 감당할 수 있는 북미 교외 및 서유럽 시장에서 도입이 가속화되고 있습니다.

배터리로 작동하는 아웃도어 기기로의 전환

캘리포니아 주와 유럽연합(EU)의 가솔린 핸드헬드 기기에 대한 정부 규제로 인해 배터리 구동 제품으로의 전환이 가속화되고 있으며, 전기 구동은 선택적 업그레이드가 아닌 표준 사양으로 자리 잡아가고 있습니다. STIHL은 2023년 매출 중 배터리 구동 제품이 24%를 차지하고 2027년까지 35%에 도달하는 것을 목표로 하고 있으며, 이는 업계의 전동화로의 전환을 보여줍니다. 로봇 유닛의 소음과 진동 감소로 야간 가동이 가능해져 주민들에게 피해를 주지 않고 하루 잔디 깎는 주기를 최대화할 수 있으며, 낮에는 물주기나 레크리에이션 활동에 집중할 수 있습니다. 배터리의 에너지 밀도 향상으로 중거리 로봇은 1회 충전으로 150분 이상 작동할 수 있으며, 급속 충전 기능을 통해 가동 중단 시간을 가동 주기의 20% 미만으로 단축할 수 있습니다. 독일의 무공해 원예 장비에 대한 200유로(215달러)의 환급금 등 정부의 인센티브는 투자 회수 기간을 단축하고, 경기 변동 속에서도 안정적인 수요를 유지하고 있습니다.

기존 잔디깎기기계와의 초기 비용 비교

로봇 잔디깎기기계의 가격은 800달러에서 5,000달러까지 다양하며, 300달러에서 800달러의 가솔린 수동식 잔디깎기기계보다 훨씬 더 비쌉니다. 500달러에 달하는 전문 업체 설치 비용은 특히 신흥국에서 처음 구입하는 소비자에게 장벽이 되고 있습니다. 선진국 시장에서는 주택 소유자가 3-5년의 투자 회수 기간과 승용 트랙터에서 이용할 수 있는 더 짧은 융자 기간을 비교 검토하고 있습니다. 소매 대출이나 구독 모델을 통해 초기 비용을 절감할 수 있지만, 이러한 옵션은 주로 프리미엄 브랜드에 국한되어 있어 보급형 부문의 판매량을 제한하고 있습니다. 남미에서는 달러화 약세로 인해 달러화 수입 가격이 상승함에 따라 소비자들이 중고 가솔린 잔디깎기기계를 선택하는 경향이 있습니다. 배터리 비용 절감과 현지 조립으로 인해 향후 가격 차이가 줄어들 가능성이 있지만, 현재 시장 성장은 여전히 저렴한 가격의 가용성 문제로 인해 제약을 받고 있습니다.

부문 분석

2025년, 501-2,000평방미터를 커버하는 중형 모델은 로봇 잔디깎기기계 시장의 42.85%를 차지했습니다. 이 압도적인 점유율은 유럽과 북미의 전형적인 교외 부지면적을 반영하고 있습니다. 이 모델들은 가격, 커버 면적, 배터리 구동 시간의 최적의 균형을 제공하며, 평균적인 주거용 정원의 요구 사항을 충족시키면서 최소한의 저장 공간을 필요로 합니다. 각 제조업체들이 체계적인 잔디 깎기 패턴을 도입하고, 무작위 내비게이션 시스템에 비해 잔디 깎기의 균일성이 향상됨에 따라 이 부문의 성장은 계속되고 있습니다. 반품률의 감소는 이 부문의 안정성을 보여주며, 이 모델들이 소비자의 성능에 대한 기대에 부응하고 있다는 것을 보여줍니다.

2,000평방미터 이상의 면적을 커버하는 하이 레인지 모델은 CAGR 17.1%로 가장 높은 성장률을 보이고 있습니다. 이러한 성장은 인건비 절감을 목표로 하는 골프장, 스포츠 시설, 교육기관에서의 도입 증가에 기인합니다. 무선 내비게이션 시스템 도입으로 광활한 지역의 설치 비용을 절감할 수 있으며, 중앙 집중식 관리 시스템을 통해 단일 장치 인터페이스를 통해 여러 장치를 관리할 수 있습니다. 500평방미터 미만의 면적을 커버하는 저가형 로봇은 일본과 영국의 밀집된 도시 지역에서 시장에서의 존재감을 유지하고 있습니다. 가격 하락이 수익률에 영향을 미치면서 제조업체들은 파티오 가장자리 트리밍 기능과 같은 추가 기능을 추가하고 있습니다. 업계의 초점은 하드웨어 혁신에서 고객 유지를 강화하기 위한 관개 및 동기화 된 일정 관리 시스템과 같은 소프트웨어 강화로 이동하고 있습니다.

2025년, 경계선 가이드 방식은 로봇 잔디깎기기계 시장에서 64.75%의 점유율을 유지했습니다. 이는 설치업체와 주택 소유주들이 우천 시나 낙엽이 많은 계절에도 안정적인 성능을 발휘하는 것을 높이 평가하기 때문입니다. 기존 배선 인프라는 브랜드 충성도를 통해 교체 수요를 지탱하고 있지만, 일부 사용자는 정원 개보수 및 수리 비용을 이유로 대체 기술을 고려하고 있습니다.

비전/카메라 기반 플랫폼은 2031년까지 연평균 복합 성장률(CAGR) 18.9%를 나타낼 것으로 예측됩니다. 이러한 시스템은 도랑을 파낼 필요가 없고, 여러 장소에 빠르게 도입할 수 있어 특히 여러 건물을 관리하는 상업용 계약자에게 유용합니다. 하이브리드 시스템은 광범위한 위치 측정을 위한 RTK-GPS와 화단 부근의 정밀한 탐색을 위한 광학 엣지 감지를 결합하여 스포츠 시설에서 센티미터 단위의 정확도를 실현합니다. 위성항법시스템(GNSS)만을 탑재한 유닛은 하늘이 잘 보이는 탁 트인 곳에서는 좋은 성능을 발휘하지만, 나무가 빽빽한 교외 환경에서는 신호 간섭으로 인해 그 효과가 떨어집니다. 각 제조업체들은 트램펄린, 차도, 야외용 가구 등 정원에서 흔히 볼 수 있는 장애물 감지 정확도를 높이기 위해 AI 알고리즘을 지속적으로 개선하고 있으며, 소프트웨어 개발에 집중하고 있음을 알 수 있습니다.

지역별 분석

2025년 유럽은 로봇 잔디깎기기계 시장 점유율의 44.80%를 차지했습니다. 이는 뿌리 깊은 원예 습관, 높은 인건비, 그리고 로봇 잔디깎기기계 도입을 촉진하는 배출가스 규제에 힘입은 것입니다. 독일, 영국, 프랑스에서는 광범위한 유통망가 유지되고 있으며, 스칸디나비아 시장에서는 단독주택 부문에서 높은 보급률을 보이고 있습니다. 유럽의 기계 규제는 안전 인증 프로세스를 간소화하고, 국경을 초월한 제품 출시를 촉진하며, 여러 지역에 걸친 통합 마케팅을 가능하게 합니다. 제조업체들은 지역별 공급망을 활용하여 미국과 중국 간의 관세를 회피하고 있으며, 이는 북미 수출에 있어 경쟁 우위를 가져다주고 있습니다.

아시아태평양은 2031년까지 13.2%의 성장이 예상되며, 2024년 737억 5,500만 위안(104억 달러) 규모에 달한 중국의 서비스 로봇 산업이 이를 뒷받침하고 있습니다. 이 업계는 국내에서 리튬 이온 배터리와 카메라 모듈을 대규모로 공급하고 있습니다. 일본에서는 노동력 인구의 감소, 한국에서는 도시지역에 잔디밭이 집중되어 있어 60dB 이하로 작동하는 컴팩트한 모델에 대한 수요가 증가하고 있습니다. 호주 지자체는 임금 상승에 대응하기 위해 공공장소에서 로봇을 시험 운용하고 있으며, 오세아니아 지역은 상업용 차량 운용을 평가하는 장소로 자리매김하고 있습니다.

북미는 광활한 잔디밭 면적이 있음에도 불구하고 유럽에 비해 보급률이 낮습니다. 또한, 무역 동향은 중국 제품보다 유럽산 수입품을 선호하고 있으며, 이는 시장 점유율 배분에 영향을 미치고 있습니다. 인플레이션 억제법에서 제안된 전기 실외기기에 대한 소비자 리베이트가 2026년에 시행되면 로봇 잔디깎기기계 도입이 확대될 가능성이 있습니다. 남미, 중동 및 아프리카 시장 점유율은 현재 한 자릿수이지만, 멕시코와 걸프만 국가의 중산층 자산 증가는 고온과 먼지에 강한 프리미엄 모델에 대한 미래 기회를 시사하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.05.20The robotic lawn mower market size is expected to grow from USD 2.4 billion in 2025 to USD 2.74 billion in 2026 and is forecast to reach USD 5.32 billion by 2031 at 14.18% CAGR over 2026-2031.

The increasing adoption of battery-powered autonomous mowing systems drives this growth. The market expansion is supported by labor shortages in the landscaping industry, enhanced environmental regulations, improvements in charging technology, and advanced vision-based navigation systems that eliminate the need for boundary wires. Manufacturers are strengthening their revenue streams through subscription services and remote software updates for existing equipment. The market benefits from retailers' focus on smart-home devices with higher profit margins, while homeowners increasingly opt for automated mowing services. The commercial segment, particularly sports field managers and facility maintenance contractors, is increasing investments in robotic mowers to address workforce shortages and maintain consistent mowing quality across extensive areas.

Global Robotic Lawn Mower Market Trends and Insights

Rising Residential Lawn-Care Outsourcing

The residential lawn care market shows increasing preference for professional services over self-maintenance, driven by dual-income households prioritizing leisure time and an aging population less inclined toward physical labor. Landscape companies address persistent labor shortages by implementing robotic mowing fleets to maintain service schedules without increasing workforce. This automation enables crews to focus on higher-margin services such as landscape design and hardscaping. The robotic mowers operate nightly, increasing the number of properties serviced per route while ensuring uniform cutting heights independent of labor constraints. The frequent, precise mowing patterns improve lawn health and reduce fertilizer requirements, enhancing the return on investment for service providers. This trend of outsourced lawn maintenance accelerates adoption across North American suburbs and Western European markets, where single-family homes predominate and household income levels support professional service fees.

Shift Toward Battery-Electric Outdoor Equipment

Government restrictions on gasoline-powered handheld equipment in California and the European Union accelerate the transition to battery-powered products, establishing electric propulsion as a standard rather than an optional upgrade. STIHL reported that battery-powered units comprised 24% of its 2023 sales and aims to reach 35% by 2027, demonstrating the industry's shift toward electrification. The reduced noise and vibration of robotic units enable overnight operation, maximizing daily mowing cycles without disrupting residents while leaving daylight hours available for watering or recreational activities. Improvements in battery energy density now enable mid-range robots to operate for over 150 minutes per charge, while rapid charging capabilities reduce downtime to less than 20% of the operational cycle. Government incentives, such as Germany's EUR 200 (USD 215) rebate on zero-emission garden equipment, reduce the investment recovery period and maintain steady demand during economic fluctuations.

High Upfront Cost versus Conventional Mowers

The cost of robotic lawn mowers ranges from USD 800 to USD 5,000, significantly higher than gas-powered push mowers priced between USD 300 and USD 800. Professional installation costs of USD 500 create barriers for first-time buyers, particularly in emerging economies. In developed markets, homeowners compare the three to five-year payback period against shorter financing terms available for riding tractors. While retail financing and subscription models reduce initial costs, these options are primarily available for premium brands, limiting sales volume in entry-level segments. In South America, currency depreciation increases dollar-denominated import prices, causing consumers to opt for used gas-powered units. Although battery cost reductions and local assembly may eventually reduce the price difference, current market growth remains constrained by affordability challenges.

Other drivers and restraints analyzed in the detailed report include:

- Labor Shortages in Landscaping Services

- Retailer Push for High-Margin Smart-Home SKUs

- Fire-Risk Recalls of Li-ion Garden Equipment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Medium units covering 501-2,000 m2 accounted for 42.85% of the robotic lawn mower market in 2025. This dominance reflects the typical suburban lot sizes in Europe and North America. These models offer an optimal balance of price, coverage area, and battery life, meeting average residential yard requirements while requiring minimal storage space. The segment's growth continues as manufacturers implement systematic cutting patterns, improving grass cutting uniformity compared to random navigation systems. The segment's stability is evident in reduced return rates, indicating these models meet consumer performance expectations.

High-range models covering areas above 2,000 m2 demonstrate the highest growth rate at 17.1% CAGR. This growth stems from increased adoption by golf courses, sports facilities, and educational institutions seeking to reduce labor costs. The implementation of wire-free navigation systems reduces installation costs for large areas, while centralized control systems enable management of multiple units through single-device interfaces. Low-range robots covering under 500 m2 maintain market presence in dense urban areas of Japan and the United Kingdom. Declining prices affect profit margins, leading manufacturers to include additional features like patio-edge trimming capabilities. The industry focus has shifted from hardware innovations to software enhancements, such as irrigation-synchronized scheduling systems, to strengthen customer retention.

Boundary-wire guidance maintained a 64.75% market share in robotic lawn mowers in 2025, as installers and homeowners value its consistent performance during rainy conditions and heavy debris seasons. The established wire infrastructure supports replacement sales through brand loyalty, though yard renovation and repair expenses motivate some users to explore alternative technologies.

Vision/camera-based platforms are projected to grow at a 18.9% CAGR through 2031. These systems eliminate trenching requirements and enable quick deployment across multiple locations, particularly benefiting commercial contractors managing multiple properties. Hybrid systems combine RTK-GPS for broad positioning with optical edge detection for precise navigation near flower beds, delivering centimeter-level accuracy for sports facilities. While Global Navigation Satellite System (GNSS) only units perform well in open areas with clear sky views, their effectiveness decreases in suburban environments with dense tree coverage due to signal interference. Manufacturers continue to enhance AI algorithms to improve the detection of common yard obstacles, including trampolines, driveways, and outdoor furniture, indicating increased focus on software development.

The Robotic Lawn Mower Market Report is Segmented by Range (Low (Less Than 500 M2), and More), by Navigation Technology (Boundary-Wire, and More), by End-User (Residential, and Commercial), by Distribution Channel (Online, and Offline), and by Geography (North America, Europe, Asia-Pacific, South America, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe held 44.80% of the robotic lawn mower market share in 2025, driven by established gardening practices, high labor costs, and emissions regulations that support robotic lawn mower adoption. Germany, the United Kingdom, and France maintain extensive dealer networks, while Scandinavian markets show high penetration in detached housing segments. European machinery regulations streamline safety certification processes, facilitating cross-border product launches and enabling consolidated marketing across multiple regions. Manufacturers leverage regional supply chains to avoid U.S.-China tariffs, providing a competitive advantage for North American exports.

Asia-Pacific demonstrates 13.2% growth through 2031, supported by China's RMB 73.755 billion (USD 10.4 billion) service-robot industry in 2024, which provides domestic lithium-ion cells and camera modules at scale. Japan's declining workforce and South Korea's concentrated urban lawns increase demand for compact models operating below 60 dB. Australian municipalities test robots in public spaces to address wage inflation, positioning Oceania as an evaluation ground for commercial fleet operations.

North America shows lower penetration compared to Europe despite extensive lawn areas, while trade dynamics favor European imports over Chinese products, affecting market share distribution. The Inflation Reduction Act's proposed consumer rebate on electric outdoor equipment may increase robotic mower adoption if implemented in 2026. South America, the Middle East, and Africa currently represent single-digit market shares, though increasing middle-class wealth in Mexico and Gulf nations indicates future opportunities for premium models designed for high temperatures and sand exposure.

- Husqvarna AB

- ANDREAS STIHL AG & Co. KG

- Honda Motor Co., Ltd.

- Deere & Company

- Robert Bosch GmbH

- Positec Technology Co., Ltd.

- The Toro Company

- Stanley Black & Decker, Inc.

- STIGA S.p.A. (3i Group plc)

- Globe Tools Group Co., Ltd.

- Segway Inc. (Ninebot Ltd.)

- Shenzhen Mammotion Technologies Co., Ltd.

- EcoFlow Technology Inc.

- FJDynamics International Ltd.

- Yamabiko Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Residential Lawn-Care Outsourcing

- 4.2.2 Shift Toward Battery-Electric Outdoor Equipment

- 4.2.3 Labor Shortages in Landscaping Services

- 4.2.4 Retailer Push for High-Margin Smart-Home SKUs

- 4.2.5 Advent of Vision-Based, Perimeter-Free Navigation

- 4.2.6 Original Equipment Manufacturer Subscription Models for Autonomous Mowing

- 4.3 Market Restraints

- 4.3.1 High Upfront Cost versus Conventional Mowers

- 4.3.2 Limited Performance on Uneven and Tall-Grass Terrains

- 4.3.3 Cyber-Security and Data-Privacy Concerns

- 4.3.4 Fire-Risk Recalls of Li-ion Garden Equipment

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Range

- 5.1.1 Low (Less Than 500 m2)

- 5.1.2 Medium (501-2,000 m2)

- 5.1.3 High (More Than 2,000 m2)

- 5.2 By Navigation Technology

- 5.2.1 Boundary-Wire

- 5.2.2 Vision / Camera

- 5.2.3 GNSS / RTK-GPS

- 5.3 By End-User

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.4 By Distribution Channel

- 5.4.1 Online (Direct, Marketplaces)

- 5.4.2 Offline (DIY Stores, Specialty Dealers)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Spain

- 5.5.2.5 Italy

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 South Korea

- 5.5.3.4 India

- 5.5.3.5 Australia

- 5.5.3.6 New Zealand

- 5.5.3.7 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Iran

- 5.5.5.4 Oman

- 5.5.5.5 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Rest of Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Husqvarna AB

- 6.4.2 ANDREAS STIHL AG & Co. KG

- 6.4.3 Honda Motor Co., Ltd.

- 6.4.4 Deere & Company

- 6.4.5 Robert Bosch GmbH

- 6.4.6 Positec Technology Co., Ltd.

- 6.4.7 The Toro Company

- 6.4.8 Stanley Black & Decker, Inc.

- 6.4.9 STIGA S.p.A. (3i Group plc)

- 6.4.10 Globe Tools Group Co., Ltd.

- 6.4.11 Segway Inc. (Ninebot Ltd.)

- 6.4.12 Shenzhen Mammotion Technologies Co., Ltd.

- 6.4.13 EcoFlow Technology Inc.

- 6.4.14 FJDynamics International Ltd.

- 6.4.15 Yamabiko Corporation