|

시장보고서

상품코드

2035147

알루미늄 전해 커패시터 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Aluminum Electrolytic Capacitors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

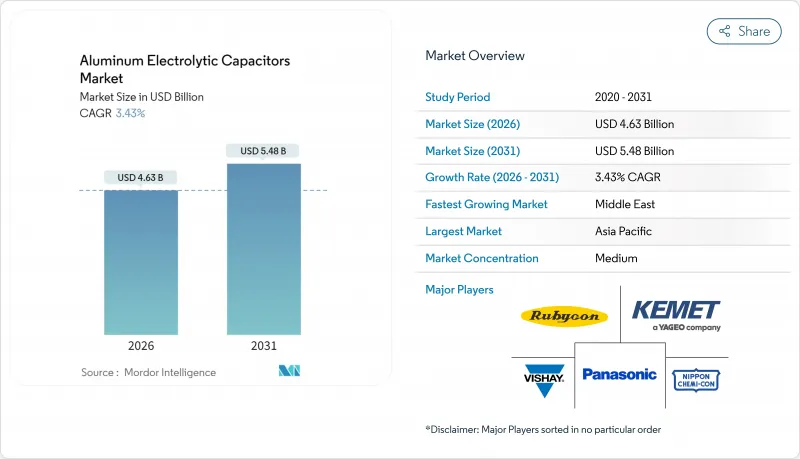

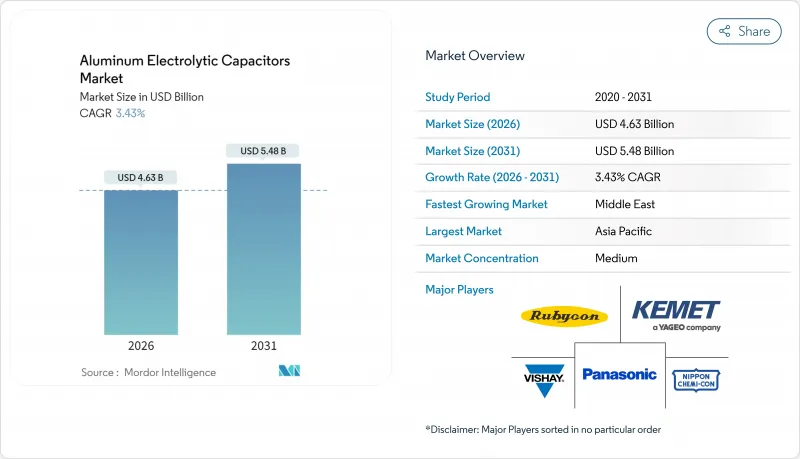

알루미늄 전해 커패시터 시장 규모는 2026년에 46억 3,000만 달러로 예상되며, 2031년까지 54억 8,000만 달러에 이를 것으로 예측되며, 기간 중 CAGR은 3.43%를 나타낼 전망입니다.

이러한 성장의 원동력은 고전압 인버터 토폴로지, 800V 전기자동차(EV) 배터리 플랫폼, 그리고 낮은 등가 직렬 저항(ESR)과 긴 수명이 요구되는 광대역 갭 파워 디바이스로의 전환에 있습니다. 스마트폰 부품의 소형화, EV 트랙션 인버터의 리플 전류 밀도 향상, 중동의 재생에너지 도입 의무화 등이 제품 설계와 지역별 수요 패턴을 재편하고 있습니다. 공급업체들은 현재 알루미늄 가격 변동 위험을 상쇄하기 위해 하이브리드 폴리머 기술, 자체 생산 에칭 포일 생산 능력, 자동차 신뢰성 인증 등을 전략의 핵심으로 삼고 있습니다. 한편, 지역 전문 기업들은 지리적 근접성과 비용 우위를 활용하여 민생 전자기기 및 산업 자동화 분야에서 설계 채택을 획득하고 있습니다.

세계 알루미늄 전해 커패시터 시장 동향 및 인사이트

PCB 실장 면적의 축소로 초소형 커패시터 수요 견인

스마트폰 및 태블릿의 전원 관리 회로는 점점 더 소형화되고 있으며, 공급업체들은 2023년 설계에 비해 30% 줄어든 기판 면적을 가진 패키지로 동일한 정전 용량을 제공해야 하는 상황입니다. 두께가 3mm 미만인 표면 실장형 알루미늄 전해 커패시터는 소음을 유발하는 세라믹 커패시터의 병렬 배치를 대체하고 있으며, 이러한 장점은 2025년에 출시된 GYG 하이브리드 시리즈에 의해 입증되고 있습니다. 수요는 아시아태평양에 집중되어 있으며, 이 지역의 수탁 제조 업체들은 극히 얇은 이윤율을 유지하기 위해 1 평방 mm 단위의 공간 절감을 최우선 과제로 삼고 있습니다. 이 요인으로 인한 CAGR의 0.5% 상향 조정은 모바일 단말기의 엄청난 출하량을 반영하고 있습니다. 박형 고분자 음극 라인에 대한 설비 투자는 기존의 액체 전해질로부터의 전환을 뒷받침하고 있습니다. 소형화 로드맵을 충족하지 못하는 공급업체는 차세대 휴대폰의 참조 설계에서 제외될 위험이 있습니다.

EV의 800V 배터리 시스템으로의 전환으로 리플 전류 요구 사항 증가

자동차 제조업체는 DC 급속 충전 시간을 단축하고 구리 질량을 줄이기 위해 배터리 팩의 전압을 400V에서 800V로 전환하고 있습니다. 이 변경으로 인해 DC 링크 커패시터에 가해지는 전압 스트레스가 두 배로 증가하여 리플 전류가 50A를 초과하여 기존의 액체 전해질 부품이 과열됩니다. 파나소닉의 ZL 오토모티브 시리즈와 이튼의 EHBSA 하이브리드 제품군은 정격 온도 135℃, ESR 10mΩ 미만의 AEC-Q200 호환 하이브리드 폴리머 솔루션으로의 전환을 보여주는 좋은 예입니다. EV의 보급으로 시장 CAGR은 0.7% 상승했으며, 중국뿐만 아니라 북미와 유럽에서도 고전압 시스템 도입이 진행되고 있습니다. 차량용 충전기 및 트랙션 인버터 공급업체는 디레이팅을 제거하기 위해 폴리머 음극의 사용을 점점 더 많이 규정하여 평균 판매 가격(ASP)의 추가 상승을 보장하고 있습니다.

알루미늄 가격 변동으로 수익률 압박

런던금속거래소(LME) 현물 가격은 2025년 12월 톤당 2,955달러로 연초 예상치를 20% 상회했습니다. 이로 인해 3개월간의 고객 가격표에 묶여 있는 커패시터 제조업체의 매출총이익률이 압박을 받고 있습니다. 에칭 포일은 부품 원가의 약 30%를 차지하며, 60-90일 정도의 가격 전가 시차가 가격 조정을 방해하고 있습니다. 미국 에너지부가 제안한 탄소 국경 조정 조치는 석탄에 의존하는 전력망 지역에 추가적인 비용 압박을 가져올 수 있습니다. 매출액이 1억 달러 미만인 중소기업은 헤지 여력이 부족하고, 파산 위험이 높으며, R&D 예산도 제한되어 있습니다.

부문 분석

500V 이상의 고전압 알루미늄 전해 커패시터는 태양광 인버터 및 산업용 드라이브가 효율 향상을 위해 DC 버스 전압을 높이면서 연간 4.4%의 성장률이 예상되며, 이는 전체 알루미늄 전해 커패시터 시장의 CAGR인 3.43%를 상회할 것으로 예측됩니다. 저전압 부품은 스마트폰, 태블릿 및 12-48V 자동차 레일 덕분에 2025년 매출의 64.21%를 차지했습니다. 고전압 산화막은 1V당 약 1.2nm의 아노다이징 정밀도가 요구되며, 클린룸 투자 및 인라인 결함 검사를 촉진하고 있습니다.

중동의 유틸리티 규모의 태양광 발전 프로젝트와 800V EV 차량용 충전기는 세분화의 경계를 모호하게 만들고 있으며, 450-500V 커패시터는 두 층에 걸쳐 있습니다. 파나소닉의 ZL 시리즈는 135℃의 내열성을 갖추고 이 크로스오버 시장을 타겟으로 하고 있으며, 보닛 내부 환경의 열 관리 문제를 강조하고 있습니다. 와이드 밴드갭 반도체로 600-700V의 중간 버스가 실현됨에 따라, 알루미늄 전해 커패시터 시장은 기존의 500V라는 분기점이 아닌 새로운 전압대 중심으로 재편될 것으로 보입니다.

고체 고분자 커패시터는 5G 기지국의 열 요구 사항을 배경으로 CAGR 4.9%로 확대될 것으로 예상되며, 2025년에는 비고체(액체) 설계가 61.47%의 점유율을 차지했습니다. 알루미늄 산화물 양극과 전도성 폴리머 음극을 결합한 하이브리드 고분자 부품은 비용과 성능의 격차를 해소하고 105℃에서 10,000시간의 수명을 실현합니다.

125°C 이상의 환경에서 고체 폴리머의 신뢰성은 여전히 과제로 남아 있습니다. 전도성 폴리머가 열화되기 때문에 자동차 엔진룸 내로의 도입이 제한되어 있습니다. 따라서 85°C 이하, RMS 전류가 2A 이하인 응용 분야에서는 액체 전해질이 여전히 주류를 유지하고 있습니다. 특히 ESR이 열 설계의 제약 요인으로 작용하는 자동차 DC-DC 컨버터에서 인증 데이터가 축적됨에 따라 하이브리드 폴리머 형태의 알루미늄 전해 커패시터 시장 규모는 꾸준히 확대될 것으로 예측됩니다.

지역별 분석

아시아태평양은 중국의 스마트폰 조립 공장, 일본의 자동차 전장, 한국의 파운드리를 중심으로 2025년 매출의 45.38%를 차지했습니다. 국내 수요와 수출량이 모두 결합되어 이 지역은 알루미늄 전해 커패시터 시장의 중심지가 되었습니다. 태국, 말레이시아, 베트남 정부는 세제혜택을 제공하고 있으며, 무라타제작소, 파나소닉 등으로부터 생산능력을 유치하고 있습니다.

중동은 사우디의 10GW 규모의 NEOM 프로젝트와 아랍에미리트의 2.6GW 규모의 모하메드 빈 라시드 알 막툼 태양광 발전소와 같은 기가급 태양광 발전소 덕분에 4.7%의 가장 높은 CAGR을 기록했습니다. 이러한 발전소용 인버터에는 85℃에서 10만 시간의 정격 수명을 가진 600-900V의 커패시터가 필요해 고전압 커패시터에 대한 수요가 증가하고 있습니다. 히타치 에너지의 시안 공장은 걸프협력회의(GCC) 회원국의 설비 수요를 충족시키기 위해 2025년까지 생산량을 3배로 확대해, 이 지역이 중국의 생산 능력을 끌어들이고 있음을 강조하고 있습니다.

북미에서는 EV 조립 공장의 증설과 저ESR DC 버스용 커패시터를 필요로 하는 하이퍼스케일 데이터센터 건설이 호재로 작용하고 있습니다. 유럽은 에너지 가격 상승이라는 역풍에 시달리고 있지만, 전기화 의무화로 인해 자동차 및 산업용 부품에 대한 프리미엄 수요는 유지되고 있습니다. 남미는 하이브리드 플랫폼을 채택한 브라질의 자동차 부품 공급업체를 중심으로 소규모 기반에서 성장하고 있습니다. 한편, 아프리카는 오프 그리드용 태양광 컨트롤러에 초점을 맞춘 신흥 시장으로 남아 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.05.20The aluminum electrolytic capacitors market size is USD 4.63 billion in 2026 and is forecast to reach USD 5.48 billion by 2031, reflecting a 3.43% CAGR through the period.

Momentum stems from a shift toward high-voltage inverter topologies, 800 V electric-vehicle (EV) battery platforms, and wide-bandgap power devices that demand lower equivalent series resistance (ESR) and longer lifetime. Component miniaturization in smartphones, higher ripple-current densities in EV traction inverters, and renewable-energy mandates in the Middle East are reshaping product design and geographic demand patterns. Supplier strategies now emphasize hybrid polymer technology, captive etched-foil capacity, and automotive reliability qualifications to offset aluminum price volatility. At the same time, regional specialists leverage proximity and cost advantages to win design slots in consumer electronics and industrial automation.

Global Aluminum Electrolytic Capacitors Market Trends and Insights

Shrinking PCB Real Estate Driving Ultra-Miniaturised Capacitors

Power-management circuits in smartphones and tablets continue to shrink, forcing suppliers to deliver identical capacitance in packages occupying 30% less board area than 2023 designs. Surface-mount aluminum electrolytic capacitors under 3 mm profile are displacing parallel banks of ceramics that create acoustic noise, an advantage demonstrated by Nichicon's GYG hybrid series released in 2025. Demand is concentrated in Asia Pacific, where contract manufacturers prioritize square-millimetre savings to sustain razor-thin margins. The driver's 0.5% uplift to the overall CAGR reflects the sheer shipment volume of mobile devices. Capital investment in low-profile polymer cathode lines underlines the transition from traditional liquid electrolytes. Suppliers that cannot meet miniaturization roadmaps risk exclusion from next-generation handset reference designs.

Push Toward 800 V Battery Systems in EVs Elevates Ripple Current Requirements

Automakers are migrating from 400 V to 800 V pack voltages to shorten DC-fast-charging sessions and trim copper mass. The change doubles voltage stress on DC-link capacitors and pushes ripple current beyond 50 A RMS, overheating conventional liquid-electrolyte parts. Panasonic's ZL automotive series and Eaton's EHBSA hybrid family illustrate the move to AEC-Q200 hybrid polymer solutions rated at 135 °C and ESR below 10 mΩ. EV adoption drives a 0.7% boost to market CAGR, with North America and Europe joining China in high-voltage rollouts. Onboard charger and traction-inverter suppliers increasingly stipulate polymer cathodes to eliminate derating, locking in higher average-selling-price (ASP) growth.

Aluminium Price Volatility Compressing Margins

London Metal Exchange spot prices reached USD 2,955 per metric ton in December 2025, 20% higher than early-year forecasts, trimming gross margins for capacitor makers locked into three-month customer price lists. Etched foil comprises roughly 30% of bill-of-material cost, and a 60- to 90-day pass-through lag hampers price adjustments. The U.S. Department of Energy's proposed carbon-border adjustments could add further cost pressure in coal-reliant grid regions. Smaller firms under USD 100 million revenue lack hedging leverage, heightening bankruptcy risk and limiting R&D budgets.

Other drivers and restraints analyzed in the detailed report include:

- Growing Investments in Utility-Scale Solar Inverters

- Wide-bandgap Power Devices Creating Need for Low-ESR Bulk Capacitance

- Supply Risk of High-Purity Etched Foil

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

High-voltage aluminum electrolytic capacitors above 500 V are forecast to grow at 4.4% annually, eclipsing the 3.43% aluminum electrolytic capacitors market CAGR as solar inverters and industrial drives lift DC-bus voltages for efficiency. Low-voltage parts still command 64.21% of 2025 revenue thanks to phones, tablets, and 12-48 V automotive rails. High-voltage oxide layers require anodization precision near 1.2 nm per volt, pushing cleanroom investments and inline defect inspection.

Utility-scale solar projects in the Middle East and 800 V EV onboard chargers blur segmentation boundaries, with 450-500 V capacitors straddling both tiers. Panasonic's ZL series targets this crossover with 135 °C endurance, underscoring thermal-management challenges in under-hood environments. As wide-bandgap semiconductors enable intermediate 600-700 V buses, the aluminum electrolytic capacitors market is likely to realign around new voltage clusters rather than the historical 500 V breakpoint.

Solid polymer capacitors should advance at 4.9% CAGR on the back of 5G base-station thermal demands, while non-solid liquid designs held 61.47% share in 2025. Hybrid polymer parts that marry aluminium oxide anodes with conductive-polymer cathodes bridge cost and performance gaps, extending life to 10,000 hours at 105 °C.

Solid polymer reliability above 125 °C remains a hurdle: conductive polymers degrade, limiting automotive under-hood deployment. Liquid electrolytes therefore retain dominance in applications below 85 °C and currents under 2 A RMS. The aluminum electrolytic capacitors market size for hybrid polymer formats is expected to expand steadily as qualification data accumulates, especially in automotive DC-DC converters where ESR dictates thermal-design budgets.

The Aluminum Electrolytic Capacitors Market Report is Segmented by Voltage (High Voltage (Above 500 V), and Low Voltage (Up To 500 V)), Electrolyte Type (Non-Solid Liquid, Solid Polymer, and Hybrid Polymer), Mounting Configuration (Surface-Mount, Through-Hole (Radial, and Axial), and More), Application (Industrial Automation, Telecommunications, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific captured 45.38% of 2025 revenue, anchored by Chinese smartphone assembly plants, Japanese auto electronics, and Korean foundries. Domestic demand plus export volumes make the region the epicentre of the aluminum electrolytic capacitors market. Governments in Thailand, Malaysia, and Vietnam offer tax holidays, drawing capacity from Murata, Panasonic, and others.

The Middle East posts the fastest 4.7% CAGR thanks to giga-scale solar farms such as Saudi Arabia's 10 GW NEOM project and the United Arab Emirates' 2.6 GW Mohammed bin Rashid Al Maktoum Solar Park. Inverters for these plants need 600-900 V capacitors rated for 100,000 hours at 85 °C, boosting high-voltage demand. Hitachi Energy's Xi'an line tripled output in 2025 to serve Gulf Cooperation Council installations, underlining the region's pull-on Chinese capacity.

North America benefits from EV assembly expansions and hyperscale datacentre builds that require low-ESR DC-bus capacitance. Europe faces energy-price headwinds but sustains premium demand for automotive and industrial parts through electrification mandates. South America grows from a smaller base, led by Brazilian auto suppliers adopting hybrid platforms, while Africa remains an emerging market focused on off-grid solar controllers.

- Nippon Chemi-Con Corporation

- Panasonic Holdings Corporation

- Yageo Corporation (KEMET)

- Vishay Intertechnology Inc.

- Nichicon Corporation

- Rubycon Corporation

- TDK Corporation (EPCOS Brand)

- Cornell Dubilier Electronics

- Lelon Electronics Corporation

- Samwha Capacitor Group

- Nantong Jianghai Capacitor Co.

- NIC Components Corp.

- Elna Co., Ltd.

- Suncon (Sanyo)

- Illinois Capacitor (Cornell)

- Hitano Enterprise Corp.

- Samyoung Electronics Co., Ltd.

- Taiwan Chinsan Electronics Industrial Co., Ltd.

- Cheng Tung Industrial Co., Ltd.

- CapXon Group

- Jianghai Europe Electronic Components GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shrinking PCB Real Estate Driving Ultra-miniaturised Capacitors

- 4.2.2 Push Toward 800 V Battery Systems in EVs Elevates Ripple Current Requirements

- 4.2.3 Growing Investments in Utility-Scale Solar Inverters

- 4.2.4 Government Incentives for Smart Manufacturing (Industry 4.0)

- 4.2.5 Wide-bandgap Power Devices Creating Need for Low-ESR Bulk Capacitance

- 4.2.6 Edge AI Hardware Proliferation in 5G Base-Stations

- 4.3 Market Restraints

- 4.3.1 Aluminium Price Volatility Compressing Margins

- 4.3.2 Supply Risk of High-Purity Etched Foil

- 4.3.3 Solid Polymer Reliability Concerns Above 125 °C

- 4.3.4 Design-in Shift Toward Multi-layer Polymer Capacitors

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Investment Analysis

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Bargaining Power of Buyers

- 4.9.2 Bargaining Power of Suppliers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitute Products

- 4.9.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Voltage

- 5.1.1 High Voltage (Greater than 500 V)

- 5.1.2 Low Voltage (Up to 500 V)

- 5.2 By Electrolyte Type

- 5.2.1 Non-solid (Liquid) Electrolyte

- 5.2.2 Solid Polymer Electrolyte

- 5.2.3 Hybrid Polymer

- 5.3 By Mounting Configuration

- 5.3.1 Surface-Mount

- 5.3.2 Through-Hole (Radial, Axial)

- 5.3.3 Snap-In

- 5.3.4 Screw Terminal

- 5.3.5 Other Mounting Configurations

- 5.4 By Application

- 5.4.1 Industrial Automation

- 5.4.2 Telecommunications

- 5.4.3 Consumer Electronics

- 5.4.4 Automotive (ICE and EV)

- 5.4.5 Energy and Power

- 5.4.6 Other Applications

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Rest of Asia Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Nippon Chemi-Con Corporation

- 6.4.2 Panasonic Holdings Corporation

- 6.4.3 Yageo Corporation (KEMET)

- 6.4.4 Vishay Intertechnology Inc.

- 6.4.5 Nichicon Corporation

- 6.4.6 Rubycon Corporation

- 6.4.7 TDK Corporation (EPCOS Brand)

- 6.4.8 Cornell Dubilier Electronics

- 6.4.9 Lelon Electronics Corporation

- 6.4.10 Samwha Capacitor Group

- 6.4.11 Nantong Jianghai Capacitor Co.

- 6.4.12 NIC Components Corp.

- 6.4.13 Elna Co., Ltd.

- 6.4.14 Suncon (Sanyo)

- 6.4.15 Illinois Capacitor (Cornell)

- 6.4.16 Hitano Enterprise Corp.

- 6.4.17 Samyoung Electronics Co., Ltd.

- 6.4.18 Taiwan Chinsan Electronics Industrial Co., Ltd.

- 6.4.19 Cheng Tung Industrial Co., Ltd.

- 6.4.20 CapXon Group

- 6.4.21 Jianghai Europe Electronic Components GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment