|

시장보고서

상품코드

2043873

정형외과용 생체 재료 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Orthopedic Biomaterials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

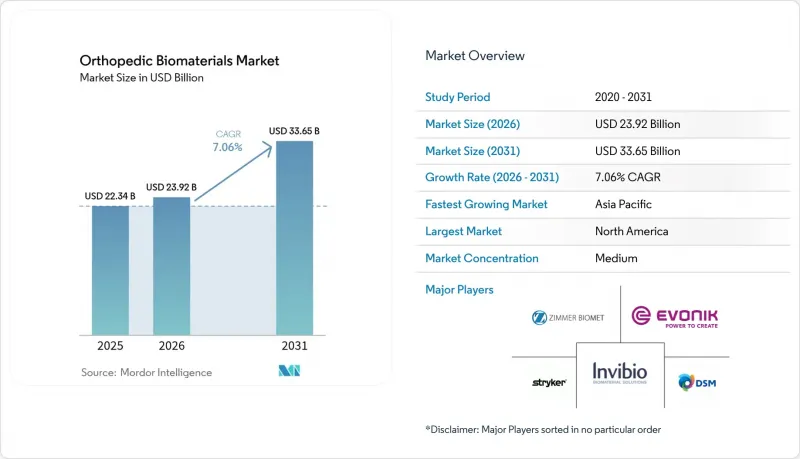

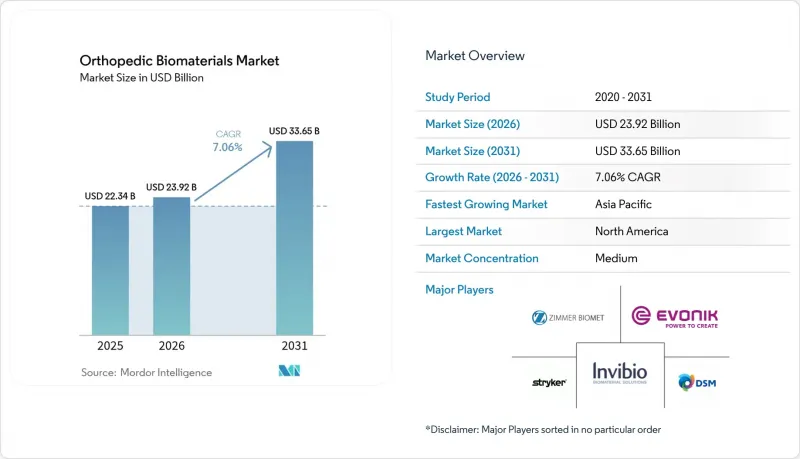

정형외과용 생체 재료 시장 2026년 규모는 239억 2,000만 달러로 추정되고 있어 2025년 223억 4,000만 달러에서 성장하여 2031년에는 336억 5,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 복합 성장률(CAGR) 7.06%를 나타낼 것으로 예측됩니다.

이러한 성장은 인구 고령화, 골관절염 유병률의 급증, 스포츠 및 교통 사고로 인한 부상의 꾸준한 발생, 환자 개인화 및 생체 활성 임플란트 분야의 급속한 기술 발전과 함께 이루어지고 있습니다. 미국 FDA의 획기적 의료기기 프로그램 등 규제적 지원으로 새로운 생체모방 소재 시장 출시 기간이 단축되는 한편, 팬데믹 이후 미처리 안건 해소를 위한 병원 측 수요가 시술 건수를 뒷받침하고 있습니다. 각 업체들은 적층 가공 기술을 활용하여 재수술의 위험을 줄이는 용도에 적합한 부품을 제공하고 있으며, 지속가능성에 대한 요구로 인해 공급망은 생분해성 제제로 전환하고 있습니다. 지속적인 공급망 압박과 엄격한 심사기준은 정형외과용 생체 재료 시장의 향후 성장세를 둔화시킬 뿐, 그 흐름을 저해하는 요인은 아닙니다.

세계의 정형외과용 생체 재료 시장 동향과 인사이트

고령화에 따른 골관절염의 부담

세계적으로 평균 수명의 연장과 생활습관 요인으로 인해 골관절염의 유병률이 증가하고 있으며, 관절 재건 솔루션에 대한 지속적인 수요가 발생하고 있습니다. 2045년까지 폐경 후 여성의 약 50%가 이 질환에 걸릴 것으로 예측되며, 2050년까지 무릎 골관절염 환자 수는 75% 증가할 것으로 예측됩니다. 이와 함께 고관절 및 무릎 관절 재치환 수술 건수가 증가함에 따라 내구성이 높고 마모에 강한 생체 재료에 대한 수요가 증가하고 있습니다. 체질량 지수(BMI) 증가는 전 세계 전체 사례의 20% 이상에 기여하고 있으며, 대사 스트레스와 기계적 마모가 결합하여 임플란트 수명을 연장하는 고강도, 저부스러기 폴리머의 개발을 가속화하고 있습니다.

신흥 시장에서의 스포츠 및 교통사고로 인한 외상 증가 추세

도시화와 자동차화로 인해 많은 저소득 지역에서 근골격계 외상 발생률이 증가하고 있습니다. 케냐 병원에서는 정형외과 입원 환자의 59.4%가 교통사고로 인한 입원 환자이며, 그중 85%가 15세에서 64세 사이의 연령층입니다. 가나에서도 비슷한 경향을 보이고 있으며, 부상자의 42%가 자동차 사고로 인한 부상입니다. 스포츠에 대한 자발적인 참여가 증가하면서 젊은 층의 재건 수술 건수가 증가함에 따라, 공급업체들은 기계적 강인성과 뼈의 조기 유합의 균형을 맞춘 고분자-세라믹 복합재 개발에 박차를 가하고 있습니다.

수술 다운코딩 및 상환액 감소

보험사는 문서화 요건을 강화하고 있으며, 병원은 모든 정형외과적 적응증에 대한 정당성을 입증해야 합니다. 현재 메디케어는 무릎 인공관절 전치환술을 승인하기 전에 보존적 치료의 실패를 증명할 것을 요구하고 있어, 수술 전 대기 기간이 길어지고 있습니다. MS-DRG 코드에 따른 복합외상 상환액은 9,496달러에서 5,639달러까지 다양하며, 의료 서비스 제공업체의 예산 책정 불확실성을 증가시키고 있습니다. 따라서 의료기기 제조업체는 비용 상쇄 주장을 입증하고, 코더의 컴플라이언스를 유지하기 위한 증거자료를 제출해야 합니다.

부문 분석

2025년에는 고성능 폴리머가 46.58%의 점유율로 가장 큰 매출 비중을 차지했습니다. 이는 관골컵과 척추 케이지의 채용이 꾸준히 증가한 것이 주요 요인으로 작용했습니다. 에보닉의 'VESTAKEEP Fusion'은 2상 인산칼슘을 첨가하여 기계적 강도를 유지하면서 PEEK에 생체 활성을 부여할 수 있음을 보여주고 있습니다. 표면개량형 제품이 기존 뼈 통합의 한계를 극복함에 따라 고분자 분야의 정형외과용 생체 재료 시장 규모는 꾸준히 확대될 것으로 전망됩니다. 현재 규모가 작은 세라믹 및 생체 활성 유리는 외과 의사들이 고유의 골전도성과 방사선 투과성을 활용함에 따라 2031년까지 연평균 복합 성장률(CAGR) 7.82%의 견조한 성장세를 보일 것으로 예측됩니다. 폴리머 코어와 세라믹 코팅을 결합한 하이브리드 디자인은 하중 지지력과 골 친화성을 융합하여 단순히 공간을 채우는 것이 아니라 치유에 참여하는 재료로의 전환을 상징합니다.

금속 카테고리는 스트레스 차폐 현상 및 니켈 과민증과 관련하여 다시 한 번 엄격한 시선에 노출되어 있습니다. Zimmer Biomet의 Tivanium 합금은 저니켈 성분으로 알레르기를 완화하는 것을 목표로 하고 있습니다. 실리콘 질화물과 같은 틈새 혁신 기업은 항균성 표면과 열 안정성을 추구하고 있으며, Sintx는 이 화합물에 대해 FDA 승인을 받은 유일한 회사라고 주장하고 있습니다. 인산칼슘 시멘트는 성형 가능한 골 결손 충전재로 여전히 의료기관의 지지를 받고 있지만, 흡수성이 조절된 마그네슘 합금에 대한 지속적인 연구는 향후 완전 생분해성 및 하중 분산 기능을 갖춘 구조물로의 전환을 예견하고 있습니다.

2025년에도 고령화 사회에서 고관절 및 무릎 관절 치환술 건수가 여전히 높은 수준을 유지함에 따라 관절 재건 분야는 매출의 38.25%를 차지했습니다. 그럼에도 불구하고, 스미스 앤 네퓨의 REGENETEN과 같은 생체유도 패치가 기존 수복술에 비해 회전근개 건판 재파열률을 68% 감소시킨다는 증거에 힘입어, 정형생물학 분야는 CAGR 8.03%로 다른 모든 분야를 능가하는 성장세를 보이고 있습니다. 성장세를 보이고 있습니다. 보험사들이 대체 수술을 늦추거나 피하는 재생의료에 대한 선호도가 높아짐에 따라 바이오로직스에 의한 정형외과용 생체 재료 시장 규모는 확대될 것으로 예측됩니다.

신흥국의 고에너지 외상 증가로 인해 척추 및 외상 고정용 임플란트는 견고한 성장세를 이어가고 있습니다. 과거 경증 골관절염에 국한되었던 인공관절 치환술은 활동적인 노년층에서 인공관절 치환술을 미루기 위한 보조요법으로 재조명되고 있습니다. 하드웨어 제조업체들이 골절을 안정화시키면서 골유합 조직 형성을 자극하는 성장인자를 플레이트와 못에 내장한 통합 구조물을 개발하면서 기술의 융합이 진행되고 있습니다.

지역별 분석

북미는 첨단 수술용 로봇 기술과 종합적인 보험 적용에 힘입어 2025년 매출의 39.90%를 차지했습니다. 정형외과용 생체 재료 시장은 VELYS 로봇 무릎관절 시스템, KINCISE 2 자동 고관절 시스템 등 부품의 위치를 정밀하게 조정하는 기술의 등장으로 수혜를 받고 있습니다. 그러나 지불자의 엄격한 문서화 요건과 FDA의 원료 공급에 대한 경고는 수익률에 대한 압박을 강조하고 있습니다. 병원 그룹은 수명 가치 지표를 기반으로 한 의료기기 선택에 점점 더 중점을 두고 있으며, 공급업체는 임상 데이터 외에도 사용 비용에 대한 증거를 제시하도록 요구하고 있습니다.

아시아태평양은 급속한 고령화와 중산층의 보험 가입 확대에 힘입어 2031년까지 연평균 복합 성장률(CAGR) 7.98%를 나타낼 것으로 예측됩니다. 국내 제조업체들은 수입 의존도를 낮추기 위해 적층제조(적층제조) 연구소를 확충하고 있으며, 각국 정부는 3D 프린팅 임플란트 승인 절차를 간소화하고 있습니다. 인도와 같은 시장에서는 접근성을 확대하기 위해 가격 상한제를 도입하고 있으며, 다국적 기업들은 생산 현지화 및 판매 채널 전략을 재검토해야 하는 상황입니다. 국가별 다양성은 여전히 높으며, 일본의 성숙한 규제 감독 체계는 급성장하는 동남아시아 국가들의 진화하는 프레임워크와 대조를 이룹니다.

유럽에서는 EU 의료기기 규정으로 인해 추적성이 강화되고 에코 디자인 요구사항이 가속화됨에 따라 2030년까지 꾸준한 성장이 예상됩니다. 병원에서는 정형외과용 부품의 '생산부터 폐기까지' 추적 시스템을 시범적으로 도입하여 생분해성 제품 채택을 확대할 수 있는 길을 마련하고 있습니다. 중동 및 아프리카에서는 수술실 수용능력 확대를 위해 민관협력을 추진하고 있습니다. GCC(걸프협력회의) 국가들만 해도 연간 439억 달러를 의료기기에 지출하고 있습니다. 라틴아메리카에서는 임상시험 관광이 활성화되고 있으며, 칠레에서는 2023년 33건의 정형외과 의료기기 임상시험이 진행되어 2021년 20건보다 증가하였습니다. 브라질에서는 수입품과 국산 무릎관절 임플란트의 가격 차이를 줄이기 위해 현지 생산에 대한 우대 정책을 시행하고 있으며, 이는 지역 공급업체들의 부상을 촉진하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTH 26.05.29Orthopedic Biomaterials market size in 2026 is estimated at USD 23.92 billion, growing from 2025 value of USD 22.34 billion with 2031 projections showing USD 33.65 billion, growing at 7.06% CAGR over 2026-2031.

Growth stems from a confluence of demographic aging, surging osteoarthritis prevalence, steady sports- and traffic-injury incidence, and rapid technological progress in patient-specific and bioactive implants. Regulatory catalysts such as the U.S. FDA's breakthrough device program shorten launch timelines for novel biomimetic materials , while hospital demand for post-pandemic backlog reduction sustains procedural volumes. Companies leverage additive manufacturing to deliver fit-for-purpose components that reduce revision risk, and sustainability mandates push the supply base toward biodegradable formulations. Persistent supply chain stresses and tighter reimbursement scrutiny temper, but do not derail, the forward trajectory of the orthopedic biomaterials market.

Global Orthopedic Biomaterials Market Trends and Insights

Ageing-Linked Osteoarthritis Burden

Global life expectancy gains intersect with lifestyle factors to lift osteoarthritis prevalence, creating enduring demand for joint reconstruction solutions. Nearly 50% of post-menopausal women are expected to develop the condition by 2045, and knee osteoarthritis cases could rise 75% by 2050 . Parallel growth in revision hip and knee arthroplasty volumes amplifies requirements for durable, wear-resistant biomaterials. Elevated body-mass index contributes to more than 20% of global cases, coupling metabolic stress with mechanical wear and accelerating formulation of high-strength, low-debris polymers that extend implant longevity.

Sports & Road-Injury Up-Trend in Emerging Markets

Urbanization and motorization raise musculoskeletal trauma incidence across many lower-income regions. In Kenyan hospitals, road accidents account for 59.4% of orthopedic admissions, with 85% of victims in the 15-64 age bracket . Comparable patterns in Ghana show vehicular crashes comprising 42% of injuries. Rising elective sports participation also expands reconstruction volumes among younger patients, prompting suppliers to tailor polymer-ceramic composites that balance mechanical resilience with accelerated bone in-growth.

Procedure Down-Coding & Reimbursement Erosion

Payers tighten documentation demands, forcing hospitals to justify every orthopedic indication. Medicare now requires proof of failed conservative care before authorizing total knees, extending pre-operative timelines. Payment bands fluctuate widely; complex trauma reimbursements range from USD 9,496 to USD 50,639 under MS-DRG codes, adding budgeting uncertainty for providers. Device firms must therefore demonstrate cost-offset claims and supply evidence dossiers to maintain coder compliance.

Other drivers and restraints analyzed in the detailed report include:

- 3-D Printed Patient-Specific Implants Adoption

- Rapid FDA Breakthrough Device Designations for Biomimetic Materials

- Post-Implant Infection Litigations Increasing Insurer Scrutiny

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

High-performance polymers generated the largest revenue slice in 2025, reflecting 46.58% share, anchored by strong uptake in acetabular cups and spinal cages. Evonik's VESTAKEEP Fusion illustrates how adding biphasic calcium phosphate turns PEEK bioactive without sacrificing mechanical strength. The orthopedic biomaterials market size for polymers is projected to expand steadily as surface-enhanced variants tackle historical osseointegration limits. Ceramics and bioactive glasses, while smaller today, post a brisk 7.82% CAGR through 2031 as surgeons capitalize on innate osteoconductivity and radiolucency. Hybrid designs that bond polymer cores to ceramic coatings blend load tolerance with bone affinity, marking a shift toward materials that participate in healing rather than merely occupy space.

The metals category faces renewed scrutiny tied to stress shielding and nickel hypersensitivity. Zimmer Biomet's Tivanium alloy targets allergy mitigation with low-nickel chemistry. Niche disruptors such as silicon nitride pursue antibacterial surfaces and thermal stability, with Sintx claiming sole FDA-cleared status for the compound. Calcium-phosphate cements retain hospital favor for moldable bone void fillers, yet ongoing research into controlled-resorption magnesium alloys foreshadows future movement toward fully degradable load-sharing constructs.

Joint reconstruction retained 38.25% revenue in 2025 as hip and knee arthroplasty volumes remained high among aging populations. Nonetheless, orthobiologics outpace all other uses with an 8.03% CAGR, propelled by evidence that bioinductive patches such as Smith+Nephew's REGENETEN cut rotator-cuff re-tear rates 68% versus conventional repair. The orthopedic biomaterials market size attributed to biologics is set to widen as payers warm to regeneration that delays or avoids replacement surgery.

Spinal and trauma fixation implants continue reliable growth thanks to rising high-energy impacts in emerging economies. Viscosupplementation, once confined to mild osteoarthritis, is being repositioned as an adjunct to postpone arthroplasty among active seniors. Convergence arises as hardware manufacturers embed growth factors within plates or nails, creating integrated constructs that stabilize fractures while stimulating callus formation.

The Orthopedic Biomaterials Market Report is Segmented by Material Type (High-Performance Polymers, Ceramics and Bioactive Glasses, and More), Application (Orthobiologics, Joint Reconstruction, and More), Biodegradability (Non-Biodegradable Biomaterials, Biodegradable Biomaterials), Condition (Osteoarthritis, Osteoporosis, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 39.90% of 2025 revenue, anchored by advanced surgical robotics and comprehensive insurance cover. The orthopedic biomaterials market benefits from technology showcases such as the VELYS robotic knee and KINCISE 2 automated hip system that refine component alignment. Yet payer documentation tightening and raw-material supply warnings issued by the FDA underscore profit-margin pressure. Hospital groups increasingly weigh device selection on lifetime value metrics, encouraging vendors to present cost-in-use evidence alongside clinical data.

Asia-Pacific posters an 7.98% CAGR to 2031 on the back of rapid aging and expanding middle-class insurance coverage. Domestic manufacturers scale additive manufacturing labs to cut import reliance, while governments streamline approval pathways for 3-D printed implants. Markets such as India roll out price ceilings to widen access, pushing multinationals to localize production and adjust channel strategies. Country-level diversity remains high, with Japan's mature regulatory oversight contrasting with evolving frameworks in fast-growing Southeast Asian nations.

Europe grows steadily through 2030 as the EU Medical Device Regulation tightens traceability and accelerates eco-design mandates. Hospitals pilot cradle-to-grave tracking of orthopedic components, paving the way for higher biodegradable uptake. Middle East & Africa endorse public-private collaborations to raise theater capacity; the GCC alone spends USD 43.9 billion annually on medical devices. Latin America fosters clinical-trial tourism; Chile hosted 33 orthopedic device studies in 2023, up from 20 in 2021. Local manufacturing incentives in Brazil aim to narrow price gaps between imported and domestic knee implants, supporting regional supplier emergence.

List of Companies Covered in this Report:

- Stryker

- Zimmer Biomet

- Johnson & Johnson

- Smiths Group

- Medtronic

- Globus Medical

- Exactech

- Invibio (Victrex)

- Evonik Industries

- Mitsubishi Chemical Advanced Materials

- Cam Bioceramics

- Kyocera Medical

- BASF Biomaterials

- Heraeus Medical

- Orthofix

- Conmed

- Wright Medical (Stryker)

- NuVasive

- LimaCorporate

- CeramTec

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Ageing?Linked Osteoarthritis Burden

- 4.2.2 Sports & Road-Injury Up-Trend in Emerging Markets

- 4.2.3 3-D Printed Patient-Specific Implants Adoption

- 4.2.4 Rapid FDA Breakthrough Device Designations for Biomimetic Materials

- 4.2.5 Hospital PPP Tenders in LATAM & MENA Favouring Local Biomaterials Sourcing

- 4.2.6 Circular-Economy Push for Bio-Resorbable Materials

- 4.3 Market Restraints

- 4.3.1 Procedure Down-Coding & Reimbursement Erosion

- 4.3.2 Post-Implant Infection Litigations Increasing Insurer Scrutiny

- 4.3.3 Raw-Material Supply Volatility

- 4.3.4 Talent Shortage in Orthobiologic R&D Labs

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porters Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Material Type

- 5.1.1 High-Performance Polymers

- 5.1.2 Ceramics and Bioactive Glasses

- 5.1.3 Calcium-Phosphate Cements

- 5.1.4 Metals and Metal Alloys

- 5.1.5 Others

- 5.2 By Application

- 5.2.1 Orthobiologics

- 5.2.2 Joint Reconstruction

- 5.2.3 Viscosupplementation

- 5.2.4 Spinal and Trauma Fixation Implants

- 5.2.5 Others

- 5.3 By Biodegradability

- 5.3.1 Non-Biodregradable Biomaterials

- 5.3.2 Biodegradable Biomaterials

- 5.4 By Condition

- 5.4.1 Osteoarthritis

- 5.4.2 Osteoporosis

- 5.4.3 Bone Tumors

- 5.4.4 Rheumatoid Arthritis

- 5.4.5 Trauma Management

- 5.4.6 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Stryker

- 6.3.2 Zimmer Biomet

- 6.3.3 Johnson and Johnson

- 6.3.4 Smith & Nephew

- 6.3.5 Medtronic

- 6.3.6 Globus Medical

- 6.3.7 Exactech

- 6.3.8 Invibio (Victrex)

- 6.3.9 Evonik Industries

- 6.3.10 Mitsubishi Chemical Advanced Materials

- 6.3.11 Cam Bioceramics

- 6.3.12 Kyocera Medical

- 6.3.13 BASF Biomaterials

- 6.3.14 Heraeus Medical

- 6.3.15 Orthofix

- 6.3.16 ConMed

- 6.3.17 Wright Medical (Stryker)

- 6.3.18 NuVasive

- 6.3.19 LimaCorporate

- 6.3.20 CeramTec

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment